|

시장보고서

상품코드

2044011

5G 독립형 코어 전환 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)5G Standalone Core Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

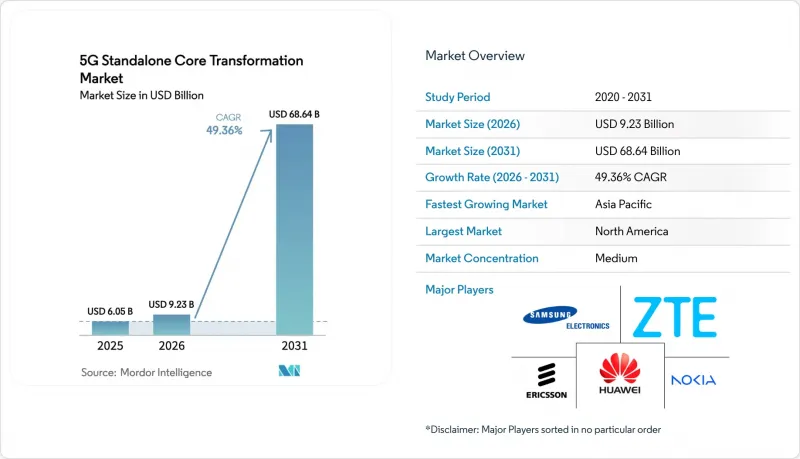

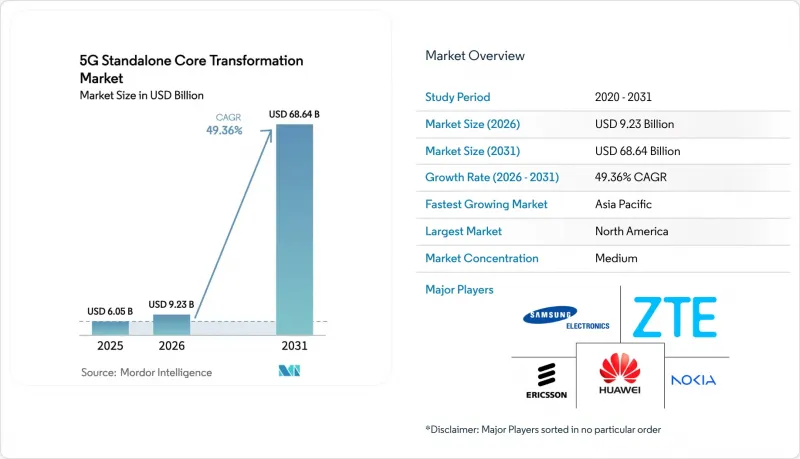

5G 독립형 코어 전환 시장 규모는 2025년 60억 5,000만 달러로 평가되었습니다. 2026년 92억 3,000만 달러로 확대되어 2031년까지 686억 4,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 49.36%를 나타낼 전망입니다.

이러한 급격한 성장의 배경에는 통신사업자들의 비독립형(NSA) 아키텍처로의 전환 증가, 인더스트리 4.0 사이트의 사설망에 대한 투자 확대, 도입 주기를 단축하는 하이퍼스케일러와의 제휴 등이 있습니다. 클라우드 네이티브 설계를 통해 네트워크 슬라이싱, 초저지연, 엣지 컴퓨팅의 수익화를 가능하게 하고, 통신사업자는 중복된 EPC(Evolutionary Packet Core) 리소스를 없애고 시그널링 오버헤드를 줄일 수 있습니다. 미국, 중국, 인도, 유럽연합(EU)의 공공 부문 인센티브는 지방 지역에서의 커버리지 확대를 가속화하고 있습니다. 한편, 3GPP Release 18의 사양은 멀티 벤더 통합을 간소화하고, Tier 2 통신 사업자와 기업이 API 기반 솔루션을 채택하도록 장려하고 있습니다. 동시에 컨테이너화된 네트워크 기능, RedCap 지원 대량 IoT 모듈, AI 지원 슬라이스 오케스트레이션을 통해 소비자 모바일 브로드밴드보다 훨씬 더 많은 수익원을 확보할 수 있으며, 5G 독립형 코어 전환 시장은 지속적인 두 자릿수 성장세를 보이고 있습니다.의 궤도에 오르고 있습니다.

세계의 5G 독립형 코어 전환 시장 동향 및 인사이트

통신 사업자의 NSA에서 SA로의 빠른 전환

통신사업자들은 병행 유지보수가 운영비용을 증가시키고, 초저지연 초신뢰성 통신(URLC), 전용 네트워크 슬라이스와 같은 고급 기능의 도입을 방해하기 때문에 듀얼코어 아키텍처에서 철수하고 있습니다. 2024년부터 2025년까지 Telia, Three UK, MTN South Africa, O2 Telefonica가 상용 전환을 통해 경제적 이점을 입증했으며, Telia는 EPC(Evolution Packet Core) 폐지 후 시그널링 오버헤드가 30% 감소했다고 보고했습니다. 세계 모바일 공급업체 협회(GMSA)의 집계에 따르면, 독립형(SA) 인프라에 투자하는 통신 사업자는 181개사로 전년 대비 140개사 대비 증가했습니다. 이러한 전환은 서비스형 네트워크(Network-as-a-Service, NaaS)의 수익 기회를 창출합니다. 기업들은 NSA(Non Standalone) 환경의 제약으로 인해 실현 불가능한 미션 크리티컬 워크로드를 위해 보장된 네트워크 슬라이스를 임대할 수 있기 때문입니다.

Tier 1 통신사업자의 클라우드 네이티브 컨테이너화 네트워크 기능 도입

Tier 1 통신사들은 수평적 확장 및 다운타임 없는 업그레이드를 위해 핵심 네트워크 플랫폼을 쿠버네티스로 전환하고 있습니다. 구글 클라우드의 에릭슨 온디맨드 코어(On-Demand Core)는 60초 이내에 사용자 플레인 기능을 실행할 수 있으며, 통신사업자가 피크타임에 용량을 10배까지 확장할 수 있게 해줍니다. Three UK는 레드햇 오픈시프트(Red Hat OpenShift)로 오케스트레이션된 9Tbit/s의 코어를 운영하며, 물리적 서버를 40% 절감하면서 3,000만 명의 가입자에게 서비스를 제공합니다. O2 텔레포니카는 프랑크푸르트의 AWS Outposts에 컨트롤 플레인 워크로드를 배치하여 자동차 및 산업 분야 고객의 지연 시간을 단축했습니다. 이러한 사례들은 컨테이너화를 통해 서비스 도입 주기를 단축하고 하드웨어 의존도를 낮출 수 있다는 것을 입증하고 있습니다.

클라우드 네이티브 5G 코어(5GC)로의 전환에 따른 높은 설비투자(CAPEX) 및 기술력 부족

독립형 방식을 도입하기 위해서는 새로운 컴퓨팅 클러스터, 소프트웨어 라이선스, DevOps 파이프라인이 필요하지만, 공인된 Kubernetes 엔지니어는 여전히 부족합니다. 맥킨지는 5G에 대한 총 투자 규모를 4,000억-5,000억 달러로 추산하고 있으며, 이 중 핵심 네트워크 현대화가 최대 5분의 1을 차지할 것으로 예상하고 있습니다. 딜로이트 조사에 따르면, 응답한 통신사업자의 65%가 인력 부족을 가장 큰 병목현상으로 꼽았습니다. 중소 통신사업자가 매니지드 서비스에 의존하게 되면 수익률 압박과 커스터마이징 속도 저하가 우려됩니다.

부문 분석

하드웨어는 2025년 매출의 58.40%를 차지하며, 이는 컨테이너화된 기능을 호스팅하는 데 필요한 x86 또는 ARM 컴퓨트 노드, 100기가비트 스위치, RAN 장비의 초기 구매를 반영했습니다. 5G 독립형 코어 전환 시장에서 하드웨어 시장 규모는 꾸준히 성장할 것으로 예상되지만, 오케스트레이션 인텔리전스로 가치가 이동함에 따라 점유율이 하락할 것으로 예측됩니다. 반면, 소프트웨어 매출은 마이크로서비스 라이선싱, AI를 활용한 라이프사이클 자동화, 지속적 제공에 힘입어 CAGR 52.4%의 견조한 성장세를 보일 것으로 예측됩니다. 에릭슨의 Release 25A나 노키아의 MX Industrial Edge를 도입한 통신사들은 분기별 코드 릴리스가 아닌 매주 기능 제공을 통해 클라우드 네이티브 스택이 가져다주는 속도 우위를 보여주고 있습니다.

서비스 제공업체들은 소프트웨어와 더불어 컨설팅, 통합, 매니지드 오퍼레이션을 세트로 제공하는 경우가 늘고 있습니다. Oracle의 '커뮤니케이션즈 클라우드 네이티브 코어(Communications Cloud Native Core)는 범용 하드웨어 상에서 구동함으로써 보다폰과 텔레포니카의 자본 집약도를 30% 감소시켰습니다. VMware의 'Telco Cloud Platform'은 벤더의 소프트웨어와 하드웨어를 분리하는 Kubernetes 기반을 제공하여 통신사업자가 유리한 어플라이언스 가격을 협상할 수 있도록 지원합니다. 릴리즈 18에서 오픈 API가 표준화됨에 따라 차별화 요소가 커스텀 실리콘에서 소프트웨어 민첩성으로 이동하고, 빠르게 진화하는 컨테이너 에코시스템과 정적인 어플라이언스 환경 간의 성능 격차가 확대되고 있습니다.

지역별 분석

북미는 FCC의 농촌 지역 기금 보조금, NTIA의 Open RAN 보조금, 그리고 2 억 명의 인구를 커버하는 C 밴드의 적극적인 전개로 인해 2025년매출의 40.03%를 창출했습니다. Verizon의 시카고와 댈러스에서 독립형 방식으로의 전환은 산업 자동화를 위한 프리미엄 슬라이싱을 가능하게 하고, AT&T는 2026년 말까지 비독립형 앵커를 폐지할 계획입니다. 캐나다에서는 3.8GHz 대역 주파수 경매가 진행되었고, Rogers, Bell, Telus가 토론토와 밴쿠버에서 코어 네트워크 시범 운영을 시작했습니다. 한편, 멕시코의 텔셀과 AT&T 멕시코는 멕시코시티와 몬테레이에서 시범 운영을 시작했습니다. 탄탄한 자본 시장, 주파수 조기 접근성, 하이퍼스케일 데이터센터와의 근접성 등으로 인해 이 지역은 수익성 리더로 자리매김하고 있습니다.

아시아태평양은 고성장의 원동력이며, 2031년까지 연평균 복합 성장률(CAGR) 59.6%로 확대될 것으로 예측됩니다. 중국의 360만 기지국망과 산업정보화부(MIIT)의 독립형 코어 네트워크 의무화가 8억 9,000만 가입자를 대상으로 한 폭발적인 규모 확대를 뒷받침하고 있습니다. 일본에서는 NTT도코모, KDDI, 소프트뱅크가 전국적으로 전개하고 있으며, 에릭슨, 노키아, 삼성의 장비를 활용하여 자율주행차 및 스마트팩토리 고객에게 서비스를 제공합니다. 한국의 SK텔레콤, KT, LG유플러스는 자동차와 클라우드 게임을 위한 AI 기반 네트워크 슬라이싱에 집중하고 있으며, 인도의 Reliance Jio는 그린필드 독립형 아키텍처로 5,000개 도시를 커버하고 있습니다. 인도의 6GHz 대역 할당과 한국의 5G+ 로드맵을 포함한 지역별 산업 정책은 엣지 대응 코어에 대한 수요를 더욱 촉진하고 있습니다.

유럽은 절대적인 규모에서 북미와 아시아태평양에 비해 뒤쳐져 있지만, EU의 5G 실행 계획에 따라 조정된 주파수 정책의 혜택을 누리고 있습니다. 도이치텔레콤은 아우토반 연선의 자동차 제조업체를 대상으로 프랑크푸르트, 뮌헨, 베를린에서 독립형 코어 네트워크 운영을 시작했습니다. Orange는 파리와 리옹에서 서비스를 시작했고, EE와 Vodafone UK는 런던과 맨체스터에 코어를 구축했습니다. 제재로 인해 러시아 통신사업자들은 서유럽산 장비에 대한 접근이 제한되어 도입이 둔화되고 있지만, Swisscom, Telenor, TIM은 클라우드 네이티브 어플라이언스를 채택함으로써 소규모 시장에서도 빠르게 전환할 수 있다는 것을 보여주고 있습니다. 반면, 남미, 중동 및 아프리카는 아직 초기 단계이지만, 미래 가능성이 높다고 할 수 있습니다. 클라로, TIM, 비보는 상파울루와 리우데자네이루에서 시범운영을 실시하고, 사우디의 STC, UAE의 에티사라트, 남아공의 MTN은 도시지역 기업용 구역을 개설하고, 주파수 경매가 종료되는 2027년까지 커버리지를 확대할 계획입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The 5G Standalone Core Transformation Market size is expected to increase from USD 6.05 billion in 2025 to USD 9.23 billion in 2026 and reach USD 68.64 billion by 2031, growing at a CAGR of 49.36% over 2026-2031. Rising operator migration from non-standalone architectures, expanding private network spend across Industry 4.0 sites, and hyperscaler alliances that shorten deployment cycles underpin this sharp trajectory. Cloud-native design unlocks network slicing, ultra-low latency, and edge-computing monetization, allowing carriers to retire duplicated evolved packet core resources and shrink signaling overhead. Public-sector incentives in the United States, China, India, and the European Union accelerate coverage in rural zones, while 3GPP Release 18 specifications simplify multi-vendor integration, encouraging tier-2 operators and enterprises to adopt API-driven solutions. At the same time, containerized network functions, RedCap-enabled mass-IoT modules, and AI-assisted slice orchestration expand the addressable revenue pool far beyond consumer mobile broadband, positioning the 5G standalone core transformation market for sustained double-digit growth.

Global 5G Standalone Core Transformation Market Trends and Insights

Rapid Migration of Operators From NSA to SA Deployments

Operators are abandoning dual-core architectures because parallel maintenance inflates operating costs and blocks advanced features such as ultra-reliable low-latency communication and dedicated network slices. Commercial cutovers by Telia, Three UK, MTN South Africa, and O2 Telefonica during 2024-2025 validated the economic upside, with Telia reporting a 30% reduction in signaling overhead after decommissioning its evolved packet core. The Global Mobile Suppliers Association counted 181 operators investing in standalone infrastructure, up from 140 a year earlier. This migration unlocks network-as-a-service revenue, as enterprises lease guaranteed slices for mission-critical workloads unattainable under non-standalone constraints.

Cloud-Native, Containerized Network-Function Adoption by Tier-1 CSPs

Tier-1 carriers are re-platforming cores on Kubernetes to gain horizontal scaling and zero-downtime upgrades. Ericsson's On-Demand core on Google Cloud spins up user-plane functions in under 60 seconds, helping operators scale capacity tenfold during peak events. Three UK operates a 9 Tbit/s core orchestrated by Red Hat OpenShift, serving 30 million subscribers with 40% fewer physical servers. O2 Telefonica colocated control-plane workloads on AWS Outposts in Frankfurt, trimming latency for automotive and industrial clients. These proofs confirm that containerization compresses service introduction cycles and reduces hardware intensity.

High CAPEX and Skills Gap for Cloud-Native 5GC Transformation

Standalone adoption demands new compute clusters, software licenses, and DevOps pipelines while certified Kubernetes engineers remain scarce. McKinsey pegged the total 5G spend at USD 400-500 billion, with core modernization accounting for up to one-fifth of that. Deloitte found 65% of surveyed operators cited talent shortages as the primary bottleneck. As smaller carriers turn to managed services, margin compression and slower customization follow.

Other drivers and restraints analyzed in the detailed report include:

- Explosion of Private-5G and Campus Networks Across Industry 4.0 Sites

- AI-Optimized Dynamic Network Slicing Commercial Pilots

- Inter-Operability Issues Across Multi-Vendor Cores and Legacy EPC

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 58.40% of 2025 revenue, reflecting up-front purchases of x86 or ARM compute nodes, 100-gigabit switches, and RAN gear needed to host containerized functions. The 5G standalone core transformation market size for hardware is projected to grow steadily but cede share as value shifts toward orchestration intelligence. In contrast, software revenue is forecast to climb at a robust 52.4% CAGR, propelled by microservice licensing, AI-powered lifecycle automation, and continuous delivery. Operators deploying Ericsson Release 25A and Nokia MX Industrial Edge report weekly feature drops rather than quarterly code releases, demonstrating the speed premium of cloud-native stacks.

Service providers increasingly bundle consulting, integration, and managed operations alongside software. Oracle's Communications Cloud Native Core lowered capital intensity by 30% for Vodafone and Telefonica by running on commodity gear. VMware's Telco Cloud Platform supplies the Kubernetes substrate that decouples vendor software from hardware, allowing carriers to negotiate favorable appliance pricing. As Release 18 hardwires open APIs, differentiation shifts from custom silicon to software agility, widening the performance gap between fast-moving container ecosystems and static appliance estates.

The 5G Standalone Core Transformation Market Report is Segmented by Component (Hardware, Software, and Services), Deployment Model (Public Cloud, Private Cloud, and Hybrid/On-premises), End-User (Telecom Operators, and Enterprises/Private 5G Owners), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.03% of 2025 revenue on the back of FCC rural-fund subsidies, NTIA Open RAN grants, and aggressive C-band rollouts that reached 200 million POPs. Verizon's standalone cutover in Chicago and Dallas opened premium slices for industrial automation, while AT&T plans to decommission non-standalone anchors by late 2026. Canada auctioned 3.8 GHz spectrum and saw Rogers, Bell, and Telus pilot cores in Toronto and Vancouver, whereas Mexico's Telcel and AT&T Mexico began trials in Mexico City and Monterrey. Strong capital markets, early access to spectrum, and proximity to hyperscale data centers position the region as a profitability leader.

Asia-Pacific is the high-growth engine, forecast to expand at a 59.6% CAGR through 2031. China's 3.6 million base-station grid and MIIT mandate for standalone cores underpin explosive scale across 890 million subscribers. Japan's nationwide launch by NTT Docomo, KDDI, and SoftBank leverages Ericsson, Nokia, and Samsung gear to service autonomous-vehicle and smart-factory clients. South Korea's SK Telecom, KT, and LG U+ focus on AI-driven network slicing for automotive and cloud gaming, while India's Reliance Jio covers 5,000 cities on a greenfield standalone architecture. Regional industrial policies, including India's 6 GHz allocation and South Korea's 5G+ roadmap, further lift demand for edge-enabled cores.

Europe trails North America and Asia-Pacific on an absolute scale, but benefits from coordinated spectrum policy under the EU 5G Action Plan. Deutsche Telekom lit standalone cores in Frankfurt, Munich, and Berlin, targeting automotive OEMs along the Autobahn corridors. Orange activated service in Paris and Lyon, and EE and Vodafone UK rolled out cores in London and Manchester. Sanctions limit Russian operator access to Western equipment, slowing adoption, but Swisscom, Telenor, and TIM demonstrate that smaller markets can still transition quickly by adopting cloud-native appliances. Meanwhile, South America and the Middle East, and Africa remain early-stage yet promising. Claro, TIM, and Vivo conducted trials in Sao Paulo and Rio de Janeiro, while STC Saudi Arabia, Etisalat UAE, and MTN South Africa launched urban enterprise zones and plan broader coverage by 2027 as spectrum auctions conclude.

List of Companies Covered in this Report:

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Mavenir Systems, Inc.

- Affirmed Networks, Inc. (now part of Microsoft)

- NEC Corporation (Nippon Electric Company, Limited)

- Hewlett Packard Enterprise Company

- Oracle Corporation

- Athonet S.r.l. (now part of HPE)

- Casa Systems, Inc.

- Cumucore Oy

- Druid Software Limited

- IPLOOK Networks Co., Ltd.

- Parallel Wireless, Inc.

- Rakuten Symphony, Inc.

- VMware, Inc. (now part of Broadcom)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Migration of Operators From NSA to SA Deployments

- 4.2.2 Government-Backed 5G Stimulus Packages and Spectrum Incentives

- 4.2.3 Explosion of Private-5G and Campus Networks Across Industry 4.0 Sites

- 4.2.4 Cloud-Native, Containerised Network-Function Adoption by Tier-1 CSPs

- 4.2.5 AI-Optimised Dynamic Network Slicing Commercial Pilots

- 4.2.6 Emergence of RedCap Devices Unlocking Mass-IoT SA Traffic

- 4.3 Market Restraints

- 4.3.1 High CAPEX and Skills Gap for Cloud-Native 5GC Transformation

- 4.3.2 Inter-Operability Issues Across Multi-Vendor Cores and Legacy EPC

- 4.3.3 Elevated Cyber-Attack Surface in Service-Based Architectures

- 4.3.4 Mid-band Spectrum Fragmentation Slowing SA Coverage Expansion

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid / On-premises

- 5.3 By End-User

- 5.3.1 Telecom Operators

- 5.3.2 Enterprises / Private 5G Owners

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of the Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Huawei Technologies Co., Ltd.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Nokia Corporation

- 6.4.4 ZTE Corporation

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Juniper Networks, Inc.

- 6.4.8 Mavenir Systems, Inc.

- 6.4.9 Affirmed Networks, Inc. (now part of Microsoft)

- 6.4.10 NEC Corporation (Nippon Electric Company, Limited)

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 Oracle Corporation

- 6.4.13 Athonet S.r.l. (now part of HPE)

- 6.4.14 Casa Systems, Inc.

- 6.4.15 Cumucore Oy

- 6.4.16 Druid Software Limited

- 6.4.17 IPLOOK Networks Co., Ltd.

- 6.4.18 Parallel Wireless, Inc.

- 6.4.19 Rakuten Symphony, Inc.

- 6.4.20 VMware, Inc. (now part of Broadcom)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment