|

시장보고서

상품코드

2044029

TaaP(Telco-as-a-Platform) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Telco-as-a-Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

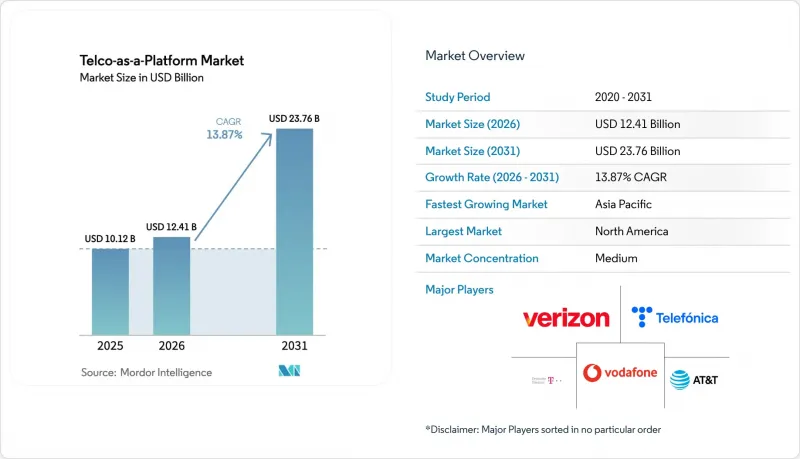

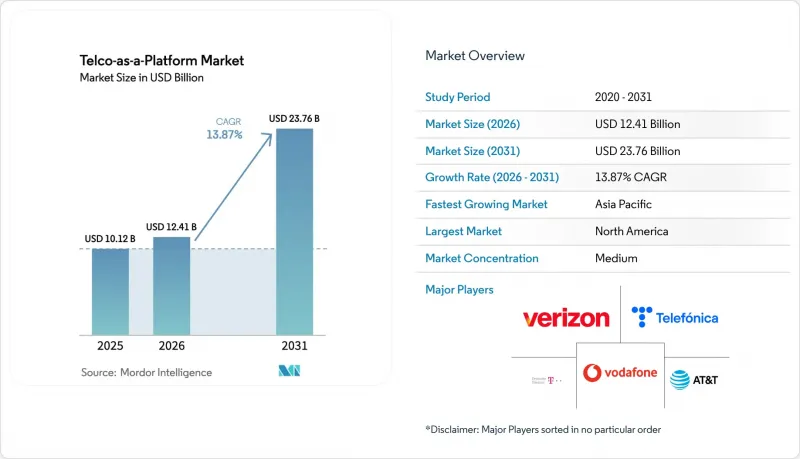

TaaP(Telco-as-a-Platform) 시장 규모는 2025년 101억 2,000만 달러로 평가되었습니다. 2026년 124억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 13.87%를 나타내, 2031년까지 237억 6,000만 달러에 이를 것으로 예측됩니다.

5G 독립형 코어의 도입 확대, 멀티 액세스 엣지 컴퓨팅(MAEC)의 상용화, 네트워크 노출 인터페이스의 표준화로 인해 업계는 순수한 연결 서비스에서 프로그래밍 가능한 플랫폼으로의 전환을 가속화하고 있습니다. 북미, 유럽, 아시아태평양의 통신사들은 현재 통합 API를 통해 온디맨드 품질, 기기 위치 정보, SIM 스왑 감지 기능을 제공하고 있으며, 이를 통해 기업 및 소프트웨어 개발자의 통합 비용을 절감하고 있습니다. 하이퍼스케일러와의 제휴를 통해 무선 기지국 내에 클라우드 컴퓨팅이 도입되면서 통신사는 단순한 대역폭 도매업체가 아닌 엣지 클라우드의 오케스트레이터로 자리매김하고 있습니다. 동시에 유럽, 중국, 인도 및 걸프 지역 국가들의 데이터 주권 규제로 인해 로컬 처리가 요구되고 있으며, 컴플라이언스와 확장성의 균형을 맞추는 하이브리드 플랫폼 아키텍처에 대한 요구가 증가하고 있습니다. 클라우드 제공업체, CPaaS 전문 기업 및 신규 시장 진출기업들이 여전히 구독형 BSS 및 OSS 스택에 의존하는 레거시 사업자에게 도전장을 내밀면서 경쟁의 압력이 높아지고 있습니다.

세계의 TaaP(Telco-as-a-Platform) 시장 동향과 인사이트

5G 독립형 코어의 보급으로 네트워크 노출이 가능해졌습니다.

SA(Standalone) 코어는 네트워크 노출 기능(Network Exposure Functions)을 도입하여 써드파티 소프트웨어가 안전한 노스바운드 API를 통해 서비스 품질(QoS) 조정, 위치 보증, 세션 관리 등을 수행할 수 있도록 합니다. 세션 관리를 수행할 수 있도록 합니다. 차이나모바일은 2025년 말까지 5G SA 무선 기지국 100만 대를 돌파하고, 북미 통신사들도 주요 도시 지역에서 SA 코어를 가동하여 실시간 네트워크 슬라이싱을 상용화할 수 있게 되었습니다. 3GPP 릴리즈 16과 17에서 기본 인터페이스를 정의했고, GSMA Open Gateway와 Linux Foundation의 CAMARA 프로젝트는 이를 개발자를 위한 REST API로 매핑했습니다. 이를 통해 소프트웨어 팀은 한 번의 호출로 여러 캐리어에 걸친 확정 지연을 요청할 수 있게 되었습니다. 통신사들은 현재 획일적인 접속 서비스가 아닌 대역폭과 지연의 계층화를 통한 차별화로 수익화를 꾀하고 있으며, 2028년까지 전 세계 5G 회선의 대다수가 SA방식으로 전환됨에 따라 지속적인 수익원이 개척되고 있습니다.

임베디드 커넥티비티 및 API 액세스에 대한 기업 수요 증가

은행은 계정 탈취 사기를 방지하기 위해 SIM 스왑 및 번호 확인 호출을 내장하고 있으며, 병원에서는 10밀리초 이상의 지터를 허용하지 않는 원격 진단을 위해 네트워크 슬라이스를 확보하고 있습니다. 제조업체는 엣지 컴퓨팅과 결합된 프라이빗 5G를 통해 로봇을 제어하고 API를 사용하여 교대 근무 시 대역폭을 스케줄링하고 있습니다. T-Mobile이 2025년에 출시한 T-Platform은 물류 기업이 슬라이스 및 IoT 연결을 자동으로 프로비저닝할 수 있는 셀프 서비스형 마켓플레이스를 제공하여 몇 주씩 걸리던 조달 주기를 없앴다. 단순화된 종량제 모델은 통신 전문 지식이 없는 중소기업을 끌어들여 포춘지 선정 500대 다국적 기업 외의 수익원을 확장하고 있습니다.

API 수익화를 가로막는 레거시 IT 및 BSS/OSS의 제약

월 단위 과금 엔진에서는 API 호출을 초 단위로 측정하거나, 레이턴시 클래스에 연동된 동적 가격 설정을 지원할 수 없습니다. Oracle과 Amdocs는 클라우드 네이티브 과금 스택을 출시했지만, 수백만 명의 가입자를 전환하는 것은 통신 사업자에게 해약 위험과 수익 보장에 대한 공백을 초래할 수 있습니다. TM 포럼의 '오픈 디지털 아키텍처' 청사진이 재구축의 지침이 되고 있지만, 2025년까지 파일럿 단계를 벗어난 사업자는 극히 일부에 불과합니다. 실시간 정책 제어가 없다면, 많은 통신사들은 획일적인 번들만 제공하게 되고, 하이퍼스케일러와의 차별성을 잃게 됩니다.

부문 분석

CPaaS는 2025년 32.45%의 점유율을 유지했으며, 프로토콜을 간단한 REST 호출로 추상화하는 메시징 선구자 기업이 주도했습니다. 엣지 클라우드 플랫폼은 현재 15.12%의 연평균 복합 성장률(CAGR)로 가장 높은 성장세를 기록하고 있으며, 기업들은 백홀을 피하기 위해 무선 기지국 내에 마이크로 서비스를 배치하고 있습니다. Verizon 5G Edge는 미국 내 50개 이상의 대도시 지역에서 사용자로부터 10밀리초 이내의 거리에서 컴퓨팅을 제공하고, 공장에서 실시간으로 이상 징후를 감지할 수 있도록 지원합니다. GSMA Open Gateway의 8개의 API 제품군 통합은 통신 및 컴퓨팅을 연결하는 네트워크 노출 마켓플레이스를 추가합니다.

이러한 변화는 수익 모델도 재구성하고 있습니다. CPaaS가 메시지 단위, 분 단위로 이용료를 부과하는 반면, 엣지 플랫폼은 CPU 사이클, 스토리지, 보장된 대역폭에 대해 요금을 부과합니다. 엣지 클라우드의 하위 부문인 Telco-as-a-Platform 시장 규모는 예측 기간이 끝날 때까지 큰 점유율을 차지할 것으로 예상되며, 이는 자율주행차, 컴퓨터 비전, 몰입형 미디어의 현장 분석에 대한 수요를 반영하고 있습니다. BSS/OSS-as-a-Service 솔루션은 On-Premise 재구축보다 과금 및 카탈로그 기능의 아웃소싱을 선호하는 지역 통신사업자를 끌어들여 진입 비용 곡선을 평탄하게 만들고 있습니다.

퍼블릭 클라우드는 2025년 매출에서 여전히 56.43%를 차지했지만, EU, 중국, 중동 일부 지역의 엄격한 현지화 규제로 인해 하이브리드 아키텍처가 CAGR 14.03%로 성장하고 있습니다. Deutsche Telekom과 Google Cloud는 키와 메타데이터를 독일 국내에만 저장하는 'Sovereign Cloud' 스택을 출시하여 하이퍼스케일 혁신과 규제적 보장을 결합했습니다. 기업들은 지연 시간이 중요한 패킷을 엣지 거점으로 라우팅하고, 배치 분석을 중앙 지역으로 전송함으로써 비용과 컴플라이언스를 동시에 최적화할 수 있습니다.

프라이빗한 영역은 규제가 엄격한 BFSI(은행, 금융, 보험) 및 헬스케어 분야에 국한된 틈새 영역에 머물러 있습니다. 그러나 이러한 수직적 시장에서도 현재 On-Premise 클러스터와 통신사 엣지 전체에 걸쳐 정책을 통합하는 페더레이션 오케스트레이션 계층에 의존하고 있습니다. '디지털 시장법'은 지배적 클라우드 사업자에게 상호운용성 지원을 의무화하여 통신사업자의 협상력을 강화하고 있습니다. 중국이나 인도에서는 사이버 보안법에 따라 개인 데이터의 국경 간 전송이 금지되어 있어, 익명화된 API를 통해서만 퍼블릭 클라우드와 상호 연결되는 국내 에지 그리드를 장려하고 있습니다.

지역별 분석

북미는 2025년 매출의 28.54%를 차지했으며, 초기 5G SA(독립형) 도입과 클라우드-엣지 간 파트너십이 이를 뒷받침하고 있습니다. Verizon 5G Edge는 AWS Wavelength와 연계하여 75개 도시 지역에 구축되어 있으며, 이를 통해 EC 기업은 고객과 10밀리초 이내의 거리에서 추천 엔진을 가동할 수 있습니다. 한편, AT&T Network Edge는 100개 이상의 도시에서 Azure의 컴퓨팅 기능을 통합하고 있습니다. T-Mobile의 마켓플레이스는 중소기업의 도입을 가속화하고 있습니다. 연방통신위원회(FCC)는 Open RAN의 다양성을 권장하고 있지만, 각 주마다 프라이버시 법이 다르기 때문에 여러 주에 걸쳐 전개하는 것은 복잡합니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 14.97%로 가장 높은 성장이 예상됩니다. 차이나모바일의 광범위한 SA 네트워크는 산업단지에 대한 전국적인 커버리지를 제공하며, 버티 에어텔의 마켓플레이스는 인도 스타트업 생태계에 번호 인증 및 IoT 연결에 대한 접근을 가능하게 합니다. NTT도코모는 자율주행차 시험 운행을 위한 네트워크 슬라이싱을 상용화했습니다. 또한, 싱가텔은 AWS와 협력하여 싱가포르를 국경을 초월한 엣지 서비스 허브로 자리매김하고 있습니다. 규제 환경은 중국의 엄격한 현지화부터 싱가포르의 오픈 데이터 회랑에 이르기까지 다양하며, 플랫폼의 설계와 가격 설정에 영향을 미치고 있습니다.

유럽에서는 '디지털 시장법', 'GDPR(EU 개인정보보호규정)' 등 오픈 액세스와 프라이버시 준수를 의무화하는 통일된 정책의 혜택을 누리고 있습니다. 도이치텔레콤, 오렌지, 텔레포니카는 데이터 거주 규정을 충족하면서 설비 투자를 분담하는 페더레이션 엣지(Federated Edge)를 시범 운영하고 있습니다. 보더폰의 API 마켓플레이스는 21개국에 걸쳐 부정행위 방지 및 IoT 번들 수익화를 실현하고 있습니다. 중동의 통신 사업자들은 사우디와 UAE의 정부 워크로드 호스팅을 위해 소버린 클라우드의 특혜를 활용하고 있습니다. 한편, 아프리카 통신사들은 4G 커버리지가 확대되는 가운데 스마트 농업용 IoT에 집중하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Telco-as-a-Platform Market size is expected to grow from USD 10.12 billion in 2025 to USD 12.41 billion in 2026 and is forecast to reach USD 23.76 billion by 2031 at 13.87% CAGR over 2026-2031.

The growing deployment of 5G standalone cores, the commercialization of multi-access edge computing, and the standardization of network exposure interfaces are accelerating the industry's pivot from pure connectivity to programmable platforms. Operators in North America, Europe, and Asia-Pacific now expose quality-on-demand, device-location, and SIM-swap detection capabilities through unified APIs, reducing integration costs for enterprises and software developers. Partnerships with hyperscalers place cloud compute inside radio sites, positioning telcos as edge-cloud orchestrators rather than bandwidth wholesalers. At the same time, data-sovereignty regulations in Europe, China, India, and the Gulf states require localized processing, creating demand for hybrid platform architectures that balance compliance with scalability. Competitive pressure intensifies as cloud providers, CPaaS specialists, and greenfield operators challenge legacy carriers that still rely on subscription-oriented BSS and OSS stacks.

Global Telco-as-a-Platform Market Trends and Insights

Proliferation of 5G Standalone Core Enabling Network Exposure

Standalone cores introduce Network Exposure Functions that allow third-party software to invoke quality-of-service tuning, location assurance, and session management through secure northbound APIs. China Mobile surpassed 1 million 5G SA radios by late 2025, and North American operators activated SA cores in major metros, making real-time network slicing commercially viable. 3GPP Releases 16 and 17 defined the underlying interfaces, and the GSMA Open Gateway, along with the Linux Foundation CAMARA project, mapped them to a developer-friendly REST API, giving software teams a single call to request deterministic latency across multiple carriers. Operators now monetize differentiated bandwidth and latency tiers rather than flat connectivity, opening up recurring revenue streams as SA penetration scales toward a majority of global 5G lines before 2028.

Rising Enterprise Demand for Embedded Connectivity and API Access

Banks embed SIM-swap and number-verification calls to stop account-takeover fraud, while hospitals reserve network slices for remote diagnostics that cannot tolerate jitter exceeding 10 milliseconds. Manufacturers orchestrate robotics over private 5G combined with edge compute, using APIs to schedule bandwidth during shift changes. T-Mobile's 2025 launch of T-Platform offered a self-service marketplace where logistics firms automatically provision slices and IoT connections, removing procurement cycles that once took weeks. Simplified pay-as-you-go models attract SMEs that lack telecom expertise, broadening the revenue pool beyond Fortune 500 multinationals.

Legacy IT and BSS/OSS Constraints Hindering API Monetization

Monthly billing engines cannot meter per-second API calls or support dynamic pricing tied to latency classes. Oracle and Amdocs released cloud-native charging stacks, yet migrating millions of subscribers exposes carriers to churn risk and revenue assurance gaps. TM Forum's Open Digital Architecture blueprint guides the rebuild, but only a small subset of operators moved beyond the pilot stage by 2025. Without real-time policy control, many carriers offer only blunt bundles, undermining differentiation from hyperscalers.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Revenue Diversification Beyond Connectivity Services

- MEC Adoption Driving Low-Latency Application Ecosystem

- Fragmented Standards for Network-Exposure APIs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CPaaS maintained a 32.45% share in 2025, led by messaging pioneers that abstract protocols into simple REST calls. Edge Cloud Platform now records the highest trajectory, with a 15.12% CAGR, as enterprises deploy microservices within radio sites to avoid backhaul. Verizon 5G Edge provides compute within 10 milliseconds of users across more than 50 U.S. metros, enabling factories to detect anomalies in real time. GSMA Open Gateway's alignment of eight API families adds network exposure marketplaces that bond communications with compute.

The shift also reshapes revenue models. While CPaaS charges usage fees per message or per minute, edge platforms charge for CPU cycles, storage, and guaranteed bandwidth. The Telco-as-a-Platform market size for the Edge Cloud subsegment is projected to capture a larger share by the end of the forecast window, reflecting demand for in-situ analytics across autonomous vehicles, computer vision, and immersive media. BSS/OSS-as-a-Service solutions attract regional carriers that prefer to outsource charging and catalog functions rather than rebuild on premises, flattening the cost curve for entry.

Public cloud still accounted for 56.43% of 2025 revenue, but strict localization rules in the EU, China, and parts of the Middle East are driving hybrid architectures at a 14.03% CAGR. Deutsche Telekom and Google Cloud launched a Sovereign Cloud stack that stores keys and metadata only inside German borders, blending hyperscale innovation with regulatory assurance. Enterprises route latency-critical packets to edge locations while forwarding batch analytics to central regions, optimizing cost and compliance simultaneously.

Private deployments remain a niche confined to heavily regulated BFSI and healthcare domains. Yet even these verticals now rely on federated orchestration layers that unify policy across on-premise clusters and telco edges. The Digital Markets Act obliges dominant cloud providers to support interoperability, strengthening carrier bargaining power. In China and India, cybersecurity laws prohibit cross-border transfer of personal data, fueling domestic edge grids that interconnect with public clouds only through anonymized APIs.

The Telco-As-A-Platform Market Report is Segmented by Platform Type (CPaaS, Network Exposure Platform, and More), Deployment Model (Public Cloud, Private Cloud, and More), Network Technology (4G/LTE, NB-IoT and LPWAN, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Manufacturing, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 28.54% of 2025 revenue, underpinned by early 5G SA launches and cloud-edge partnerships. Verizon 5G Edge, coupled with AWS Wavelength, spans 75 metro zones, allowing e-commerce firms to run recommendation engines within ten milliseconds of customers, while AT&T Network Edge embeds Azure compute in more than 100 cities. T-Mobile's marketplace accelerates SME adoption. Although the Federal Communications Commission encourages Open RAN diversity, divergent state privacy laws complicate multi-state deployments.

Asia-Pacific posts the highest forecast growth at 14.97% CAGR through 2031. China Mobile's extensive SA footprint provides nationwide coverage for industrial parks, while Bharti Airtel's marketplace makes number-verification and IoT connectivity accessible to India's start-up ecosystem. NTT DOCOMO commercialized network slicing for autonomous vehicle trials, and Singtel, with AWS, positions Singapore as a hub for cross-border edge services. Regulatory climates vary, from China's strict localization to Singapore's open data corridors, shaping platform design and pricing.

Europe benefits from unified policies, such as the Digital Markets Act and the GDPR, that mandate open access and privacy compliance. Deutsche Telekom, Orange, and Telefonica pilot federated edges that share capex while meeting data-residency rules. Vodafone's API marketplace spans 21 countries and monetizes fraud-prevention and IoT bundles. Middle East carriers leverage sovereign-cloud incentives to host government workloads in Saudi Arabia and the UAE, while African operators focus on smart-agriculture IoT as 4G coverage widens.

- Vodafone Group Plc

- Deutsche Telekom AG

- Telefonica, S.A.

- AT&T Inc.

- Verizon Communications Inc.

- Orange S.A.

- China Mobile Limited

- China Telecom Corporation Limited

- NTT DOCOMO, Inc.

- Singapore Telecommunications Limited

- Rakuten Symphony, Inc.

- Telstra Group Limited

- T-Mobile US, Inc.

- BT Group plc

- KDDI Corporation

- Swisscom AG

- Dish Network Corporation

- Ericsson AB

- Bharti Airtel Limited

- Rogers Communications Inc.

- Telenor ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Standalone Core Enabling Network Exposure

- 4.2.2 Rising Enterprise Demand for Embedded Connectivity and API Access

- 4.2.3 Shift Toward Revenue Diversification Beyond Connectivity Services

- 4.2.4 MEC Adoption Driving Low-Latency Application Ecosystem

- 4.2.5 Regulatory Push for Open Networks And Fair Access

- 4.2.6 Edge-Native AI Workloads Requiring Telecom-Grade Platforms

- 4.3 Market Restraints

- 4.3.1 Legacy IT and BSS/OSS Constraints Hindering API Monetization

- 4.3.2 Fragmented Standards for Network Exposure APIs

- 4.3.3 Security and Data Sovereignty Concerns Among Enterprises

- 4.3.4 Uncertain ROI for Telcos Investing in Platform Capabilities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 CPaaS

- 5.1.2 Network Exposure Platform (API Marketplace)

- 5.1.3 Edge Cloud Platform

- 5.1.4 BSS/OSS-as-a-Service

- 5.1.5 Other Platform Types (IoT Connectivity Platform)

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Network Technology

- 5.3.1 4G/LTE

- 5.3.2 5G Non-Standalone (NSA)

- 5.3.3 5G Stand-Alone (SA)

- 5.3.4 NB-IoT and LPWAN

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 Manufacturing

- 5.5.2 Automotive and Transportation

- 5.5.3 Media and Entertainment

- 5.5.4 Healthcare

- 5.5.5 Energy and Utilities

- 5.5.6 BFSI

- 5.5.7 Retail and E-Commerce

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Vodafone Group Plc

- 6.4.2 Deutsche Telekom AG

- 6.4.3 Telefonica, S.A.

- 6.4.4 AT&T Inc.

- 6.4.5 Verizon Communications Inc.

- 6.4.6 Orange S.A.

- 6.4.7 China Mobile Limited

- 6.4.8 China Telecom Corporation Limited

- 6.4.9 NTT DOCOMO, Inc.

- 6.4.10 Singapore Telecommunications Limited

- 6.4.11 Rakuten Symphony, Inc.

- 6.4.12 Telstra Group Limited

- 6.4.13 T-Mobile US, Inc.

- 6.4.14 BT Group plc

- 6.4.15 KDDI Corporation

- 6.4.16 Swisscom AG

- 6.4.17 Dish Network Corporation

- 6.4.18 Ericsson AB

- 6.4.19 Bharti Airtel Limited

- 6.4.20 Rogers Communications Inc.

- 6.4.21 Telenor ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions