|

시장보고서

상품코드

2044037

LED 기판용 사파이어 크리스탈 성장 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

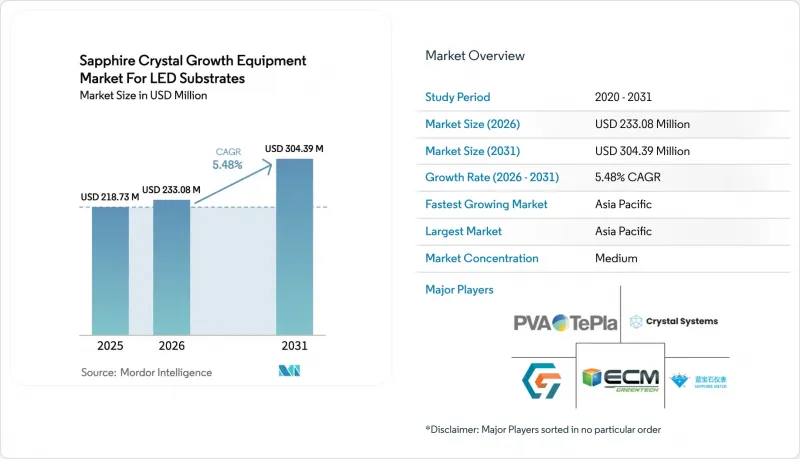

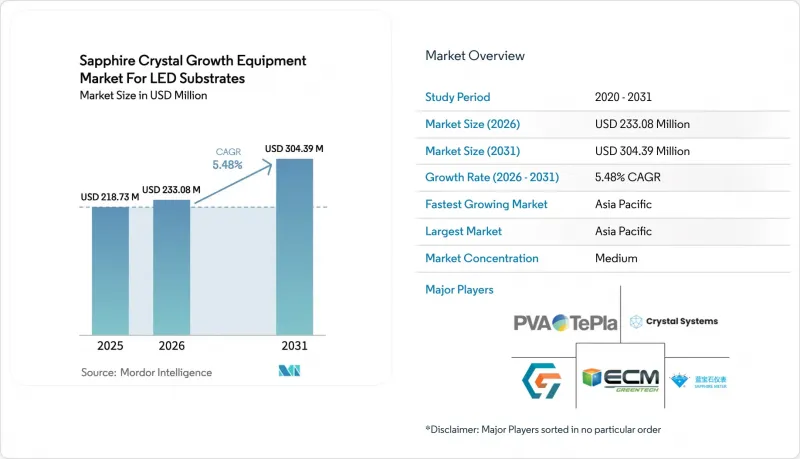

LED 기판용 사파이어 크리스탈 성장 장비 시장 규모는 2025년에 2억 1,873만 달러로 평가되었습니다. 2026년 2억 3,308만 달러에 이르며, 예측 기간(2026-2031년) CAGR 5.48%를 나타내, 2031년에는 3억 439만 달러에 이를 전망입니다.

북미와 유럽의 일반 조명 수요 둔화는 미니 LED 백라이트, 자동차 헤드업 디스플레이, 증강현실(AR) 기기의 사양 요구 사항 증가와 맞물려 있습니다. 2024-2025년 세계 사파이어 웨이퍼 생산능력 증설에서 중국 에피택시 파운드리가 약 60%를 차지했지만, 최근 중국의 에피택시 파운드리의 설비투자는 대구경 부울과 고도의 자동화에 편중되어 있어 기존 4인치 라인의 수주 사이클을 압박하고 있습니다. 유럽과 미국의 용광로 업체들은 특허받은 열장 설계를 활용하여 300mm 이상 시스템에서 점유율을 지키고 있는 반면, 중국 경쟁사들은 가격 경쟁력과 현지화된 서비스를 통해 150-300mm 부문에서 성장세를 보이고 있습니다. 프리미엄 디스플레이의 보급과 미국 에너지부 및 유럽연합의 에코 디자인 지침에 따른 지속적인 LED 개조 의무화와의 상호작용이 예상 성장 곡선이 현재 한 자릿수 중반의 기준선을 넘어 가속화될지 여부를 결정하게 될 것입니다.

LED 기판용 사파이어 크리스탈 성장 장비 시장 동향과 전망

중국 에피택시 파운더리의 공격적인 생산능력 확대 추진

중국의 LED 칩 제조업체는 2024년부터 2025년까지 150개 이상의 새로운 MOCVD 원자로를 가동했습니다. 그 선두에는 산안광전(San'an Optoelectronics)과 HC SemiTek이 있으며, 후자의 28억 위안(3억 9,200만 달러)을 투자한 양저우 프로젝트는 미니 LED 및 마이크로 LED용 기판을 목표로 하고 있습니다. 이러한 움직임은 단기적으로 6인치 및 8인치 사파이어 웨이퍼에 대한 수요를 급증시켰지만, 그릇당 처리량을 최적화하는 150-300mm 및 300mm 이상의 용광로로의 조달 전환을 가져왔습니다. 국무원에서 화합물 반도체 인프라를 위해 500억 위안(70억 달러)의 자금을 지원하면서 설비 확충에 힘을 실어주고 있습니다. 그러나 2025년 1분기 웨이퍼 평균 판매 가격이 전년 동기 대비 12% 하락함에 따라, 구매자는 사이클 타임을 단축하는 자동화를 우선순위에 둘 수밖에 없는 상황입니다. 그 결과, 설비 교체 주기가 빨라지고, AI를 활용한 공정 제어 패키지의 도입률이 증가하고 있으며, 용광로 하드웨어와 예측 분석을 결합할 수 있는 공급업체가 혜택을 보고 있습니다.

하이엔드 TV의 미니 LED 백라이트 채택 급증

고급 TV 제조업체들은 2024년에 약 800만 대의 미니 LED TV를 출하했으며, 2023년 대비 35% 증가했습니다. Samsung Electronics와 LG디스플레이는 파주 및 기타 거점에서 패널 생산 능력을 확대되고 있습니다. 각 미니 LED 어레이는 수천 개의 발광 칩의 빈 매칭을 실현하기 위해 고품질 사파이어 기판에 의존하고 불순물 허용치를 1ppm 미만으로 엄격하게 제한합니다. 자동차 헤드업 디스플레이와 신흥 AR 글래스에서도 유사한 아키텍처가 검토되고 있으며, 결함 없는 결정 덩어리에 대한 수요가 더욱 증가하고 있습니다. 장비 OEM 업체들은 현재 구식 카이로프로스법 라인에서는 고비용의 개조 또는 변위 밀도가 낮은 초크랄스키법 장비로 완전히 교체하지 않으면 충족할 수 없는 고객 사양에 직면해 있습니다. 이러한 프리미엄 요구사항은 퍼니스 당 평균 판매가격(ASP)을 높이는 한편, 소모품 및 소프트웨어 업그레이드를 통한 라이프사이클 수익 확보로 이어집니다.

SiC 용광로 라인에 비해 높은 설비 투자 요구 사항

턴키 방식의 200mm 사파이어 생산 라인은 800만-1,200만 달러의 비용이 소요되며, 같은 규모의 실리콘 카바이드(SiC) 승화법 설비의 경우 500만-700만 달러의 비용이 소요됩니다. 반면, SiC 웨이퍼의 판매가격은 30-40% 더 비쌉니다. 정부의 인센티브, 특히 미국의 CHIPS 법은 SiC 및 기타 와이드 밴드갭 재료를 불균형적으로 우대하여 투자를 더욱 분산시키고 있습니다. 현재 LED 평균판매가격(ASP)으로는 사파이어 제조 장비의 투자 회수 기간이 4-5년에 달하고, 보다 빠른 수익을 원하는 벤처 캐피탈의 신규 진출기업에게는 장벽이 되고 있습니다. 각 벤더들은 장비의 구독형 제공과 성과 연동형 가격 책정을 통해 고가의 초기 비용 부담을 줄이고 있지만, 자금 조달의 제약으로 인해 중견 팹에서의 도입은 여전히 지연되고 있습니다.

부문 분석

결정 성장로는 2025년 지출의 69.87%를 차지하여 LED 기판용 사파이어 크리스탈 성장 장비 시장에서 결정 성장로의 중심적인 역할을 강조했습니다. 그러나 현재 파운드리 업체들은 용광로와 소프트웨어 중심의 공정 제어 패키지를 세트로 판매하는 경향이 강해지고 있으며, 2024년에는 자동화 도입률이 42%를 나타냈습니다. LED 기판용 사파이어 크리스탈 성장 장비 시장에서 자동화 및 공정 제어 시스템 시장 점유율은 임금 인플레이션과 디스플레이 사양의 강화로 인해 2031년까지 연평균 복합 성장률(CAGR) 6.13%로 가장 빠르게 성장할 것으로 예측됩니다. 유럽과 미국 OEM 업체들은 AI를 활용한 열장 최적화로 차별화를 꾀하는 반면, 중국 업체들은 고처리량 팹을 기반으로 한 총소유비용(TCO) 보장으로 경쟁하고 있습니다.

장비의 갱신 주기는 평균 8-10년이지만, 300mm로의 전환으로 감가상각 기간이 단축되어 아직 사용 가능한 6인치 장비의 감가상각이 불가피한 상황입니다. 한편, 자동화 플랫폼은 3-5년의 짧은 업데이트 주기를 특징으로 하며, 이를 통해 지속적인 수익원을 창출하고 용광로 주문 변동으로부터 공급업체를 보호합니다. 흑연 도가니, 고순도 알루미나와 같은 소모품은 고객을 OEM 생태계에 더욱 묶어두어 경쟁 우위를 하드웨어 가격에서 토탈 솔루션의 성능으로 점차 이동시키고 있습니다.

'LED 기판용 사파이어 크리스탈 성장 장비 시장' 산업 보고서는 장비 유형(결정 성장로, 열장 및 도가니 시스템 등), 성장 기술(카이로프로스법, 엣지 정의 필름 공급 성장법, 열교환기법 등), 사파이어 직경 대응 능력(150mm 이하, 150-300mm, 300mm 이상), 지역별로 구분하여 조사하였습니다. 및 지역별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

지역별 분석

아시아태평양은 2025년 LED 기판용 사파이어 크리스탈 성장 장비 시장 규모의 72.68%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 5.72%를 나타낼 것으로 예측됩니다. 중국은 전 세계 웨이퍼 생산량의 약 55%를 차지하고 있으며, 이는 용광로 감가상각을 상쇄하는 지방정부의 보조금에 힘입은 바 큽니다. 대만은 고수익률의 미니 LED 기판을 전문적으로 생산하고 있으며, 한국의 삼성디스플레이와 LG디스플레이는 미니 LED TV의 생산능력을 빠르게 확장하고 있어 간접적으로 사파이어 기판 수요를 증가시키고 있습니다. 일본의 기존 LED 기업들은 설비투자를 SiC와 GaN으로 전환하고 있지만, 니치아 화학공업과 도요타 합성 수요로 인해 국내의 틈새 장비 시장은 여전히 유지되고 있습니다.

북미와 유럽은 2025년 매출의 약 18%를 차지했지만, LED 칩 제조 기지 부족과 파워일렉트로닉스에 편향된 보조금 프로그램 등으로 인해 제약이 있습니다. 미국 'CHIPS and Science Act'에서 사파이어에 대한 자금 배분은 극히 일부에 불과하며, Wolfspeed의 SiC로의 전략적 전환으로 인해 역사적으로 주요 구매자였던 기업이 시장에서 철수했습니다. 유럽의 '칩스법'도 마찬가지로 첨단 로직과 SiC에 중점을 두고 있으며, 사파이어 수요는 단결정과 같은 전문 업체에 맡겨져 있습니다. 그러나 이 회사의 EU향 선적은 제재와 관련된 마찰에 직면해 있습니다. 규제는 여전히 LED의 채택을 촉진하고 있지만, 그 결과 발생하는 기판 주문은 주로 아시아 파운드리에 집중되어 있습니다.

'기타 지역'은 2025년 매출의 10% 미만을 차지했지만, 사우디아라비아, UAE, 브라질의 인프라 전기화로 인해 이 지역은 더욱 성장할 것으로 예측됩니다. 인도의 100억 달러 규모의 '반도체 미션'은 2028년부터 2030년까지 시장 맵를 바꿀 수 있지만, 2026년 3월 사파이어용 장비 수주는 확인되지 않고 있습니다. 특히 남아시아 각국 정부가 현지 조달 인센티브를 검토함에 따라 장비 제조업체들은 잠재적인 국내 조달 요건을 충족시키기 위해 합작 조립 모델을 검토하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe sapphire crystal growth equipment market for LED substrates market size was valued at USD 218.73 million in 2025, USD 233.08 million in 2026, and reach USD 304.39 million by 2031, at a CAGR of 5.48% during the forecast period (2026-2031).

Moderating general-illumination demand in North America and Europe coincides with rising specification pressure from mini-LED backlighting, automotive head-up displays and augmented-reality devices. Chinese epitaxy foundries accounted for roughly 60% of global sapphire wafer capacity additions between 2024 and 2025, yet their recent equipment spend skews toward larger-diameter boules and advanced automation, compressing order cycles for legacy 4-inch lines. Western furnace vendors defend share in above-300 mm systems by leveraging patented thermal-field designs, while Chinese peers gain traction in the 150-300 mm segment through price leadership and localized service. The interplay between premium display uptake and continued LED retrofit mandates under the U.S. Department of Energy and European Union Ecodesign directive will determine whether the projected growth curve accelerates beyond today's mid-single-digit baseline.

Insights and Trends of Sapphire Crystal Growth Equipment Market For LED Substrates

Aggressive Capacity Expansion by Chinese Epitaxy Foundries

Chinese LED chipmakers commissioned more than 150 new MOCVD reactors during 2024-2025, spearheaded by San'an Optoelectronics and HC SemiTek, whose CNY 2.8 billion (USD 392 million) Yangzhou project targets mini-LED and micro-LED substrates. This uptick triggered a near-term spike in demand for 6-inch and 8-inch sapphire wafers, yet it also realigned procurement toward 150-300 mm and above-300 mm furnaces that optimize throughput per boule. State Council funding of CNY 50 billion (USD 7 billion) for compound-semiconductor infrastructure reinforces the build-out, although wafer ASPs slipped 12% year-on-year in Q1 2025, compelling buyers to prioritize automation that compresses cycle time. The net effect raises installed base turnover and lifts attach rates for AI-driven process-control packages, benefiting suppliers able to combine furnace hardware with predictive analytics.

Surging Mini-LED Backlighting Adoption in High-End TVs

Premium television manufacturers shipped roughly 8 million mini-LED sets in 2024, a 35% jump over 2023, with Samsung Electronics and LG Display expanding panel capacity at Paju and other hubs. Each mini-LED array relies on a higher-quality sapphire substrate to achieve bin-matching for thousands of emissive chips, tightening impurity tolerances to sub-1 ppm. Automotive head-up displays and emerging AR glasses evaluate similar architectures, further lifting demand for defect-free boules. Equipment OEMs now face customer specifications that older Kyropoulos lines can meet only via costly retrofits or complete replacement with Czochralski tools that deliver lower dislocation densities. These premium requirements raise per-furnace ASPs but also lock in higher lifecycle revenue from consumables and software upgrades.

High Capex Requirement Compared with SiC Furnace Lines

A turnkey 200 mm sapphire line costs USD 8-12 million, versus USD 5-7 million for an equivalently sized silicon-carbide sublimation setup, while SiC wafers sell at 30-40% higher prices. Government incentives, notably the U.S. CHIPS Act, disproportionately favor SiC and other wide-bandgap materials, further diverting investment. Payback for sapphire tools stretches to 4-5 years under current LED ASPs, a hurdle for venture-backed entrants seeking quicker returns. Vendors mitigate sticker shock through equipment-as-a-service offerings and outcome-based pricing, yet financing constraints still delay adoption among second-tier fabs.

Other drivers and restraints analyzed in the detailed report include:

- Transition Toward 300 mm Sapphire Boules to Reduce Wafer CMP Loss

- Energy Savings Mandates from U.S. DOE and EU Ecodesign

- Volatile Alumina Prices Tightening OEM Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystal growth furnaces anchored 69.87% of 2025 spending, underscoring their central role in the sapphire crystal growth equipment market for LED substrates industry market size. Foundries, however, now increasingly bundle furnaces with software-centric process control packages, lifting automation attach rates to 42% in 2024. The sapphire crystal growth equipment market for LED substrates industry market share for automation and process control systems is poised to expand fastest at 6.13% CAGR through 2031 as wage inflation and tighter display specifications converge. Western OEMs differentiate through AI-driven thermal-field optimization, while Chinese vendors compete on total-cost-of-ownership guarantees that resonate with high-throughput fabs.

Replacement cycles average 8-10 years, yet the pivot to 300 mm compresses depreciation schedules, forcing write-offs of serviceable 6-inch tools. Automation platforms enjoy shorter three-to-five-year refresh intervals, creating a recurring revenue stream that cushions suppliers from furnace order volatility. Consumables such as graphite crucibles and high-purity alumina further lock customers into OEM ecosystems, gradually shifting competitive leverage from hardware price to total solution performance.

The Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and More), Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and Above 300 Mm), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 72.68% of the sapphire crystal growth equipment market for LED substrates industry market size in 2025 and is tracking a 5.72% CAGR through 2031. China alone absorbed roughly 55% of global wafer output, fueled by municipal subsidies that offset furnace depreciation. Taiwan specializes in high-margin mini-LED substrates, while South Korea's Samsung Display and LG Display balloon mini-LED TV capacity, indirectly ratcheting up sapphire substrate pull. Japan's LED incumbents divert capex to SiC and GaN, yet demand from Nichia and Toyoda Gosei still sustains a niche domestic equipment market.

North America and Europe collectively represented about 18% of 2025 revenue, constrained by limited LED chip fab footprints and subsidy programs skewed toward power electronics. The U.S. CHIPS and Science Act directed only a fractional slice of funding toward sapphire, and Wolfspeed's strategic pivot to SiC eliminated a major historical buyer. Europe's Chips Act similarly orients toward advanced logic and SiC, leaving sapphire consumption to specialized vendors such as Monocrystal, whose EU shipments face sanctions-related friction. Regulations still spur LED adoption, but the resulting substrate orders largely accrue to Asian foundries.

The Rest of the World accounted for less than 10% of sales in 2025, yet infrastructure electrification in Saudi Arabia, the UAE and Brazil positions the region for incremental gains. India's USD 10 billion Semiconductor Mission could alter the map by 2028-2030, though no sapphire tool orders were booked as of March 2026. Equipment OEMs weigh joint-venture assembly models to satisfy potential domestic-content rules, especially as South Asian governments explore localization incentives.

- GT Advanced Technologies Inc.

- PVA TePla AG

- ECM Greentech S.A. (Cyberstar)

- Crystal Systems Inc.

- Zhejiang Jingjing Science and Technology Co., Ltd.

- Crystec Technology Trading GmbH

- Monocrystal LLC

- Ferrotec Holdings Corporation

- Castech Inc.

- Linton Crystal Technologies

- Hangzhou Shalom Electro-optics Technology Co., Ltd.

- Advanced Crystal Technology Inc.

- Naura Technology Group Co., Ltd.

- Toyo Tanso Co., Ltd.

- Changchun Up Optotech Co., Ltd.

- Silian Optoelectronics (Chongqing) Co., Ltd.

- Heraeus Noblelight Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mini-LED Backlighting Adoption in High-End TVs

- 4.2.2 Aggressive Capacity Expansion by Chinese Epitaxy Foundries

- 4.2.3 Energy Savings Mandates From U.S. DOE and EU Ecodesign

- 4.2.4 Transition Toward 300 mm Sapphire Boules to Reduce Wafer CMP Loss

- 4.2.5 Integration of AI-Enabled Predictive Control in Growth Furnaces

- 4.2.6 Accelerated Capital Subsidies for Compound-Semiconductor Clusters in India

- 4.3 Market Restraints

- 4.3.1 Volatile Alumina Prices Tightening OEM Margins

- 4.3.2 High Cap-Ex Requirement Compared with SiC Furnace Lines

- 4.3.3 Yield Losses During Core-Drilling of Large-Diameter Boules

- 4.3.4 Sluggish LED Lighting Retrofit Demand in Europe Post-2024

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Ecosystem Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Upto 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GT Advanced Technologies Inc.

- 6.4.2 PVA TePla AG

- 6.4.3 ECM Greentech S.A. (Cyberstar)

- 6.4.4 Crystal Systems Inc.

- 6.4.5 Zhejiang Jingjing Science and Technology Co., Ltd.

- 6.4.6 Crystec Technology Trading GmbH

- 6.4.7 Monocrystal LLC

- 6.4.8 Ferrotec Holdings Corporation

- 6.4.9 Castech Inc.

- 6.4.10 Linton Crystal Technologies

- 6.4.11 Hangzhou Shalom Electro-optics Technology Co., Ltd.

- 6.4.12 Advanced Crystal Technology Inc.

- 6.4.13 Naura Technology Group Co., Ltd.

- 6.4.14 Toyo Tanso Co., Ltd.

- 6.4.15 Changchun Up Optotech Co., Ltd.

- 6.4.16 Silian Optoelectronics (Chongqing) Co., Ltd.

- 6.4.17 Heraeus Noblelight Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

(주말 및 공휴일 제외)