|

시장보고서

상품코드

2044038

아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

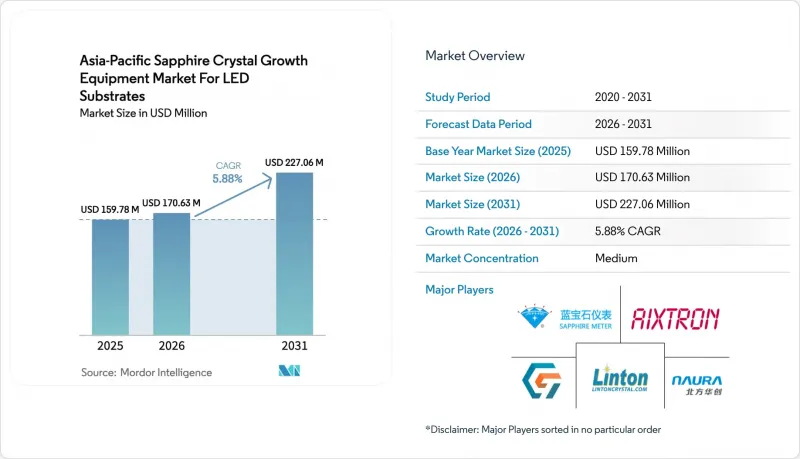

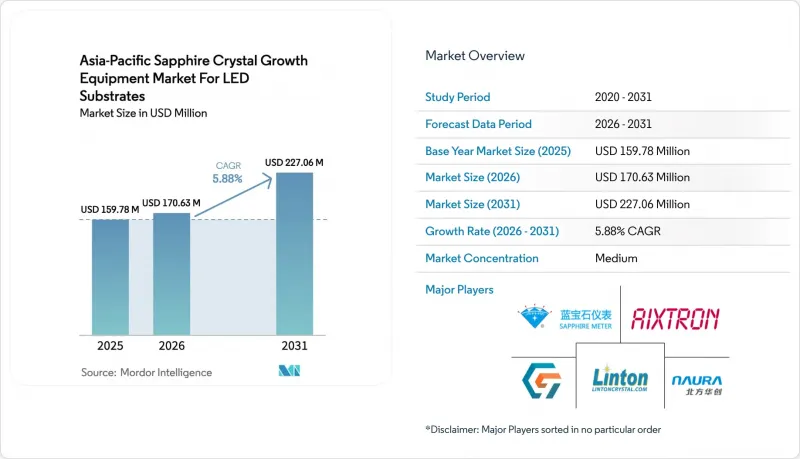

아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 시장 규모는 2025년 1억 5,978만 달러로 평가되었습니다. 2026년 1억 7,063만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.88%를 나타내, 2031년에는 2억 2,706만 달러에 이를 것으로 예측됩니다.

중국 본토의 견조한 패널 투자, 한국과 대만의 안정적인 수요, 그리고 동남아시아의 새로운 생산능력 계획이 계속해서 설비투자의 기반이 되고 있습니다. 중국, 대만, 일본 정부의 경기 부양책으로 인해 대상 장비 구매에 대한 투자 회수 기간이 단축되는 한편, 패널 제조업체의 8인치 사파이어로의 전환이 더 크고 자동화된 용광로에 대한 수요를 견인하고 있습니다. 작업자에 의존하는 시드(종자) 결정의 편차를 최소화하는 결정 성장 자동화는 특히 마이크로 LED에 대응하고자 하는 팹에서 선호되는 추가 기능으로 부상하고 있습니다. 환율과 원자재 가격의 변동은 여전히 변동 요인으로 작용하고 있지만, TV, 모니터, 자동차 디스플레이의 미니 LED 보급률 상승이 사파이어 기판 수요를 뒷받침하고 있습니다.

아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 시장 동향 및 전망

중국 본토의 미니 LED 백라이트 생산 능력의 급속한 확대

중국에서는 2025년에 800만 대 이상의 미니 LED TV가 출하되었으며, 2026년에는 1,000만 대를 넘어설 것으로 예측됩니다. 이는 국내 TV 시장의 약 1/3, 전 세계 미니 LED TV 출하량의 70% 이상을 차지합니다. 75인치 미니 LED 패널 한 장에는 수천 개의 다이가 내장되어 있어 사파이어 기판에 대한 수요가 증가하여 육성로 구매가 앞당겨지고 있습니다. 90억 위안(12억 4,000만 달러)을 투자하여 연간 5억 개 이상의 미니 LED 백라이트 모듈을 생산할 수 있도록 설계된 HKC의 류양 캠퍼스는 키로프로스 및 자동화 설비 수주를 견인하는 규모의 좋은 예입니다. 패널 업체인 BOE와 CSOT는 Gen10.5 라인을 최적화하고 LG디스플레이의 광저우 Gen8.5 공장을 흡수함으로써 연간 5,000만장 이상의 LCD TV 패널 출하량을 확보하여 중국 업스트림 공정의 설비 수요를 더욱 강화하고 있습니다. CES 2026에서 첫 선을 보인 RGB 미니 LED 아키텍처는 더 높은 밀도의 다이 배치를 필요로 하며, 그 결과 기판의 균일성이 높아야 합니다. 이는 새로운 소성로의 폐쇄 루프 공정 제어 옵션에 대한 주문을 촉진하고 있습니다.

디스플레이 LED 공급망에서 8인치 사파이어 웨이퍼로의 전환이 진행되고 있습니다.

디스플레이용 LED 제조업체들은 다이당 비용을 절감하고 생산 처리량을 높이기 위해 6인치에서 8인치(200mm) 사파이어로 전환하고 있습니다. 2025년, 아헨 공과대학(RWTH Aachen)과 AIXTRON은 5대의 200mm 유성 MOCVD 반응기를 사용하여 200mm 사파이어에 질소 극성 III-질화물 헤테로 구조를 성공적으로 제작하여 대형 웨이퍼 에피택시의 실현 가능성을 입증했습니다. 웨이퍼 직경이 확대됨에 따라 400mm 이상의 크루서블과 정밀한 열장 제어가 요구되고 있으며, 고해상도 비전 시스템 및 전동식 실드 리프트를 통합한 설비로 업그레이드가 진행되고 있습니다. 베이징대학은 세 번의 에피택시 및 박리 사이클을 견딜 수 있는 재사용 가능한 r면 사파이어를 제시하여 향후 순 웨이퍼 소비량 감소를 시사하고, 용광로의 투자 회수 모델을 뒷받침하는 결과를 도출했습니다. 그러나 300mm를 넘어서면 변위 밀도와 반경 방향 응력이 급격히 증가하기 때문에 팹에서는 수율을 허용 가능한 수준으로 유지하기 위해 고도의 자동화를 도입하는 경우가 많습니다.

카이로프로스로의 높은 설비투자액과 긴 투자 회수 기간

800-1,000kg의 부울을 처리할 수 있는 최신 카이로프로스 용광로는 설치 비용이 보통 100만 달러 이상으로, 보급형 초크랄스키법 장비를 훨씬 능가합니다. 자금 조달 문제는 동남아시아에서 가장 심각한 문제입니다. 이 지역에서는 정부 보증의 신용 한도가 제한되어 있고, 민간 금융기관은 더 높은 담보를 요구하기 때문입니다. LED 칩 가격 변동도 상황을 더욱 악화시키고 있습니다. 2026년 초 구리 및 은 가격 상승에 따른 현물 가격 10% 상승은 판매량 부진을 상쇄하지 못하고 회수 기간을 36개월 이상 연장하는 결과를 낳았습니다. 열응력 해석에 따르면, 자연 냉각 시 최대 폰-미세스 응력이 발생하며, 이에 대응하기 위해서는 히터 존의 제어를 강화해야 하며, 이는 비용 증가로 이어집니다. 광학 품질은 떨어지지만, 소용량 CZ법이나 엣지 정의법 시스템은 여전히 신규 공장 건설의 대안으로 남아있습니다.

부문 분석

2025년 아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 시장에서 결정 성장로는 매출의 70.42%를 차지했습니다. 성장 자동화 및 공정 제어 애드온 제품은 기초 규모는 작지만 2031년까지 연평균 6.17% 성장할 것으로 예상되며, 아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 시장 전체 CAGR을 상회할 것으로 예측됩니다. 육성로는 여전히 핵심 자산으로, 불의 직경, 광학 품질 및 처리량을 결정하기 때문에 여전히 핵심 자산입니다. 그러나 작업자에 의존하는 시드 공정은 여전히 수율 저하를 초래하기 때문에 팹은 새로운 설비 투자 예산을 용융 대류를 안정화하기 위한 소프트웨어 및 비전 시스템 업그레이드에 사용하고 있습니다.

자동화 업체들은 고해상도 카메라, 레이저 거리 측정기 및 예측 분석 기능을 통합하여 용융 간격을 실시간으로 추적하고 밀봉 드리프트 속도를 자동으로 조정합니다. 이러한 업그레이드를 통해 사이클별 편차를 줄여 팹이 마이크로 LED 기판 사양을 충족할 수 있도록 돕고 있습니다. 2024년 석영 도가니 가격 하락으로 인해 열장 및 도가니 서브시스템은 수익률 압박에 직면했지만 여전히 애프터마켓의 수익원을 지탱하고 있습니다. 각 공급업체들은 정기적인 매출을 보장하기 위해 장수명 단열재 및 소모품을 판매하여 아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 시장의 산업 생태계의 균형을 유지하고 있습니다.

'아시아태평양의 LED 기판용 사파이어 크리스탈 성장 장비 시장 보고서'는 장비 유형(결정 성장로, 열장 및 도가니 시스템 등), 성장 기술(카이로프로스법, 엣지 정의 필름 공급 성장법, 열교환기 등), 사파이어 직경 대응 능력(최대 150mm, 150-300mm 등), 지역별로 분류되어 있습니다. 등) 및 지역별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe Asia-Pacific sapphire crystal growth equipment market for LED substrates industry size is expected to grow from USD 159.78 million in 2025 to USD 170.63 million in 2026 and is forecast to reach USD 227.06 million by 2031 at a 5.88% CAGR over 2026-2031.

Robust panel investments in Mainland China, steady demand from Korea and Taiwan, and renewed capacity planning in Southeast Asia continue to anchor capital spending. Government stimulus programs in China, Taiwan, and Japan shorten payback cycles for qualifying tool purchases, while panel makers' migration to 8-inch sapphire drives demand for larger, more automated furnaces. Crystal-growth automation that minimizes operator-dependent seeding variability is emerging as a preferred add-on, especially among fabs chasing micro-LED readiness. Currency and commodity cost swings remain a swing factor, but rising mini-LED penetration in televisions, monitors, and automotive displays provides a firm demand floor for sapphire substrates.

Insights and Trends of Asia-Pacific Sapphire Crystal Growth Equipment Market For LED Substrates

Rapid Expansion of Mini-LED Backlighting Capacity in Mainland China

China shipped more than 8 million mini-LED televisions in 2025 and is on track to surpass 10 million units in 2026, roughly one-third of the domestic TV market and more than 70% of global mini-LED TV volumes. Each 75-inch mini-LED panel integrates thousands of dies, lifting sapphire substrate demand and pulling furnace purchases forward. HKC's Liuyang campus, financed at CNY 9 billion (USD 1.24 billion) and designed for more than 500 million mini-LED backlight modules per year, exemplifies the scale driving Kyropoulos and automation orde. Panel majors BOE and CSOT optimized Gen10.5 lines and absorbed LG Display's Guangzhou Gen8.5 fab to secure over 50 million annual LCD TV panel shipments, reinforcing China's upstream pull on equipment. RGB mini-LED architectures debuted at CES 2026 demand tighter die placement, which in turn requires higher substrate uniformity, spurring orders for closed-loop process-control options on new furnaces.

Ongoing Migration to 8-Inch Sapphire Wafers in Display LED Supply Chains

Display LED makers are transitioning from 6-inch to 8-inch (200 mm) sapphire to pare cost per die and boost fab throughput. RWTH Aachen and AIXTRON demonstrated nitrogen-polar III-nitride heterostructures on 200 mm sapphire using a 5 X 200 mm Planetary MOCVD reactor in 2025, proving large-wafer epitaxy viability. Larger diameters demand crucibles over 400 mm and precise thermal-field control, driving upgrades that bundle high-resolution vision systems and motorized shield lifts Peking University showed reusable r-plane sapphire that survives three epitaxy-and-exfoliation cycles, hinting at future reductions in net wafer consumption and supporting furnace payback models. However, dislocation density and radial stress rise sharply beyond 300 mm, so fabs often adopt advanced automation to keep yields acceptable.

High Capital Intensity and Long Payback Period for Kyropoulos Furnaces

A modern Kyropoulos furnace capable of 800-1,000 kg boules typically costs more than USD 1 million installed, well above entry-level Czochralski tools. Financing challenges are most acute in Southeast Asia, where state-backed credit lines are limited and private lenders demand higher collateral. LED chip pricing swings worsen the equation; a 10% spot-price hike on back of copper and silver inflation in early 2026 failed to offset volume softness, stretching projected paybacks beyond 36 months. Thermal-stress modeling shows the highest von Mises stress during natural cooldown, which compels additional heater-zone controls that add cost. Smaller capacity CZ or Edge-Defined systems remain fallback options for greenfield fabs despite lower optical quality.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies for Domestic LED Equipment Vendors in China and Taiwan

- Increasing Adoption of Micro-LED in Wearables and AR Devices

- Technical Challenges in Scaling Above 300 mm Sapphire Boules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystal growth furnaces generated the majority of Asia-Pacific sapphire crystal growth equipment market for LED substrates industry revenue at 70.42% in 2025. Growth automation and process-control add-ons, while a smaller base, are projected to grow 6.17% annually through 2031, outpacing the overall Asia-Pacific sapphire crystal growth equipment market for LED substrates CAGR. Furnaces remain cornerstone assets because they determine boule diameter, optical quality, and throughput. However, operator-dependent seeding still introduces yield loss; fabs therefore allocate new-tool budgets toward software and vision upgrades that stabilize melt convection.

Automation vendors integrate high-resolution cameras, laser rangefinders, and predictive analytics that track melt-gap in real time and adjust shield-lift speed automatically. These upgrades cut cycle-to-cycle variability and help fabs meet micro-LED substrate specifications. Thermal-field and crucible sub-systems face margin squeeze because quartz-crucible prices eased in 2024, but they still anchor aftermarket revenue streams. Suppliers market longer-life insulation and consumables to lock in annuity sales, keeping the Asia-Pacific sapphire crystal growth equipment market for LED substrates industry ecosystem balanced.

The Asia-Pacific Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger, and More), Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AIXTRON SE

- NAURA Technology Group Co. Ltd.

- Linton Crystal Technologies

- GT Advanced Technologies Inc.

- Crystal Systems Inc.

- JingJieHui Optoelectronic Equipment Co. Ltd.

- Shenyang Crystec Corporation

- Advanced Micro-Furnace Systems Co. Ltd.

- Ningbo Hiconics Superconductor Technology Co. Ltd.

- Shenyang Silicon Technology Co. Ltd.

- Zhejiang Jingsheng Mechanical and Electrical Co. Ltd.

- Shandong Sico Industrial Co. Ltd.

- Hangzhou Silian Technology Co. Ltd.

- Hebei Rubang Advanced Technology Co. Ltd.

- TeraSemiconductor Co. Ltd.

- Htech Machinery Co. Ltd.

- A-Plane Technologies Inc.

- Suzhou Crystal Growth Equipment Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Mini-LED Backlighting Capacity in Mainland China

- 4.2.2 Ongoing Migration to 8-inch Sapphire Wafers in Display LED Supply Chains

- 4.2.3 Government Subsidies for Domestic LED Equipment Vendors in China and Taiwan

- 4.2.4 Increasing Adoption of Micro-LED in Wearables and AR Devices

- 4.2.5 Rising Demand for High-Efficiency Lighting in Smart Cities Initiatives

- 4.2.6 Localization Policies Favoring Indigenous Equipment in Japan

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity and Long Payback Period for Kyropoulos Furnaces

- 4.3.2 Technical Challenges in Scaling Above 300 mm Sapphire Boules

- 4.3.3 Volatility in LED Chip Pricing Compressing Equipment ROI

- 4.3.4 Supply Chain Disruptions for High-Purity Alumina Crucibles

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Upto 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Taiwan

- 5.4.3 Japan

- 5.4.4 Rest of the Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AIXTRON SE

- 6.4.2 NAURA Technology Group Co. Ltd.

- 6.4.3 Linton Crystal Technologies

- 6.4.4 GT Advanced Technologies Inc.

- 6.4.5 Crystal Systems Inc.

- 6.4.6 JingJieHui Optoelectronic Equipment Co. Ltd.

- 6.4.7 Shenyang Crystec Corporation

- 6.4.8 Advanced Micro-Furnace Systems Co. Ltd.

- 6.4.9 Ningbo Hiconics Superconductor Technology Co. Ltd.

- 6.4.10 Shenyang Silicon Technology Co. Ltd.

- 6.4.11 Zhejiang Jingsheng Mechanical and Electrical Co. Ltd.

- 6.4.12 Shandong Sico Industrial Co. Ltd.

- 6.4.13 Hangzhou Silian Technology Co. Ltd.

- 6.4.14 Hebei Rubang Advanced Technology Co. Ltd.

- 6.4.15 TeraSemiconductor Co. Ltd.

- 6.4.16 Htech Machinery Co. Ltd.

- 6.4.17 A-Plane Technologies Inc.

- 6.4.18 Suzhou Crystal Growth Equipment Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment