|

시장보고서

상품코드

2044052

아시아태평양의 차량 임베디드 소프트웨어 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Vehicle-Embedded Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

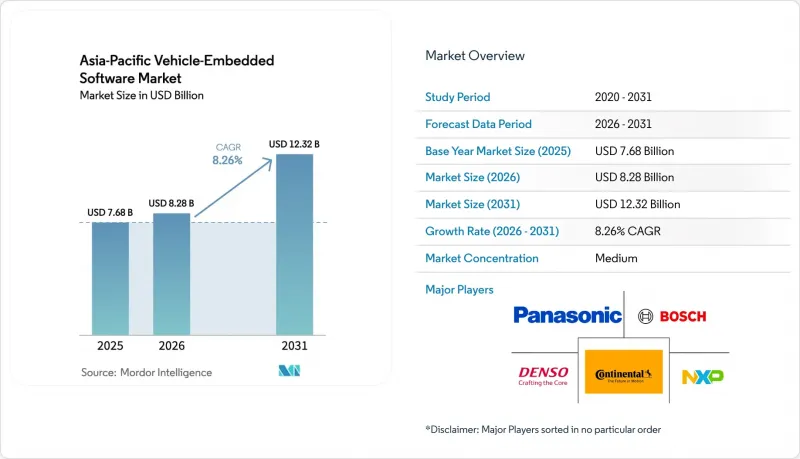

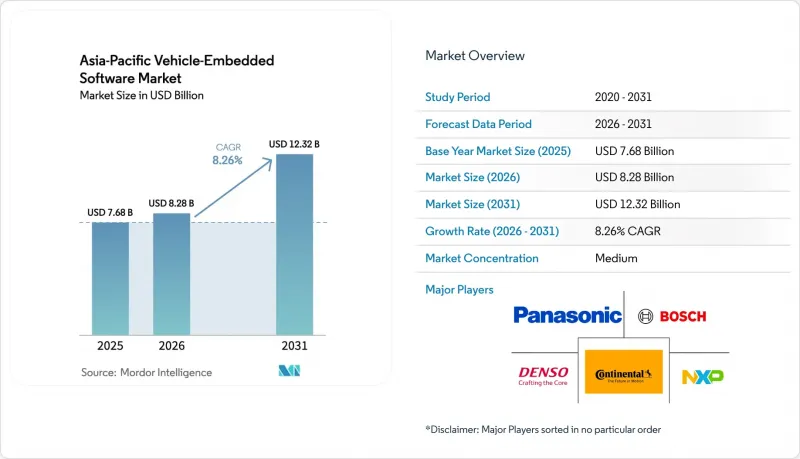

아시아태평양의 차량 임베디드 소프트웨어 시장 규모는 2025년 76억 8,000만 달러에서 2026년에는 82억 8,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.26%로 성장을 지속하여, 2031년에는 123억 2,000만 달러에 이를 것으로 예측됩니다.

전동화의 확산, 첨단 운전 보조 기능의 의무화, 중앙 집중식 컴퓨팅 플랫폼으로의 급속한 전환으로 차량 1대당 소프트웨어 지출은 하드웨어 비용을 훨씬 능가하는 속도로 증가하고 있습니다. 중국의 GB 44495-2024, 일본의 개정된 도로 운송 차량법과 같은 새로운 사이버 보안 규정으로 인해 분산형 전자 제어 장치에서 확장 가능한 미들웨어에 의존하는 존 및 도메인 아키텍처로의 전환이 가속화되고 있습니다. 오픈소스 AUTOSAR Adaptive 스택과 리눅스 기반 운영체제는 지역 공급업체의 진입장벽을 낮추고, 무선 업데이트(OTA) 생태계는 OEM(자동차 제조업체)의 판매 후 수익원을 개척하고 있습니다. 아시아태평양의 차량 임베디드 소프트웨어 시장에서 중국의 소프트웨어 기업, 인도의 엔지니어링 서비스 제공업체, 그리고 세계 1등급 공급업체들이 ISO 26262 감사를 통과할 수 있는 검증된 코드베이스를 빠른 시간 내에 제공하기 위해 경쟁하고 있습니다. 경쟁하는 가운데 경쟁은 더욱 치열해지고 있습니다.

아시아태평양 차량 임베디드 소프트웨어 시장 동향 및 인사이트

승용차 전동화 가속화

중국 내 배터리 전기자동차(BEV)는 2025년 950만 대를 넘어 승용차 판매의 38%를 차지하며 소프트웨어로 관리되는 배터리 관리 시스템에 대한 수요를 견인했습니다. 인도의 한 제조업체는 1,500달러 미만의 스쿠터에 실시간 OS를 탑재하여 인산철 리튬 배터리 팩의 제어 및 예측 주행거리 기능을 구현하고 있습니다. 2025년 4월부터 시행되는 일본의 연비 규제는 형식 인증 시 소프트웨어에 의한 파워트레인 최적화를 의무화하고 있으며, Tier 1 공급업체는 반도체 파트너와 공동 알고리즘 개발에 참여하고 있습니다. 현재 프리미엄 전기 세단의 각 모델에는 3억 개 이상의 코드가 탑재되어 있으며, 이는 기존 모델의 3배에 해당하며, 미들웨어의 수익 기회를 확대되고 있습니다.

중국과 일본의 첨단 운전자 보조 시스템(ADAS) 의무화

2026년 1월부터 시행되는 중국의 자동 긴급 제동 및 차선 유지 기능 의무화는 연간 약 2,500만 대의 신차에 적용됩니다. 일본은 2025년 3월 도로 운송 차량법 일부를 개정하여 3.5톤 이상 트럭에도 어댑티브 크루즈 컨트롤(ACC)을 적용 대상으로 추가함으로써 상용차 fleet에 ADAS 도입 범위를 확대했습니다. 르네사스는 2025년에 도요타에 200만 개 이상의 R-Car V4H 칩을 출하하여 ADAS와 인포테인먼트의 처리 부하를 단일 컴퓨팅 도메인으로 통합할 수 있도록 지원했습니다. 콘티넨탈의 CAEdge 플랫폼은 신경망 전처리를 전용 가속기에 오프로드하여 15밀리초의 검출 지연시간을 실현하고 있습니다. ASIL-D를 준수하는 기능 안전 검증은 출시 주기에 최대 18개월의 추가 기간이 필요하며, 이 지역 전체에서 OEM과 공급업체 간의 협력 관계를 더욱 긴밀하게 만들고 있습니다.

차량 ECU의 사이버 보안 취약점

UN R155 준수 감사에 따르면, 레거시 아키텍처의 23%가 하드웨어 암호화 기능이 부족하여 OEM 업체들은 개당 40달러 이상의 비용이 소요되는 리노베이션을 해야 하는 것으로 나타났습니다. 홍콩은 2026년 12월까지 R155 및 R156을 준수할 예정이며, 그레이마켓에서 수입된 차량도 새로운 개조 수요가 발생하고 있습니다. 중국의 GB 44495-2024는 전체 라이프사이클에 걸친 사이버 보안 관리를 의무화하고 있으며, CAN 버스 트래픽의 이상 징후를 모니터링하는 클라우드 기반 보안 운영 센터의 도입을 촉진하고 있습니다. 반도체 부족으로 인해 보안이 강화된 마이크로컨트롤러의 출시가 지연되고 있으며, 알려진 취약점에 대한 노출 기간이 길어지고 있습니다.

부문 분석

오토바이 시장은 1,500달러 미만의 스쿠터에 리눅스 대시보드, 블루투스, 원격 진단 기능을 통합하는 인도 및 동남아시아의 스타트업 기업들에 힘입어 CAGR 9.23%로 확대될 것으로 예측됩니다. 승용차는 중국의 2,100만대 생산량과 일본의 전자 기술 전통에 힘입어 2025년 아시아태평양 차량 임베디드 소프트웨어 시장 점유율 55.21%를 유지했습니다. 소형 상용차는 한국과 호주의 실시간 추적 의무화에 대응하기 위해 차량 텔레매틱스를 통합하고 있습니다. 대형 트럭은 진동과 오일 품질 데이터를 분석하는 예지보전을 채택하여 예기치 못한 다운타임을 15% 줄였습니다.

이륜차가 판매량 기준 성장을 주도하는 가운데, 승용차는 여전히 아시아태평양 차량 임베디드 소프트웨어 시장 규모에서 가장 큰 수익원입니다. 그러나 인도네시아나 필리핀에서는 가격에 민감한 세단에서 목표 가격을 달성하기 위해 고급 미들웨어를 생략하는 경우가 많습니다. 소형 밴은 전자기록장치 의무화의 수혜를 받고 있으며, 차량 당 소프트웨어 판매량 증가로 이어지고 있습니다. 대형 상용차는 센서가 비정상적인 패턴을 감지한 경우에만 정비 예약을 하는 예지보전 플랫폼에 대해 더 높은 평균 판매 가격을 지불하고 있으며, 이로 인해 차량 임베디드 소프트웨어의 수익률은 더욱 확대되고 있습니다.

존 컨트롤러는 이종 프로세서 간 데이터를 중개하는 서비스 지향적 프레임워크가 필요하기 때문에 미들웨어는 CAGR 9.56%로 확대될 것으로 예측됩니다. 2025년 기준, 애플리케이션 소프트웨어는 아시아태평양 차량 임베디드 소프트웨어 시장 규모의 38.43%를 차지했지만, 빠른 업데이트를 위해 컨테이너화된 배포로 전환하고 있습니다. 운영체제는 인포테인먼트의 경우 리눅스로, 안전 기능의 경우 QNX 및 유사한 마이크로커널로 수렴되어 공통의 툴체인을 사용할 수 있게 되었습니다. 가치가 상위 계층으로 이동함에 따라 펌웨어의 수익은 비례적으로 감소하고 있습니다.

Tier 1 공급업체들이 특정 시스템온칩(SoC)에 최적화된 자체 미들웨어 번들을 점점 더 많이 제공하고 있어, 자동차 제조업체의 전환 비용이 증가하고 있습니다. COVESA와 같은 컨소시엄은 상호운용성을 유지하기 위해 개방형 인터페이스 정의를 공개하고 있습니다. 그 결과, 아시아태평양의 차량 임베디드 소프트웨어 업계는 성능에 최적화된 폐쇄형 스택과 개방형 커뮤니티 코드가 혼재되어 있으며, OEM 업체들은 시장 출시 시간과 장기적인 벤더 종속성 사이에서 균형을 맞추어야 하는 상황에 처해 있습니다. 균형을 맞추어야 합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Asia-Pacific vehicle-embedded software market size is expected to grow from USD 7.68 billion in 2025 to USD 8.28 billion in 2026 and is forecast to reach USD 12.32 billion by 2031 at 8.26% CAGR over 2026-2031.

Pervasive electrification, mandatory advanced driver assistance functions, and the rapid pivot toward centralized compute platforms are expanding software spend per vehicle far faster than hardware costs. New cybersecurity mandates such as China's GB 44495-2024 and Japan's revised Road Transport Vehicle Act are accelerating the migration from distributed electronic control units to zonal and domain architectures that rely on scalable middleware. Open-source AUTOSAR Adaptive stacks and Linux-based operating systems are lowering entry barriers for regional suppliers, while over-the-air update ecosystems are unlocking post-sale revenue streams for original equipment manufacturers. Competitive intensity is rising as Chinese software houses, Indian engineering service providers, and global tier-1s race to deliver validated code bases that can pass ISO 26262 audits on compressed timelines within the Asia-Pacific vehicle-embedded software market.

Asia-Pacific Vehicle-Embedded Software Market Trends and Insights

Accelerating Electrification of Passenger Cars

Battery electric vehicle deliveries in China surpassed 9.5 million units in 2025, accounting for 38% of passenger-car sales and driving demand for software-managed battery management systems. Indian manufacturers embed real-time operating systems in sub-USD 1,500 scooters to regulate lithium iron phosphate packs and deliver predictive range functions. Japan's April 2025 efficiency rules require software-validated power-train optimization during type approval, pulling tier-1s into joint algorithm development with semiconductor partners. Each premium electric sedan now ships with more than 300 million lines of code, triple the load of a conventional model, magnifying middleware revenue opportunities.

Mandatory Advanced Driver Assistance Systems in China and Japan

China's automatic emergency braking and lane-keeping mandate effective January 2026 covers roughly 25 million new vehicles a year. Japan amended its Road Transport Vehicle Act in March 2025 to extend adaptive cruise control to trucks over 3.5 tons, widening ADAS reach into commercial fleets. Renesas shipped over 2 million R-Car V4H chips to Toyota in 2025, supporting consolidation of ADAS and infotainment loads on one compute domain. Continental's CAEdge platform reaches 15-millisecond detection latency by offloading neural-net preprocessing to dedicated accelerators. Functional-safety validation at ASIL-D continues to add up to 18 months to release cycles, driving tighter OEM-supplier collaboration across the region.

Cybersecurity Vulnerabilities in Vehicle ECUs

UN R155 compliance audits show 23% of legacy architectures lack hardware cryptography, forcing OEM retrofits costing more than USD 40 per unit. Hong Kong will align with R155 and R156 by December 2026, adding fresh retrofit demand across gray-market imports. China's GB 44495-2024 mandates full-lifecycle cybersecurity management, spurring cloud-based security operation centers that watch CAN-bus traffic for anomalies. Semiconductor shortages slow the rollout of security-enhanced microcontrollers, extending exposure windows for known vulnerabilities.

Other drivers and restraints analyzed in the detailed report include:

- Over-The-Air Update Ecosystems Scaling Across OEMs

- Emerging Software-Defined Vehicle Architectures

- Scarcity of Functional Safety-Certified Developers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Two-wheelers are projected to expand at 9.23% CAGR, propelled by Indian and Southeast Asian start-ups that bundle Linux dashboards, Bluetooth, and remote diagnostics into scooters below USD 1,500. Passenger cars retained 55.21% of Asia-Pacific vehicle-embedded software market share in 2025, buoyed by China's 21 million-unit output and Japan's electronics heritage. Light commercial vehicles integrate fleet telematics to comply with real-time tracking mandates in South Korea and Australia. Heavy trucks adopt predictive maintenance that analyzes vibration and oil quality data, reducing unplanned downtime by 15%.

While two-wheelers drive unit growth, passenger cars remain the largest revenue engine for the Asia-Pacific vehicle-embedded software market size, yet cost-sensitive sedans in Indonesia and the Philippines often strip advanced middleware to hit target price points. Light-duty vans benefit from mandated electronic logging devices, fostering incremental software sales per vehicle. Heavy commercial vehicles pay higher average selling prices for prognostics platforms that schedule service visits only when sensors flag abnormal patterns, further widening embedded software margins.

Middleware is forecast to rise at 9.56% CAGR as zonal controllers need service-oriented frameworks that broker data among heterogeneous processors. Application software held 38.43% of Asia-Pacific vehicle-embedded software market size in 2025, yet is shifting to containerized deployment for faster updates. Operating systems converge around Linux for infotainment and QNX or similar microkernels for safety, enabling common toolchains. Firmware revenue declines proportionally as value migrates upward.

Tier-1s increasingly offer proprietary middleware bundles tuned to specific system-on-chips, raising switching costs for automakers. Consortia such as COVESA publish open interface definitions to preserve interoperability. The resulting blend of closed performance-optimized stacks and open community code forces OEMs to balance time-to-market against long-term vendor lock-in across the Asia-Pacific vehicle-embedded software industry.

The Asia-Pacific Vehicle-Embedded Software Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Software Type (Operating System, Middleware, Application Software, and Firmware), Application (ADAS and Safety, Infotainment, Powertrain, and More), Propulsion Type (Internal Combustion Engine, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Panasonic Holdings Corporation

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- BlackBerry Limited

- NVIDIA Corporation

- Qualcomm Incorporated

- Elektrobit Automotive GmbH

- ETAS GmbH

- Tata Elxsi Limited

- KPIT Technologies Limited

- Aptiv PLC

- Huawei Technologies Co. Ltd.

- Baidu Inc.

- Hyundai AutoEver Corporation

- Mahindra Electric Automobile Limited

- Fujitsu Limited

- Hitachi Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Electrification of Passenger Cars

- 4.2.2 Mandatory Advanced Driver Assistance Systems in China and Japan

- 4.2.3 Over-the-Air Update Ecosystems Scaling Across OEMs

- 4.2.4 Open-Source AUTOSAR Adoption by Tier-1s

- 4.2.5 Emerging Software-Defined Vehicle Architectures

- 4.2.6 AI-Centric Embedded Platforms for Autonomous Shuttles

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Vulnerabilities in Vehicle ECUs

- 4.3.2 Scarcity of Functional Safety-Certified Developers

- 4.3.3 Rising BOM Cost Pressure on Low-End Two-Wheeler Makers

- 4.3.4 Fragmented Asia Pacific Regulatory Compliance Landscape

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.2 By Software Type

- 5.2.1 Operating System

- 5.2.2 Middleware

- 5.2.3 Application Software

- 5.2.4 Firmware

- 5.3 By Application

- 5.3.1 ADAS and Safety

- 5.3.2 Infotainment

- 5.3.3 Powertrain

- 5.3.4 Body Control and Comfort

- 5.3.5 Telematics

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine

- 5.4.2 Battery Electric Vehicle

- 5.4.3 Hybrid Electric Vehicle

- 5.4.4 Fuel Cell Electric Vehicle

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 India

- 5.5.5 Australia and New Zealand

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Denso Corporation

- 6.4.3 Continental AG

- 6.4.4 Panasonic Holdings Corporation

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 Renesas Electronics Corporation

- 6.4.7 BlackBerry Limited

- 6.4.8 NVIDIA Corporation

- 6.4.9 Qualcomm Incorporated

- 6.4.10 Elektrobit Automotive GmbH

- 6.4.11 ETAS GmbH

- 6.4.12 Tata Elxsi Limited

- 6.4.13 KPIT Technologies Limited

- 6.4.14 Aptiv PLC

- 6.4.15 Huawei Technologies Co. Ltd.

- 6.4.16 Baidu Inc.

- 6.4.17 Hyundai AutoEver Corporation

- 6.4.18 Mahindra Electric Automobile Limited

- 6.4.19 Fujitsu Limited

- 6.4.20 Hitachi Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment