|

시장보고서

상품코드

2044059

유럽의 반도체 다이오드 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Semiconductor Diode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

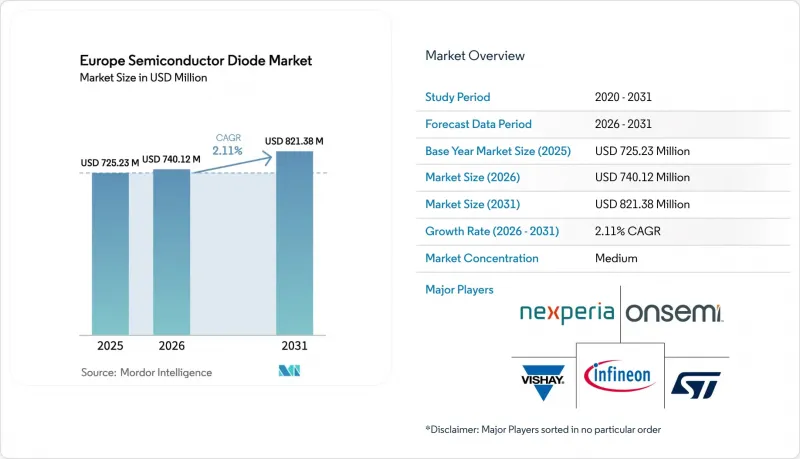

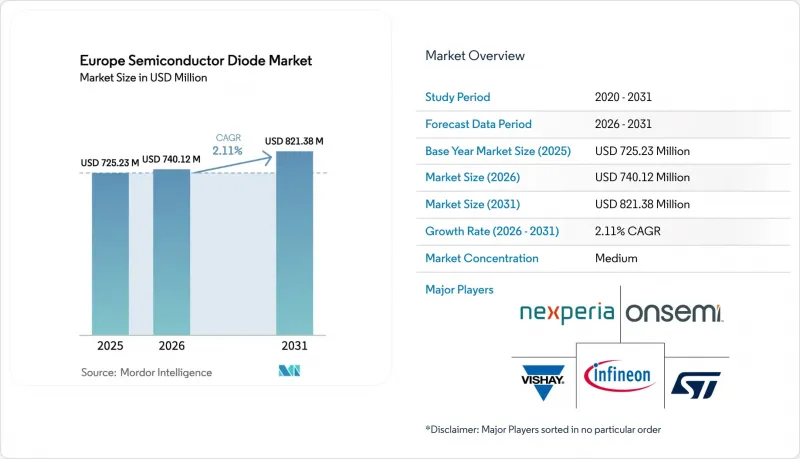

유럽의 반도체 다이오드 시장 규모는 2025년에 7억 2,523만 달러로 평가되었습니다. 2026년 7억 4,012만 달러에서 2031년까지 8억 2,138만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 2.11%를 나타낼 전망입니다.

실리콘 카바이드(SiC)와 질화갈륨(GaN)이 자동차 및 산업용 시장을 휩쓸고 있는 가운데, 기존 실리콘은 비용 중심의 소비자 및 통신 장비 시장에서 여전히 강력한 입지를 유지하고 있으며, 광대역 갭 재료로의 단계적 전환이 진행되고 있습니다. 100억 유로(116억 1,000만 달러) 규모의 ESMC 팹과 인피니언의 스마트 파워 팹 등 독일의 민관합동 메가 프로젝트는 지역 생산능력 회랑의 기반이 되어 200mm SiC 웨이퍼의 설계 도입 활동을 촉진하고 있습니다. 이탈리아 카타니아 클러스터는 ST마이크로일렉트로닉스의 SiC 디바이스 라인에 50억 유로(58억 달러), 자체 기판 생산에 7억 3,000만 유로(8억 4,726만 달러)의 지원을 받고 있으며, 칩스법(Chips Act)의 인센티브가 수직계열화를 위해 자본을 유도하고 있는 실례를 보여주고 있습니다. 쇼트키 정류기는 서버용 전원 공급 장치와 EV 차량용 충전기에서 여전히 핵심적인 역할을 하고 있지만, USB4, 썬더볼트 및 차량용 이더넷을 위한 과도 전압 억제기(TVS) 어레이는 다른 모든 디바이스 클래스를 능가하는 성장세를 보이고 있습니다. 2024년 초 전기요금 폭등(197유로/MWh)이 팹의 수익률을 압박하고 있지만, 2025년 9월 반도체 핵심 선언 이후 정책의 지속성은 첨단 노드 및 광대역 갭에 대한 투자에 대한 추가적 추진력을 제공할 것으로 보입니다.

유럽의 반도체 다이오드 시장 동향 및 인사이트

E-모빌리티가 주도하는 SiC 쇼트키 수요 증가

800V 플랫폼으로 전환하는 배터리 전기자동차(BEV)는 유럽에서 SiC 쇼트키 다이오드 수요의 주요 촉매제가 되고 있습니다. 이는 OEM 업체들이 더 빠른 충전과 가벼운 구리 하네스를 요구하고 있기 때문입니다. ST마이크로일렉트로닉스는 SOP-2026 패키지에 쇼트키 다이오드와 공봉된 4세대 SiC MOSFET에 대해 지리자동차(Geely)와 현대자동차(Hyundai)로부터 설계 채택을 획득했습니다. 2024년 하반기에 출시될 인피니언의 'HybridPACK Drive G3'는 독일 고급차 브랜드를 위해 CoolSiC MOSFET과 프리휠 다이오드를 통합한 제품입니다. 카타니아 및 울프스피드 자를란트에서 200mm SiC 웨이퍼로 전환함으로써 2027년까지 암페어당 다이 비용을 20-25% 절감할 수 있을 것으로 예측됩니다. 그러나 중국 BEV 수입품에 대한 EU의 반보조금 관세(17-35.3%)로 인해 단기적인 판매량 증가는 둔화되고 있으며, AEC-Q101 0등급 인증 획득으로 제품 출시까지의 리드타임이 12-18개월 연장되고 있습니다.

EU 칩 법에 따른 자금 조달 파이프라인 확대

'칩스법'에 따라 승인된 세계 최초의 7개 팹은 총 315억 유로(365억 6,000만 달러)의 지출을 확보했으며, 그중 3개는 광대역 갭 디바이스 전용입니다. ST마이크로일렉트로닉스만 해도 시칠리아의 디바이스 생산능력 확대에 50억 유로(58억 달러), 기판 사업에 7억 3,000만 유로(8억 4,721만 달러)를 투자하고 있으며, 온세미컨덕터는 로즈노프의 SiC 사업 확장에 16억 4,000만 유로(19억 달러)를 투자하고 있습니다. 미화 19억 달러)를 할당하고 있습니다. 스페인의 Imec이 지원하는 말라가 센터와 2026년 2월에 7억 유로 규모의 나노IC 파일럿 라인은 중소기업에 300mm 공정에 대한 접근성을 제공하고, 첨단 노드 프로토타이핑의 리스크를 줄일 수 있도록 지원합니다. 세미콘코리션의 '칩스법 2.0' 제정은 2028년까지 200억-300억 유로(2321억-348억 2,000만 달러)의 민간 자본을 추가로 유치할 수 있습니다.

SiC 기판 비용 차이 : Si 대비 6배 이상 차이

기판은 완성된 SiC 다이오드 비용의 절반을 차지하며, 여전히 동급 실리콘 웨이퍼의 6배에 달하는 가격으로 보급의 걸림돌로 작용하고 있습니다. 150mm에서 200mm로 전환하면 2027년까지 평방센티미터당 비용이 약 20% 감소하지만, 2031년까지 절대적인 가격 차이는 실리콘의 4배로 유지될 것입니다. ST마이크로일렉트로닉스와 인피니언의 수직적 통합은 변동성이 큰 현물 시장에 대한 주요 헤지 수단으로 활용되고 있습니다.

부문 분석

2025년 기준 쇼트키 다이오드는 유럽의 반도체 다이오드 시장 규모의 43.12%를 차지했으며, 이 점유율은 EV 충전기 및 서버용 PSU의 동기 정류 효율을 향상시키는 0.5V 미만의 순방향 전압 강하로 인해 발생합니다. 제너다이오드 및 소신호 다이오드는 기준 및 스위칭용으로 활용되고 있으며, TVS 및 ESD 어레이는 USB4 및 차량용 이더넷의 도입으로 인해 2.36%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다.

현재, 실리콘에 비해 용량이 훨씬 작다는 이유로 48V 마일드 하이브리드 버스에 GaN TVS를 지정하는 OEM이 증가하고 있습니다. 또한, 역복구 시간이 10ns 미만이 필요한 5G 기지국 개보수 공사도 쇼트키 다이오드 수요를 견인하고 있습니다. LiDAR용 틈새 시장인 레이저 다이오드는 매출의 5% 미만을 차지하지만, 대체 기술인 VCSEL이 부상하고 있는 가운데서도 905nm 에지 발광 설계에 대한 수요가 꾸준히 증가하고 있습니다.

실리콘은 2025년 기준 유럽의 반도체 다이오드 시장 점유율 71.43%를 유지했으며, 그 배경에는 성숙한 공급망, 풍부한 웨이퍼 생산 능력, 그리고 소비자, 통신, 저전압 산업 분야의 바이어들이 지지하는 수십 년간의 신뢰성 데이터가 있습니다. 실리콘 카바이드는 여전히 소수 소재이지만, 800V 트랙션 인버터, 650V 서보 드라이브, 350kW 그리드 스케일 배터리 충전기에서 실리콘보다 30-40% 낮은 스위칭 손실이 요구됨에 따라 2031년까지 연평균 복합 성장률(CAGR) 2.44%를 나타낼 것으로 예측됩니다. 성장하고 있습니다. ST마이크로일렉트로닉스의 카타니아 공장은 2033년까지 주당 15,000장의 200mm 웨이퍼 생산을 목표로 하고 있으며, 온세미의 로즈노프 생산라인은 2027년까지 연간 4만장의 150mm 웨이퍼 생산을 목표로 하고 있습니다. 이러한 움직임으로 인해 예측 기간 동안 유럽의 반도체 다이오드 시장에서 SiC의 점유율은 9-10%까지 확대될 수 있습니다. 질화갈륨은 2025년 점유율이 3%에 불과하지만, 11kW 차량용 충전기 및 48V 마일드 하이브리드용 DC-DC 컨버터 분야에서 입지를 다지고 있습니다. 이 분야에서는 500kHz 스위칭으로 인덕터를 소형화하여 좁은 엔진룸 내에서 전력 밀도를 향상시킬 수 있습니다. 산화갈륨과 같은 신흥 초광대역 갭 재료는 아직 실용화되기 전 단계이지만, NanoIC와 같은 EU가 지원하는 파일럿 라인에서는 200°C 이상의 접합 온도에서 3kV 이상의 역 바이어스를 견딜 수 있는 실증용 다이오드 샘플이 제공되고 있습니다.

수직적 통합의 움직임이 비용 곡선을 다시 쓰고 있습니다. ST마이크로일렉트로닉스의 7억 3천만 유로 규모의 자체 기판 프로젝트는 2026년까지 SiC 웨이퍼 수요의 40%를 자체 생산하여 현물 시장의 변동성 리스크를 줄이고, 암페어당 다이 비용을 4분의 1 가까이 절감하는 것을 목표로 하고 있습니다. 인피니언도 드레스덴에서 유사한 리스크 헤지를 진행하고 있으며, 현재 200mm SiC 생산으로 전환하면서 2027년 이후 양산 확대를 위해 300mm 로트 시험 생산을 진행하고 있습니다. GeneSiC나 리틀퓨즈의 자회사 등 자체 잉곳 제조 능력이 없는 디바이스 업체들은 다년간의 기판 공급 계약을 체결하는 경우가 늘고 있으며, 웨이퍼의 경제성이 상대적으로 좋은 GaN으로 전환을 추진하고 있습니다. 실리콘은 USB 전원 어댑터, 셋톱박스, 가전제품과 같은 저전압 용도에서 여전히 주류가 될 것입니다. 그러나 자동차, 재생에너지, 중공업 고객들이 효율화 요구사항과 라이프사이클 비용 절감을 이유로 광대역 갭 정류기를 표준화함에 따라 2031년까지 지역 전체 점유율은 60%대 후반까지 하락할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe Europe Semiconductor Diode Market size was valued at USD 725.23 million in 2025 and is estimated to grow from USD 740.12 million in 2026 to reach USD 821.38 million by 2031, at a CAGR of 2.11% during the forecast period (2026-2031).

A gradual pivot toward wide-bandgap materials is unfolding as silicon carbide (SiC) and gallium nitride (GaN) capture automotive and industrial sockets, while legacy silicon remains entrenched in cost-sensitive consumer and telecom gear. Germany's public-private megaprojects, including the EUR 10 billion (USD 11.61 billion) ESMC fab and Infineon's Smart Power Fab, are anchoring regional capacity corridors and stimulating design-in activity for 200 mm SiC wafers. Italy's Catania cluster, backed by EUR 5 billion (USD 5.80 billion) for STMicroelectronics' SiC device line and EUR 730 million (USD 847.26 million) for captive substrate output, demonstrates how Chips Act incentives funnel capital toward vertical integration. Schottky rectifiers keep their central role in server power supplies and EV on-board chargers, yet transient-voltage-suppression (TVS) arrays for USB4, Thunderbolt and automotive Ethernet outpace all other device classes. Elevated electricity tariffs 197 EUR/MWh in early 2024 squeeze fab margins, but policy continuity after the September 2025 Semicon Coalition declaration signals further tailwinds for advanced-node and wide-bandgap investment.

Europe Semiconductor Diode Market Trends and Insights

E-Mobility Led SiC-Schottky Pull-Through

Battery-electric vehicles moving to 800 V platforms are the prime catalyst for SiC Schottky demand in Europe, as OEMs seek faster charging and lighter copper harnesses. STMicroelectronics logged design wins with Geely and Hyundai for fourth-generation SiC MOSFETs co-packaged with Schottky diodes for SOP-2026 lines. Infineon's HybridPACK Drive G3, rolled out in late 2024, integrates CoolSiC MOSFETs and free-wheeling diodes for German premium brands. Transitioning to 200 mm SiC wafers at Catania and Wolfspeed Saarland is expected to trim die cost per ampere by 20-25% by 2027. Yet EU anti-subsidy duties of 17-35.3% on Chinese BEV imports have softened near-term unit pull-through, and AEC-Q101 Grade 0 validation pushes product-launch lead-times out by 12-18 months.

Expansion of EU Chips Act Funding Pipeline

Seven first-of-a-kind fabs approved under the Chips Act have secured EUR 31.5 billion (USD 36.56 billion) in combined spending, with three dedicated to wide-bandgap devices. STMicroelectronics alone commands EUR 5 billion (USD 5.80 billion) for device capacity and EUR 730 million (USD 847.21 million) for substrates in Sicily, while onsemi allocates EUR 1.64 billion (USD 1.90 billion) to Roznov SiC expansion. Spain's Imec-backed Malaga center and the EUR 700 million NanoIC pilot line, funded in February 2026, give SMEs 300 mm access and de-risk advanced-node prototyping. The Semicon Coalition's call for a "Chips Act 2.0" could unlock another EUR 20-30 billion (USD 23.21 -34.82 billion) in private capital by 2028.

SiC Substrate Cost Delta vs. Si Greater Than 6X

Substrates account for half of finished SiC diode cost and still price out at six times equivalent silicon wafers, hindering broader penetration. Moving from 150 mm to 200 mm cuts cost per square centimeter by roughly 20% by 2027, yet the absolute premium stays quadruple that of silicon through 2031. Vertical integration at STMicro and Infineon remains the chief hedge against volatile spot markets.

Other drivers and restraints analyzed in the detailed report include:

- Telecom 5G / FTTx Rectifier Renewal

- EV On-Board Charger Design-Wins for GaN TVS

- Automotive OEM PPAP Backlog Less Than18 Months

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Schottky devices represented 43.12% of the Europe semiconductor diode market size in 2025, a share rooted in their sub-0.5 V forward drop that improves synchronous rectifier efficiency in EV chargers and server PSUs. Zener and small-signal diodes serve as references and for switching, while TVS and ESD arrays post the steepest 2.36% CAGR thanks to USB4 and automotive Ethernet rollouts.

More OEMs now specify GaN TVS for 48 V mild-hybrid buses, citing order-of-magnitude lower capacitance than silicon counterparts. Schottky demand also benefits from 5G base-station retrofits that require less than 10 ns of reverse recovery time. Niche laser diodes for LiDAR contribute under 5% of revenue but see solid traction in 905 nm edge-emitting designs, even as VCSEL alternatives loom.

Silicon retained 71.43% Europe semiconductor diode market share in 2025, underpinned by its mature supply chain, abundant wafer capacity and decades-long reliability data favored by consumer, telecom and low-voltage industrial buyers. Silicon carbide, though still a minority material, is pacing a 2.44% CAGR to 2031 as 800 V traction inverters, 650 V servo drives and 350 kW grid-scale battery chargers demand 30-40% lower switching losses than silicon can deliver. STMicroelectronics' Catania hub targets 15,000 200 mm wafers per week by 2033, while onsemi's Roznov line will push 40,000 150 mm wafers annually by 2027, moves that could lift SiC's slice of the Europe semiconductor diode market size toward 9-10% over the forecast horizon. Gallium nitride, holding barely 3% volume in 2025, is carving footholds in 11 kW on-board chargers and 48 V mild-hybrid DC-DC converters, where 500 kHz switching shrinks inductors and raises power density in cramped engine bays. Emerging ultra-wide-bandgap options such as gallium oxide remain pre-commercial, but EU-funded pilot lines like NanoIC are sampling demonstrator diodes that withstand over 3 kV reverse bias at junction temperatures above 200 °C.

Vertical-integration plays are rewriting cost curves: STMicroelectronics' EUR 730 million captive-substrate project seeks to internalize 40% of its SiC wafer demand by 2026, cutting exposure to spot-market swings and shaving die cost per ampere by nearly one-quarter. Infineon pursues a similar hedge at Dresden, shifting to 200 mm SiC production today and piloting 300 mm lots for post-2027 ramps. Device makers without in-house boule capacity, including GeneSiC and Littelfuse subsidiaries, increasingly lock multi-year substrate supply contracts or pivot toward GaN where wafer economics are comparatively benign. Silicon will still dominate low-voltage sockets USB power bricks, set-top boxes, home appliances-yet its region-wide share is likely to dip to the high-sixties by 2031 as automotive, renewable-energy and heavy-industry clients standardize on wide-bandgap rectifiers for efficiency mandates and lifetime cost reductions.

The Europe Semiconductor Diode Market Report is Segmented by Type (Schottky, Zener, and More), Base Material (Silicon, Silicon Carbide, and More), End-Use Industry (Automotive and Transportation, Consumer Electronics, and More), Application (Power Rectification and Conversion, and More), Package Type (Surface Mount, and Through-Hole), and Country (Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Infineon Technologies AG

- STMicroelectronics N.V.

- Nexperia B.V.

- Vishay Intertechnology, Inc.

- onsemi Corporation

- ROHM Co., Ltd.

- Littelfuse, Inc.

- Toshiba Electronic Devices and Storage Corp.

- Renesas Electronics Corp.

- Hitachi Power Semiconductor Device Ltd.

- Mitsubishi Electric Corp.

- Microchip Technology Inc.

- Central Semiconductor Corp.

- WeEn Semiconductors

- Semikron Danfoss

- GeneSiC Semiconductor

- ABB Semiconductors

- Diotec Semiconductor AG

- IXYS (Littelfuse)

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Mobility Led SiC-Schottky Pull-Through

- 4.2.2 Expansion of EU Chips Act Funding Pipeline

- 4.2.3 Telecom 5G / FTTx Rectifier Replacement Cycle

- 4.2.4 EV On-Board Charger Design-Wins for GaN TVS

- 4.2.5 Power-Dense Data-Centre PSUs Less Than 3 kW

- 4.2.6 Edge-AI Industrial Drives Less Than 650 V

- 4.3 Market Restraints

- 4.3.1 SiC Substrate Cost Delta vs. Si Greater Than 6x

- 4.3.2 Automotive OEM PPAP Backlog Less Than 18 Months

- 4.3.3 EU Energy-Price Volatility on Fab OPEX

- 4.3.4 Trade-Remedy Tariffs on Chinese BEV Imports

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Schottky

- 5.1.2 Zener

- 5.1.3 TVS / ESD

- 5.1.4 Laser

- 5.1.5 Small-Signal Switching

- 5.1.6 Other Types

- 5.2 By Base Material

- 5.2.1 Silicon (Si)

- 5.2.2 Silicon Carbide (SiC)

- 5.2.3 Gallium Nitride (GaN)

- 5.2.4 Other Base Materials

- 5.3 By End-Use Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Consumer Electronics

- 5.3.3 Communications Infrastructure

- 5.3.4 Industrial Automation and Power

- 5.3.5 Computing and Data Centre

- 5.3.6 Other End-Use Industries

- 5.4 By Application

- 5.4.1 Power Rectification and Conversion

- 5.4.2 Voltage Regulation and Reference

- 5.4.3 Electrostatic / Surge / Circuit Protection

- 5.4.4 Other Applications

- 5.5 By Package Type

- 5.5.1 Surface Mount (SMD)

- 5.5.2 Through-Hole

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank / Share, Products and Services, Recent Developments)

- 6.1.1 Infineon Technologies AG

- 6.1.2 STMicroelectronics N.V.

- 6.1.3 Nexperia B.V.

- 6.1.4 Vishay Intertechnology, Inc.

- 6.1.5 onsemi Corporation

- 6.1.6 ROHM Co., Ltd.

- 6.1.7 Littelfuse, Inc.

- 6.1.8 Toshiba Electronic Devices and Storage Corp.

- 6.1.9 Renesas Electronics Corp.

- 6.1.10 Hitachi Power Semiconductor Device Ltd.

- 6.1.11 Mitsubishi Electric Corp.

- 6.1.12 Microchip Technology Inc.

- 6.1.13 Central Semiconductor Corp.

- 6.1.14 WeEn Semiconductors

- 6.1.15 Semikron Danfoss

- 6.1.16 GeneSiC Semiconductor

- 6.1.17 ABB Semiconductors

- 6.1.18 Diotec Semiconductor AG

- 6.1.19 IXYS (Littelfuse)

- 6.1.20 Wolfspeed, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment