|

시장보고서

상품코드

2044069

디지털 접근성 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Digital Accessibility Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

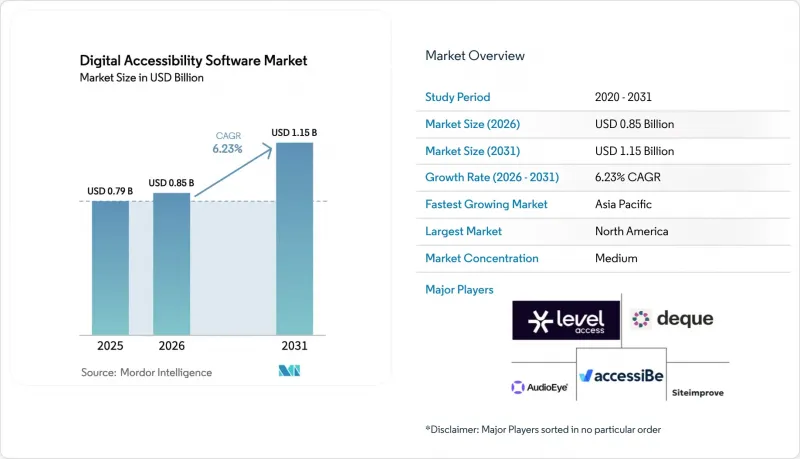

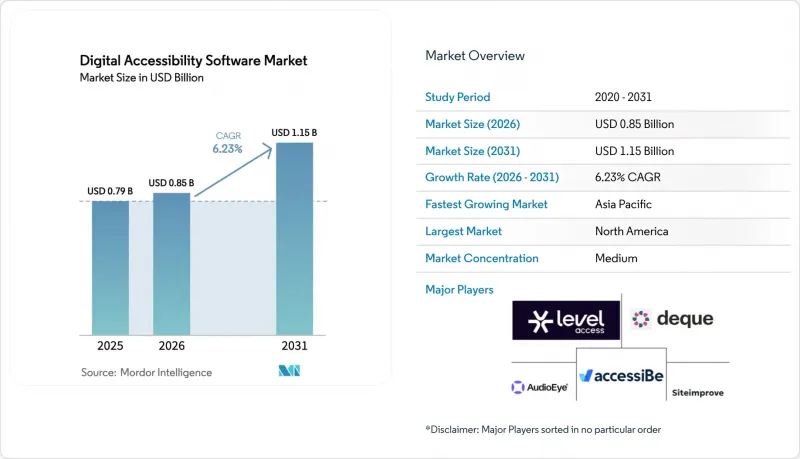

디지털 접근성 소프트웨어 시장 규모는 2025년에 7억 9,000만 달러로 평가되었습니다. 2026년 8억 5,000만 달러에서 2031년까지 11억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 6.23%를 나타낼 전망입니다.

현재 성장의 원동력이 되고 있는 것은 단발성 감사가 아닌 정기적인 구독입니다. 이는 구매자가 정부 입찰 및 ESG 스코어카드에서 지속적인 준수를 보여줘야 하기 때문입니다. 2025년 10월 WCAG 2.2의 ISO 표준화와 2025년 6월 유럽연합 접근성 법 시행으로 접근성 디자인은 단순한 법적 부수적인 사항이 아닌 수익 창출의 전제조건으로 재정의되었습니다. 커밋마다 코드를 스캔하는 클라우드 API, 즉시 수정안을 제안하는 AI 모델, 접근성 적합성 보고서를 자동 입력하는 조달 툴킷을 통해 적합성은 DevOps의 지표로 탈바꿈했습니다. 북미 수요는 여전히 섹션 508 규정에 의해 뒷받침되고 있지만, 일본, 인도, 호주가 민간 부문 계약을 의무적인 가이드라인에 맞추면서 아시아태평양이 추가 지출을 주도할 것으로 예측됩니다. 플랫폼의 차별화는 현재 AI의 정확성, 모바일 우선 테스트, 그리고 기계의 결과물을 검증하는 인간 감사 서비스의 깊이에 따라 달라집니다.

세계의 디지털 접근성 소프트웨어 시장 동향 및 인사이트

WCAG 2.2 표준의 급속한 확산

ISO/IEC 40500 : 2025에 따라 WCAG 2.2는 임의 지침에서 공식 벤치마크로 격상되었으며, 포춘지 선정 500대 기업의 조달팀은 현재 레벨 AA 준수를 필수 입찰 기준으로 삼고 있습니다. 유럽 규제 당국은 회원국들이 WCAG 2.1에서 업그레이드를 허용하고 있기 때문에 벤더는 유럽 대륙에서 계약을 체결하기 위해 여러 버전의 테스트를 지원해야 합니다. 독일과 프랑스 정부 기관은 2027년까지 WCAG 2.2를 채택할 계획이며, 이로 인해 레거시 스캐닝 엔진의 업데이트 주기가 가속화되고 있습니다. 모듈식 규칙 라이브러리를 갖춘 플랫폼은 새로운 표준을 보다 빠르게 도입할 수 있어 조달 기한이 임박했을 때 선점 효과를 얻을 수 있습니다. Deque Systems의 2026년 1월 릴리스에서는 확장된 규칙 세트로 모델을 재학습시킨 후 테스트 속도가 4배 향상되었다고 주장하며, 알고리즘의 민첩성이 업데이트 속도에 미치는 영향을 강조하고 있습니다.

90% 이상의 AI 기반 수정 정확도

접근성 데이터로 미세 조정된 대규모 언어 모델은 2025년 92%의 정확도를 달성하여 구매자의 신뢰를 떨어뜨리는 오감지를 줄였습니다. 자동화된 코드 제안은 개발자의 수정 시간을 몇 시간에서 몇 분으로 단축시켜 중견기업도 지속적인 스캐닝을 경제적으로 실현할 수 있게 해줍니다. 2026년 3월 구글이 발표한 'Natively Adaptive Interfaces' 프레임워크는 AI를 브라우저 계층에 내장하여 UI가 운동 기능 장애에 맞게 자동 조정될 수 있도록 합니다. 자동화가 확대됨에 따라 조직은 레거시 용도에 숨어있는 문제를 발견하게 되고, 이는 엣지 케이스 검증에 대한 컨설팅 수요를 뒷받침하고 있습니다. 따라서 AI를 통한 초기 선별과 온디맨드 방식의 인력 감사를 결합하는 벤더는 양과 복잡성 모두에서 수익원을 확보할 수 있습니다.

통일된 세계 집행 메커니즘의 부재

대륙을 넘나들며 사업을 전개하는 기업들은 WCAG 2.0, 2.1, 2.2 외에도 국가별 법률에 대응해야 하며, 각 국가마다 고유한 기한과 벌칙이 있어 컴플라이언스 부담이 가중되고 있습니다. 벤더는 여러 규칙 세트를 유지해야 하고, 이는 연구개발비와 영업 지원 비용을 증가시키고 있습니다. 인도의 일부 주와 같이 처벌이 없는 관할권에서의 채택률은 40% 미만이며, 이는 총 수요 규모를 희석시키고 있습니다. 현지의 기존 기업들은 현지 사정에 맞는 서비스를 제공함으로써 성공을 거두고 있으며, 이것이 세계 플랫폼의 확장을 복잡하게 만들고 있습니다. ITU와 같은 통일된 기관이 존재하지 않기 때문에 인증이 국경을 넘어 통용되는 경우가 드물고, 규모의 경제가 제한되어 있습니다.

부문 분석

모바일 스위트는 인도, 인도네시아, 브라질에서 은행, 결제, 소매업이 스마트폰 중심의 슈퍼앱으로 전환되면서 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.39%로 가장 빠른 성장세를 보일 것으로 예측됩니다. 한편, 웹사이트 플랫폼은 2025년 기준 디지털 접근성 소프트웨어 시장 점유율의 36.32%를 차지했지만, 데스크톱 트래픽이 급증하면서 성장세가 둔화되고 있습니다. 모바일 테스트에는 많은 레거시 스캐너에 없는 고유 기능, 제스처 시뮬레이션, 생체 인식 워크플로우 확인, UIAccessibility 및 TalkBack을 위한 API 커버리지가 필요합니다. Deque Systems와 같은 벤더들은 제스처 AI를 통합하여 모바일 스캔 시간을 75% 단축하여 앱 퍼스트 기업에서 우위를 점하고 있습니다.

틈새 카테고리에 대한 압박은 점점 더 커지고 있습니다. 색상 대비 분석 도구와 캡션 지원 도구는 점점 더 광범위한 제품군에 통합되는 추세이며, 단일 기능 제품은 상품화되는 추세입니다. 문서 및 PDF 수정 소프트웨어는 정부 및 금융 분야에서 꾸준한 수요가 있지만, 워크플로우가 디지털 네이티브 포맷으로 전환되는 분야에서는 점유율을 잃어가고 있습니다. 이러한 작업을 하나의 대시보드에 통합하는 플랫폼은 평균 판매가격이 높고 해지율이 낮아 디지털 접근성 소프트웨어 시장에서 통합 추세가 강화되고 있습니다.

탄력적인 가격 정책과 GitHub, GitLab, Bitbucket의 파이프라인과의 즉각적인 통합으로 2025년 매출의 64.13%를 클라우드 도입이 차지했습니다. 커밋마다 지속적인 스캔을 통해 결함 유출률을 낮추기 때문에 개발팀은 접근성을 보안 테스트와 마찬가지로 접근성을 다루고 있습니다. 소스코드를 격리해야 하는 국방 및 의료 분야에서는 여전히 On-Premise형 툴이 사용되고 있지만, 그 성장률은 전체 디지털 접근성 소프트웨어 시장보다 몇 포인트 뒤쳐져 있습니다. 하이퍼스케일러 업체들은 DevOps 템플릿에 기본 스캐닝 기능을 포함시킴으로써 가격 경쟁을 심화시켰고, 독립 벤더들은 정확도, 규칙의 깊이 또는 산업별 프리셋으로 차별화를 꾀할 수 밖에 없게 되었습니다.

클라우드 구독형 디지털 접근성 소프트웨어 시장 규모는 API 사용량에 따른 과금 모델을 통해 홀리데이 캠페인이나 라이브 스트리밍 이벤트 시 웹 트래픽 급증에 따른 비용 조정이 가능해짐에 따라 확대될 것으로 보입니다. 반면, On-Premise 도입과 연계된 영구 라이선스 모델은 사용량에 따른 업셀링 수단이 없어 수익성 측면에서 역풍을 맞고 있습니다.

지역별 분석

북미는 20년간의 섹션 508 감독 체계와 공인 감사인의 풍부한 인력 기반에 힘입어 2025년 지출의 39.87%를 차지할 것으로 예측됩니다. 적합성 확보를 위한 예산은 프로젝트 도입에서 지속적인 모니터링 구독으로 전환되고 있으며, 이로 인해 이 지역의 성장이 더디게 진행되고 있습니다. 아시아태평양은 2024년 일본의 민간 부문 의무화, 인도의 주정부 포털에 대한 WCAG 요건 확대, 호주 정부 사이트의 레벨 AA 달성 시한을 배경으로 2031년까지 연평균 7.21%의 성장률을 나타낼 것으로 예측되며, 이는 모든 지역 중 가장 높은 성장률을 나타낼 것으로 예측됩니다. 중 가장 높은 성장률을 나타낼 것으로 예측됩니다. 싱가포르의 30억 싱가포르 달러(22억 달러) 규모의 인클루전 프로그램은 이 지역 수요를 더욱 가속화시키고 있습니다.

유럽의 동향은 2025년 6월부터 시행되는 유럽연합(EU) 접근성 법에 영향을 받습니다. 규제 당국은 처벌보다는 지침에 중점을 둔 완만한 유예기간을 두고 있어 일시적인 정체 현상이 발생하고 있습니다. 독일과 프랑스가 2027년까지 WCAG 2.2를 채택하겠다는 의사를 밝힘에 따라 업그레이드 주기가 다시 시작될 것이며, 벤더들은 단일 플랫폼 내에서 두 가지 규칙 세트를 모두 충족시켜야 하는 상황에 직면하게 될 것입니다.

남미에서는 브라질의 법률에 따라 디지털 서비스 접근성이 의무화되면서 관심이 높아지고 있지만, 시행 상황에 따라 편차가 있어 조달이 더디게 진행되고 있습니다. 중동 및 아프리카에서의 도입은 이제 막 시작되었지만, 남아공의 2025년판 '디지털 포용 정책' 초안과 아랍에미리트의 '스마트 두바이' 프레임워크는 향후 모멘텀을 시사하고 있습니다. 각 벤더들은 현지 입찰에 대응하기 위해 현지 시스템 통합사업자와의 채널 파트너십을 모색하고 있으며, 자금이 부족한 구매자에게는 셀프 서비스형 오버레이 솔루션이 제공되고 있습니다. 따라서 디지털 접근성 소프트웨어 시장은 지역마다 다른 속도로 진화하고 있으며, 공급업체들은 각 지역의 성숙도에 따라 비즈니스 모델을 조정할 수밖에 없는 상황에 처해 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The digital accessibility software market size is projected to be USD 0.79 billion in 2025, USD 0.85 billion in 2026, and reach USD 1.15 billion by 2031, growing at a CAGR of 6.23% from 2026 to 2031.

Growth now comes from recurrent subscriptions rather than one-time audits because buyers must show continuous conformance in government tenders and ESG scorecards. October 2025 ISO adoption of WCAG 2.2 and June 2025 enforcement of the European Union Accessibility Act re-positioned accessible design as a revenue prerequisite instead of a legal afterthought. Cloud APIs that scan code during every commit, AI models that propose instant fixes, and procurement toolkits that auto-populate Accessibility Conformance Reports have turned conformance into a DevOps metric. North American demand remains anchored by Section 508 rules, yet Asia-Pacific is set to lead incremental spending as Japan, India, and Australia align private-sector contracts with mandatory guidelines. Platform differentiation now pivots on AI accuracy, mobile-first testing, and the depth of human audit services that validate machine output.

Global Digital Accessibility Software Market Trends and Insights

Rapid Adoption of WCAG 2.2 Standards

ISO/IEC 40500:2025 elevated WCAG 2.2 from voluntary guidance to a formal benchmark, and Fortune 500 sourcing teams now list Level AA conformance as a mandatory bid criterion. European regulators allow members to upgrade from WCAG 2.1, so vendors must support multi-version testing to win continental contracts. German and French agencies plan to adopt WCAG 2.2 by 2027, accelerating refresh cycles for legacy scanning engines. Platforms with modular rule libraries ingest new criteria faster, giving them a first-mover advantage when procurement deadlines tighten. Deque Systems' January 2026 release claims four-fold faster testing after retraining models on the expanded rule set, highlighting how algorithmic agility influences renewal rates.

AI-Driven Remediation Accuracy Exceeding 90 Percent

Large language models fine-tuned on accessibility data reached 92% precision in 2025, reducing false positives that historically eroded buyer confidence. Automated code suggestions now cut developer fix time from hours to minutes, making continuous scanning economically viable for mid-market firms. Google's March 2026 Natively Adaptive Interfaces framework pushes AI to the browser layer, letting UIs auto-adjust for motor impairments. As automation scales, organizations uncover hidden issues in legacy apps, which sustains consulting demand for edge-case validation. Vendors pairing AI triage with on-demand human auditors therefore capture both volume and complexity revenue streams.

Lack of Unified Global Enforcement Mechanisms

Corporations operating across continents juggle WCAG 2.0, 2.1, and 2.2 plus country-specific acts, each with unique timelines and penalties, elevating compliance overhead. Vendors must maintain multiple rule sets, which inflates R&D and sales enablement costs. Adoption in jurisdictions without fines, such as several Indian states, lags below 40%, diluting the total demand pool. Regional incumbents thrive by tailoring offerings to local nuances, complicating global platform rollouts. The absence of a unifying body akin to the ITU means certifications rarely transfer across borders, capping economies of scale.

Other drivers and restraints analyzed in the detailed report include:

- Government Procurement Rules Mandating Section 508 Compliance

- Low-Code and No-Code Tools Reducing Buyer TCO

- High False-Positive Rates in Legacy Engines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile suites delivered the fastest growth trajectory, posting a projected 7.39% CAGR from 2026 to 2031 as banking, payments, and retail activity shifted to smartphone-centric super-apps in India, Indonesia, and Brazil. While website platforms still held 36.32% of the digital accessibility software market share in 2025, their growth tempers as desktop traffic plateaus. Mobile testing demands distinct capabilities, gesture simulation, biometric workflow checks, and API coverage for UIAccessibility and TalkBack, that many legacy scanners lack. Vendors such as Deque Systems cut mobile scan time by 75% after embedding gesture AI, giving them an edge with app-first enterprises.

Pressure on niche categories is rising. Color-contrast analyzers and captioning helpers are increasingly bundled into broader suites, pushing single-function products toward commoditization. Document and PDF remediation software enjoys sticky demand in government and finance, but loses share where workflows migrate to born-digital formats. Platforms that weave these tasks into one dashboard capture higher average selling prices and lower churn, reinforcing consolidation trends in the digital accessibility software market.

Cloud deployments accounted for 64.13% of 2025 revenue thanks to elastic pricing and instant integration with GitHub, GitLab, and Bitbucket pipelines. Continuous scans at every commit reduce defect escape rates, so development teams see accessibility the same way they treat security testing. On-premise tools persist in defense and healthcare segments that must isolate source code, yet their growth lags behind the broader digital accessibility software market by several points. Hyperscalers intensified price pressure by embedding baseline scans in DevOps templates, forcing independent vendors to differentiate on accuracy, rule depth, or industry-specific presets.

The digital accessibility software market size for cloud subscriptions will expand as API-metered models align costs with surges in web traffic during holiday campaigns or live-streamed events. Conversely, perpetual-license models tied to on-premise installations face revenue headwinds because they lack usage-based upsell levers.

Digital Accessibility Software Market Report is Segmented by Type (Website Accessibility Platforms, Automated Scan and Audit Tools, and More), Deployment Mode (Cloud-Based, and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (E-Commerce and Retail, BFSI, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 39.87% of 2025 spending because of two decades of Section 508 oversight and a deep bench of certified auditors. Conformance budgets have now shifted from project implementations to continuous monitoring subscriptions, moderating regional growth. Asia-Pacific is projected to record a 7.21% CAGR to 2031, the fastest among all regions, driven by Japan's private-sector mandate effective 2024, India's extension of WCAG requirements to state portals, and Australia's deadline for Level AA government sites. Singapore's SGD 3 billion (USD 2.2 billion) inclusion program further accelerates regional demand.

Europe's trajectory depends on the European Union Accessibility Act, which began enforcement in June 2025. Regulators have granted a soft grace period, focusing on guidance rather than penalties, creating a temporary plateau. German and French intentions to adopt WCAG 2.2 by 2027 will restart upgrade cycles, forcing vendors to juggle dual rule sets within a single platform.

South America shows rising interest as Brazil's law requires digital services to be accessible, yet uneven enforcement slows procurement. Middle East and Africa adoption is nascent; South Africa's 2025 draft Digital Inclusion Policy and the United Arab Emirates' Smart Dubai framework hint at future momentum. Vendors eye channel partnerships with regional system integrators to navigate local tenders, while self-service overlays cater to cash-constrained buyers. The digital accessibility software market therefore evolves at uneven velocities, compelling suppliers to tailor commercial models to regional maturity levels.

- Level Access, Inc.

- Siteimprove A/S

- AudioEye, Inc.

- Deque Systems, Inc.

- UserWay Inc.

- Monsido ApS

- Crownpeak Technology, Inc.

- Silktide Ltd.

- accessiBe Ltd.

- EqualWeb Ltd.

- UsableNet, Inc.

- TPGi, A Vispero Company

- Allyant, Inc.

- Google LLC

- Microsoft Corporation

- International Business Machines Corporation

- WebAIM, Utah State University

- Dubbot LLC

- Applause App Quality, Inc.

- Testlio, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Rapid Adoption of WCAG 2.2 Standards

- 4.3.2 AI-Driven Remediation Accuracy Exceeding 90 Percent

- 4.3.3 Government Procurement Rules Mandating Section 508 Compliance

- 4.3.4 Low-Code and No-Code Tools Reducing Buyer TCO

- 4.3.5 ESG Scorecards Adding Digital-First CX KPIs

- 4.3.6 Expansion of Streaming Services Requiring Accessible Video

- 4.4 Market Restraints

- 4.4.1 Lack of Unified Global Enforcement Mechanisms

- 4.4.2 High False-Positive Rates in Legacy Engines

- 4.4.3 Shortage of Certified Accessibility Auditors

- 4.4.4 Overlay-Fatigue Backlash Among Disability Advocates

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Industry Ecosystem Analysis

- 4.10 Key Use Cases and Case Studies

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Website Accessibility Platforms

- 5.1.2 Automated Scan and Audit Tools

- 5.1.3 Color-Contrast and Readability Checkers

- 5.1.4 Mobile and App Accessibility Suites

- 5.1.5 Video and Captioning Assist Tools

- 5.1.6 Document and PDF Remediation Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 E-Commerce and Retail

- 5.4.2 Banking, Financial Services and Insurance

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Education

- 5.4.6 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Level Access, Inc.

- 6.4.2 Siteimprove A/S

- 6.4.3 AudioEye, Inc.

- 6.4.4 Deque Systems, Inc.

- 6.4.5 UserWay Inc.

- 6.4.6 Monsido ApS

- 6.4.7 Crownpeak Technology, Inc.

- 6.4.8 Silktide Ltd.

- 6.4.9 accessiBe Ltd.

- 6.4.10 EqualWeb Ltd.

- 6.4.11 UsableNet, Inc.

- 6.4.12 TPGi, A Vispero Company

- 6.4.13 Allyant, Inc.

- 6.4.14 Google LLC

- 6.4.15 Microsoft Corporation

- 6.4.16 International Business Machines Corporation

- 6.4.17 WebAIM, Utah State University

- 6.4.18 Dubbot LLC

- 6.4.19 Applause App Quality, Inc.

- 6.4.20 Testlio, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment