|

시장보고서

상품코드

2044073

산업 안전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial Safety - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

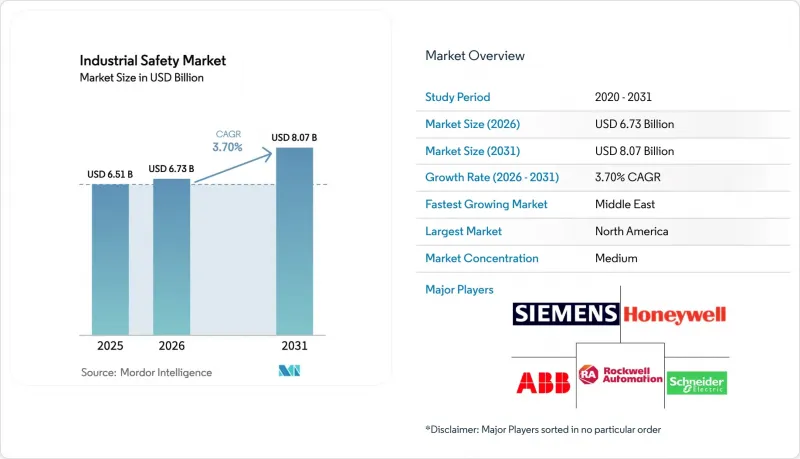

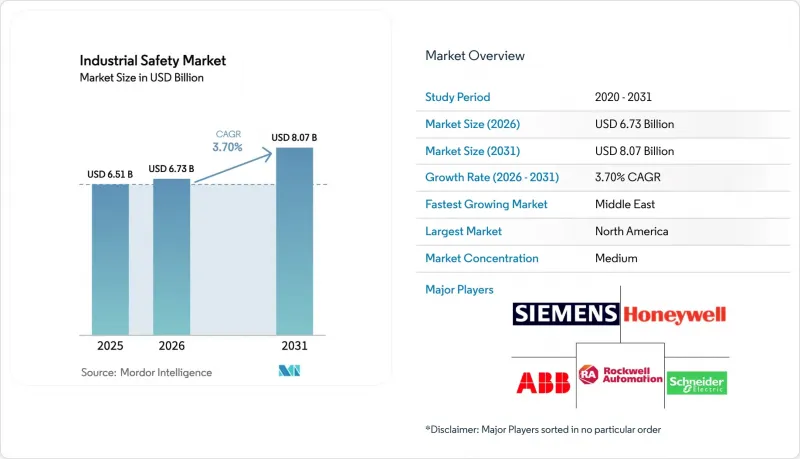

산업 안전 시장 규모는 2025년에 65억 1,000만 달러로 평가되었습니다. 2026년 67억 3,000만 달러에서 2031년까지 80억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 3.7%를 나타낼 전망입니다.

수요는 일회성 하드웨어 업그레이드에서 사이버 보안, 실시간 분석, 모듈식 리노베이션을 결합한 통합 안전 아키텍처로 이동하고 있으며, 이를 통해 사업자들은 점점 더 엄격해지는 인증 일정과 유럽 위원회의 ESG 공시 요건을 충족할 수 있습니다. 가능하게 합니다. 안전 센서는 여전히 하드웨어 스택의 기반이 되고 있지만, 라이프사이클 지원을 위한 다년 서비스 계약이 현재 가장 강력한 가격 결정력을 확보하고 있습니다. 비상 정지 플랫폼이 수익의 대부분을 차지하고 있지만, 수소, 제약, 심해 생산 사업자들이 과압 방어 시스템을 재설계하는 가운데 고신뢰성 압력 보호 시스템이 가장 빠른 단위 성장을 기록하고 있다(IEC). 지역별로는 북미가 가장 큰 지출 기반을 가지고 있지만, 사우디와 아랍에미레이트가 정부계 펀드의 지침에 따라 가장 빠르게 예산을 확대하고 있다(로이터). 각 벤더들은 엣지 대응 컨트롤러, 클라우드 분석, 플러그 앤 플레이 모듈 등을 출시하여 이에 대응하고 있으며, 이를 통해 기존 설비의 시운전 주기를 단축하고 총 도입비용을 절감하고 있습니다.

세계의 산업 안전 시장 동향과 인사이트

고위험 산업의 규제 압력 증가

유럽연합(EU)의 '기업 지속가능성 보고 지침'에 따라 5만 개 이상의 기업이 사고 데이터 공개를 의무화하고 있으며, 기능 안전에 대한 지출이 이사회 차원의 컴플라이언스 지표가 되고 있습니다. 미국에서는 2024년에 시작된 12개의 OSHA(산업안전보건국) 국가 중점 프로그램을 통해 위반 건당 최고 벌금이 16만 1,323달러로 인상되어 SIL(안전 수준) 인증을 받은 비상 정지 및 화재 및 가스 모니터링 프로젝트에 대한 자본 배분이 가속화되고 있습니다. 동시에 IEC 61511 2판은 안전 계측 시스템에 대한 위협 모델링을 의무화하여 사이버 보안의 허점을 막고, 기존 설비 운영 사업자에게 문서화와 네트워크 세분화 업그레이드를 요구하고 있습니다. 이에 대해 보험사들은 보험계약 갱신 시 기능안전감사를 포함시키고, 미준수 시설에 대해서는 보험료를 인상하는 대응을 하고 있습니다. 전반적으로 규제 집행의 가속화는 투자 회수 기간을 단축하고, 안전 대책의 업그레이드를 '임의 지출'에서 '필수 지출'로 격상시키고 있습니다.

IIoT, 로보틱스, 고도의 자동화 확산

2025년까지 127개 공정 플랜트에서 운영될 허니웰의 Forge 플랫폼은 실시간 원격 측정과 머신러닝 모델을 결합하여 밸브 및 액추에이터의 고장을 최대 14일 전에 예측하여 예기치 못한 다운타임을 약 5분의 1로 줄입니다. IEC 61508 SIL 2 인증을 획득한 ABB의 SafeMove2 로봇 제품군은 협업 작업에서 동적 속도 및 힘 제한을 가능하게 하며, 안전 요구 사항을 새로운 자동화 셀로 확장합니다. ABB. 이러한 디지털 레이어는 신뢰성을 향상시키는 한편, 사이버 공격의 표적이 될 수 있는 영역을 넓히고, 현재는 ISA/IEC 62443에 기반한 제어가 필요하며, 이로 인해 통합 비용이 두 자릿수 증가했습니다. ISA. 레거시 제어 시스템에 IIoT를 추가하는 기업은 데이터 사일로화의 위험에 노출되어 예측적 안전성을 확보할 수 없고, 근본적인 비즈니스 사례를 약화시킬 수 있습니다. 그럼에도 불구하고, 생산성의 이점은 복잡성 증가를 능가하여 예측 CAGR을 0.9% 상승시키는 효과를 가져옵니다.

SIL 인증 시스템의 높은 초기 설비투자

중규모 정유시설를 위한 SIL 3 비상정지 패키지 비용은 미화 420만-680만 달러이며, 제3자 검증에 미화 110만-190만 달러가 추가로 소요되어 SIL을 지원하지 않는 제어 시스템 업그레이드에 비해 3배 이상 비용이 증가합니다. 신흥 시장의 계약자는 현지 조달 규정으로 인해 재설계 또는 수입 면제가 필요한 미인증 밸브를 사용해야 하는 경우, 추가적인 부담에 직면하게 됩니다. 모듈식 사전 인증된 스키드는 설치 비용을 20% 절감할 수 있지만, 그 도입은 여전히 레이아웃이 유동적인 신규 건설 프로젝트에 편중되어 있습니다. 따라서 자금 부족으로 인해 공정 안전 위험이 가장 높은 자산의 업그레이드가 지연되어 산업 안전 시장의 CAGR이 0.8% 하락했습니다.

부문 분석

안전 센서는 IEC 61511의 중복성 규정으로 인해 SIL 3 루프의 검출기 수가 3배 증가함에 따라 2025년 매출의 33.37%를 차지했습니다. 컨트롤러 및 릴레이는 2위를 차지했으며, 제약 시설에 적합한 Pilz PSS 4000과 같은 컴팩트한 모듈식 설계가 그 뒤를 이었습니다. 밸브는 부분 스트로크 진단으로 오버홀 간격이 길어짐에 따라 밸브의 수명이 길어지고 있습니다. 한편, 배리어, 전원, HMI의 경우, 아시아 신규 업체들이 유럽과 미국의 기존 업체들보다 저렴한 가격으로 진입하고 있습니다. 서비스는 3.96%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 이는 다년 계약을 통해 내압 테스트, 펌웨어 업데이트, 예비 부품 풀을 패키지로 묶어 예측 가능한 수입원을 확보할 수 있기 때문입니다. 하니웰은 사이트 간 프레임워크 계약에 힘입어 2025년 라이프사이클 서비스 수주가 19% 증가했다고 보고했습니다. 컨설팅 및 교육은 4.02%의 성장률을 보이고 있으며, 심각한 인력 부족 속에서 TUV 인증 감사인은 높은 일당을 받고 있습니다.

'서비스형 계약'으로의 전환으로 수익률이 하드웨어에서 지속적인 수익으로 전환되고 있습니다. 공장에서 사전 테스트를 거친 스키드는 현장 작업 시간을 4분의 1로 줄였지만, 설치 비용은 여전히 서비스 지출의 30.53%를 차지합니다. 2010년 이전에 설치된 북미 안전 시스템의 40%가 현재 두 번째 내압 시험 주기를 앞두고 있어 유지보수 및 시험 업무가 확대되고 있습니다. 기존 장비 포트폴리오가 노후화되는 가운데, 현장 서비스 및 분석 기능을 결합한 벤더가 우선 공급업체 지위를 확보하고 전체 산업안전 시장에서 지갑 점유율을 확대하며 전환 비용을 높이고 있습니다.

정유 및 화학 API 분야에서 수십년동안 지속된 규제에 힘입어 비상 정지(ESD) 솔루션은 2025년 매출의 37.62%를 차지했습니다. 그 뒤를 이어 화재 및 가스 모니터링 솔루션이 뒤를 이었으며, 배선 비용을 절감하고 오작동을 60% 감소시키는 무선 감지기가 그 뒤를 잇고 있습니다. ESD 시스템 시장에서의 선도적 지위는 수십 년간의 도입 실적과 규제 정착을 반영하고 있습니다. 2017년 최종 개정된 미국석유협회(API)의 RP 14C 표준은 해양 플랫폼에 대한 ESD 로직을 규정하고 있으며, 유럽연합(EU)의 세베소 III 지침은 가연성 또는 독성 물질을 취급하는 상위 수준의 시설에 대해 ESD 인터록을 의무화하고 있습니다. 의무화하고 있습니다.

HIPPS는 4.11%의 가장 높은 CAGR을 기록했습니다. 이는 수소 파이프라인이나 무균 충전 및 마무리 설비에서 대기 중 배출로 인한 처벌을 피하기 위해 밀리초 단위의 차단이 요구되기 때문입니다. 버너 관리는 탈탄소화 프로젝트와 관련된 폐열 터빈 및 수소 터빈에서 그중요성이 커지고 있습니다. 고신뢰성 경보 관리 및 안전 계측 기능(SIF) 로직 솔버를 포함한 '기타 안전 시스템'은 SIL 4 인증이 필수적인 원자력 및 항공우주 분야에서 틈새 시장으로 채택되고 있지만, 전문 엔지니어링 요구 사항과 제한된 벤더 기반 때문에 전체 안전 시스템 매출에서 차지하는 비중은 8% 미만입니다. 전체 안전 시스템 매출에서 차지하는 비중은 8% 미만에 불과합니다.

지역별 분석

북미는 노후화된 정유시설가 밀집되어 있고, 빠른 업그레이드를 유도하는 OSHA의 벌칙 배율로 인해 2025년 산업안전 시장 점유율 33.73%를 차지했습니다. 캐나다의 오일샌드 생산업체들은 SAGD(증기압입(SAGD) 유정용 SIL 3 인터록에 9억 2천만 캐나다 달러(6억 8,000만 달러)를 투자하여 지역 내 지출 확대에 기여했습니다. 멕시코의 업스트림 광구 개방은 시운전 기간을 3분의 1로 단축하는 모듈식 안전 스키드를 핵심으로 하는 새로운 시설의 건설을 촉진하고 있습니다.

유럽에서는 세베소 III 규정 및 근로자 안전 정보 공개 의무에 따라 컴플라이언스가 추진되고 있습니다. 독일의 주요 화학업체들만 해도 2025년 안전 개보수를 위해 14억 유로(15억 달러)를 책정했습니다. 영국 보건안전집행국(HSE)은 내압시험이 지연되고 있는 사업자에게 78건의 개선 권고를 내리고 원격 밸브 진단 도입에 박차를 가하고 있습니다. 동유럽에서는 신규 프로젝트 예산 문제로 마찰을 빚고 있지만, EU의 보조금을 활용하여 수소 허브에 SIL-3 컨트롤러를 도입하고 있습니다.

중동은 2026년부터 2031년까지 4.19%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 사우디아라비아 공공투자기금(PIF)은 NEOM 산업 클러스터에 32억 달러를 투자했으며, ADNOC는 루와이스(Ruwais)의 14개 생산라인에 Ability System 800xA 컨트롤러와 SafeMove2 로봇 기술을 통합하여 엔지니어링 비용을 22% 절감했습니다. 아프리카는 남아공의 광업과 나이지리아의 업스트림 부문이 주도하고 있지만, 자금 제약과 TUV 인증 인력 부족으로 인해 여전히 개발 단계에 있습니다. 아시아태평양에서는 양극화 현상이 나타나고 있습니다. 중국과 인도는 수소 및 석유화학 산업 확장에 박차를 가하고 있으며, 동남아시아의 LNG 메가 프로젝트에서는 수출 금융을 확보하기 위해 SIL-2 검출기를 채택하고 있습니다. 남미에서는 Petrobras와 Baca Mujerta의 개발 사업자가 엔지니어링 인력 부족을 해결하기 위해 사전 인증된 스키드에 의존하고 있으며, 지출은 상품 가격 변동에 따라 변동하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe Industrial Safety market size is projected to be USD 6.51 billion in 2025, USD 6.73 billion in 2026, and reach USD 8.07 billion by 2031, growing at a CAGR of 3.7% from 2026 to 2031.

Demand is shifting from one-off hardware upgrades toward integrated safety architectures that combine cybersecurity, real-time analytics, and modular retrofits, enabling operators to satisfy tightening certification timelines and ESG disclosures EUROPEAN COMMISSION. Safety sensors still anchor the hardware stack, yet multiyear service contracts for lifecycle support now secure the strongest pricing power. Emergency Shutdown platforms dominate revenues, but High Integrity Pressure Protection Systems post the fastest unit growth as hydrogen, pharmaceutical, and deep-water producers re-engineer overpressure defenses IEC. Regionally, North America holds the largest spending base, whereas Saudi Arabia and the United Arab Emirates are scaling budgets the quickest under sovereign-fund mandates REUTERS. Vendors are responding with edge-ready controllers, cloud analytics, and plug-and-play modules that shorten brownfield commissioning cycles while lowering total installed cost.

Global Industrial Safety Market Trends and Insights

Increasing Regulatory Pressure Across High-Risk Industries

The European Union's Corporate Sustainability Reporting Directive obliges more than 50,000 firms to disclose incident data, turning functional-safety outlays into a board-level compliance metric. In the United States, twelve OSHA National Emphasis Programs launched in 2024 lifted maximum penalties to USD 161,323 per violation, accelerating capital allocation for SIL-rated Emergency Shutdown and Fire and Gas Monitoring projects. IEC 61511 Edition 2 simultaneously closed cybersecurity loopholes by mandating threat modeling for Safety Instrumented Systems, forcing brownfield operators to upgrade documentation and network segmentation IEC. Insurers have reacted by embedding functional-safety audits into policy renewals, raising premiums on non-compliant sites. Collectively, faster enforcement compresses return-on-investment horizons and elevates safety upgrades from discretionary to essential spending.

IIoT, Robotics and Advanced Automation Penetration

Honeywell's Forge platform, active across 127 process plants in 2025, combines live telemetry with machine-learning models that predict valve or actuator failure up to 14 days in advance, trimming unplanned downtime by nearly one-fifth. ABB's SafeMove2 robotics suite, certified to IEC 61508 SIL 2, enables dynamic speed and force limiting for collaborative tasks, expanding safety requirements to new automation cells ABB. While these digital layers improve reliability, they also widen the cyber-attack surface and now require ISA/IEC 62443 controls that add double-digit integration cost ISA. Enterprises that bolt IIoT onto legacy controls risk data silos that cannot drive predictive safety, weakening the underlying business case. Still, productivity benefits outweigh incremental complexity, securing a 0.9% positive lift on forecast CAGR.

High Upfront CAPEX for SIL-Rated Systems

A SIL 3 Emergency Shutdown package for a midsize refinery costs USD 4.2-6.8 million plus another USD 1.1-1.9 million for third-party verification, delivering a 3X premium over a non-SIL control upgrade. Emerging-market contractors face an added burden when local-content rules mandate uncertified valves that require redesign or import waivers. Modular, pre-certified skids can shave 20% off installed cost, yet adoption remains skewed to greenfield builds where layouts are still fluid. Capital scarcity, therefore, delays upgrades at the very assets that bear the highest process-safety risk, clipping 0.8% from the Industrial Safety market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Worker-Safety KPIs Embedded in ESG Scorecards

- Functional-Safety Certification Demand in Emerging Economies

- Complex Integration with Legacy PLC and DCS Assets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Safety sensors secured 33.37% of 2025 revenue as IEC 61511 redundancy rules tripled detector counts in SIL 3 loops IEC. Controllers and relays ranked second, spearheaded by compact, modular designs such as Pilz PSS 4000 that fit pharmaceutical suites. Valves lag as partial-stroke diagnostics extend overhaul intervals, while Asian entrants undercut Western incumbents on price for barriers, power supplies, and HMIs. Services post a 3.96% CAGR because multi-year contracts bundle proof tests, firmware updates, and spare pools, locking in predictable income streams. Honeywell reported a 19% jump in lifecycle-service bookings in 2025, driven by cross-site framework deals. Consulting and training advance at 4.02% as TUV-licensed auditors command premium day rates amid acute talent gaps.

The shift toward as-a-service engagement pulls margin from hardware into recurring revenue. Installation still holds 30.53% of service spend, although factory-pretested skids compress onsite labor by one-quarter. Maintenance and testing activities scale up because 40% of North American safety systems installed prior to 2010 are now approaching their second proof-test cycle. As brownfield portfolios age, vendors that bundle field services with analytics secure preferred-supplier status, deepening wallet share and raising switching costs across the Industrial Safety market.

Emergency Shutdown solutions generated 37.62% of 2025 revenue, underpinned by decades of regulatory entrenchment in refining and chemicals API. Fire and Gas Monitoring follows, boosted by wireless detectors that lower cabling cost and reduce false trips by 60%. ESD systems' market leadership reflects decades of installed base and regulatory entrenchment: the American Petroleum Institute's RP 14C standard, last revised in 2017, prescribes ESD logic for offshore platforms, while the European Union's Seveso III Directive mandates ESD interlocks for upper-tier establishments handling flammable or toxic substances.

HIPPS registers the strongest 4.11% CAGR as hydrogen pipelines and aseptic fill-finish suites require millisecond-level cutoffs to avert vent-to-atmosphere penalties. Burner Management gains relevance in waste-heat and hydrogen turbines tied to decarbonization projects. Other Safety Systems, encompassing High Integrity Alarm Management and Safety Instrumented Function logic solvers, are seeing niche adoption in nuclear and aerospace applications where SIL 4 certification is mandatory, but account for less than 8% of total safety-system revenue due to their specialized engineering requirements and limited vendor base.

The Industrial Safety Market Report is Segmented by Component (Safety Sensors, and More), Safety System (Emergency Shutdown, Fire and Gas Monitoring, and More), Service (Installation and Commissioning, and More), Security Level (SIL 1, and More), End-User Industry (Oil and Gas, Energy and Power, Chemicals and Petrochemicals, Metals and Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 33.73% of the Industrial Safety market share in 2025, thanks to a dense base of aging refineries and OSHA penalty multipliers that motivate rapid upgrades. Canada's oil sands producers invested CAD 920 million (USD 680 million) in SIL 3 interlocks for steam-assisted gravity drainage wells, extending the capture of regional spend. Mexico's opening of upstream acreage sparks new facilities designed around modular safety skids that cut commissioning by one-third.

Europe advances compliance under Seveso III and worker-safety disclosure mandates. Germany's chemical majors alone earmarked EUR 1.4 billion (USD 1.5 billion) for safety upgrades in 2025. The United Kingdom's Health and Safety Executive served 78 improvement notices to operators behind on proof testing, accelerating adoption of remote valve diagnostics. Eastern Europe faces budget friction on greenfield projects, but leverages EU grants to embed SIL-3 controllers in hydrogen hubs.

The Middle East logs the fastest 4.19% CAGR throughout 2026-2031. Saudi Arabia's Public Investment Fund devoted USD 3.2 billion to NEOM industrial clusters, while ADNOC integrates Ability System 800xA controllers and SafeMove2 robotics across 14 Ruwais trains, shaving 22% engineering cost. Africa, led by South Africa's mining and Nigeria's upstream sectors, remains nascent due to capital constraints and a shortage of TUV-certified talent. Asia Pacific displays bifurcation: China and India accelerate under hydrogen and petrochemical expansions, whereas Southeast Asian LNG megaprojects employ SIL-2 detectors to unlock export financing. South America cycles spend with commodity prices, as Petrobras and Vaca Muerta developers rely on pre-certified skids to counter engineering shortages.

- Schneider Electric SE

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- ABB Ltd.

- Emerson Electric Co.

- Baker Hughes Company

- HIMA Paul Hildebrandt GmbH

- Yokogawa Electric Corporation

- Omron Corporation

- Johnson Controls International plc

- Balluff GmbH

- Keyence Corporation

- IDEC Corporation

- SICK AG

- Mitsubishi Electric Corporation

- Endress+Hauser AG

- Pilz GmbH & Co. KG

- Pepperl+Fuchs SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Regulatory Pressure Across High-Risk Industries

- 4.2.2 IIoT, Robotics And Advanced Automation Penetration

- 4.2.3 Worker-Safety Kpis Embedded In ESG Scorecards

- 4.2.4 Functional-Safety Certification Demand In Emerging Economies

- 4.2.5 Cyber-Secure Safety System Architectures

- 4.2.6 Retrofit-Friendly, Modular Safety Plug-Ins

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX For SIL-Rated Systems

- 4.3.2 Complex Integration With Legacy PLC/DCS

- 4.3.3 Scarcity Of TUV-Certified Functional-Safety Engineers

- 4.3.4 ROI Uncertainty In Low-Incident Industries

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Safety Sensors

- 5.1.2 Safety Controllers and Relays

- 5.1.3 Safety Valves

- 5.1.4 Other Components

- 5.2 By Safety System

- 5.2.1 Emergency Shutdown (ESD)

- 5.2.2 Fire and Gas Monitoring

- 5.2.3 High Integrity Pressure Protection (HIPPS)

- 5.2.4 Burner Management Systems (BMS)

- 5.2.5 Other Safety Systems

- 5.3 By Service

- 5.3.1 Installation and Commissioning

- 5.3.2 Consulting and Training

- 5.3.3 Maintenance and Support

- 5.3.4 Testing and Inspection

- 5.4 By Security Level (SIL)

- 5.4.1 SIL 1

- 5.4.2 SIL 2

- 5.4.3 SIL 3

- 5.4.4 SIL 4

- 5.5 By End-user Industry

- 5.5.1 Bottles And Jars

- 5.5.2 Oil and Gas

- 5.5.2.1 Caps And Closures

- 5.5.3 Energy and Power

- 5.5.3.1 Bulk-Grade Products

- 5.5.4 Chemicals and Petrochemicals

- 5.5.4.1 Other Rigid Plastics Product Types

- 5.5.5 Metals and Mining

- 5.5.6 Food and Beverage

- 5.5.6.1 Pouches

- 5.5.7 Pharmaceutical and Healthcare

- 5.5.7.1 Bags

- 5.5.8 Automotive

- 5.5.8.1 Films And Wraps

- 5.5.9 Aerospace and Defense

- 5.5.9.1 Other Flexible Plastics Product Types

- 5.5.10 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share For Key companies, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Honeywell International Inc.

- 6.4.3 Rockwell Automation Inc.

- 6.4.4 Siemens AG

- 6.4.5 ABB Ltd.

- 6.4.6 Emerson Electric Co.

- 6.4.7 Baker Hughes Company

- 6.4.8 HIMA Paul Hildebrandt GmbH

- 6.4.9 Yokogawa Electric Corporation

- 6.4.10 Omron Corporation

- 6.4.11 Johnson Controls International plc

- 6.4.12 Balluff GmbH

- 6.4.13 Keyence Corporation

- 6.4.14 IDEC Corporation

- 6.4.15 SICK AG

- 6.4.16 Mitsubishi Electric Corporation

- 6.4.17 Endress+Hauser AG

- 6.4.18 Pilz GmbH & Co. KG

- 6.4.19 Pepperl+Fuchs SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment