|

시장보고서

상품코드

2044076

팟캐스트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Podcasting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

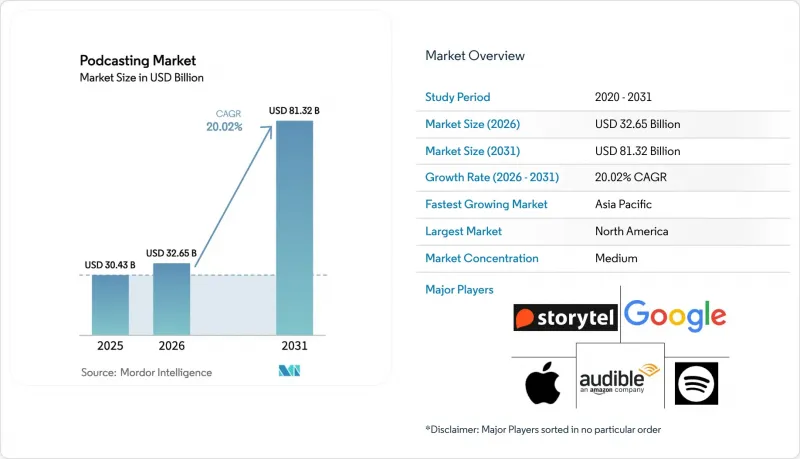

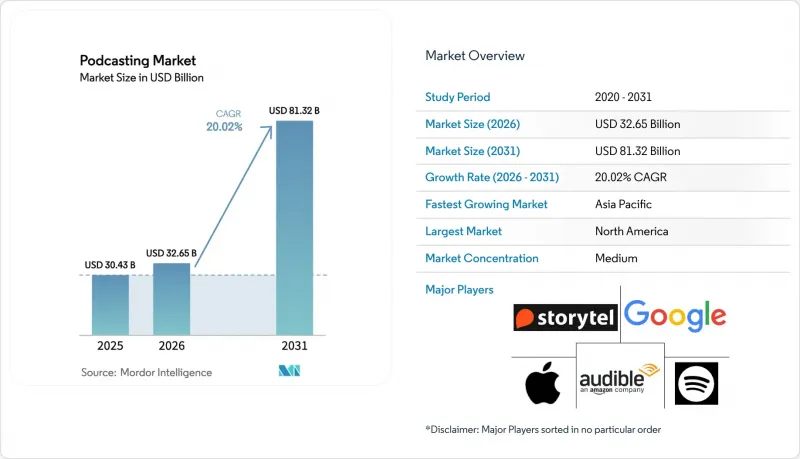

팟캐스트 시장 규모는 2025년 304억 3,000만 달러, 2026년 326억 5,000만 달러에서 2031년까지 813억 2,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 20.02%를 나타낼 전망입니다.

이러한 견조한 성장은 기존 TV의 광고비가 비디오 팟캐스트로 이동하고, 프로그래매틱 오디오 인프라가 빠르게 구축되고, 팟캐스트가 스마트 스피커와 커넥티드 TV의 생태계에 깊숙이 통합되고 있음을 반영합니다. 동영상 CPM(노출 단가)이 높을수록 에피소드당 총 수익이 향상되고, 유통 리스크가 분산되어 플랫폼의 경제성은 음성과 동영상을 모두 유통하는 크리에이터에게 유리한 방향으로 이동하고 있습니다. 또한, 동적 광고 삽입 툴을 통해 브랜드가 지역, 기기, 시간대별로 청취자를 타겟팅하는 동시에 호스트가 직접 읽어주는 진정성 있는 분위기를 유지할 수 있게 되면서 광고주들 수요도 증가하고 있습니다. 공급 측면에서는 압축 효율의 향상과 클라우드 편집 툴로 인해 제작 비용이 절감되어 더 많은 크리에이터들이 시즌 내내 시청자의 관심을 유지할 수 있는 연속극을 제작하고 있습니다.

세계 팟캐스트 시장 동향과 인사이트

유튜브 및 커넥티드 TV 플랫폼에서 동영상 팟캐스트의 수익화 확대 추진

광고주들이 온라인에서 젊은 시청자를 쫓는 가운데, 비디오 팟캐스트는 TV 방송에서 브랜드 예산을 빼앗아 가고 있습니다. 현재 고화질 촬영 비용은 TV 스튜디오 제작 비용의 몇 분의 1에 불과하며, 크리에이터는 기존 오디오 광고 단가의 거의 두 배에 달하는 에피소드당 약 35달러의 CPM을 얻을 수 있게 되었습니다. Roku와 Amazon Fire TV는 팟캐스트 시청 시간이 두 자릿수 성장을 기록하고 있으며, 거실 시청자들이 장편 에피소드를 틈새 케이블 채널처럼 취급하고 있음이 입증되고 있습니다. 크리에이터는 이중의 수익화 혜택을 누리고 있습니다. 왜냐하면, 같은 컨텐츠가 Spotify나 Apple Podcasts에서는 오디오로 제공되지만, 유튜브에서는 프리롤과 미드롤에 동영상 광고가 추가되기 때문입니다. 16:9 포맷으로 녹화하는 호스트가 늘어남에 따라 팟캐스트 시장은 RSS 기반 배포를 포기하지 않고 유튜브의 장편 엔터테인먼트와의 경쟁을 심화시키고 있습니다.

북미에서 프로그래매틱 오디오 광고 구매의 보급률은 35% 이상입니다.

자동화된 광고 구매는 디스플레이 광고와 검색 광고 캠페인에 익숙한 브랜드 관리자에게 팟캐스트 광고 게재가 간소화됩니다. 현재 DSP(Demand Side Platform)와 SSP(Supply Side Platform)는 팟캐스트 광고?을 옴니채널 대시보드에 통합하여 대행사들이 실시간으로 노출 빈도를 최적화할 수 있도록 하고 있습니다. 동적 광고 삽입은 청취자프로파일에 맞추어 메시지를 전달하기 때문에 호스트가 읽어주는 기존의 고정형 스팟 광고에 비해 전환율을 높일 수 있습니다. 독립 크리에이터들은 캐스트와 메가폰의 셀프 서비스형 마켓플레이스를 활용하고 있습니다. 이를 통해 이전에는 상위 10명의 크리에이터에게만 한정되었던 프리미엄 광고 수요가 일반인에게도 개방되고 있습니다. 유럽에서 GDPR(EU 개인정보보호규정)을 준수하는 타겟팅이 의무화되고, 아시아태평양에서도 유사한 거래소가 등장함에 따라 전 세계 프로그램matic 광고의 점유율이 북미 기준치를 넘어서면서 전체 팟캐스트 시장의 수익을 끌어올릴 것으로 예측됩니다.

유럽 내 허위정보 규제에 따른 컨텐츠 검열 비용 증가

디지털 서비스법(DSA)과 유럽 미디어 자유법(EMFA)에 따라 플랫폼은 심사위원 고용, AI 필터 도입, 투명성 보고서 발행을 의무화하고 있으며, 중간 규모의 호스팅 업체는 연간 5만-20만 유로(5만3,000-21만2,000달러)의 컴플라이언스 비용이 추가되고 있습니다. 소규모 업체들은 이러한 비용을 흡수하기 위해 고군분투하고 있으며, 퇴출과 합병을 강요당하고 있어 크리에이터들의 선택의 폭이 좁아지고 있습니다. 역외 적용 규정에 따라 EU 역외 기업이라도 법정대리인을 선임해야 하며, 이는 국경을 넘어선 사업 확장에 걸림돌이 되고 있습니다. 이에 따라 크리에이터들은 삭제 위험이 있는 논란의 소지가 있는 주제를 자율적으로 규제하게 되어 컨텐츠의 다양성이 훼손될 우려가 있습니다. 그 결과, 유럽의 매출 성장은 다른 선진 지역에 비해 둔화되고 있습니다.

부문 분석

'트루 크라임'은 깊이 있고 연속성 있는 스토리로 시대의 공기를 담아내어 캐주얼 리스너를 단숨에 듣는 팬과 프리미엄 구독자로 만들었습니다. 이 부문의 CAGR 20.62%는 여러 시즌에 걸친 탐사보도 및 법정 드라마에 대한 스튜디오의 투자 확대를 반영하고 있으며, 이는 종종 다큐멘터리와 책으로 제작되는 경우가 많습니다. 평균 CPM이 42달러에 달하는 것은 광고주들이 열성적인 청취자 층을 강력하게 원하고 있다는 것을 입증합니다. 뉴스/정치 장르가 여전히 팟캐스트 시장 점유율의 가장 큰 부분을 차지하고 있지만, 당파성 대립으로 인해 습관적 청취가 분열되어 청취자 수 증가가 정체되고 있습니다. 코미디, 스포츠, 사회문제 관련 컨텐츠는 여전히 호황을 누리고 있지만, 숏폼 동영상 플랫폼과의 경쟁이 심화되고 있습니다.

핀테크 앱, D2C(소비자직접판매) 브랜드 등 광고주들은 높은 완시청률과 여성층에 편중된 시청자층을 이유로 '트루클라이밍'을 선호하고 있습니다. Wonder와 Parcast와 같은 스튜디오는 국제적인 현지화 버전을 출시하고 있으며, 남미와 유럽에서 다국어 개발을 지원하고 있습니다. 한편, 다큐멘터리 스타일의 내러티브 방식이 비즈니스, 테크놀로지, 헬스케어 장르에도 파급되어 팟캐스트 시장 전체의 제작 수준을 끌어올리고 있습니다. 스토리텔링 스타일이 다양해짐에 따라 얼리어답터 층을 넘어 도달 범위가 넓어지고, 크리에이터의 평생 가치가 안정화되고 있습니다.

내러티브 및 스토리텔링 프로그램은 CAGR 20.88%로 성장하며 청취자 수 증가율에서 인터뷰 형식을 추월했습니다. 라이터룸, 폴리 아티스트, 라이선싱이 완료된 곡에 대한 투자로 제작의 질은 오디오북 수준의 수준으로 향상되고 있습니다. 광고주들은 광고 스킵률 감소에 대한 보상으로 미드롤 CPM을 25% 이상 인상하여 이 포맷의 프리미엄 포지셔닝을 강화하고 있습니다. 인터뷰 형식의 팟캐스트는 설치비용이 저렴하고, 매주 쉽게 배포할 수 있다는 장점으로 인해 여전히 많은 수의 구독자를 확보하고 있으며, 팟캐스트 시장 전체에 안정적인 광고 인벤토리를 제공합니다.

하이브리드 형식은 라이브 패널과 대본에 기반한 스토리 전개를 결합한 것으로, 시각적 요소가 참여도를 높이는 유튜브에서 인기 있는 구조입니다. 솔로 모노로그는 오피니언 리더를 대상으로 마스터 클래스 형식의 인사이트를 제공하는 한편, 대담 형식의 패널 쇼는 라이브 스트리밍 중 시청자 채팅을 활용하여 사용자 생성 질문을 다루고 있습니다. 모든 포맷에서 크리에이터들은 음성과 동시에 4K 영상을 촬영하는 경우가 증가하고 있으며, 팟캐스트 앱, 유튜브, 커넥티드 TV 채널에 배포하는 것을 최대한 활용하고 있습니다.

지역별 분석

북미는 2025년 매출의 45.61%, 디지털 광고 예산의 3분의 1 이상을 차지하고, 팟캐스트 인벤토리로 유도하는 프로그래매틱 오디오가 그 뒤를 이을 것으로 보입니다. 미국은 대규모 광고주 기반과 성숙한 DSP-SSP 인프라 덕분에 여전히 중심지로서의 지위를 유지하고 있습니다. 캐나다와 멕시코는 영어와 스페인어, 영어와 프랑스어 컨텐츠를 활용하여 캠페인의 도달 범위를 확장하고 이중 언어 성장을 가져왔습니다. 스마트 스피커의 높은 보급률로 인해 팟캐스트는 가정의 일상에 자리 잡았고, 사용자 1인당 평균 청취 시간을 늘리며 프리미엄 CPM을 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 21.25%로 지역별로 가장 높은 성장세를 보이고 있습니다. 일본에서는 기업이 경영진을 호스트 삼아 브랜드 팟캐스트를 주도하고 있으며, 인도와 중국에서는 기술직 종사자나 통근자에게 적합한 단편 에피소드 형식을 통해 보급이 진행되고 있습니다. 중국 내 Ximalaya의 월간 사용자 수 2억 8,000만 명은 오디오북과 팟캐스트를 융합한 하이브리드 플랫폼의 가능성을 보여주고 있습니다. 동남아시아에서는 에피소드를 30MB 미만으로 압축하여 모바일 대역폭의 제약을 완화하고, 저렴한 요금제를 통해 지방 도시와 농촌 지역까지 도달 범위를 넓히고 있습니다.

유럽에서는 '디지털 서비스법'에 대한 컴플라이언스 부담으로 인해 중간 규모 호스트의 운영 비용이 증가하면서 성장이 둔화되고 있습니다. 독일은 실화 범죄와 탐사보도 분야의 소비를 주도하고 있는 반면, 영국은 코미디와 패널 형식의 프로그램에 강점을 가지고 있습니다. 남미에서는 브라질과 아르헨티나에서 스페인어와 포르투갈어 시리즈가 3배로 증가하는 등 언어 중심의 붐이 일어나고 있습니다. 아랍에미리트(UAE) 등 중동 시장에서는 정부 지원의 팟캐스트 인큐베이터가 시범적으로 도입되고 있지만, 보급은 스마트폰 이용률이 높은 도시 지역에 집중되어 있습니다. 아프리카는 차량용 커넥티비티가 탑재된 차량이 18%에 불과하고, 모바일 데이터 요금이 여전히 비싸고, 다른 지역에서 지속적 청취를 촉진하는 시간대에는 이용이 제한되어 있어 뒤쳐져 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The podcasting market size is projected to expand from USD 30.43 billion in 2025 and USD 32.65 billion in 2026 to USD 81.32 billion by 2031, registering a CAGR of 20.02% between 2026-2031.

Robust growth reflects the migration of linear-television dollars into video podcasts, the rapid rollout of programmatic audio infrastructure, and the deepening integration of podcasts into smart-speaker and connected-TV ecosystems. Platform economics are shifting in favor of creators who deliver both audio and video, because higher video CPMs lift overall revenue per episode and diversify distribution risk. Advertiser demand is also rising as dynamic ad-insertion tools let brands target listeners by geography, device, and daypart while still preserving host-read authenticity. On the supply side, greater compression efficiency and cloud editing tools reduce production costs, encouraging more creators to launch serialized shows that keep audiences engaged across seasons.

Global Podcasting Market Trends and Insights

Growing Monetization of Video Podcasts on YouTube and Connected-TV Platforms

Video podcasts are siphoning brand budgets away from broadcast television as advertisers follow younger viewers online. High-definition filming now costs a fraction of studio television, letting creators capture CPMs near USD 35, almost double traditional audio rates. Roku and Amazon Fire TV report double-digit growth in podcast viewing hours, proving that living-room audiences treat long-form episodes like niche cable channels. Creators benefit from dual monetization because the same content streams as audio on Spotify and Apple Podcasts while adding pre-roll and mid-roll video inventory on YouTube. As more hosts record in 16:9 formats, the podcasting market deepens its competition with YouTube long-form entertainment without abandoning RSS-based distribution.

Programmatic Audio Ad Buying Penetration Exceeding 35 Percent in North America

Automated ad buying simplifies podcast placement for brand managers used to display and search campaigns. Demand-side and supply-side platforms now stitch podcast inventory into omnichannel dashboards, letting agencies optimize frequency in real time. Dynamic ad insertion pins messages to listener profiles, boosting conversion rates compared with evergreen host-read spots. Independent creators tap self-service marketplaces on Acast and Megaphone, which democratize premium ad demand previously reserved for the top 10. As Europe enforces GDPR-compliant targeting and Asia-Pacific rolls out similar exchanges, global programmatic share is set to climb beyond North America's benchmark, lifting overall podcasting market revenue.

Heightened Content Moderation Costs Amid Misinformation Regulations in Europe

The Digital Services Act and the European Media Freedom Act force platforms to hire reviewers, deploy AI filters, and issue transparency reports, adding annual compliance costs between EUR 50,000 and 200,000 (USD 53,000-212,000) for mid-size hosts. Small providers struggle to absorb these expenses, prompting exits or mergers that shrink creator choice. Extraterritorial provisions mean even non-EU firms must appoint legal representatives, deterring cross-border expansion. Creators respond by self-censoring controversial topics that risk takedown, which could dilute content diversity. The result is slower European revenue growth compared with other developed regions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Smart Speakers in Gen Z Households

- Corporate Communications Pivot to Branded Podcasts in Asia-Pacific Multinationals

- Low In-Car Internet Penetration Limiting Listenership in Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

True Crime captured the zeitgeist with deeply serialized narratives that transform casual listeners into binge cohorts and premium subscribers. The segment's 20.62% CAGR reflects growing studio investment in multi-season investigations and courtroom dramas, often spun off into documentaries or book deals. CPMs averaging USD 42 validate advertiser appetite for hyper-engaged audiences. While News and Politics retains the largest slice of the podcasting market share, audience growth there is flattening as partisanship fragments habitual listening. Comedy, Sports, and Society content remain vibrant but face fiercer competition from short-form video platforms.

Advertisers like fintech apps and direct-to-consumer brands prioritize True Crime due to high completion rates and female-skewing demographics. Studios such as Wondery and Parcast release international localizations, supporting multilanguage growth in South America and Europe. Meanwhile, documentary-style narrative techniques spill into Business, Technology, and Health genres, raising overall production standards across the podcasting market. The diversification of storytelling styles is broadening reach beyond early-adopter segments and stabilizing lifetime value for creators.

Narrative and Storytelling show advances at a 20.88% CAGR, overtaking the interview format in listener growth. Investments in writers' rooms, foley artists, and licensed scores elevate production values to near-audiobook quality. Advertisers reward the reduced ad-skipping with mid-roll CPM uplifts above 25%, reinforcing the format's premium positioning. Interview podcasts still dominate output volume because of low setup costs and the ease of weekly releases, supporting stable advertiser inventory for the broader podcasting market.

Hybrid formats blend live panels with scripted narrative arcs, a structure popular on YouTube where visual cues amplify engagement. Solo monologues cater to thought leaders offering master-class-style insight, while conversational panel shows leverage audience chat on live streams to surface user-generated questions. Across every format, creators increasingly capture 4K video simultaneously with audio, maximizing distribution across podcast apps, YouTube, and connected-TV channels.

The Podcasting Market Report is Segmented by Genre (News and Politics, Comedy, Society and Culture, and More), Format (Interview, Conversational/Panel, and More), Revenue Model (Advertising-Supported, Subscription-Based, and More, Device/Access Point (Smartphones, Computers and Laptops, and More)), End-User Sector (Consumer Media and Entertainment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 45.61% of 2025 revenue, buoyed by programmatic audio, which accounts for over one-third of digital ad budgets and funnels them into podcast inventory. The United States remains the epicenter thanks to a large advertiser base and mature DSP-SSP infrastructure. Canada and Mexico add bilingual growth, leveraging English-Spanish and English-French content to extend campaign reach. High smart-speaker adoption embeds podcasts into household routines, lifting average listening hours per user and supporting premium CPMs.

Asia-Pacific posts the highest regional CAGR at 21.25% through 2031. Japan's corporates spearhead branded podcasts featuring executive hosts, while India and China spread adoption via technology workforces and commuter-friendly short-episode formats. Ximalaya's 280 million monthly users in China showcase the potential of hybrid audiobook-podcast platforms. In Southeast Asia, mobile bandwidth constraints are mitigated by sub-30 MB episode compression, expanding reach into secondary cities and rural districts with affordable data plans.

Europe is growing more slowly due to the compliance burden of the Digital Services Act, which increases operating costs for mid-size hosts. Germany leads consumption in true crime and investigative journalism, whereas the United Kingdom excels in comedy and panel formats. South America witnesses a language-led boom as Spanish and Portuguese series triple output in Brazil and Argentina. Middle East markets like the United Arab Emirates pilot government-backed podcast incubators, yet adoption concentrates in urban areas with high smartphone usage. Africa trails because only 18% of vehicles have in-car connectivity and mobile data prices remain high, limiting the daypart that elsewhere fuels sustained listening.

- Apple Inc.

- Spotify AB

- Amazon.com Inc. (Audible and Amazon Music)

- Google LLC

- iHeartMedia Inc.

- Sirius XM Holdings Inc. (Stitcher)

- Acast AB

- Podbean LLC

- Anchor FM Inc.

- Megaphone LLC

- Wondery LLC

- Luminary Media LLC

- TuneIn Inc.

- Pandora Media LLC

- Cumulus Media Inc. (Westwood One Podcast Network)

- PRX Public Radio Exchange

- Tencent Holdings Ltd. (Ximalaya)

- Castbox FM Pte. Ltd.

- Buzzsprout (Higher Pixels Inc.)

- Libsyn Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Monetization of Video Podcasts on YouTube and Connected-TV Platforms

- 4.2.2 Programmatic Audio Ad Buying Penetration Exceeding 35 Percent in North America

- 4.2.3 Rising Adoption of Smart Speakers in Gen Z Households, Especially United States and United Kingdom

- 4.2.4 Corporate Communications Pivot to Branded Podcasts in Asia-Pacific Multinationals

- 4.2.5 Surging Demand for Local-Language Podcasts Across South America

- 4.2.6 Sub-30 MB Mobile Episode Compression Improving Reach in Emerging Asia

- 4.3 Market Restraints

- 4.3.1 Heightened Content Moderation Costs Amid Misinformation Regulations in Europe

- 4.3.2 Low In-Car Internet Penetration Limiting Listenership in Africa

- 4.3.3 Fragmented Rights Management for Cross-Border Podcast Licensing

- 4.3.4 Apple and Spotify Store Commission Structures Squeezing Independent Creators

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Genre

- 5.1.1 News and Politics

- 5.1.2 Comedy

- 5.1.3 Society and Culture

- 5.1.4 True Crime

- 5.1.5 Sports

- 5.1.6 Education

- 5.1.7 Health and Wellness

- 5.1.8 Technology

- 5.1.9 Business and Finance

- 5.1.10 Arts and Entertainment

- 5.2 By Format

- 5.2.1 Interview

- 5.2.2 Conversational / Panel

- 5.2.3 Solo Monologue

- 5.2.4 Narrative / Storytelling

- 5.2.5 Hybrid / Experimental

- 5.3 By Revenue Model

- 5.3.1 Advertising-Supported

- 5.3.2 Subscription-Based

- 5.3.3 Crowdfunding and Donations

- 5.3.4 Branded and Corporate-Sponsored

- 5.4 By Device / Access Point

- 5.4.1 Smartphones

- 5.4.2 Computers and Laptops

- 5.4.3 Smart Speakers

- 5.4.4 Connected TVs

- 5.4.5 In-Car Infotainment Systems

- 5.4.6 Wearables

- 5.5 By End-User Sector

- 5.5.1 Consumer Media and Entertainment

- 5.5.2 Education and E-Learning Institutions

- 5.5.3 Corporations and Enterprises

- 5.5.4 Non-Profit and Government Organizations

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Spotify AB

- 6.4.3 Amazon.com Inc. (Audible and Amazon Music)

- 6.4.4 Google LLC

- 6.4.5 iHeartMedia Inc.

- 6.4.6 Sirius XM Holdings Inc. (Stitcher)

- 6.4.7 Acast AB

- 6.4.8 Podbean LLC

- 6.4.9 Anchor FM Inc.

- 6.4.10 Megaphone LLC

- 6.4.11 Wondery LLC

- 6.4.12 Luminary Media LLC

- 6.4.13 TuneIn Inc.

- 6.4.14 Pandora Media LLC

- 6.4.15 Cumulus Media Inc. (Westwood One Podcast Network)

- 6.4.16 PRX Public Radio Exchange

- 6.4.17 Tencent Holdings Ltd. (Ximalaya)

- 6.4.18 Castbox FM Pte. Ltd.

- 6.4.19 Buzzsprout (Higher Pixels Inc.)

- 6.4.20 Libsyn Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment