|

시장보고서

상품코드

2044081

웹 호스팅 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Web Hosting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

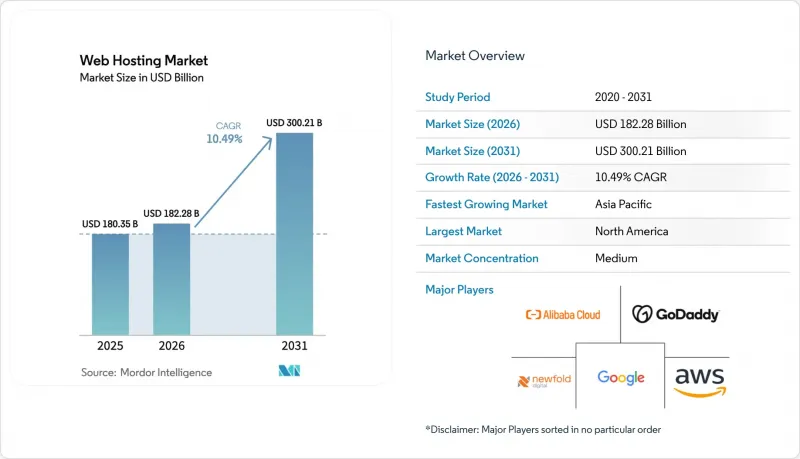

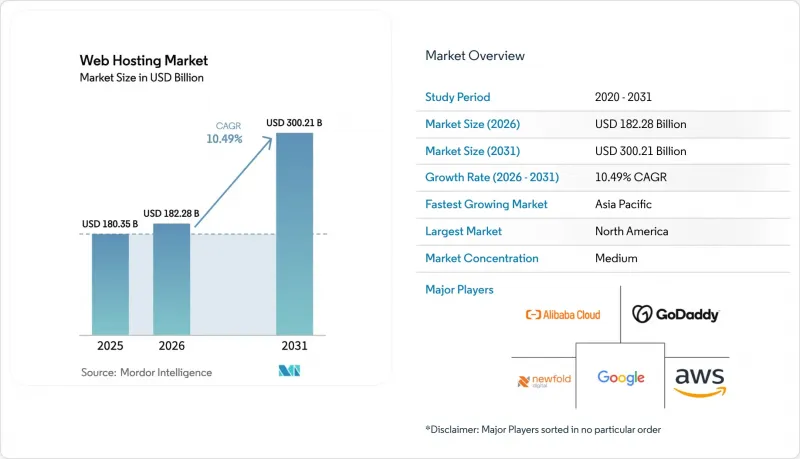

웹 호스팅 시장 규모는 2025년에 1,803억 5,000만 달러로 평가되었습니다. 2026년 1,822억 8,000만 달러에서 2031년까지 3,002억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 10.49%를 나타낼 전망입니다.

생성형 AI 워크로드 도입이 증가함에 따라 기업들은 기존 공유 서버로는 대응할 수 없는 GPU 지원 엣지 인프라로 전환하고 있습니다. 유럽연합(EU), 인도, 중국의 데이터 거주지 규제로 인해 기업들이 On-Premise, 소버린 클라우드, 하이퍼스케일 클라우드로 용도를 분산시키면서 하이브리드 구축이 가속화되고 있습니다. 노코드 플랫폼에서 디지털 스토어를 운영하는 소규모 사업자들은 99.99%의 가동률을 원하고 있으며, 이에 따라 지출이 클라우드 및 관리형 워드프레스 플랜으로 이동하고 있습니다. 기본적인 가동률 보장은 더 이상 필수 조건이 아니기 때문에 각 공급업체들은 이제 번들로 제공되는 가시성 도구와 탄소중립 인증을 위해 경쟁하고 있습니다.

세계의 웹 호스팅 시장 동향 및 인사이트

중소기업의 전자상거래 폭발적 확대

2024년 말 기준, 노코드 커머스 플랫폼을 사용하는 전 세계 사업자는 460만 개에 달했으며, 공급자는 플래시 세일 시 트래픽을 흡수할 수 있는 탄력적인 인프라를 제공해야 합니다. 소규모 소매업체들은 이제 PCI-DSS 스캔과 통합 결제 게이트웨이를 포함한 번들 솔루션을 기대하고 있으며, 그 가치는 단순한 서버 용량에서 즉시 사용 가능한 스토어 프론트 환경 제공으로 옮겨가고 있습니다. 엔드투엔드 커머스 스위트에 호스팅 기능을 통합한 업체들은 DevOps 담당자가 없는 사업자들 사이에서 점유율을 확대되고 있습니다. 동남아시아의 크로스보더 EC에서는 지연시간을 100밀리초 미만으로 낮추기 위해 엣지 거점이 필요하며, 지역 데이터센터 구축이 촉진되고 있습니다. 월간 구독 계약은 소매업체의 민첩성을 높여주지만, 호스트 사업자에게는 해약 위험을 증가시키기 때문에 예측 가능한 고객 유지 도구에 대한 투자를 촉구하고 있습니다.

고가용성 및 저지연 사이트에 대한 수요 급증

금융 규제 당국은 현재 디지털 채널의 가동 시간을 컴플라이언스 지표로 분류하고 있으며, 유럽은행감독청(EBA) 규정은 은행에 99.95%의 가용성을 요구하고 있습니다. 동영상 스트리밍, 실시간 게임, 원격 의료는 사용자로부터 50km 이내의 엣지 캐싱에 의존하고 있으며, 이를 대규모로 제공할 수 있는 것은 하이퍼스케일러와 성숙한 CDN 사업자들뿐입니다. 서버리스 컴퓨팅의 등장으로 전 세계 분산 실행이 보편화되면서 단일 지역의 오리진 서버로 인한 병목현상이 사라졌습니다. 자율주행차 및 산업용 IoT와 같은 지연에 민감한 워크로드에는 5G 통합형 엣지 호스팅이 필요하지만, 기존의 공유 호스팅으로는 이 간극을 메우기가 어렵습니다. 지연시간과 오류율을 실시간으로 가시화하는 가시성 대시보드는 기본적인 가동률 보장 이상의 차별화 요소로 작용하고 있습니다.

클라우드 공인 호스팅 엔지니어 부족이 심각합니다.

LinkedIn의 보고서에 따르면, 2025년에는 클라우드 아키텍처 기술에 대한 수요가 공급보다 2.3배 더 많았습니다. 15만 달러가 넘는 평균 연봉은 엔지니어들을 호스팅 업체에서 핀테크 기업이나 SaaS 유니콘 기업으로 끌어들이고 있습니다. 인력이 부족한 팀은 고객이 기대하는 자동화 프로젝트를 지연시키고, 수개월에 걸친 재교육 프로그램은 불확실한 결과만 낳을 수 있습니다. 원격근무로 인해 기존의 임금 격차가 줄어들고, 자격만으로는 더 이상 능력을 보장할 수 없기 때문에 채용 주기가 길어지고 있습니다.

부문 분석

2025년 공유 호스팅은 매출의 37.28%를 차지했지만, 엔트리 레벨 사용자조차도 자동 확장 및 강력한 보안을 제공하는 클라우드 플랫폼으로 이동함에 따라 이 부문은 점유율이 줄어들고 있습니다. 클라우드 호스팅은 연평균 10.53% 성장할 것으로 예상되며, 2031년까지 웹 호스팅 시장에서 상당한 점유율을 차지할 것으로 예측됩니다. VPS 및 전용 호스팅은 루트 액세스를 원하는 개발자와 단일 테넌트 하드웨어를 필요로 하는 규제 산업에서 틈새 시장을 형성하고 있습니다. 코로케이션은 시설 운영을 외부에 위탁하면서 물리적 관리 권한을 유지하고자 하는 기업들을 끌어들이고 있습니다. 매니지드 워드프레스 플랜은 캐시 기능과 스테이징 환경을 번들로 제공하여 대행사가 인프라가 아닌 콘텐츠에 집중할 수 있도록 지원합니다.

2024년에서 2025년 사이, 공급자들이 cPanel 기반 플랜을 폐지하고 Kubernetes로 오케스트레이션된 스택을 우선시하게 되면서 클라우드 전환이 가속화되었습니다. 멀티 클라우드가 주류가 되면서 기업의 78%가 최소 2개 이상의 벤더에 걸쳐 워크로드를 실행하고 있으며, 이는 전략적으로 락인(lock-in)을 피하려는 태도를 반영하고 있습니다. 관리형 워드프레스 제공업체들은 현재 헤드리스 CMS 기능을 추가하여 클라이언트가 정적 자산을 엣지 네트워크로 푸시하여 페이지 로딩 시간을 단축하고, 웹 호스팅 시장의 도달 범위를 최신의 잼스택 워크플로우로 확장하고 있습니다.

2025년 지출 중 퍼블릭 클라우드는 여전히 45.58%를 차지했지만, 컴플라이언스 요구사항이 워크로드 분산화를 촉진함에 따라 하이브리드 및 멀티 클라우드 환경은 2031년까지 연평균 10.75%의 성장률을 나타낼 것으로 전망됩니다. 이러한 변화로 인해 엄격한 데이터 위치법이 시행되고 있는 지역에서 하이브리드 솔루션의 웹호스팅 시장 점유율이 확대될 것입니다. 물리적 분리가 의무화된 곳에서는 프라이빗 클라우드가 여전히 중요하지만, 호스팅형 프라이빗 서비스로 인해 전용 환경과 멀티테넌트 환경의 경계가 모호해지고 있습니다.

하이브리드 환경을 관리하기 위해서는 ID 동기화, 데이터베이스 복제, 일관된 태깅이 필요합니다. Kubernetes는 이식성을 제공하는 반면, FinOps 팀은 상시 가동 워크로드를 변경 없이 마이그레이션할 때 발생하는 비용 증가를 최적화합니다. 인텔 SGX, AMD SEV, ARM 트러스트존(TrustZone) 등 기밀 컴퓨팅의 등장으로 기밀 데이터가 처리되는 동안에도 암호화된 상태로 유지되는 하이브리드 배포가 가능해짐에 따라, 개인 식별 정보(PII)를 다루는 워크로드를 On-Premise에 배치해야만 했던 규제 우려를 해결할 수 있게 되었습니다. 규제에 대한 우려를 해소할 수 있습니다.

지역별 분석

북미는 고밀도 하이퍼스케일 데이터센터 클러스터와 기업들의 클라우드 조기 도입에 힘입어 2025년 매출의 38.63%를 차지했습니다. 이 지역은 포화상태에 가까워지면서 성장이 둔화되고 있지만, 소버린 클라우드의 변형과 AI 전용 GPU 팜이 투자를 뒷받침하고 있습니다. 남미의 호스팅 수요는 브라질과 아르헨티나에 집중되어 있으며, 인플레이션 변동과 환율 하락으로 인해 공급자는 계약 통화를 달러로 설정하고 환율 변동에 따라 매월 조정되는 동적 가격 책정을 도입할 수밖에 없습니다.

아시아태평양은 2024년 UPI 거래 건수가 1,000억 건을 돌파한 인도의 디지털 결제 확산에 힘입어 CAGR 10.93%를 나타냈습니다. 인도네시아나 베트남의 핀테크 기업들은 국내 규정을 준수하기 위해 자카르타나 호치민시에 저지연 노드를 배치하고 있습니다. 텔레하우스(Telehouse)와 같은 공급자의 엣지 구축으로 2024년까지 15개의 데이터센터가 추가되어 주요 도시 지역의 왕복 지연 시간이 180밀리초에서 50밀리초 미만으로 단축될 것으로 예측됩니다.

유럽에서는 GDPR(EU 개인정보보호규정)의 세부적인 요구사항과 규모의 필요성이 균형을 이루고 있습니다. OVHcloud, Hetzner 등 지역 기업들이 역내 데이터 스토리지를 추진하는 가운데, AWS는 2024년 독립적인 'European Sovereign Cloud'로 이에 대응했습니다. 중동 및 아프리카는 신흥 시장으로, 모바일 우선의 인터넷 보급(UAE와 사우디아라비아의 스마트폰 보급률이 80% 이상)이 고지연 및 불안정한 셀룰러 네트워크에 최적화된 호스팅에 대한 수요를 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Web Hosting market size was valued at USD 180.35 billion in 2025 and estimated to grow from USD 182.28 billion in 2026 to reach USD 300.21 billion by 2031, at a CAGR of 10.49% during the forecast period (2026-2031). Ongoing adoption of generative AI workloads is steering enterprises toward GPU-ready edge infrastructure that legacy shared servers cannot support. Data-residency rules in the European Union, India, and China are accelerating hybrid deployments as firms distribute applications across on-premise, sovereign, and hyperscale clouds. Small merchants launching digital storefronts on no-code platforms are demanding 99.99% uptime, which is shifting spend toward cloud and managed WordPress tiers. Providers now compete on bundled observability tools and carbon-neutral credentials because basic uptime promises have become table stakes.

Global Web Hosting Market Trends and Insights

Explosive E-Commerce Expansion Among SMEs

No-code commerce platforms counted 4.6 million global merchants in late 2024, forcing providers to deliver elastic infrastructure that can absorb flash-sale traffic. Micro-retailers now expect bundles with PCI-DSS scans and integrated payment gateways, so value is shifting from raw server capacity to turnkey storefront enablement. Providers that embed hosting inside end-to-end commerce suites gain share among merchants lacking DevOps staff. Cross-border shopping in Southeast Asia requires edge points of presence to keep latency under 100 milliseconds, encouraging regional data-center rollouts. Monthly subscription contracts improve agility for retailers but raise churn risk for hosts, prompting investment in predictive-retention tooling.

Surging Demand for High-Availability and Low-Latency Sites

Financial regulators now classify digital-channel uptime as a compliance metric; European Banking Authority rules mandate 99.95% availability for banks. Video streaming, real-time gaming and tele-medicine rely on edge caching within 50 kilometers of users, which only hyperscalers and mature CDN operators can supply at scale. The rise of serverless computing has normalized globally distributed execution, removing the bottleneck of single-region origin servers. Latency-sensitive workloads tied to autonomous vehicles and industrial IoT require 5G-integrated edge hosting, a gap that traditional shared hosts struggle to bridge. Observability dashboards exposing latency and error rates in real time have become differentiators more than basic uptime guarantees.

Acute Shortage of Cloud-Certified Hosting Engineers

LinkedIn reported demand for cloud architecture skills outpacing supply by 2.3 times in 2025. Median salaries above USD 150,000 tempt engineers to move from hosting vendors to fintechs and SaaS unicorns. Under-staffed teams delay automation projects that customers expect, while multi-month reskilling programs carry uncertain returns. Remote work narrows traditional wage arbitrage, and credentials alone no longer guarantee competence, lengthening hiring cycles.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Migration to Hybrid and Multi-Cloud Architectures

- Carbon-Neutral Green Hosting Differentiation

- Escalating Cyber-Attacks and Data-Sovereignty Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shared hosting controlled 37.28% revenue in 2025 yet the segment is losing ground as even entry-level users migrate to cloud platforms offering auto-scaling and stronger security. Cloud hosting is forecast to grow at 10.53% and is expected to command a sizeable share of the Web Hosting market size by 2031. VPS and dedicated hosting hold niche positions among developers wanting root access and regulated industries needing single-tenant hardware. Colocation attracts firms retaining physical control while outsourcing facilities operations. Managed WordPress tiers bundle caching and staging, enabling agencies to focus on content rather than infrastructure.

The shift toward cloud accelerated in 2024-2025 as providers deprecated cPanel-based plans in favor of Kubernetes-orchestrated stacks. Multi-cloud became mainstream with 78% of enterprises running workloads across at least two vendors, reflecting strategic avoidance of lock-in. Managed WordPress players now add headless CMS features so clients can push static assets to edge networks, shrinking page-load times and extending the Web Hosting market reach into modern Jamstack workflows.

Public cloud still accounts for 45.58% of 2025 spend; however, hybrid and multi-cloud environments are projected to grow at a 10.75% CAGR through 2031 as compliance requirements drive workload distribution. This shift will increase the Web Hosting market share of hybrid solutions in regions that enforce strict data-location laws. Private cloud remains relevant where physical isolation is mandated, though hosted private services blur the line between dedicated and multitenant.

Managing hybrid estates demands synchronized identity, replicated databases, and consistent tagging. Kubernetes delivers portability, while FinOps teams optimize cost spikes that occur when always-on workloads migrate unmodified. The rise of confidential computing-Intel SGX, AMD SEV, ARM TrustZone-enables hybrid deployments where sensitive data remains encrypted even during processing, addressing regulatory concerns that previously forced on-premise deployment of workloads handling personally identifiable information.

The Web Hosting Market is Segmented by Hosting Type (Shared Hosting, Virtual Private Server Hosting, and More), Deployment Mode (Public Cloud, Private Cloud, and More), End-User Vertical (Large Enterprises, Small and Medium-Sized Enterprises, and More), Application (Public Websites, and More), Pricing Model (Subscription, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.63% of 2025 revenue, supported by dense hyperscale data-center clusters and early enterprise cloud adoption. Growth is moderating as the region approaches saturation, yet sovereign-cloud variants and AI-specific GPU farms sustain investment. outh America's hosting demand concentrates in Brazil and Argentina, where inflation volatility and currency devaluation force providers to denominate contracts in U.S. dollars and implement dynamic pricing that adjusts monthly based on exchange-rate fluctuations.

Asia-Pacific is projected to expand at a 10.93% CAGR, underpinned by the proliferation of digital payments in India, where UPI volumes crossed 100 billion transactions in 2024. Indonesian and Vietnamese fintechs deploy low-latency nodes in Jakarta and Ho Chi Minh City to comply with national regulations. Edge expansions by providers such as Telehouse added 15 data centers in 2024, cutting round-trip latency from 180 milliseconds to under 50 milliseconds in key metros.

Europe balances GDPR nuances with the need for scale. Regional companies such as OVHcloud and Hetzner promote in-region data storage, while AWS responded in 2024 with an isolated European Sovereign Cloud. Middle East and Africa represent nascent markets where mobile-first internet adoption-smartphone penetration exceeds 80% in UAE and Saudi Arabia-drives demand for hosting optimized for cellular networks with high latency and intermittent connectivity.

List of Companies Covered in this Report:

- Amazon Web Services

- Google LLC

- Microsoft Corporation

- GoDaddy Inc.

- Newfold Digital

- Alibaba Cloud

- Tencent Cloud

- Liquid Web LLC

- DigitalOcean

- OVH Groupe SA

- Hetzner Online GmbH

- WP Engine

- 1and1 IONOS

- Hostinger International Ltd.

- SiteGround Hosting Ltd.

- A2 Hosting LLC

- Kinsta Inc.

- DreamHost LLC

- GreenGeeks LLC

- InMotion Hosting Inc.

- The Constant Company LLC

- Namecheap Inc.

- HostGator LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Explosive E-Commerce Expansion Among SMEs

- 4.1.2 Surging Demand For High-Availability and Low-Latency Sites

- 4.1.3 Rapid Migration To Hybrid/Multi-Cloud Architectures

- 4.1.4 Carbon-Neutral Green Hosting Differentiation

- 4.1.5 Gen-AI-Ready Edge and GPU Server Demand Surge

- 4.2 Market Restraints

- 4.2.1 Acute Shortage of Cloud-Certified Hosting Engineers

- 4.2.2 Escalating Cyber-Attacks and Data-Sovereignty Regulation

- 4.2.3 Margin Pressure From Race-To-Zero Pricing

- 4.2.4 Energy-Price Volatility And Power-CAPEX Inflation

- 4.3 Value Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Sustainability Positioning and Green Hosting Initiatives

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hosting Type

- 5.1.1 Shared Hosting

- 5.1.2 Virtual Private Server (VPS) Hosting

- 5.1.3 Dedicated Hosting

- 5.1.4 Cloud Hosting

- 5.1.5 Colocation Hosting

- 5.1.6 Managed WordPress Hosting

- 5.1.7 Reseller Hosting

- 5.1.8 Other Hosting Types

- 5.2 By Deployment Mode

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid/Multi-Cloud

- 5.3 By End-user Vertical

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SMEs)

- 5.3.3 Individual Bloggers/Creators

- 5.3.4 Software Developers and SaaS Start-ups

- 5.4 By Application

- 5.4.1 Public Websites

- 5.4.2 E-commerce Stores

- 5.4.3 Web Applications

- 5.4.4 Mobile Applications and APIs

- 5.4.5 SaaS/PaaS Platforms

- 5.4.6 Other Applications

- 5.5 By Pricing Model

- 5.5.1 Subscription (Fixed-Term)

- 5.5.2 Metered/Pay-as-you-go

- 5.5.3 Tiered (Usage-Bracket)

- 5.5.4 Freemium and Ad-Supported

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 GoDaddy Inc.

- 6.4.5 Newfold Digital

- 6.4.6 Alibaba Cloud

- 6.4.7 Tencent Cloud

- 6.4.8 Liquid Web LLC

- 6.4.9 DigitalOcean

- 6.4.10 OVH Groupe SA

- 6.4.11 Hetzner Online GmbH

- 6.4.12 WP Engine

- 6.4.13 1and1 IONOS

- 6.4.14 Hostinger International Ltd.

- 6.4.15 SiteGround Hosting Ltd.

- 6.4.16 A2 Hosting LLC

- 6.4.17 Kinsta Inc.

- 6.4.18 DreamHost LLC

- 6.4.19 GreenGeeks LLC

- 6.4.20 InMotion Hosting Inc.

- 6.4.21 The Constant Company LLC

- 6.4.22 Namecheap Inc.

- 6.4.23 HostGator LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment