|

시장보고서

상품코드

2044089

아날로그 반도체 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Analog Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

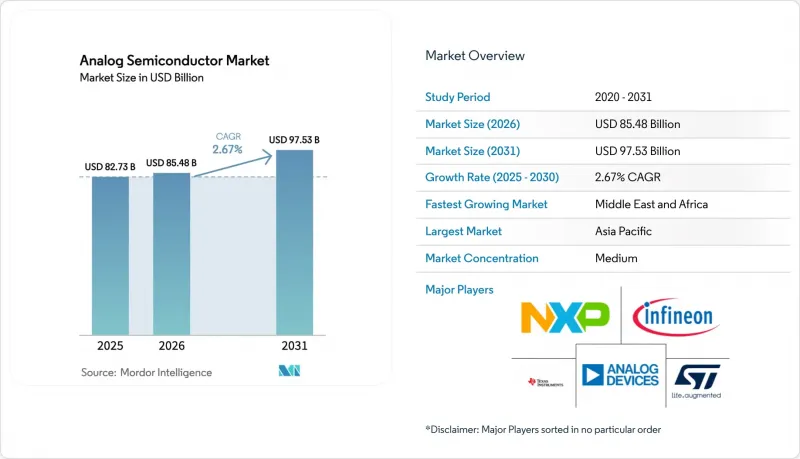

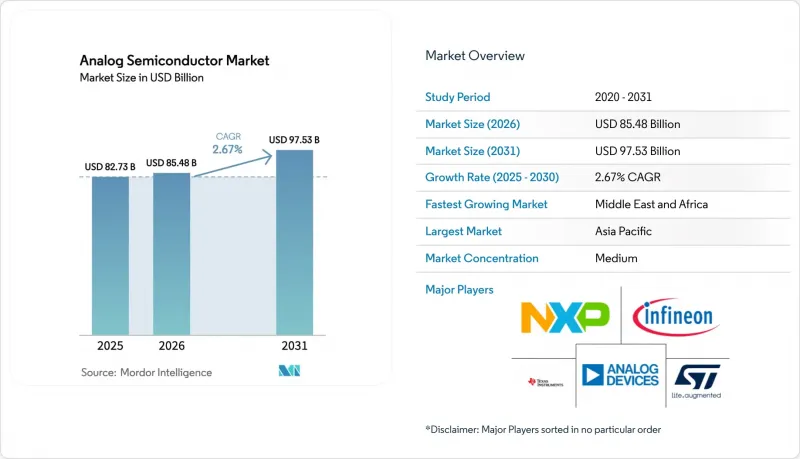

아날로그 반도체 시장 규모는 2026년 854억 8,000만 달러에서 2031년까지 975억 3,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR 2.67%를 나타낼 것으로 예측됩니다.

출하량은 2026년 2,447억 3,000만 개에서 2031년 3,428억 8,000만 개로 증가하여 CAGR 6.98%를 나타낼 것으로 예측됩니다. 범용 제품 카테고리의 가격 압박이 지속되는 가운데, 물량 성장과 매출 성장의 격차는 더욱 확대될 것입니다. 2025년, 특정 용도용 아날로그 IC가 여전히 큰 매출 기준을 유지했지만, 엣지 컴퓨팅 및 공장 자동화 하드웨어의 표준화가 진행됨에 따라 많은 신규 설계가 범용 부품으로 전환되고 있으며, 카탈로그 제품 포트폴리오 전체적으로 경쟁 환경이 심화되고 있습니다. 아시아태평양의 제조업체들은 질화갈륨(GaN)을 이용한 급속 충전 생태계에 힘입어 전 세계 수요의 거의 절반을 차지하고 있습니다. 한편, 중동의 방산 관련 프로젝트는 내방사선 프론트엔드에 대한 좋은 비즈니스 기회를 창출하고 있습니다. 동시에 텍사스와 드레스덴의 300mm 팹 증설은 수년간의 웨이퍼 공급 병목현상을 해소하기 위한 것이지만, 외부 파운드리에 의존하는 팹리스 기업에게는 단기적인 공급 확보에 대한 리스크가 남아있습니다.

세계의 아날로그 반도체 시장 동향과 인사이트

아시아 스마트폰 생태계에서 급속 충전 어댑터의 보급 확대

아시아 휴대폰 제조업체는 2025년에 USB-PD 3.1 및 자체 65W-240W 고속 충전 프로토콜을 표준화했습니다. 이러한 전환에 따라 더 높은 스위칭 주파수와 낮은 발열을 가진 질화갈륨(GaN) 전력 관리 IC가 필요하게 되었습니다. Navitas는 이러한 어댑터용으로 1억 개 이상의 GaN 디바이스를 출하했으며, Renesas는 USB-C 컨트롤러와 GaN 게이트 드라이버를 통합하여 외부 부품을 5분의 1로 줄였습니다. 현지 Tier 2 OEM 업체들은 부품 비용 절감을 빠르게 수용하고 설계 주기를 단축하여 아날로그 반도체 시장에서 아시아태평양의 우위를 더욱 공고히 하고 있습니다.

북미의 산업용 IoT 확산으로 고정밀 데이터 컨버터에 대한 수요가 증가할 것

2025년 미국 공장에는 1,500만 개 이상의 IoT 센서 노드가 도입되었으며, 각 노드는 마이크로볼트 수준의 노이즈 플로어를 가진 16비트 이상의 ADC를 필요로 했습니다. 아날로그 디바이스의 멀티센서 프런트엔드는 개별 부품 수를 40% 줄였고, 텍사스 기기는 진동 분석을 위해 40kHz 샘플링을 지원하는 델타 시그마 트랜스듀서를 제공했습니다. 이에 따른 수요 증가는 카탈로그 제품 판매를 증가시켜 아날로그 반도체 시장에서 고정밀 컨버터를 프리미엄 가격대로 유지하고 있습니다.

PMIC 공급을 제한하는 300mm 팹 생산 능력의 병목 현상

텍사스 기기와 세계 파운드리가 새로운 생산 라인을 추가했지만, TSMC는 여전히 300mm 제조 장비의 대부분을 첨단 로직에 할당하고 있으며, 레거시 노드의 아날로그 생산은 여전히 수요 초과 상태입니다. 2025년 하반기에는 리드타임이 20주를 넘어섰고, IC 제조업체들이 웨이퍼를 자체 수요로 돌리면서 자동차용 프로그램에서는 심각한 공급 부족이 발생했습니다. 이러한 생산능력의 압박은 대량 생산되는 전력관리 IC의 생산을 계속 억제하고 있으며, 아날로그 반도체 시장의 단기적인 성장을 둔화시키고 있습니다.

부문 분석

범용 IC는 2025년 매출에서 차지하는 비중은 미미했지만, 산업 자동화를 지배하는 모듈형 하드웨어 플랫폼과의 적합성을 반영하여 CAGR 6.52%로 성장을 견인할 것으로 예측됩니다. OEM 업체들이 개발 일정을 몇 개월 단축하기 위해 기성품 부품을 채택함에 따라 이러한 카탈로그 제품인 증폭기 및 비교기 관련 아날로그 반도체 시장 규모는 확대될 것입니다.

특정 용도 설계는 2025년에도 매출의 45.71%를 차지했으며, 맞춤형 ASIC 프로젝트에는 더 긴 검증 기간이 필요하기 때문에 성장세가 둔화될 것으로 예측됩니다. 자동차 배터리 관리 ASIC 및 5G RF 프론트엔드는 대량 생산 부문에서 맞춤형 아날로그 부품이 여전히 중요하다는 것을 보여주지만, 구성 가능한 카탈로그 제품의 성능이 향상됨에 따라 아날로그 반도체 시장에서의 점유율은 점차 정상화될 것입니다. 온세미컨덕터의 Treo 플랫폼은 실리콘 카바이드(SiC) 트랙션 인버터를 위한 절연 게이트 드라이버와 전류 감지 기능을 통합한 산업용 ASIC로 혹독한 환경에 대응합니다.

연산 증폭기는 의료 및 산업용 엔드포인트의 고정밀 센싱이 견인차 역할을 하면서 CAGR 5.83%를 나타낼 것으로 예측됩니다. 마이크로볼트 수준의 오프셋 전압을 가진 프리미엄 증폭기는 더 높은 평균 판매 가격을 유지하고 있으며, 신호 조정 장치에서 아날로그 반도체 시장 규모 내에서 가치 기여도를 유지하고 있습니다. Analog Devices의 AD7380은 전압 레퍼런스가 내장된 16비트 순차 비교형 ADC로, 외부 고정밀 저항이 필요 없어 인쇄 회로 기판 면적을 30% 절감할 수 있습니다.

2025년 29.83%의 점유율을 차지한 전원 관리 부품은 스마트폰 및 노트북 OEM 제조업체의 구매력이 커짐에 따라 더욱 급격한 가격 하락에 직면하고 있습니다. 한편, 고해상도 컨버터와 견고한 인터페이스 트랜시버는 전자파 적합성(EMC) 기준의 강화로 인해 웨이퍼 비용 상승에도 불구하고 수익률 안정화에 기여하고 있습니다. 다이오드와 트랜지스터는 정전기 방전(ESD) 보호 및 부하 스위칭에서 틈새 시장을 형성하고 있지만, 집적 솔루션의 점유율 확대에 따라 2025년 디스크리트 제품 출하량은 전년 대비 5% 감소할 것으로 예측됩니다.

지역별 분석

아시아태평양은 아날로그 반도체 시장의 중심을 유지하고 있으며, 2025년에는 매출의 45.72%를 차지했습니다. 중국, 일본, 한국공급망은 스마트폰, 자동차용 파워 모듈, 5G 무선기기용 대용량 아날로그 반도체를 흡수하고 있습니다. 중국의 3,440억 위안(470억 달러) 규모의 '국가 IC 기금'과 일본의 설비 세액 공제 등 정부 인센티브는 현지 생산 능력 확대를 지원하고 지역의 자립성을 강화하고 있습니다. 인도의 반도체 인센티브 프로그램은 아날로그 반도체 팹에 대한 제안을 불러일으켰지만, 규제 당국의 승인에 24개월 이상 걸렸기 때문에 생산 능력 증설은 2027년까지 지연될 것으로 예측됩니다.

중동은 국방 기관의 항공전자 및 위성 탑재체 현대화에 따라 2031년까지 연평균 7.02%의 가장 높은 성장률을 나타낼 것으로 예측됩니다. 아랍에미리트(UAE)와 사우디아라비아의 노력으로 방사선 내성 프론트엔드 전문 설계 센터에 자본이 투입되어 아날로그 반도체 시장 내 프리미엄 하위 부문을 형성하고 있습니다.

북미는 전 세계 매출의 약 4분의 1을 차지하고 있으며, CHIPS법에 따라 총 390억 달러의 보조금이 국내 웨이퍼 생산에 힘을 실어주고 있습니다. 유럽은 EU 칩스법에 따라 430억 유로(469억 달러)의 지원을 받아 약 5분의 1의 점유율로 그 뒤를 잇고 있습니다. 반면, 남미와 아프리카는 10% 미만이지만, 자동차 및 Off-grid 에너지 시스템에서 선택적 수요를 볼 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 및 수량)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The analog semiconductor market size is expected to increase from USD 85.48 billion in 2026 to USD 97.53 billion by 2031, growing at a CAGR of 2.67% over 2026-2031. Volume shipments will climb from 244.73 billion units in 2026 to 342.88 billion units by 2031, a 6.98% CAGR that widens the gap between unit and revenue growth as price pressure persists in commodity categories. Application-specific analog ICs retained a sizeable revenue base in 2025, yet rising standardization in edge-computing and factory-automation hardware is steering many new designs toward general-purpose parts, tightening competitive dynamics across catalog portfolios. Asia-Pacific manufacturers account for almost half of global demand, propelled by gallium-nitride fast-charging ecosystems, while defense-driven projects in the Middle East create premium opportunities for radiation-hardened front-ends. Simultaneously, 300 mm fab ramps in Texas and Dresden aim to relieve long-standing wafer bottlenecks, but near-term allocation risk remains for fabless suppliers that depend on external foundries.

Global Analog Semiconductor Market Trends and Insights

Proliferation Of Fast-Charging Power Adapters In Asian Smartphone Ecosystems

Asian handset makers standardized USB-PD 3.1 and proprietary 65 W-240 W fast-charge protocols in 2025, a shift that required gallium-nitride power management ICs with higher switching frequencies and reduced thermal budgets. Navitas shipped more than 100 million GaN devices into these adapters, while Renesas integrated USB-C controllers and GaN gate drivers to cut external components by one-fifth. Local tier-two OEMs quickly embraced the lower bill-of-materials cost, accelerating design cycles and reinforcing Asia-Pacific's dominance within the analog semiconductor market.

Industrial IoT Adoption Elevating Demand For High-Precision Data Converters In North America

Factories across the United States deployed over 15 million IoT sensor nodes in 2025, each calling for 16-bit-plus ADCs with microvolt-level noise floors. Analog Devices' multisensor front-ends trimmed discrete counts by 40%, and Texas Instruments delivered delta-sigma converters supporting 40 kHz sampling for vibration analytics. The resulting demand uplift bolsters catalog revenues and keeps high-accuracy converters at premium price points within the analog semiconductor market.

300 mm Fab Capacity Bottlenecks Limiting PMIC Supply

Texas Instruments and GlobalFoundries added new lines, yet TSMC still allocates most 300 mm tools to advanced logic, leaving analog runs on legacy nodes oversubscribed. Lead times stretched beyond 20 weeks in late 2025 and automotive programs felt acute shortages as integrated device manufacturers diverted wafers to in-house needs. The tight capacity continues to restrain output of high-volume power-management ICs, tempering near-term expansion in the analog semiconductor market.

Other drivers and restraints analyzed in the detailed report include:

- Roll-Out Of 5G Infrastructure Amplifying RF Analog IC Demand In East Asia

- AI-Accelerated Edge Devices Requiring Ultra-Low-Power Data-Acquisition ICs

- Volatility In Analog Wafer-Foundry Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General-purpose ICs accounted for modest revenue in 2025 yet are projected to lead growth at a 6.52% CAGR, reflecting their fit with modular hardware platforms that dominate industrial automation. The analog semiconductor market size tied to these catalog amplifiers and comparators will expand as OEMs adopt off-the-shelf parts to shave months from development schedules.

Application-specific designs, while still responsible for 45.71% revenue in 2025, face slower gains as custom ASIC projects require longer validation windows. Automotive battery-management ASICs and 5G RF front-ends illustrate how high-volume sectors will keep bespoke analog relevant, but their share of the analog semiconductor market will gradually normalize as configurable catalog alternatives improve performance envelopes. Industrial ASICs address harsh environments, with onsemi's Treo platform integrating isolated gate drivers and current sensing for silicon carbide traction inverters

Operational amplifiers are forecast to post a 5.83% CAGR, driven by precision sensing in medical and industrial endpoints. Premium amplifiers with microvolt offset voltages sustain higher average selling prices, preserving value contribution within the analog semiconductor market size for signal-conditioning devices. Analog Devices' AD7380, a 16-bit successive-approximation ADC with integrated voltage reference, eliminates external precision resistors and reduces printed circuit board area by 30%.

Power-management parts, holding 29.83% share in 2025, confront steeper price erosion because smartphone and notebook OEMs wield greater purchasing leverage. Conversely, high-resolution converters and rugged interface transceivers benefit from tighter electromagnetic-compatibility standards, helping stabilize margins despite rising wafer costs. Diodes and transistors serve niche roles in electrostatic discharge protection and load switching, yet discrete shipments declined 5% year-over-year in 2025 as integrated solutions gained share.

The Analog Semiconductor Market Report is Segmented by Device Type (General Purpose Analog IC and Application-Specific Analog IC), Component (Resistors, Capacitors, Inductors, and More), Wafer Size (200mm, 300mm, and More), End-User Industry (Consumer Electronics, IT and Telecom, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific remains the center of gravity for the analog semiconductor market, accounting for 45.72% of revenue in 2025. Supply ecosystems in China, Japan, and South Korea absorb high-volume analog for smartphones, automotive power modules, and 5G radios. Government incentives such as China's CNY 344 billion (USD 47 billion) National IC Fund and Japan's equipment tax credits underpin local capacity expansions, reinforcing regional self-reliance. India's semiconductor incentive program attracted proposals for analog fabs, yet regulatory approvals extended beyond 24 months, delaying capacity additions until 2027.

The Middle East is projected to chart the fastest CAGR of 7.02% through 2031 as defense agencies modernize avionics and satellite payloads. United Arab Emirates and Saudi Arabia initiatives funnel capital into design centers that specialize in radiation-tolerant front-ends, carving out a premium sub-segment within the analog semiconductor market.

North America accounts for roughly one-quarter of global revenue, with CHIPS Act grants totaling USD 39 billion catalyzing domestic wafer production. Europe follows at nearly one-fifth share, supported by the EUR 43 billion (USD 46.9 billion) EU Chips Act, while South America and Africa collectively represent less than 10% yet display selective uptake in automotive and off-grid energy systems.

List of Companies Covered in this Report:

- Texas Instruments Inc.

- Analog Devices Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- onsemi

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Rohm Co., Ltd.

- Skyworks Solutions Inc.

- Cirrus Logic Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems Inc.

- Diodes Incorporated

- Vicor Corp.

- Power Integrations Inc.

- Semtech Corp.

- Qorvo Inc.

- Allegro MicroSystems Inc.

- Vishay Intertechnology Inc.

- Maxim Integrated Products Inc.

- Richtek Technology Corp.

- Broadcom Inc.

- Tower Semiconductor Ltd.

- AnalogicTech Corp.

- Nordic Semiconductor ASA (Analog Front-End ICs)

- Alpha & Omega Semiconductor Ltd.

- Silergy Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Surge in 48 V Mild-Hybrid Vehicles Across Europe

- 4.2.2 Proliferation of Fast-Charging Power Adapters in Asian Smartphone Ecosystems

- 4.2.3 Industrial IoT Adoption Elevating Demand for High-Precision Data Converters in North America

- 4.2.4 Roll-Out of 5 G Infrastructure Amplifying RF Analog IC Demand in East Asia

- 4.2.5 Escalating Defense Modernization Driving Radiation-Hardened Analog Procurement in the Middle East

- 4.2.6 AI-Accelerated Edge Devices Requiring Ultra-Low-Power Data-Acquisition ICs

- 4.3 Market Restraints

- 4.3.1 300 mm Fab Capacity Bottlenecks Limiting PMIC Supply

- 4.3.2 Volatility in Analog Wafer-Foundry Pricing

- 4.3.3 Design-In Cycles Stretching Time-to-Revenue for Niche Automotive ASICs

- 4.3.4 Counterfeit Passive Components Undermining Reliability in South-East Asia

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Device Type (Value and Volume)

- 5.1.1 General Purpose Analog IC

- 5.1.1.1 Amplifiers and Comparators

- 5.1.1.2 Interface

- 5.1.1.3 Power Management

- 5.1.1.4 Signal Conversion

- 5.1.2 Application-Specific Analog IC

- 5.1.2.1 Automotive

- 5.1.2.2 Communications

- 5.1.2.3 Computer

- 5.1.2.4 Consumer

- 5.1.2.5 Industrial

- 5.1.1 General Purpose Analog IC

- 5.2 By Component (Value)

- 5.2.1 Resistors

- 5.2.2 Capacitors

- 5.2.3 Inductors

- 5.2.4 Diodes

- 5.2.5 Transistors

- 5.2.6 Operational Amplifiers

- 5.3 By Wafer Size (Value)

- 5.3.1 200 mm

- 5.3.2 300 mm

- 5.3.3 Other Sizes

- 5.4 By End-User Industry (Value)

- 5.4.1 Consumer Electronics

- 5.4.2 IT and Telecom

- 5.4.3 Automotive and Transportation

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Healthcare Devices

- 5.4.6 Aerospace and Defense

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Analog Devices Inc.

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 Infineon Technologies AG

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 onsemi

- 6.4.7 Renesas Electronics Corp.

- 6.4.8 Microchip Technology Inc.

- 6.4.9 Rohm Co., Ltd.

- 6.4.10 Skyworks Solutions Inc.

- 6.4.11 Cirrus Logic Inc.

- 6.4.12 Silicon Laboratories Inc.

- 6.4.13 Monolithic Power Systems Inc.

- 6.4.14 Diodes Incorporated

- 6.4.15 Vicor Corp.

- 6.4.16 Power Integrations Inc.

- 6.4.17 Semtech Corp.

- 6.4.18 Qorvo Inc.

- 6.4.19 Allegro MicroSystems Inc.

- 6.4.20 Vishay Intertechnology Inc.

- 6.4.21 Maxim Integrated Products Inc.

- 6.4.22 Richtek Technology Corp.

- 6.4.23 Broadcom Inc.

- 6.4.24 Tower Semiconductor Ltd.

- 6.4.25 AnalogicTech Corp.

- 6.4.26 Nordic Semiconductor ASA (Analog Front-End ICs)

- 6.4.27 Alpha & Omega Semiconductor Ltd.

- 6.4.28 Silergy Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment