|

시장보고서

상품코드

2044107

로터리 펌프 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Rotary Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

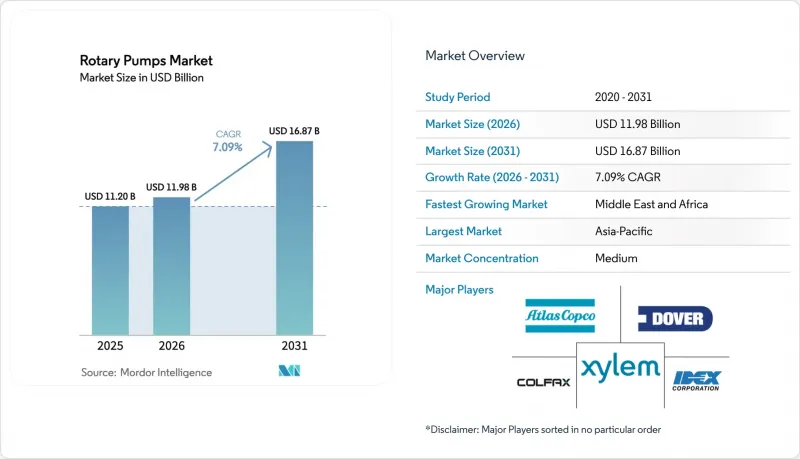

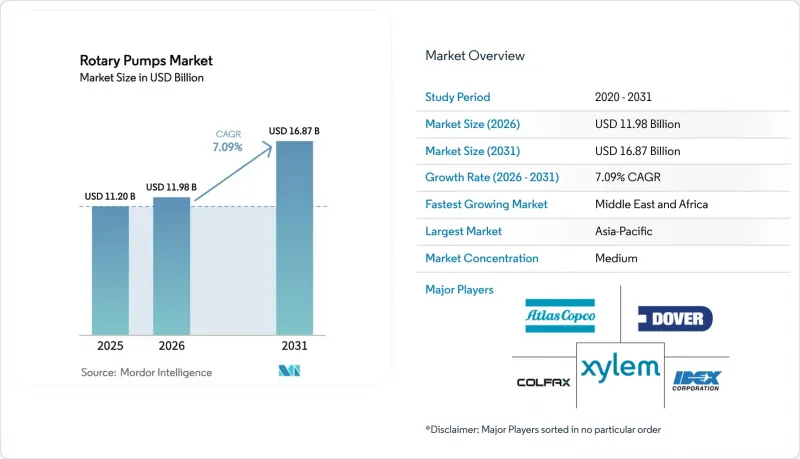

로터리 펌프 시장 규모는 2025년 112억 달러, 2026년 119억 8,000만 달러에서 2031년까지 168억 7,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 CAGR 7.09%를 기록할 전망입니다.

정유공장이 고점도 서비스 라인을 개조하고, 아시아 석유화학 콤비네이션이 API-676을 준수하는 기어 펌프와 스크류 펌프를 도입하고, 북미 식품 가공업체가 점점 더 엄격해지는 위생 기준을 충족하기 위해 기존 위생 원심 펌프를 교체하는 등 구조적 수요가 증가하고 있습니다. 구조적 수요가 증가하고 있습니다. 해양 사업자들은 맥동으로 인한 피로를 피하기 위해 심해 FPSO에서 트윈 스크류 유닛의 표준화를 추진하고 있습니다. 한편, 미국 지자체는 '인프라 투자 및 고용법'의 보조금을 활용하여 슬러지, 소화조 및 유입수 처리를 위해 로터리 로브 펌프와 프로그레시브 캐비티 펌프를 지정하고 있습니다. 진동, 온도, 씰 상태 데이터를 모니터링하는 디지털 트윈 플랫폼의 채택 확대로 일회성 예비 부품 판매에서 장기적인 모니터링 계약으로 전환되고 있으며, 이는 대규모 도입 실적을 보유한 기존 제조업체에 우위를 가져다주고 있습니다. 유럽의 위조 애프터마켓 부품 및 휘발성 유기 화합물(VOC) 규제 강화로 인해 총소유비용(TCO) 계산이 복잡해졌지만, API-676 인증 및 센서의 신뢰성 확보는 여전히 각 최종 시장에서 결정적인 구매 기준이 되고 있습니다.

세계 로터리 펌프 시장 동향 및 인사이트

에너지 부문의 브라운필드 개보수, 고점도 유체 처리 수요를 견인합니다.

북미와 중동의 정유사들은 그린필드 프로젝트에서 중질유 블렌드 및 재생 가능 원료에 대응해야 하는 병목현상 해소 프로그램으로 자본을 전환하고 있으며, 이에 따라 5,000 cP 이상의 점도에 대응하는 인증된 외기어 펌프 및 원심 펌프를 5,000 cP 이상의 점도에 대응하는 인증된 외기어 펌프와 트윈 스크류 펌프로 대대적인 교체가 진행되고 있습니다. 에퀴노르(Equinor)의 몬스타드 정유시설의 10억 달러 규모의 현대화 프로젝트에는 전동식 로터리 펌프가 도입되었으며, 이를 통해 Scope 2 배출량을 30% 줄일 수 있을 것으로 예측됩니다. 석유 및 가스 기후 이니셔티브(OGCI)는 회원사들이 2028년까지 2,500대의 추가 로터리 유닛을 필요로할 것으로 예상하고 있으며, 이는 다년간 수요 전망을 확고히 하고 있습니다. API-676 표준의 엄격한 밀봉, 진동, 케이싱에 대한 제한으로 인해 인증된 공급업체의 수가 제한되어 있으며, 표준을 준수하는 공급업체는 프리미엄 가격을 확보할 수 있습니다. 이러한 요인들이 복합적으로 작용하여 전체 정유시설 건설이 둔화되더라도 고점도 펌프의 브라운필드(기존 설비)의 갱신 수요는 계속 확대될 것으로 보입니다.

중국 및 인도의 석유화학 플랜트 증설로 인해 API-676을 준수하는 로터리 펌프가 필요합니다.

2025년에 일일 1,481만 배럴의 기록적인 처리 능력을 달성한 중국에서는 연간 4,000만 톤을 생산하는 Rongsheng의 절강 콤플렉스에 힘입어 장기 주문이 고압 기어 펌프와 스크류 펌프로 꾸준히 이동하고 있습니다. 여기에는 수입 의존도를 낮추기 위해 현지에서 설계한 70MPa 등급의 제품도 포함되어 있습니다. 인도에서는 2030년까지 150만 배럴/일 규모의 정유공장 확장 계획이 진행 중이며, 이에 따라 릴라이언스와 인도석유공사는 폴리머 등급프로파일렌 및 부타디엔 이송 작업을 위해 트윈 스크류 펌프 공급업체를 사전 인증했습니다. 국제에너지기구(IEA)는 2030년까지 석유화학 원료 수요가 연간 6.2% 증가할 것으로 전망하고 있으며, 이로 인해 수지 및 엘라스토머 플랜트 전체에서 API-676 표준 장비에 대한 수요가 더욱 증가할 것으로 예상하고 있습니다. 엔지니어링, 조달, 건설(EPC) 계약업체들은 보다 엄격한 환경 규제를 충족하기 위해 누출 감지 포트가 있는 이중 압력 밀봉을 의무화하고 있으며, 이는 공급업체들의 차별화를 촉진하고 있습니다. 그 결과, 예측 기간 동안 아시아의 석유화학 메가 프로젝트는 규제 준수 로터리 펌프의 가장 큰 수주처가 될 것입니다.

아시아 비공식 공급업체에 의한 저가의 위조 부품의 유통

유럽연합 지적재산권청(EUIPO)에 따르면, 위조 로터, 씰, 베어링이 EU 국경에서 압수되는 산업 부품의 12%를 차지하고 있으며, 그 대부분은 중국과 인도에서 생산된 것으로 나타났습니다. 비규격 엘라스토머는 고온 환경이나 화학적으로 가혹한 환경에서 빠르게 열화되기 때문에 조기 누출 및 고가의 다운타임을 초래할 수 있습니다. 전자상거래 플랫폼은 인증되지 않은 부품을 쉽게 구할 수 있어 엄격한 벤더 인증 프로토콜이 없는 유지보수 팀을 압도하고 있습니다. 유압협회(Hydraulic Institute)는 QR 코드 및 블록체인 인증 프레임워크를 도입했지만, 북미 이외 지역에서의 채택은 여전히 제한적이며, 회색 시장 유통 경로가 여전히 존재하고 있습니다. 공장 운영자가 균일한 검증 시스템을 도입하기 전까지는 위조 예비 부품이 정품 애프터마켓의 수익률을 계속 잠식하고 OEM의 브랜드 가치를 계속 훼손할 것입니다.

부문 분석

2025년 기준, 외기어 펌프는 시장 점유율의 32.47%를 차지했습니다. 이는 단순하고 견고한 구조가 업스트림 유전의 모래가 섞인 원유와 높은 흡입 양정을 견딜 수 있기 때문입니다. 2031년까지 8.43% 성장할 것으로 예상되는 트윈 스크류 모델이 FPSO 상부 및 폴리머 반응기에서 흔히 발생하는 맥동 및 가스 혼입 문제를 해결함에 따라 외기어 펌프의 점유율은 감소할 것으로 예측됩니다. Seatrium의 P-84 및 P-85 FPSO 계약과 NETZSCH의 1,400 m3/h XXLB-F의 출시는 운영자와 공급업체들이 메가 프로젝트를 위해 트윈 스크류 기술을 확장하고 있으며, 이는 차별화된 성능의 솔루션으로 전환하고 있음을 보여줍니다. 성능으로 차별화된 솔루션으로의 전환을 촉진하고 있습니다. 한편, 내부 기어 펌프는 낮은 전단이 필수적인 음료, 초콜릿, 퍼스널케어용 유체 등 위생적인 틈새 시장에서 입지를 다지고 있습니다. 반면, 베인 펌프와 3축 스크류 펌프는 여전히 이동식 유압 장비와 고압 선박 윤활 용도에 국한되어 있습니다. Roto Pumps의 모듈식 P-Range는 성숙한 외부 기어 설계에서도 혁신이 계속되고 있음을 보여주며, 총소유비용(TCO) 지표에서 긴 씰 수명과 낮은 진동을 약속하는 스크류 기술이 점점 더 유리하게 작용하고 있습니다.

현재 고객의 사양은 API-676 준수와 디지털 대응을 요구하고 있으며, 벤더는 표준 프레임이라도 센서 포트와 공장 출하 시 진동 프로브를 내장해야 합니다. 바이오 오일, 재생 가능 디젤 등 에너지 전환용 연료가 파이프라인에 넘쳐나면서 유체의 점도 변동이 심해짐에 따라 체적 효율을 떨어뜨리지 않고 회전수를 조절할 수 있는 스크류 펌프의 가치가 높아지고 있습니다. 결과적으로, 로터리 펌프 시장의 경쟁 환경은 견고하고 디지털에 대응하는 트윈 스크류 플랫폼을 대량 생산할 수 있으면서도 외기어 펌프의 대체 사업에서 틈새 수익률을 유지할 수 있는 공급업체에게 유리하게 작용할 것입니다.

석유 및 가스 부문은 업스트림, 미드스트림, 다운스트림의 광범위한 도입으로 2025년 28.42%의 점유율을 차지했지만, 탈탄소화 목표가 화석연료에 대한 설비투자를 억제하고 있어 이 부문의 성장세는 전체 시장의 CAGR을 밑돌고 있습니다. 반면, 식품 및 음료 가공업체들은 식품안전현대화법(FSMA)의 요구사항과 EU의 '팜 투 포크(Farm to Fork)' 이니셔티브에 따라 위생 설비를 체계적으로 업데이트해야 하기 때문에 2031년까지 연평균 복합 성장률(CAGR) 9.11%로 펌프 구매를 확대할 것으로 예측됩니다. 새로운 위생 라인에 내장된 센서는 세척 주기 및 공정 온도에 대한 실용적인 데이터를 생성하여 컴플라이언스 리스크를 줄이기 때문에 이 부문의 견고한 도입 곡선을 설명합니다.

화학 및 석유화학 플랜트, 특히 폴리머 등급의 모노머를 처리하는 중국 및 인도의 복합시설에서 고압 및 고온 대응 기어펌프와 스크류 펌프에 대한 고가의 주문이 여전히 발생하고 있습니다. 상수도, 하수처리, 전력 분야는 안정적인 기반 수요를 창출하고 있으며, '인프라 투자 및 고용법'의 예산 배분으로 노후화된 미국 시설의 프로그레시브 캐비티 펌프와 로브 펌프의 교체가 잇따르고 있습니다. 광업, 펄프 및 제지 분야는 내마모성 로터리 설계에 대한 변동성이 큰 수요를 창출하고 있으며, 이로 인해 예측 기간 동안 공급업체의 수익원이 더욱 다양해져 유가 변동에 대한 민감도가 낮아질 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년 40.19%의 점유율을 차지해, 중국의 정유시설 가동률이 사상 최고치를 기록한 점과 인도의 수입 대체 정책으로 국내 API-676 공급업체에 대한 수주가 유도된 점이 호재로 작용할 것으로 보입니다. 중동 및 아프리카는 사우디 아람코의 자잔 확장 프로젝트, UAE의 루와이스 복합단지, 나이지리아의 65만 배럴/일 규모의 단고테 정유공장이 각각 고 유량, 고압의 기어식 및 스크류식 모델을 지정하면서 CAGR 9.08%를 나타낼 것으로 예측됩니다. 기록할 것으로 예측됩니다. 북미에서는 기존 시설의 수소화 처리 설비 업그레이드와 더불어 500억 달러 규모의 연방정부 물 인프라 지출을 통해 지방 자치 단체의 펌프 교체에 대한 보조금을 지원하여 안정적인 수주 파이프라인을 확보했습니다.

유럽에서는 위생 펌프의 기술 혁신과 VOC 규제에 따른 개보수 수요의 역풍이 맞물려 사업자들이 이중 실링과 실링리스 옵션의 비용을 비교 검토하는 가운데, 견조하지만 눈에 띄는 성장은 없을 것으로 예측됩니다. 남미의 성장 궤도는 브라질의 FPSO 건조 프로그램과 칠레의 구리 정광 파이프라인에 크게 의존하고 있으며, 내마모성 및 저맥동 유닛의 수주 잔고는 장기적이지만 그 규모는 제한적일 것으로 예측됩니다. 전반적으로, 지역적 분산화는 거시 경제의 변동성을 완화하고 로터리 펌프 공급업체의 균형 잡힌 세계 성장 전망을 뒷받침하고 있습니다.

아시아 선진국들도 저탄소 연료로의 전환을 추진하고 있으며, 일본에서는 유휴 정제능력의 1/3을 지속가능한 항공연료 생산으로 전환하고 있습니다. 이 전환으로 인해 이미 100bar 이상의 정격 압력을 가진 듀플렉스 스틸 트윈 스크류 펌프에 대한 새로운 입찰이 발생했습니다. 한편, 호주의 LNG 액화 사업자들은 배출 규제 강화에 대응하기 위해 수처리 모듈에 로터리 로브 펌프와 프로그레시브 캐비티 펌프를 설치하고 있으며, 퍼스나 다윈에 서비스 거점을 두고 있는 벤더에게는 애프터마켓 서비스 수익 확대의 기회로 작용하고 있습니다. 애프터마켓 서비스 수익 확대에 기여하고 있습니다. 한국에서는 혼합 플라스틱 폐기물을 처리하기 위해 울산과 여수의 화학 재활용 라인을 업그레이드하고 있으며, VOC 누출을 제거하고 산업 배출 지침에 해당하는 현지 기준을 충족하기 위해 마그네틱 커플링이 장착된 API-676 기어펌프가 지정되어 있습니다. 지정되었습니다. 마지막으로, 싱가포르 주롱섬에서는 바이오 크래커의 처리 능력을 강화하고 있으며, 점도 1,000 cP 이상의 지방산 원료를 처리할 수 있는 500 m3/h 이상의 스크류 펌프가 필요합니다. 이에 따라 동남아시아는 고성능 로터리 장비의 주요 시장으로서의 역할이 더욱 강화되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The rotary pumps market size is projected to expand from USD 11.20 billion in 2025 and USD 11.98 billion in 2026 to USD 16.87 billion by 2031, registering a 7.09% CAGR between 2026 and 2031.

Structural demand is strengthening as refineries retrofit high-viscosity service lines, Asian petrochemical complexes commission API-676 gear and screw models, and North American food processors replace legacy sanitary centrifugals to meet tightening hygiene rules. Offshore operators are standardizing twin-screw units on deep-water FPSOs to avoid pulsation-induced fatigue, while United States municipalities, armed with Infrastructure Investment and Jobs Act grants, are specifying rotary lobe and progressive-cavity pumps for sludge, digester, and influent duties. Rising adoption of digital-twin platforms that monitor vibration, temperature, and seal-health data is converting transactional spare-part sales into long-term monitoring contracts, handing an advantage to incumbents with large installed bases. Counterfeit aftermarket parts and stricter volatile-organic-compound (VOC) rules in Europe complicate total-cost-of-ownership calculations, yet API-676 certification and sensor-enabled reliability remain decisive purchase criteria across end markets.

Global Rotary Pumps Market Trends and Insights

Energy-Sector Brownfield Upgrades Driving High-Viscosity Fluid Handling Demand

Refiners across North America and the Middle East are redirecting capital from greenfield projects to debottlenecking programs that must accommodate heavier crude blends and renewable feedstocks, prompting large-scale replacement of centrifugal pumps with external-gear and twin-screw models certified for viscosities above 5,000 cP. Equinor's USD 1 billion modernization at the Mongstad refinery integrates electrified rotary pumps that are expected to curb Scope 2 emissions by 30%. The Oil and Gas Climate Initiative projects that member companies will require 2,500 additional rotary units by 2028, anchoring multi-year demand visibility. Strict API-676 seal, vibration, and casing limits restrict the qualified supplier pool, enabling compliant vendors to secure premium pricing. Together these factors ensure that even when overall refinery construction slows, brownfield replacement volumes for high-viscosity pumps will keep expanding.

Petrochemical Capacity Additions in China and India Requiring API-676 Compliant Rotary Pumps

China's record 14.81 million bpd throughput in 2025, supported by Rongsheng's 40 million t/yr Zhejiang complex, is steadily shifting long-term orders toward high-pressure gear and screw pumps that now include locally engineered 70 MPa ratings to reduce import dependence. India's 1.5 million bpd refinery expansion plan through 2030 has led Reliance and Indian Oil to pre-qualify twin-screw suppliers for polymer-grade propylene and butadiene transfer duties. The International Energy Agency forecasts petrochemical feedstock demand to rise 6.2% annually through 2030, reinforcing the pull for API-676 equipment across resin and elastomer plants. Engineering, procurement, and construction contractors are mandating dual-pressurized seals with leak-detection ports to satisfy tighter environmental rules, bolstering supplier differentiation. Consequently, Asian petrochemical mega-projects will remain the single largest booking source for compliant rotary pumps over the forecast horizon.

Availability of Low-Cost Counterfeit Spares from Unorganized Asian Vendors

The European Union Intellectual Property Office notes that counterfeit rotors, seals, and bearings now represent 12% of industrial parts seized at EU borders, with most originating in China and India. Substandard elastomers degrade quickly in high-temperature or chemically aggressive environments, leading to premature leaks and costly downtime. E-commerce platforms make uncertified parts easy to procure, overwhelming maintenance teams that lack strict vendor-qualification protocols. The Hydraulic Institute has introduced QR-code and blockchain authentication frameworks, but adoption outside North America remains limited, allowing gray-market channels to persist. Until plant operators universally implement verification systems, counterfeit spares will continue to erode legitimate aftermarket margins and damage OEM brand equity.

Other drivers and restraints analyzed in the detailed report include:

- Recovery of Offshore FPSO Construction in Brazil Boosting Twin-Screw Pump Orders

- Food-Grade Gear Pump Uptake Amid U.S. FSMA Clean-in-Place Mandates

- Strict VOC-Emission Rules Limiting Mechanical-Seal Selection for Rotary Pumps in EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

External-gear pumps commanded 32.47% of share in 2025 because their simple, rugged architecture tolerates sand-laden crude and high suction lift in upstream fields. Their share is expected to slide as twin-screw models, projected to grow 8.43% through 2031, solve pulsation and gas-entrainment issues common on FPSO topsides and polymer reactors. Seatrium's P-84 and P-85 FPSO contracts and NETZSCH's 1,400 m3/h XXLB-F launch confirm that operators and suppliers are scaling two-screw technology for mega-project service, reinforcing the shift toward performance-differentiated solutions. Internal-gear pumps, meanwhile, are securing hygienic niches in beverage, chocolate, and personal-care fluids where low shear is critical, while vane and triple-screw types remain limited to mobile hydraulics and high-pressure marine lubrication. Roto Pumps' modular P-Range shows that innovation continues in mature external-gear designs, but total cost-of-ownership metrics increasingly favor screw technologies that promise longer seal life and lower vibration.

Customer specifications now bundle API-676 compliance with digital-readiness, forcing vendors to embed sensor ports or factory-installed vibration probes even on standard frames. As energy-transition fuels such as bio-oils and renewable diesel flood pipelines, fluid viscosities vary more widely, amplifying the value of screw pumps that can adjust speed without losing volumetric efficiency. Consequently, competitive dynamics in the rotary pumps market should tilt toward suppliers capable of mass-producing robust, digitally enabled twin-screw platforms while retaining niche margins in external-gear replacement business.

Oil and gas accounted for 28.42% of the share in 2025 through broader upstream, midstream, and downstream deployment, yet the segment's forward momentum trails the headline market CAGR as decarbonization targets cap fossil-fuel capital spending. Food and beverage processors, by contrast, are forecast to expand pump purchases at a 9.11% CAGR through 2031 because FSMA mandates and EU Farm-to-Fork incentives compel systematic upgrades to sanitary equipment. Integrated sensors in new hygienic lines generate actionable data on cleaning cycles and process temperature, reducing compliance risk and explaining the segment's robust adoption curve.

Chemical and petrochemical plants still generate large-ticket orders for high-pressure, high-temperature gear and screw pumps, especially at Chinese and Indian complexes processing polymer-grade monomers. Water, wastewater, and power create steady base demand, with Infrastructure Investment and Jobs Act allocations lining up progressive-cavity and lobe pump replacements in aging U.S. facilities. Mining, pulp, and paper add volatility-resilient demand for abrasion-resistant rotary designs, ensuring that supplier revenue streams become more diversified and less sensitive to oil-price cycles over the forecast horizon.

The Rotary Pumps Market Report is Segmented by Type (External-Gear, Internal-Gear, and More), End-User Industry (Oil and Gas, Power Generation, Chemicals and Petrochemicals, Food and Beverage, and More), Discharge Pressure (Up To 10 Bar, 10-25 Bar, 25-100 Bar, and Above 100 Bar), Pump Capacity (Up To 50 M3/H, 51-150 M3/H, 151-500 M3/H, and Above 500 M3/H), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 40.19% of share in 2025, buoyed by record Chinese refinery runs and India's import-substitution policy that channels orders to domestic API-676 suppliers. The Middle East and Africa are forecast to post a 9.08% CAGR as Saudi Aramco's Jazan expansion, the UAE's Ruwais complex, and Nigeria's 650,000 bpd Dangote refinery reach full capacity, each specifying high-flow, high-pressure gear and screw models. North America benefits from brownfield hydroprocessing upgrades and USD 50 billion in federal water-infrastructure spending that subsidizes municipal pump replacements, anchoring a dependable order pipeline.

Europe combines hygienic pump innovation with VOC-induced retrofit headwinds, producing steady but not spectacular growth as operators weigh the cost of double seals against sealless options. South America's trajectory leans heavily on Brazil's FPSO build program and Chilean copper-concentrate pipelines, ensuring a long though narrower backlog for abrasion-resistant and low-pulsation units. Overall, geographic diversification tempers macro volatility and supports a balanced global growth outlook for rotary pump suppliers.

Asia's developed economies are also pivoting toward lower-carbon fuels, with Japan repurposing one-third of its idled refining capacity for sustainable-aviation-fuel production, a shift that is already generating new tenders for duplex-steel twin-screw pumps rated above 100 bar. Australia's LNG liquefaction operators are meanwhile installing rotary lobe and progressive-cavity units on water-treatment modules to comply with tightened discharge permits, expanding aftermarket service revenue for vendors that maintain Perth or Darwin service depots. South Korea is upgrading chemical recycling lines at Ulsan and Yeosu to process mixed plastic waste, specifying API-676 gear pumps fitted with magnetic couplings to eliminate fugitive VOC emissions and meet Industrial Emissions Directive-equivalent local standards. Finally, Singapore's Jurong Island is adding bio-cracker capacity that calls for above-500 m3/h screw pumps capable of handling fatty-acid feedstocks with viscosities above 1,000 cP, reinforcing Southeast Asia's role as a premium market for high-performance rotary equipment.

- Dover Corporation (Pump Solutions Group)

- IDEX Corporation (Viking Pump)

- Colfax Corporation (IMO / Allweiler)

- SPX Flow Inc.

- Xylem Inc.

- Atlas Copco AB

- Gardner Denver Holdings Inc.

- Pfeiffer Vacuum Technology AG

- ULVAC Inc.

- Busch SE

- Flowserve Corporation

- KSB SE and Co. KGaA

- Netzsch Pumpen and Systeme GmbH

- Alfa Laval AB

- PCM SA

- Seepex GmbH

- ITT Inc.

- Sulzer Ltd.

- DESMI A/S

- Kirloskar Brothers Ltd.

- Verder Group

- Roto Pumps Ltd.

- Tuthill Corporation

- Blackmer (PSG brand)

- Vogelsang GmbH and Co. KG

- Roper Technologies Inc. (Roper Pump Company)

- Leistritz AG

- Eureka Pumps AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-Sector Brown-Field Upgrades Driving High-Viscosity Fluid Handling Demand

- 4.2.2 Petrochemical Capacity Additions in China and India Requiring API-676 Compliant Rotary Pumps

- 4.2.3 Recovery of Offshore FPSO Construction in Brazil Boosting Twin-Screw Pump Orders

- 4.2.4 Food-Grade Gear Pump Uptake Amid U.S. FSMA Clean-In-Place Mandates

- 4.2.5 Rising European Craft-Brewery Installations Favoring Low-Shear Lobe Pumps

- 4.2.6 AI-Enabled Predictive Maintenance Models Increasing Aftermarket Revenues

- 4.3 Market Restraints

- 4.3.1 Availability of Low-Cost Counterfeit Spares from Unorganized Asian Vendors

- 4.3.2 Strict VOC-Emission Rules Limiting Mechanical-Seal Selection for Rotary Pumps in EU

- 4.3.3 High Upfront Cost Versus Centrifugal Alternatives in Municipal Water Plants

- 4.3.4 Skilled-Labor Shortage for Screw-Pump Maintenance in Sub-Saharan Africa

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 External-Gear

- 5.1.2 Internal-Gear

- 5.1.3 Twin-Screw

- 5.1.4 Triple-Screw

- 5.1.5 Vane

- 5.2 By End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Power Generation

- 5.2.3 Chemicals and Petrochemicals

- 5.2.4 Food and Beverage

- 5.2.5 Water and Waste-water

- 5.2.6 Other End-user Industries

- 5.3 By Discharge Pressure

- 5.3.1 Up to 10 bar

- 5.3.2 10-25 bar

- 5.3.3 25-100 bar

- 5.3.4 Above 100 bar

- 5.4 By Pump Capacity (m3/h)

- 5.4.1 Up to 50

- 5.4.2 51-150

- 5.4.3 151-500

- 5.4.4 Above 500

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Dover Corporation (Pump Solutions Group)

- 6.4.2 IDEX Corporation (Viking Pump)

- 6.4.3 Colfax Corporation (IMO / Allweiler)

- 6.4.4 SPX Flow Inc.

- 6.4.5 Xylem Inc.

- 6.4.6 Atlas Copco AB

- 6.4.7 Gardner Denver Holdings Inc.

- 6.4.8 Pfeiffer Vacuum Technology AG

- 6.4.9 ULVAC Inc.

- 6.4.10 Busch SE

- 6.4.11 Flowserve Corporation

- 6.4.12 KSB SE and Co. KGaA

- 6.4.13 Netzsch Pumpen and Systeme GmbH

- 6.4.14 Alfa Laval AB

- 6.4.15 PCM SA

- 6.4.16 Seepex GmbH

- 6.4.17 ITT Inc.

- 6.4.18 Sulzer Ltd.

- 6.4.19 DESMI A/S

- 6.4.20 Kirloskar Brothers Ltd.

- 6.4.21 Verder Group

- 6.4.22 Roto Pumps Ltd.

- 6.4.23 Tuthill Corporation

- 6.4.24 Blackmer (PSG brand)

- 6.4.25 Vogelsang GmbH and Co. KG

- 6.4.26 Roper Technologies Inc. (Roper Pump Company)

- 6.4.27 Leistritz AG

- 6.4.28 Eureka Pumps AS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment