|

시장보고서

상품코드

2044109

고강도강 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)High Strength Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

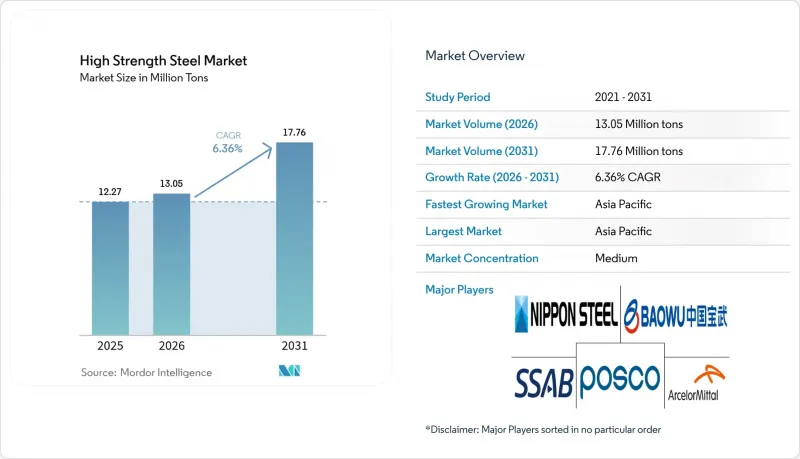

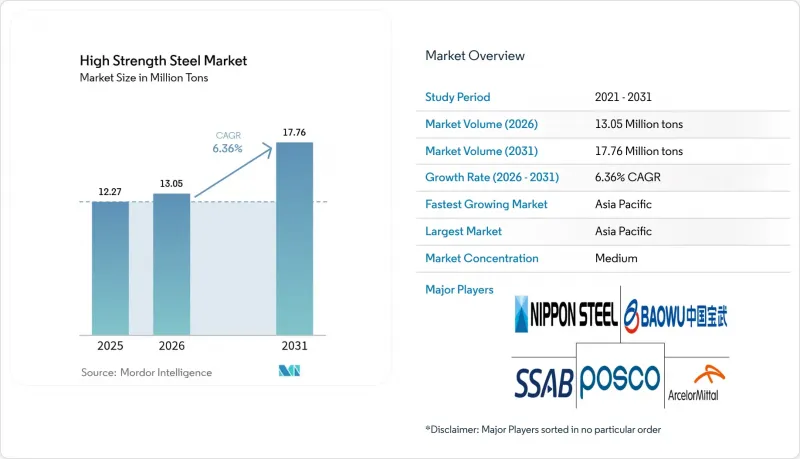

고강도강 시장 규모는 2025년 1,227만 톤에서 2026년에는 1,305만 톤으로 확대되어 2026년부터 2031년까지 CAGR 6.36%로 성장을 지속하여, 2031년까지 1,776만 톤에 이를 것으로 예측됩니다.

자동차 경량화 규제, 모듈식 고층 건축 및 해상 풍력 발전 타워의 건설 확대는 인장강도가 600MPa 이상이고 충돌 에너지 흡수성이 높은 강종에 대한 수주량 증가와 직결되어 있습니다. 듀플렉스강은 페라이트-마텐자이트 매트릭스가 복잡한 성형 공정에서도 연신율을 유지하기 때문에 가격 프리미엄이 붙습니다. 이 특성은 자동차 제조업체들이 도어 내부와 휠 하우징의 스탬핑 부품에 활용하고 있습니다. 열간성형강은 측면 충돌 시험을 견디면서 리튬이온 모듈을 열 폭주로부터 보호해야 하는 배터리 전기자동차의 섀시 프레임에 빠르게 채택이 확대되고 있습니다. 동시에 미량 합금화 페라이트-베이나이트 강판이 수소 대응 파이프라인의 최적 소재로 부상하고 있으며, 대구경 간선 파이프라인이 시험단계에서 상업적 규모로 전환되면 미래 성장 거점이 될 것으로 전망되고 있습니다.

세계 고강도강 시장 동향과 인사이트

자동차 경량화 및 충돌 안전 규제

유럽연합(EU)의 차량 CO2 배출량 상한선 95g/km와 미국의 54.5 마일/갤런 목표에 따라 자동차 제조업체들은 점점 더 까다로워지는 스몰 오버랩 충돌 테스트와 측면 충돌 테스트를 통과하면서도 화이트 바디의 질량을 20-30% 줄일 수 있는 연강으로 전환할 수밖에 없는 상황입니다. 미국 고속도로안전보험협회(IIHS)의 프로토콜 업데이트로 인해 탑승자 생존 공간의 기준이 높아졌고, 그 결과 핫스탬핑 성형된 1,500MPa의 B필러에 대한 수요가 증가했습니다. 제너럴 모터스(GM)에 따르면, 현재 Ultium 기반 트럭은 운전실 구조에 980 MPa의 이중상 강판을 채택하여 차량 중량을 180kg 줄이고 비틀림 강성을 15% 향상시켰다고 합니다. 중국 GB 38900-2020 시험 표준은 측면 기둥 충돌 시험과 지붕 붕괴 시험을 결합하여 A 기둥과 B 기둥의 설계에서 마르텐사이트계 및 복상강이 유리하게 작용할 수 있습니다. 포드는 프레스 경화 강철로 만든 배터리 인클로저가 알루미늄 압출재를 추가하지 않고도 연방 자동차 안전 표준 305(FMVSS 305)를 충족하고 차체 하부 조립을 간소화할 수 있음을 확인했습니다.

모듈식 고층 건축의 급속한 성장

조립식 강재 모듈은 S460-S690 등급의 기둥이 더 얇은 벽 두께로 동일한 하중을 지탱하기 때문에 건설업체는 도심의 건설 공사 기간을 30% 단축하고 임대 가능한 바닥 면적을 확보할 수 있습니다. 싱가포르 건축건설청(BCA)에 따르면, 2025년에는 주택 프로젝트의 22%가 모듈식 건축을 채택할 것이며, 대부분의 개발업체는 생산성 지표를 충족하기 위해 고강도 중공형강을 지정하고 있습니다. 바오스틸(Baosteel)은 기존 공사기간을 6개월 단축한 심천 고층빌딩에 Q460/Q550 강판 8만 5,000톤을 공급했습니다. 2024년판 국제건축기준(IBC)에서는 내진 지역에서 ASTM A913 Grade 65의 허용응력 한계가 상향 조정되어 캘리포니아 주와 일본에서의 사용 범위가 확대되고 있습니다. 타타스틸이 2024년에 출시한 S700MC는 -40°C 이하의 샤르피 인성을 가진 용접 가능한 형강을 필요로 하는 스칸디나비아의 모듈식 건설업체를 대상으로 합니다.

생산 비용 및 합금 원소 비용 상승

인도네시아의 매트(조제니켈) 수출 규제와 배터리 수요 급증으로 2025년 니켈 가격은 톤당 평균 18,500달러로 2024년 대비 22% 상승했습니다. 남아공의 노동쟁의가 공급을 방해하면서 크롬 현물 가격이 톤당 11,200달러까지 상승하여 스테인리스 스틸과 고장력강 생산비용이 10-15% 상승했습니다. 칠레의 광산들이 물 부족으로 생산량을 줄였기 때문에 몰리브덴 가격은 1kg당 45달러에 이르렀습니다. 아르셀로미탈은 합금 가격의 급등으로 인해 자동차 강재 사업에서 180bp의 이익률 압박이 발생했다고 밝히며, 자동차 제조업체와 분기별 가격 재협상에 착수했습니다. 동남아시아의 미니밀은 합금 시장이 안정될 때까지 마르텐사이트계 라인 가동을 연기하고 있어 생산량 증가가 지연되고 있습니다.

부문 분석

이중상(DP) 강은 2025년 고장력강 시장 규모의 25.16%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 6.72%로 확대될 것으로 예측됩니다. 이는 성형성과 600-1,200 MPa의 인장강도라는 매력적인 조합으로 대부분의 충돌 안전 기준을 충족하기 때문입니다. 폭스바겐의 MEB 플랫폼은 사이드실과 리어 플로어 크로스 멤버에 DP 980을 채택하여 최신 Euro NCAP 측면 충돌 기준을 충족시키면서 차량 중량을 12% 줄였습니다.

1,200 MPa 이상의 마르텐사이트계 및 열간 성형용 강종은 도어 인입 빔과 배터리 인클로저에 채용이 확대되고 있지만, 가공 비용이 높고 성형성이 제한적이라는 문제점이 있습니다. 이러한 문제는 국소 레이저 트리밍을 통해 완화되고 있습니다. 구멍 확대율이 우수한 복합상 강판은 다축 하중을 받는 서스펜션 암에, 페라이트-베이나이트 강판은 용접성을 중시하는 대형 트럭의 섀시 레일에 적용되고 있습니다. 담금질 및 분할강은 아직 파일럿 규모에 머물러 있지만, 2,000MPa의 인장강도와 10%의 연신율이라는 특성은 스케일업 문제가 해결되면 향후 일체형 도어링에 널리 보급될 수 있음을 시사합니다.

"고강도강 시장 보고서는 제품 유형(이중상, 복합상, 마르텐사이트계 등), 최종 사용자 산업(자동차 및 운송, 건축 및 건설, 건설기계 및 광업, 항공우주 및 방위산업, 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 로 분류되어 있습니다. 시장 예측은 수량(톤) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 고장력강 시장의 63.69%를 차지하며 시장을 주도했습니다. 배터리 전기차 생산량 증가와 인프라 투자 확대로 2031년까지 연평균 복합 성장률(CAGR) 6.81%를 유지할 것으로 예측됩니다. 중국은 2025년에 940만 대의 플러그인 하이브리드 자동차를 생산할 예정이며, 자동차 제조업체가 이중상 및 열간 성형 솔루션으로 전환할 수 있도록 GB 38900-2020 테스트 표준을 시행하고 있습니다. 인도의 '바랏말라 프로젝트' 2단계에서는 1만 2,000km의 고속도로가 신설될 예정입니다. 일본과 한국에서는 하이브리드 세단의 무게를 20% 절감하는 1,800MPa의 프레스 경화 도어링을 도입하고 있으며, 아세안 각국 정부는 중국 및 일본 자동차 업체를 유치하여 지역 내 코일 센터에 연속 소둔라인 가동을 추진하고 있습니다.

북미에서는 미국 인플레이션 억제법이 국내 조달을 장려하고 있으며, 이에 따라 Nucor사와 Cleveland-Cliffs사는 스케이트보드형 섀시용 블랭크를 공급하기 위해 연속 어닐링 설비를 보강하고 있습니다. 캐나다는 배터리 제조에 130억 캐나다 달러(96억 달러)를 투자하고, 공장 건설 중 대량의 고장력 빔과 강판을 흡수하게 됩니다. 멕시코는 2025년 380만 대의 차량을 생산할 것으로 예상되며, 국경 간 공급망이 전기 픽업 트럭으로 전환되면서 차량 1대당 최대 280kg의 고급 철강재 사용량이 증가했습니다.

유럽에서는 탄소국경조정세(CBAM)로 인해 스크랩을 원료로 하는 전기 아크로로의 전환이 가속화되고 있으며, 독일 자동차 제조업체들은 Scope 3의 목표 달성을 위해 이 가치 제안을 적극적으로 도입하고 있습니다. 영국의 해상풍력 발전 용량은 16GW에 이르렀고, S460/S500 모노파일용 강판이 소비되었습니다. 한편, 프랑스에서는 원자력 발전소 격납용기에 S690이 채택되어 원자로 건설에 있어 고품질 수요 기회가 열렸습니다. 남미, 중동 및 아프리카의 생산량은 규모는 작지만 두 자릿수 성장을 기록하고 있으며, 브라질의 광산용 트럭과 사우디아라비아의 수소 파이프라인이 견인차 역할을 하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The High Strength Steel Market size is expected to grow from 12.27 Million tons in 2025 to 13.05 Million tons in 2026 and is forecast to reach 17.76 Million tons by 2031 at 6.36% CAGR over 2026-2031.

Automotive lightweighting mandates, modular high-rise construction, and offshore-wind tower build-outs are translating directly into larger order books for grades that couple tensile strengths above 600 MPa with high crash energy absorption. Dual-phase steel commands price premiums because its ferrite-martensite matrix preserves elongation during complex forming, a property automakers exploit for door inners and wheel-housing stampings. Hot-formed steel is scaling quickly in battery-electric chassis frames that must withstand side-impact tests while shielding lithium-ion modules from thermal runaway. At the same time, micro-alloyed ferritic-bainitic plate has emerged as the material of choice for hydrogen-ready pipelines, signalling a future growth node once large-diameter trunk lines move from pilot to commercial scale.

Global High Strength Steel Market Trends and Insights

Automotive Lightweighting and Crash-Safety Mandates

Fleet CO2 caps of 95 g/km in the European Union and a 54.5 miles-per-gallon target in the United States oblige automakers to swap mild steel for grades that remove 20-30% body-in-white mass while passing ever tougher small-overlap and side-impact tests. Updates to the Insurance Institute for Highway Safety protocol raised the bar for occupant survival space, which in turn lifted demand for 1,500 MPa B-pillars formed by hot stamping. General Motors reports that Ultium-based trucks now use dual-phase 980 MPa sheet in cab structures, trimming 180 kg from curb weight and raising torsional rigidity 15%. China's GB 38900-2020 test regimen couples side-pole impacts with roof-crush metrics, a combination that rewards martensitic and complex-phase steels in A- and B-pillar designs. Ford confirms that press-hardened steel battery enclosures satisfy Federal Motor Vehicle Safety Standard 305 without adding aluminum extrusions, simplifying under-body assembly.

Rapid Growth of Modular High-Rise Construction

Prefabricated steel modules allow contractors to cut inner-city build schedules by 30% because columns of S460-S690 grade carry identical loads at thinner wall thicknesses, freeing rentable floor space. Singapore's Building and Construction Authority states that modular starts rose to 22% of residential projects in 2025, and most developers specify high strength hollow sections to comply with productivity metrics. Baosteel supplied 85,000 tons of Q460/Q550 plate for Shenzhen towers that shaved six months off traditional timelines. The 2024 International Building Code permits higher stress limits for ASTM A913 Grade 65 in seismic zones, widening usage in California and Japan. Tata Steel's S700MC launch in 2024 targets Scandinavian modular firms that require weldable sections with Charpy toughness below -40 °C.

High Production and Alloying-Element Cost Inflation

Nickel averaged USD 18,500 per ton in 2025, 22% above 2024, after Indonesia tightened matte exports and battery demand surged. Chromium spot prices rose to USD 11,200 per ton when South African labor strikes disrupted supply, lifting stainless and high strength production costs 10-15%. Molybdenum reached USD 45 per kg as Chilean mines curtailed output amid water scarcity. ArcelorMittal disclosed a 180-basis-point margin squeeze in its automotive steel business due to alloy inflation, prompting quarterly price renegotiations with automakers. Southeast Asian mini-mills have postponed martensitic line start-ups until alloy markets stabilize, delaying incremental volume.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind Tower Build-Out Accelerates Demand

- Hydrogen-Ready Pipeline Specifications for Micro-Alloyed HSS

- Joining and Welding Challenges for High-Strength Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dual-phase (DP) captured a 25.16% share of the high strength steel market size in 2025 and is forecast to advance at a 6.72% CAGR through 2031, benefiting from an attractive mix of formability and 600-1,200 MPa tensile strength that meets most crash-safety targets. Volkswagen's MEB platform uses DP 980 in side sills and rear floor cross-members, trimming vehicle mass 12% while satisfying latest Euro NCAP side-impact norms.

Martensitic and hot-formed grades above 1,200 MPa are expanding in door-intrusion beams and battery enclosures but incur higher processing costs and limited formability, issues mitigated by localized laser trimming. Complex-phase sheet with superior hole-expansion ratio wins suspension arms that experience multi-axial loads, while ferritic-bainitic plate secures chassis rails in heavy trucks that prioritize weldability. Quenched-and-partitioned steel remains pilot scale, yet its 2,000 MPa tensile strength plus 10% elongation profile signals future penetration in one-piece door rings once scaling challenges resolve.

The High Strength Steel Market Report is Segmented by Product Type (Dual-Phase, Complex Phase, Martensitic, and More), End-User Industry (Automotive and Transportation, Building and Construction, Yellow Goods and Mining, Aerospace and Defense, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific dominated the high strength steel market with 63.69% volume in 2025; rising battery-electric output and infrastructure spending will sustain a 6.81% CAGR to 2031. China built 9.4 million plug-in vehicles in 2025 and enforces GB 38900-2020 test norms that steer automakers toward dual-phase and hot-formed solutions. India's Bharatmala Phase II adds 12,000 km of highways. Japan and South Korea are introducing 1,800 MPa press-hardened door rings that cut mass by 20% in hybrid sedans, while ASEAN governments court Chinese and Japanese carmakers, pushing regional coil centers to commission continuous-annealing lines.

In North America, the U.S. Inflation Reduction Act incentivizes domestic sourcing, prompting Nucor and Cleveland-Cliffs to add continuous-annealing capacity to supply skateboard chassis blanks. Canada committed CAD 13 billion (USD 9.6 billion) to battery manufacturing that will absorb a large amount of high strength beams and plates during plant builds. Mexico produced 3.8 million vehicles in 2025, with per-unit advanced steel content up to 280 kg as cross-border supply chains pivot to electric pickups.

In Europe, Carbon Border Adjustment fees accelerate the switch to scrap-based electric-arc furnaces for lower embedded emissions, a value proposition German automakers embrace to meet scope-3 targets. Offshore-wind capacity in the United Kingdom reached 16 GW, consuming S460/S500 monopile plate, while France adopted S690 for nuclear containment shells, opening a high-grade opportunity in reactor builds. South America and the Middle-East and Africa clock smaller volumes yet post double-digit growth, anchored by Brazilian mining trucks and Saudi Arabian hydrogen pipelines.

- AM/NS India

- ArcelorMittal

- BlueScope

- China Baowu Steel Group Corp., Ltd.

- ChinaSteel

- CITIC Pacific Special Steel

- Cleveland-Cliffs Inc.

- Gerdau S/A

- HYUNDAI STEEL

- JFE Steel Corporation

- JSW Steel

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SSAB

- Tata Steel

- thyssenkrupp Steel Europe

- United States Steel Corporation

- Voestalpine AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive lightweighting and crash-safety mandates

- 4.2.2 Rapid growth of modular high-rise construction

- 4.2.3 Offshore-wind tower build-out accelerates demand

- 4.2.4 Hydrogen-ready pipeline specifications for micro-alloyed HSS

- 4.2.5 Battery-electric skateboard chassis adoption

- 4.3 Market Restraints

- 4.3.1 High production and alloying-element cost inflation

- 4.3.2 Raw-material price volatility (iron ore, alloys)

- 4.3.3 Joining and welding challenges for high-strength grades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Supply Analysis

- 4.7 Regulatory Policy Analysis

- 4.8 Trade Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Dual-Phase (DP)

- 5.1.2 Complex Phase (CP)

- 5.1.3 Martensitic

- 5.1.4 Ferritic-Bainitic (FB)

- 5.1.5 Hot-Formed (HF)

- 5.1.6 Other Product Types (Quenched and Partitioned (QandP), etc.)

- 5.2 By End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Building and Construction

- 5.2.3 Yellow Goods and Mining

- 5.2.4 Aerospace and Defense

- 5.2.5 Other End-user Industries (Renewable Energy, etc.)

- 5.3 By Geography (Volume)

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacifc

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AM/NS India

- 6.4.2 ArcelorMittal

- 6.4.3 BlueScope

- 6.4.4 China Baowu Steel Group Corp., Ltd.

- 6.4.5 ChinaSteel

- 6.4.6 CITIC Pacific Special Steel

- 6.4.7 Cleveland-Cliffs Inc.

- 6.4.8 Gerdau S/A

- 6.4.9 HYUNDAI STEEL

- 6.4.10 JFE Steel Corporation

- 6.4.11 JSW Steel

- 6.4.12 LIBERTY Steel Group

- 6.4.13 NIPPON STEEL CORPORATION

- 6.4.14 Nucor Corporation

- 6.4.15 POSCO

- 6.4.16 SSAB

- 6.4.17 Tata Steel

- 6.4.18 thyssenkrupp Steel Europe

- 6.4.19 United States Steel Corporation

- 6.4.20 Voestalpine AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment