|

시장보고서

상품코드

2044113

섬유 화학제품 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Textile Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

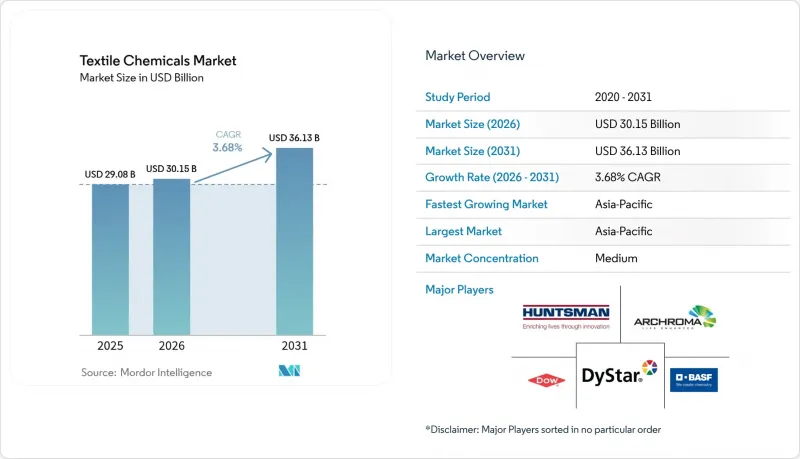

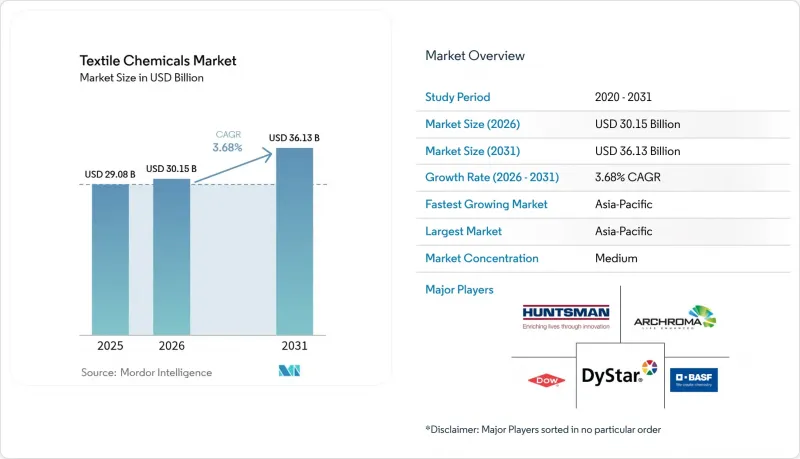

섬유 화학제품 시장 규모는 2025년 290억 8,000만 달러에서 2026년에는 301억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 3.68%로 성장을 지속하여, 2031년에는 361억 3,000만 달러에 이를 것으로 예측됩니다.

이러한 완만한 성장은 보다 엄격한 환경 규제와 지속 가능한 제조에 대한 수요 증가에 적응하고 있는 성숙한 산업계의 상황을 반영하고 있습니다. 아시아태평양의 견조한 성장, 디지털 인쇄의 보급 확대, 기능성 마감재에 대한 관심 증가와 함께 섬유 화학 산업 전반의 경쟁 우선순위를 재구성하고 있습니다. 현재 진행 중인 PFAS의 단계적 폐지 및 석유화학제품의 가격 변동으로 인해 단기적인 모멘텀이 둔화되고 있지만, 바이오 효소 기술 및 수성 기술에 대한 지속적인 투자로 섬유화학 산업의 장기적인 성장 전망은 유지될 것으로 예측됩니다.

세계 섬유 화학제품 시장 동향과 인사이트

아시아태평양 섬유 생산의 견조한 성장세

급속한 생산 능력 증가와 정부의 지원책으로 아시아태평양 전체 섬유 화학제품 시장이 성장하고 있습니다. 2024년 중국의 섬유 수출액은 5.7% 증가한 1,419억 6,000만 달러에 달해, 코팅, 사이징, 착색 공정의 대규모 화학제품 소비가 유지되고 있습니다. 인도의 생산 연동형 인센티브(PLI) 프로그램은 합성섬유에 10,683칼로리 루피가 할당되어 고성능 마감제에 대한 장기적인 수요를 견인하고 있습니다. 지역 중심공급망을 통해 바이오 및 저 VOC 화학제품의 신속한 도입이 가능하여 아시아태평양이 세계 섬유 화학 산업에서 중심적인 위치를 강화할 수 있게 되었습니다.

산업용 및 기능성 섬유에 대한 수요 증가

자동차 경량화 및 의료 위생 요구 사항으로 인해 난연성, 항균성, 내열성을 가진 화학제품에 대한 새로운 사양 기준이 확립되고 있습니다. 산업용 섬유 부문의 CAGR 4.11%는 섬유 화학제품 시장이 범용 제품에서 고가의 고가 용도 특화형 제제로 전환하고 있음을 보여줍니다. 나노기술을 활용한 마감제는 성능 기준을 더욱 높이고, 전문 공급업체들 간의 연구개발 경쟁을 더욱 치열하게 하고 있습니다.

염색 및 마감 공정의 오염 방지 비용

사업자들이 COD 및 BOD 배출 기준치 인하에 대응하기 위해 노력하는 가운데, 폐수처리시설의 개보수는 현재 막대한 설비투자가 필요한 상황입니다. 생물처리 및 막처리 기술에 대한 투자 자금을 확보할 수 없는 소규모 가공업체들은 철수하거나 합병하고 있으며, 그 결과 규제에 대응할 수 있는 대형 바이어들에게 화학물질 수요가 집중되고 있습니다. 이러한 구조조정으로 인해 섬유 화학제품 시장의 진입장벽이 높아졌고, 전환 비용도 상승하고 있습니다.

부문 분석

코팅 및 사이징용 화학물질은 2025년 매출의 27.96%를 차지하며, 섬유 및 니트 제품 생산량을 뒷받침할 것으로 예측됩니다. 이들 제품은 널리 보급되어 안정적인 기초 수요가 확보되어 패션 사이클의 침체기에도 섬유 화학제품 시장을 안정적으로 유지하고 있습니다. 그러나 혁신이 가장 두드러지는 분야는 마감제 분야로, 고객이 단일 처리 공정에서 발수성, 신축성 유지, 항균 기능을 요구함에 따라 2031년까지 연평균 복합 성장률(CAGR) 4.12%를 나타낼 것으로 예측됩니다.

환경 성능이 제품 파이프라인의 차별화 요소로 작용하고 있으며, 다기능 실리콘 폴리머 하이브리드가 불소계 발수제를 대체하고 있습니다. 탈지제는 폐수 부하를 줄이는 바이오 효소계 대체품으로 전환되고 있습니다. 이러한 발전이 결합되어 수익의 핵심을 유지하면서 수익률을 향상시키고 섬유 화학 시장에서 풍부한 비즈니스 기회를 더욱 공고히 하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 70.74%를 차지해, 중국의 3,011억 달러 규모의 수출 기반과 2030년까지 3,500억 달러 규모에 달할 것으로 예상되는 인도의 산업이 그 뒤를 잇고 있습니다. 각 지역 정부는 생산 능력 확대와 기능성 섬유 클러스터에 대한 보조금을 지속적으로 지원하고 있으며, 이는 3.86%의 연평균 복합 성장률(CAGR)을 유지하며 세계 섬유 화학제품 시장을 뒷받침하고 있습니다. 섬유 방적에서 의류 봉제까지 이어지는 공급망의 두께는 새로운 친환경 화학 기술의 신속한 실용화를 가능하게 하여 아시아태평양의 지속적인 리더십을 보장하고 있습니다.

북미는 규모는 작지만 전략적으로 중요한 점유율을 차지하고 있으며, 단가보다 사양 적합성이 우선시되는 방호용, 항공우주용, 의료용 원단을 전문적으로 취급하고 있습니다. 미국 브랜드에 대한 멕시코의 니어쇼어링 모멘텀은 지역 내 원사 염색 공장의 투자를 다시 활성화하고 고부가가치 보조제 시장에 새로운 길을 열어주고 있습니다. 캘리포니아와 뉴욕주의 PFAS 규제는 수성 발수제의 채택을 가속화하여 북미를 섬유 화학 산업에서 차세대 지속 가능한 대안의 시험장으로 자리매김하고 있습니다.

유럽의 성숙한 부문은 첨단 기계 장비와 순환 경제를 촉진하는 견고한 규제 프레임워크의 혜택을 누리고 있습니다. 섬유에서 섬유로의 재활용 화학물질에 대한 투자가 증가하고 있으며, 독일과 이탈리아가 폴리에스테르 분해공장의 선구자 역할을 하고 있습니다. 견고한 고급 및 기능성 섬유 부문은 환경 친화적인 마감재에 대한 연구 개발에 자금을 지원하여 세계 표준에 대한 유럽의 영향력을 유지하고 있습니다. 남미와 중동의 신흥 지역은 생산량을 확대하고 있지만, 인프라 부족으로 인해 섬유 화학 산업으로의 본격적인 통합이 늦어지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Textile Chemicals Market size market is expected to grow from USD 29.08 billion in 2025 to USD 30.15 billion in 2026 and is forecast to reach USD 36.13 billion by 2031 at 3.68% CAGR over 2026-2031.

This moderate growth reflects a maturing sector that is adapting to stricter environmental regulations and rising demand for sustainable manufacturing. Robust expansion in Asia Pacific, escalating adoption of digital printing, and heightened focus on functional finishes are together reshaping competitive priorities across the textile chemicals industry. Ongoing PFAS phase-outs and petrochemical price swings are tempering near-term momentum, yet sustained investment in bio-enzymatic and water-based technologies is expected to preserve long-run growth visibility within the textile chemicals industry.

Global Textile Chemicals Market Trends and Insights

Robust Growth in Asia Pacific Textile Production

Rapid capacity additions and supportive government incentives are lifting the textile chemicals market across Asia Pacific. China's 2024 textile exports grew 5.7% to USD 141.96 billion, sustaining large-scale chemical consumption in coating, sizing, and colorant operations. India's Production Linked Incentive program earmarking INR 10,683 crore for man-made fibres is steering long-run demand for high-performance finishes. Concentrated regional supply chains enable swift adoption of bio-based and low-VOC chemistries, reinforcing Asia Pacific's centrality within the global textile chemicals industry.

Rising Demand for Technical/Industrial Textiles

Automotive lightweighting and medical hygiene requirements are setting new specification baselines for flame-retardant, antimicrobial, and thermally resilient chemistries. The industrial textiles segment's 4.11% CAGR highlights how the textile chemicals market is transitioning from commodity volumes toward application-specific formulations that command premium pricing. Nanotechnology-enabled finishes are further elevating performance thresholds, intensifying R&D competition among specialty suppliers.

Pollution Control Costs in Dyeing and Finishing

Wastewater treatment upgrades now absorb significant capital outlays as operators strive to meet lower COD and BOD discharge limits. Smaller processors that cannot finance biological and membrane technologies are exiting or merging, consolidating chemical demand among larger, compliance-ready buyers. This restructuring raises entry barriers and raises switching costs within the textile chemicals market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global Regulations Favouring Low-VOC Chemistries

- Boom in Digital-Textile Printing Inks and Auxiliaries

- Volatile Petrochemical Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coating and sizing chemicals commanded 27.96% of 2025 revenue, underpinning throughput across weaving and knitting lines. Their ubiquity secures steady baseline demand, stabilising the textile chemicals market even during fashion-cycle downturns. Innovation, however, is most visible in finishing agents, expected to grow at 4.12% CAGR through 2031 as customers request water-repellent, stretch-retentive, and antimicrobial functionalities in a single bath.

Environmental performance is differentiating product pipelines, with multifunctional silicone-polymer hybrids displacing fluorinated repellents. Desizing agents have shifted toward bio-enzymatic alternatives that reduce effluent load. Collectively these advances preserve the revenue core while elevating margins, reinforcing the wealth of opportunity in the textile chemicals market.

The Textile Chemicals Market Report is Segmented by Type (Coating and Sizing Chemicals, Colorants and Auxiliaries, and More), Raw Material (Natural Fibres, Synthetic Fibres, and More), Application (Apparel, Home Furnishing, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 70.74% revenue in 2025, supported by China's USD 301.1 billion export base and India's projected USD 350 billion industry by 2030. Regional governments continue to subsidise capacity expansion and technical-textile clusters, maintaining a 3.86% CAGR that anchors the global textile chemicals market. Supply-chain depth, from fibre spinning to garment assembly, allows rapid qualification of new green chemistries, ensuring Asia Pacific's sustained leadership.

North America holds a smaller yet strategically important share, specialising in protective, aerospace, and medical fabrics where specification compliance trumps unit cost. Mexico's near-shoring momentum to US brands is reigniting regional yarn dyehouse investments, opening fresh routes for high-value auxiliaries. California and New York PFAS rules accelerate adoption of water-based repellents, positioning North America as a testbed for next-wave sustainable options within the textile chemicals industry.

Europe's mature sector benefits from advanced machinery and a robust regulatory framework that favours circularity. Investment in textile-to-textile recycling chemicals is climbing, with Germany and Italy pioneering polyester depolymerisation plants. Strong luxury and technical segments fund R&D in low-impact finishes, upholding Europe's influence on global standards. Emerging regions in South America and the Middle East are scaling output but remain constrained by infrastructure gaps, delaying their fuller integration into the textile chemicals industry.

- Achitex Minerva SpA

- Albemarle Corporation

- Archroma

- BASF

- Bozzetto Group

- CHT Group

- Clariant AG

- Covestro AG

- Croda International PLC

- Dow Inc.

- DyStar Group

- Evonik Industries AG

- Huntsman International LLC

- Kemira Oyj

- Kiri Industries Ltd

- K-Tech (India) Ltd

- L. N. Chemical Industries

- Nouryon

- Rudolf GmbH

- Sarex

- Sumitomo Chemical Co. Ltd

- Tanatex Chemicals BV

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth in Asia Pacific textile production

- 4.2.2 Rising demand for technical/industrial textiles

- 4.2.3 Stricter global regulations favouring low-VOC chemistries

- 4.2.4 Boom in digital-textile printing inks and auxiliaries

- 4.2.5 Rapid adoption of bio-enzymatic processing solutions

- 4.3 Market Restraints

- 4.3.1 Pollution control costs in dyeing and finishing

- 4.3.2 Volatile petrochemical feedstock prices

- 4.3.3 PFAS and other substance phase-outs raising reformulation costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.1.1 Bargaining Power of Buyers

- 4.5.1.2 Threat of New Entrants

- 4.5.1.3 Threat of Substitutes

- 4.5.1.4 Degree of Competitive Rivalry

- 4.5.1 Bargaining Power of Suppliers

5 Market Size and Growth Forecasts

- 5.1 By Type

- 5.1.1 Coating and Sizing Chemicals

- 5.1.2 Colorants and Auxiliaries

- 5.1.3 Finishing Agents

- 5.1.4 Desizing Agents

- 5.1.5 Other Types (Yarn Lubricant, Bleaching Agents, etc.)

- 5.2 By Raw Material

- 5.2.1 Natural Fibres

- 5.2.2 Synthetic Fibres

- 5.2.3 Bio-Based

- 5.2.4 Speciality Chemicals

- 5.3 By Application

- 5.3.1 Apparel

- 5.3.2 Home Furnishing

- 5.3.3 Automotive Textiles

- 5.3.4 Industrial Textiles

- 5.3.5 Other Applications (Medical and Hygiene Textiles, Sports Textiles, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Achitex Minerva SpA

- 6.4.2 Albemarle Corporation

- 6.4.3 Archroma

- 6.4.4 BASF

- 6.4.5 Bozzetto Group

- 6.4.6 CHT Group

- 6.4.7 Clariant AG

- 6.4.8 Covestro AG

- 6.4.9 Croda International PLC

- 6.4.10 Dow Inc.

- 6.4.11 DyStar Group

- 6.4.12 Evonik Industries AG

- 6.4.13 Huntsman International LLC

- 6.4.14 Kemira Oyj

- 6.4.15 Kiri Industries Ltd

- 6.4.16 K-Tech (India) Ltd

- 6.4.17 L. N. Chemical Industries

- 6.4.18 Nouryon

- 6.4.19 Rudolf GmbH

- 6.4.20 Sarex

- 6.4.21 Sumitomo Chemical Co. Ltd

- 6.4.22 Tanatex Chemicals BV

- 6.4.23 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment