|

시장보고서

상품코드

2044122

북미의 그린 데이터센터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

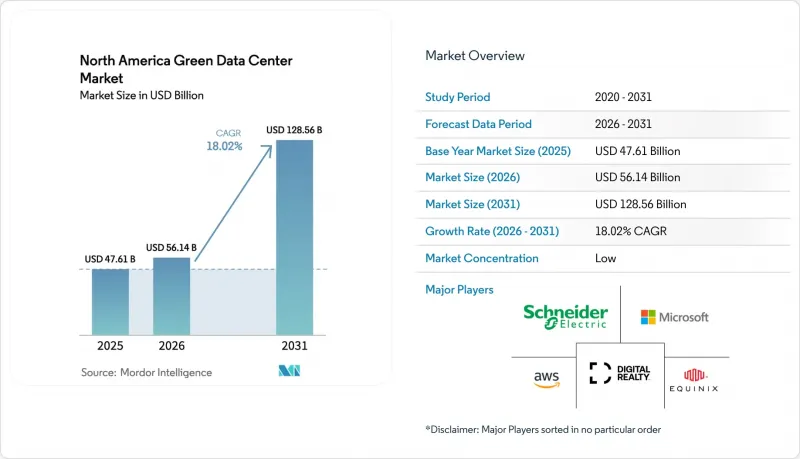

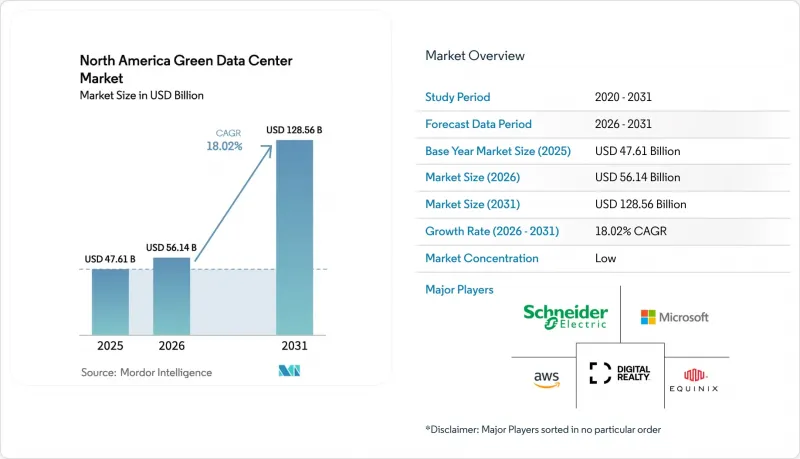

북미의 그린 데이터센터 시장 규모는 2025년 476억 1,000만 달러로 평가되었습니다. 2026년 561억 4,000만 달러에서 2031년까지 1,285억 6,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 18.02%를 나타낼 전망입니다.

열 관리 기술의 혁신, 재생 에너지 조달 전략, 그리고 인공지능을 통한 추론 워크로드 가속화로 입지 결정, 전력 아키텍처, 시설 설계가 새롭게 변화하고 있습니다. 액체 냉각으로의 개조로 인해 자본은 고밀도 홀로 이동하고 있으며, 실시간 탄소 강도 데이터는 네트워크 지연보다 더 많은 워크로드 배치에 영향을 미치고 있습니다. 2024년 이전에 장기 재생에너지 전력 구매 계약을 확보한 성숙한 사업자는 구조적인 전력 비용 우위를 누리고 있습니다. 그러나 미국의 주요 송전망 전체에 걸쳐 송전 용량이 부족하여 계통 연계 리스크가 증가함에 따라 모듈식 조립식 전기실과 현장 에너지 저장에 대한 의존도가 높아지고 있습니다.

북미의 그린 데이터센터 시장 동향 및 인사이트

북미 전역에 급증하는 하이퍼스케일 시설 건설 증가

AI 트레이닝용 랙은 기존 서버의 최대 15배에 달하는 전력을 소비하기 때문에 GPU 집약형 캠퍼스 규모는 50MW에서 200MW를 훌쩍 뛰어넘는 수준으로 확대되고 있습니다. Meta는 루이지애나 주에 300억 달러를 투자하고, 구글은 사우스캐롤라이나 주 확장 계획에 33억 달러를 확보하여 지역 전력망에 직접적인 압력을 가하고 있습니다. 현재 하이퍼스케일러 업체들은 경쟁입찰 방식의 PPA 경매에서 전력회사를 능가하는 가격으로 재생에너지 구매권을 획득하고 있어 소규모 사업자가 계약을 따낼 수 있는 기회가 제한되어 있습니다. 아마존의 펜실베니아와 노스캐롤라이나 주에 대한 300억 달러 투자 계획은 워크로드 수요가 기존 기업 IT 예산에서 분리되고 있는 현실을 여실히 보여주고 있습니다. 캠퍼스 설계에서는 송전 지연을 줄이기 위해 부지 내 변전소와 축전 설비를 통합하고 있으며, 건설 기간을 단축하는 조립식 전기실 도입이 가속화되고 있습니다.

기업의 순 제로 의무가 코로케이션 RFP를 재구성합니다.

기업의 구매 담당자는 연간 인증서를 통한 상쇄가 아닌 시간 단위로 탄소 없는 에너지와의 정합성을 규정하는 경우가 증가하고 있으며, 코로케이션 제공 업체는 조정 가능한 재생에너지와 배터리 저장을 결합해야 합니다. 마이크로소프트의 2024년 지속가능성 보고서에서는 연간 상쇄와 실시간 화석연료 의존도 사이에 차이가 있음을 인정하고, Scope 2 배출량에 대한 시장 전반의 투명성을 높이고 있습니다. 캘리포니아 주 상원 법안 100과 뉴욕 주 CLCPA는 시간별 보고를 법적 의무로 규정하고 있으며, 공급자가 탄소 강도 API와 빠른 응답 배터리를 통합함에 따라 개발 예산이 15-20% 증가했습니다.

지속 가능한 소재로 인한 초기 설비투자(Capex) 프리미엄

저탄소 콘크리트 및 재생강재 사용으로 인해 골조공사 예산이 8-12% 증가하여 배당금을 지급해야 하는 코로케이션 리츠의 개발수익률이 압박을 받게 됩니다. 에퀴닉스(Equinix)는 지속가능한 자재 사용으로 인해 일반적인 30MW 규모의 건설 프로젝트에 1,500만-2,000만 달러의 추가 비용이 발생하지만, 하이퍼스케일러 기업은 감가상각 기간 연장을 통해 이 추가 비용을 흡수할 수 있다고 밝혔습니다. 할 수 있습니다. ESG를 의식한 금융기관들은 현재 ISO 14064에 따라 매립 탄소량 공개를 요구하고 있으며, 이를 통해 프로젝트 파이낸싱 실사 시 설계상의 선택이 가시화되어 자재 공급망이 확립된 사업자에 대한 자금 조달을 촉진하고 있습니다.

부문 분석

서비스 부문은 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 19.32%를 나타낼 것으로 예측되며, 사업자들이 배출량 추적, 재생에너지 크레딧 조달, 계통 조정 소프트웨어를 아웃소싱함에 따라 북미 전체 그린 데이터센터 시장 성장률을 상회할 것으로 예측됩니다. 를 능가할 것으로 예측됩니다. 사업자들은 실시간 카본 API를 오케스트레이션 스택에 통합하여 전력망 부하가 급증할 때 워크로드 마이그레이션을 트리거할 수 있게 되었으며, 이 기능은 이전에는 하이퍼스케일러에 국한된 기능이었습니다. 전문 서비스에서는 에너지 감사, LEED 준수, PPA(전력구매계약) 구축이 패키지화되어 있으며, 설치 후 서비스에서는 배터리 재활용 및 디젤 발전기 교체가 제공됩니다. 솔루션 분야에서는 전력 인프라가 가장 큰 비중을 차지하고 있습니다. 이는 40-60kW 랙의 경우 480V 또는 600V 배전 및 변전소 업그레이드가 필요하며, 그 비용이 홀당 1,000만 달러가 넘기 때문입니다.

2025년에는 솔루션이 시장 점유율의 63.65%를 차지했으며, 기계식 설치 면적을 줄이는 액체 냉각 개조와 AI 최적화 전력 분배가 주도할 것으로 보입니다. 각 벤더들은 하드웨어와 지속적인 모니터링 계약을 세트로 판매하고 있습니다. Trane Technologies가 LiquidStack을 10억 달러에 인수한 것은 이러한 라이프사이클 수익 창출을 위한 움직임을 상징적으로 보여줍니다. Scope 2의 보고 요건이 강화되는 가운데, 시간 단위로 탄소 컴플라이언스를 보장하는 매니지드 서비스 제공업체는 추가 요금을 청구할 수 있으며, 두 자릿수 성장률을 유지하고 있습니다.

금융 기관과 정부 기관이 디젤 연료를 사용하지 않는 백업을 통해 완전 내결함성 설계를 추진함에 따라 Tier 4 도입은 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 19.77%로 확대될 것으로 예측됩니다. 듀얼 유틸리티 공급, 2N UPS 토폴로지, 모듈식 액체 냉각은 Tier 3에 비해 자본 집약도를 40-50% 증가시키지만, 규제 당국은 Tier 4 인증을 미션 크리티컬한 신뢰성과 동등한 것으로 간주하는 경향이 있습니다. 2025년에는 Tier 3 사이트가 52.86%의 점유율을 차지할 것으로 예상되며, 이는 기업들이 저렴한 비용으로 N+1 리던던던시를 채택하는 것에 대해 안심하고 있다는 것을 반영합니다.

기술 공급업체는 고효율 아키텍처로 이에 대응하고 있습니다. Vertiv의 모듈형 Liebert EXL S1 UPS는 이중 변환 모드에서 97%의 효율을 달성하여 공조 부하를 줄이고 추가 랙을 설치할 수 있는 바닥 공간을 확보할 수 있는 모듈식 Liebert EXL S1 UPS입니다. 또한, 운영사업자는 Tier 4 시설 건설과 LEED 플래티넘 인증을 결합하여 탄소배출량 감축을 어필하고, 임대료 상승을 뒷받침하는 다층적 차별화를 꾀하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe North America green data center market size is projected to expand from USD 47.61 billion in 2025 and USD 56.14 billion in 2026 to USD 128.56 billion by 2031, registering a CAGR of 18.02% between 2026 to 2031.

Thermal-management innovation, renewable-energy procurement strategies, and accelerating generative-AI inference workloads are reshaping siting decisions, power architectures, and facility designs. Liquid-cooling retrofits are shifting capital toward high-density halls, while real-time carbon-intensity data feeds influence workload placement more than network latency. Mature operators that secured long-term renewable power-purchase agreements before 2024 enjoy structural electricity-cost advantages. However, tightening transmission capacity across major U.S. grids is elevating interconnection risk and increasing dependence on modular prefabricated electrical rooms and on-site energy storage.

North America Green Data Center Market Trends and Insights

Soaring Hyperscale Build-Outs Across North America

GPU-dense campuses are scaling from 50 MW footprints to well above 200 MW because AI training racks consume up to fifteen times the power of traditional servers. Meta allocated USD 30 billion for a Louisiana complex and Google reserved USD 3.3 billion for South Carolina expansions, placing direct pressure on regional grids. Hyperscalers now outbid utilities for renewable offtake in competitive PPA auctions, limiting contract availability for smaller operators. Amazon's USD 30 billion investment pipeline across Pennsylvania and North Carolina illustrates how workload demand is decoupling from historic enterprise IT budgets. Campus designs integrate on-site substations and storage to mitigate transmission delays, accelerating adoption of prefabricated electrical rooms that compress build schedules.

Corporate Net-Zero Mandates Reshaping Colocation RFPs

Enterprise buyers increasingly stipulate hourly carbon-free energy alignment rather than annual certificate balancing, forcing colocation providers to pair battery storage with dispatchable renewables. Microsoft's 2024 sustainability filing acknowledged the gap between annual matching and real-time fossil fuel reliance, prompting marketwide transparency around Scope 2 emissions. California's Senate Bill 100 and New York's CLCPA create legal obligations for hourly reporting, raising development budgets by 15-20% as providers integrate carbon-intensity APIs and fast-response batteries.

Up-Front Capex Premium of Sustainable Materials

Low-carbon concrete and recycled steel raise shell construction budgets by 8-12% and compress development yields for colocation REITs that must honor dividend payouts. Equinix disclosed that sustainable materials added USD 15-20 million to a typical 30 MW build, a surcharge hyperscalers can absorb through longer depreciation schedules. ESG-minded lenders now request ISO 14064 embodied-carbon disclosures, making design choices visible during project finance diligence and tilting funding toward operators with proven materials supply chains.

Other drivers and restraints analyzed in the detailed report include:

- Utility-Level Renewable PPA Price Declines

- AI-Driven Airflow Optimization Cutting OpEx

- Regional Grid-Congestion and Interconnection Queue Backlog

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services segment is forecast to grow at a 19.32% CAGR from 2026-2031, outpacing broader North America green data center market growth as operators outsource emissions tracking, renewable certificate procurement, and grid-balancing software. Operators integrate real-time carbon APIs into orchestration stacks, triggering workload migration when grid intensity spikes, a capability previously limited to hyperscalers. Professional services now bundle energy audits, LEED compliance, and PPA structuring, while post-install offerings cover battery recycling and diesel-generator replacement. Within solutions, power infrastructure commands the largest share because 40-60 kW racks require 480 V or 600 V distribution and substation upgrades that exceed USD 10 million per hall.

Solutions retained 63.65% of the market share in 2025, led by liquid-cooling retrofits and AI-optimized power distribution that shrink mechanical footprints. Vendors are bundling hardware with recurring monitoring contracts; Trane Technologies' USD 1 billion purchase of LiquidStack exemplifies this move toward lifecycle revenue. As Scope 2 reporting tightens, managed-service providers that guarantee hourly carbon compliance can charge premium fees, sustaining double-digit growth rates.

Tier 4 deployments are projected to advance at a 19.77% CAGR between 2026-2031 as financial institutions and government agencies push for fully fault-tolerant designs with diesel-free backup. Dual utility feeds, 2N UPS topologies, and modular liquid cooling raise capital intensity by 40-50% relative to Tier 3, but regulators increasingly equate Tier 4 certification with mission-critical reliability. Tier 3 sites held 52.86% share in 2025, reflecting enterprise comfort with N+1 redundancy at lower cost.

Technology suppliers are responding with higher-efficiency architectures. Vertiv's modular Liebert EXL S1 UPS achieves 97% efficiency in double-conversion mode, cutting HVAC loads and freeing floor space for additional racks. Operators also pair Tier 4 builds with LEED Platinum certification to signal embodied-carbon reductions, creating multilayered differentiation that supports elevated lease rates.

The North America Green Data Center Market Report is Segmented by Component (Service, and Solution), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Schneider Electric SE

- Vertiv Holdings Co

- Eaton Corporation plc

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- Fujitsu Ltd

- IBM Corp.

- Hitachi Ltd

- Equinix Inc.

- Digital Realty Trust Inc.

- QTS Realty Trust LLC

- CyrusOne Inc.

- Switch Inc.

- Iron Mountain Data Centers

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Rittal GmbH and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring Hyperscale Build-Outs Across North America

- 4.2.2 Corporate Net-Zero Mandates Reshaping Colocation RFPs

- 4.2.3 Utility-Level Renewable PPA Price Declines

- 4.2.4 AI-Driven Airflow Optimization Cutting OpEx

- 4.2.5 Rise of Modular Liquid-Cooling Retrofits

- 4.2.6 Carbon-Credit Monetisation Pilots in Data Estates

- 4.3 Market Restraints

- 4.3.1 Up-Front Capex Premium of Sustainable Materials

- 4.3.2 Regional Grid-Congestion and Interconnection Queue Backlog

- 4.3.3 Limited Availability of Low-Carbon Concrete and Steel

- 4.3.4 Skilled-Labor Shortage for High-Density Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 By Service

- 5.1.1.1 System Integration

- 5.1.1.2 Monitoring Services

- 5.1.1.3 Professional Services

- 5.1.1.4 Other Services

- 5.1.2 By Solution

- 5.1.2.1 Power

- 5.1.2.2 Cooling

- 5.1.2.3 Servers

- 5.1.2.4 Networking Equipment

- 5.1.2.5 Management Software

- 5.1.2.6 Other Solutions

- 5.1.1 By Service

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Size

- 5.3.1 Small Data Center

- 5.3.2 Medium Data Center

- 5.3.3 Large Data Center

- 5.3.4 Hyperscale Data Center

- 5.4 By Data Center Type

- 5.4.1 Colocation Data Center

- 5.4.2 Hyperscalers Data Center/CSPs

- 5.4.3 Enterprise and Edge Data Center

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Vertiv Holdings Co

- 6.4.3 Eaton Corporation plc

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Hewlett Packard Enterprise

- 6.4.7 Fujitsu Ltd

- 6.4.8 IBM Corp.

- 6.4.9 Hitachi Ltd

- 6.4.10 Equinix Inc.

- 6.4.11 Digital Realty Trust Inc.

- 6.4.12 QTS Realty Trust LLC

- 6.4.13 CyrusOne Inc.

- 6.4.14 Switch Inc.

- 6.4.15 Iron Mountain Data Centers

- 6.4.16 Amazon Web Services

- 6.4.17 Microsoft Corporation

- 6.4.18 Google LLC

- 6.4.19 Meta Platforms Inc.

- 6.4.20 Rittal GmbH and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment