|

시장보고서

상품코드

2044130

스테아린산 칼슘 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Calcium Stearate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

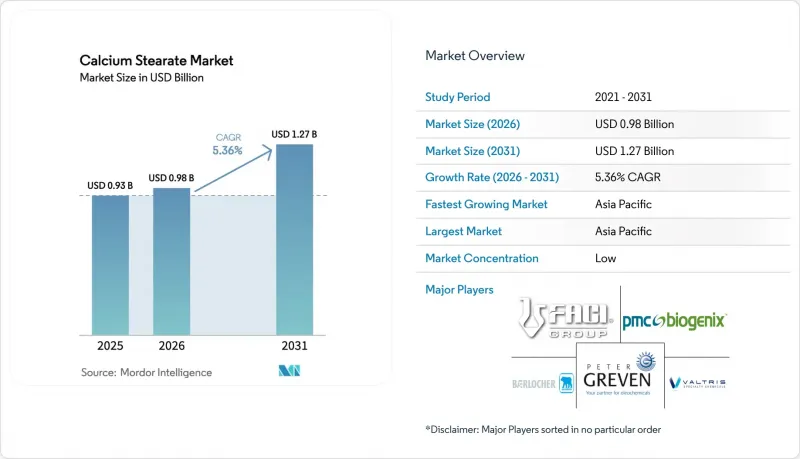

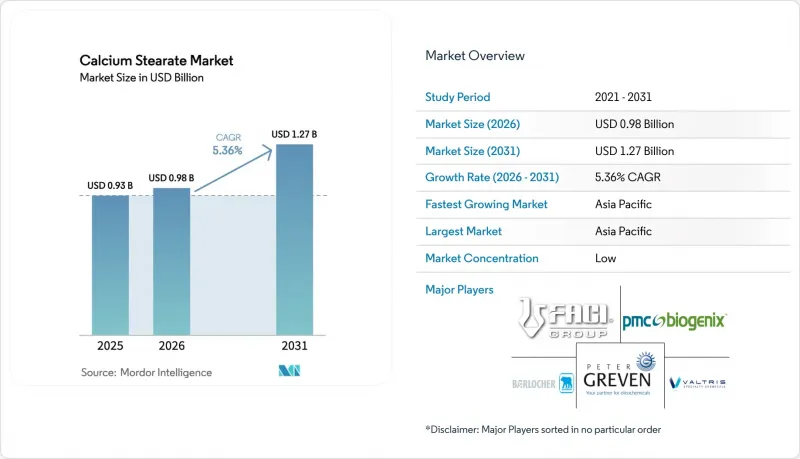

스테아린산 칼슘 시장 규모는 2025년에 9억 3,000만 달러로 평가되었고 2026년 9억 8,000만 달러에서 2031년까지 12억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.36%를 나타낼 전망입니다.

이러한 성장 궤적은 독성 금속 안정제에서 칼슘 시스템으로의 전환, 습한 지역의 내습성 콘크리트 첨가제에 대한 수요 증가, 브랜드 소유자의 지속가능성 노력에 부응하기 위한 식물성 오일 원료로의 점진적인 전환에 의해 뒷받침되고 있습니다. 규정(EU) 923/2023에 따라 공포되고 2024년 11월부터 시행되는 폴리염화비닐(PVC)의 납에 대한 규제 상한으로 인해 유럽에서 납 안정제의 경제적 근거가 사라져 급속한 배합 변경의 움직임이 일어났습니다. 이에 따라 PVC 압출 성형 시 열 안정제 및 윤활제 역할을 동시에 하는 스테아린산 칼슘에 대한 수요가 확대되고 있습니다. 이와 함께 아시아태평양의 인프라 프로젝트에서도 수요가 확대되고 있습니다. 특히 몬순의 영향을 받기 쉬운 연안 메가시티에서는 콘크리트 혼화제 배합업체들이 모세관 구멍을 막고 염화물의 침입을 막기 위해 시멘트 함량 대비 0.5-1.5%의 스테아린산 칼슘이 함유된 시멘트를 사용합니다. 북미에서는 지속가능성을 의식한 브랜드 소유주들이 현재 팜유가 아닌 식물성 원료를 지정하고 있으며, 삼림 벌채로 인한 위험으로부터 공급망을 보호하기 위해 구매자가 10-15%의 프리미엄 가격을 수용함으로써 가격의 견고함을 더하고 있습니다.

세계 스테아린산 칼슘 시장 동향 및 인사이트

건설용 화학물질 및 콘크리트 혼화제 확장

스테아린산 칼슘은 콘크리트에서 소수성 기공 봉쇄제로 작용합니다. 국내 실험실 실험에서 시멘트 중량 대비 1% 첨가 시 28일 양생 후 흡수율이 23%, 염화물 침투율이 31% 감소하는 것으로 입증되었으며, 자카르타에서 첸나이에 이르는 연안부 프로젝트에서 그 효과가 두드러지게 나타나고 있습니다. 아세안 각국 정부가 항만 확장 및 고가도로 건설에 경기부양책을 투입함에 따라 수요가 증가하고 있으며, 시멘트 제조업체와 혼화제 제조업체 간의 선순환이 이루어지고 있습니다. 이 첨가제의 초기 비용은 기존 감수제보다 높지만, 이중기능, 발수성, 윤활성으로 혼화제의 배합량을 줄일 수 있어 ASTM C494 재인증이 완료되면 장기적인 채용이 기대됩니다.

납계 안정제에서 칼슘계 안정제로의 전환

규정(EU) 923/2023의 PVC 납 함량 기준치인 0.1%로 인해 기존의 납계 안정제는 발색 유지 및 내열성에 필요한 첨가량으로 사용할 수 없게 되었습니다. 유럽의 컨버터는 재고 여유가 거의 없고, 즉시 새로운 배합의 인증을 받아야 하며, 스테아린산 칼슘을 핵심으로 하는 칼슘-아연계 시스템이 추진되고 있습니다. 주요 안정제 공급업체들이 이에 대응하고 있습니다. Baerlocher는 2023년 인도 데와스에 저탄소 공장을 가동할 예정이며, 영국 공장은 그 전에 생산 능력을 50% 이상 확대했습니다. 이러한 파급효과는 멕시코와 베트남에서도 두드러지게 나타나고 있으며, 전 세계 OEM(주문자상표부착생산자)들이 조달 감사를 효율화하기 위해 배합을 통일하면서 전 세계적으로 스테아린산 칼슘의 채택이 확대되고 있습니다.

스테아린산 원료 가격 변동

팜유 가격은 2024년 1월 톤당 7,481위안에서 12월에 1만 70위안으로 급등하여 2개월의 시차를 두고 스테아린산 가격에 직접적인 영향을 미쳤습니다. 스테아린산이 스테아린산 칼슘의 현금 비용의 약 68%를 차지한다는 점을 감안할 때, 현물 판매업자의 총이익률이 크게 압박을 받아 산동성 및 강소성의 소규모 독립 제조업체들 사이에서 일시적인 생산 중단이 잇따랐습니다. 헤지 도입 현황은 여전히 고르지 않고, 많은 생산자들이 장기 팜유 선물 거래에 필요한 신용 한도를 보유하지 않아 수익 변동성이 커지고 있습니다.

부문 분석

2025년 생산량의 약 48.22%는 여전히 분말로, 이는 전통적인 PVC 생산 라인의 인프라가 잘 정착되어 있음을 반영합니다. 그러나 독일과 일본의 무인 성형 셀에서는 ISO 45001 감사에 대응하기 위해 현재 펠릿이 지정되어 있습니다. 스테아린산 칼슘 시장이 자동 계량으로 전환함에 따라 예측 기간(2026-2031년) 동안 과립형 제품 시장 점유율은 CAGR 5.87%로 확대되어 분말형 제품을 추월할 것으로 예측됩니다. 플레이크 제품은 여전히 고무용 내부 믹서에서 사용되고 있지만, 틈새 시장에 머물러 있습니다. 수성 도료용 '플러그 앤 스프레이' 방식의 편리성으로 인해 수성 분산액은 약 25%의 가격 프리미엄을 유지하고 있습니다.

따라서 OEM 업체들이 먼지없는 표준을 추구함에 따라 스테아린산 칼슘 시장에서 펠렛 제품의 점유율이 높아질 것입니다. 초기 도입 기업들은 첨가제 폐기량을 15-20% 절감할 수 있었고, 이는 곧 스크랩율 감소로 이어진다는 것을 확인했습니다. 장비 공급업체들은 감압식 스크류가 장착된 40m3 스테인리스 스틸 사일로에 대한 주문이 활발하다고 보고하고 있으며, 이는 열가소성 수지의 가치사슬 전반에 걸쳐 그 상업적 가치를 인정받고 있다는 증거입니다.

지역별 분석

아시아태평양은 2025년 스테아린산 칼슘 시장의 44.57%를 차지하며 선두를 달리고 있으며, 예측 기간(2026-2031년) 동안 연평균 5.63%의 연평균 복합 성장률(CAGR)로 그 기세를 유지할 것으로 예측됩니다. 인도네시아의 팜유 플랜테이션과의 근접성은 스테아린산의 원료 확보가 가능하며, 인도의 국가 인프라 계획으로 인해 PVC 파이프에 대한 수요가 확대되고 있습니다. 일본 해안 지역의 건축법에서는 염화물의 침투를 제한하는 혼화제 사용을 의무화하고 있으며, 이 지역의 건설 총량이 적음에도 불구하고 고품질 스테아린산 칼슘 혼화제 사용을 장려하고 있습니다.

유럽에서 당장의 급격한 증가는 규정 923/2023에 따른 납 사용 금지와 관련이 있습니다. 향후 가교 폴리에틸렌에 대한 PVC 대체가 성장을 둔화시킬 수 있지만, 식품 접촉 용도와 제약 등급의 순도를 요구하는 틈새 시장이 가격 강세를 뒷받침하고 있습니다. 북미에서 대두 유래 파생 제품으로의 전환은 RSPO(지속가능한 팜유 원탁회의)의 페널티를 완화하고, 미국 소매업체들의 삼림 파괴 방지 서약과도 일치합니다.

라틴아메리카와 중동은 토목 건설 파이프라인과 신흥 제약 클러스터에 힘입어 각각 비슷한 수준의 CAGR로 성장하고 있습니다. 2013년부터 단계적으로 확장된 베어락커의 브라질 공장은 현재 인근 국가로 스테아린산 금속염를 수출하고 있으며, 단일 공장이 어떻게 지역 공급 체제를 형성할 수 있는지를 보여주고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Calcium Stearate Market size was valued at USD 0.93 billion in 2025 and is estimated to grow from USD 0.98 billion in 2026 to reach USD 1.27 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031).

This growth path is anchored in the transition from toxic-metal stabilizers toward calcium-based systems, stronger demand for moisture-resistant concrete additives in humid regions, and a gradual pivot to vegetable-oil feedstocks to meet brand-owner sustainability pledges. Regulatory ceilings on lead in polyvinyl chloride (PVC), published under Regulation (EU) 923/2023 and effective November 2024, dismantled the economic case for lead stabilizers in Europe, triggering rapid reformulation activity that amplifies demand for calcium stearate, which simultaneously behaves as a heat stabilizer and a lubricant during PVC extrusion. Parallel growth stems from Asia-Pacific infrastructure projects where concrete admixture formulators rely on calcium stearate at 0.5-1.5% cement loading to block capillary pores and fight chloride intrusion, especially in coastal megacities vulnerable to monsoon cycles. In North America, sustainability-conscious brand owners now specify non-palm vegetable derivatives, adding price resilience as buyers accept 10-15% premiums to de-risk supply chains from deforestation exposure.

Global Calcium Stearate Market Trends and Insights

Expansion of Construction Chemicals and Concrete Additives

Calcium stearate acts as a hydrophobic pore blocker in concrete. Laboratory trials in South Korea demonstrated that 1 % dosage by cement weight lowered water absorption by 23 % and chloride penetration by 31% after 28 days of curing, benefits that resonate in coastal projects from Jakarta to Chennai. Demand intensifies as ASEAN governments channel stimulus into port expansions and elevated highways, creating a virtuous loop between cement manufacturers and admixture blenders. Although the additive's upfront cost is higher than conventional water-reducers, dual functionality, water repellency, and lubricity shrink total admixture recipes, supporting long-term adoption once ASTM C494 requalification is complete.

Switch from Lead-Based to Calcium-Based Stabilizers

The 0.1 % lead threshold in PVC under Regulation (EU) 923/2023 renders historical lead stabilizers unusable at the loadings necessary for color retention and heat stability. European converters have little buffer inventory and must certify new formulations immediately, propelling calcium-zinc systems with calcium stearate at their core. Major stabilizer vendors have responded: Baerlocher commissioned a low-carbon plant in Dewas, India, during 2023, while its United Kingdom site lifted capacity by over 50% earlier. Spill-over is evident in Mexico and Vietnam, where global OEMs (Original Equipment Manufacturers) unify recipes to streamline procurement audits, raising global calcium stearate uptake.

Volatile Stearic-Acid Feedstock Pricing

Palm oil rallied from CNY 7,481 per ton in January 2024 to CNY 10,070 per ton by December, feeding directly into stearic-acid prices with a two-month lag. Given that stearic acid forms about 68% of calcium stearate's cash cost, gross margins for spot sellers compressed markedly, prompting short production stoppages among small independents in Shandong and Jiangsu. Hedging adoption remains uneven, and many producers lack the credit lines required for long-dated palm-oil futures, heightening earnings volatility.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Dust-Free Pelletized Additives

- Growth in Solvent-Free Dispersions for Water-Borne Coatings

- Tightening Trace-Metal Limits in Pharma Excipients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Roughly 48.22% of the 2025 volume remained powder, reflecting entrenched infrastructure in legacy PVC lines. Yet lights-out molding cells in Germany and Japan now specify pellets to meet ISO 45001 audits. Granular product forms are expected to capture a 5.87% CAGR during the forecast period (2026-2031), overtaking powders, as the calcium stearate market transitions to automated dosing. Flakes persist in rubber internal-mixers but remain niche. Water-dispersions command roughly 25% price premiums thanks to their plug-and-spray convenience for water-borne coatings.

The calcium stearate market share of pelletized forms will therefore climb as OEMs chase dust-free benchmarks. Early adopters confirm 15-20% savings in additive waste, converting directly into lower scrap rates. Equipment suppliers report brisk orders for 40-m3 stainless silos fitted with loss-in-weight screws, evidence that the commercial case is accepted across thermoplastic value chains.

The Calcium Stearate Market Report is Segmented by Product Form (Powder, Granules, Flakes, and Dispersion/Emulsion), End-User Industry (Plastics and Rubber, Construction, Personal Care and Pharmaceutical, Paper, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated the Calcium Stearate market in 2025 at 44.57% and should keep momentum with a 5.63% CAGR during the forecast period (2026-2031). Proximity to Indonesian palm plantations secures stearic feedstock, while India's National Infrastructure Pipeline advances PVC pipe intakes. Japanese coastal codes mandate admixtures that limit chloride ingress, prompting high-grade calcium stearate admixture usage despite the region's modest overall construction volume.

Europe's immediate spike is linked to Regulation 923/2023 lead bans. Over the horizon, PVC substitution by cross-linked polyethylene could temper growth, though food-contact and pharma purity niches reinforce price resilience. North America's tilt toward soybean-based derivatives alleviates RSPO (Roundtable on Sustainable Palm Oil) penalties and aligns with the United States retailer deforestation pledges.

Latin America and the Middle East each advance at a similar CAGR, paced by civil-works pipelines and nascent pharma clusters. Baerlocher's Brazil site, expanded in phases since 2013, now exports metal stearates to neighboring countries, showing how a single hub can shape regional supply.

- Akrochem Corporation

- Baerlocher GmbH

- Corporacion Sierra Madre

- Dover Chemical Corporation

- FACI Corporate S.p.A.

- GOVI NV

- Hummel Croton Inc.

- Kemipex

- Peter Greven GmbH & Co. KG

- PMC Biogenix, Inc.

- Sinwon Chemical Co., Ltd.

- Univar Solutions LLC

- Valtris Specialty Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of construction chemicals and concrete additives

- 4.2.2 Switch from lead-based to Ca-based stabilizers

- 4.2.3 OEM push for dust-free pelletised additives to improve shopfloor health and automation

- 4.2.4 Growth in solvent-free dispersions for water-borne coatings

- 4.2.5 Food-contact packaging shift to vegetable-oil-derived calcium stearate grades

- 4.3 Market Restraints

- 4.3.1 Volatile stearic-acid feed-stock pricing

- 4.3.2 Tightening trace-metal limits in high-potency pharma excipients

- 4.3.3 ESG-linked loans penalising palm-oil based supply chains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Form

- 5.1.1 Powder

- 5.1.2 Granules

- 5.1.3 Flakes

- 5.1.4 Dispersion / Emulsion

- 5.2 By End-user Industry

- 5.2.1 Plastics and Rubber

- 5.2.2 Construction

- 5.2.3 Personal Care and Pharmaceutical

- 5.2.4 Paper

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Akrochem Corporation

- 6.4.2 Baerlocher GmbH

- 6.4.3 Corporacion Sierra Madre

- 6.4.4 Dover Chemical Corporation

- 6.4.5 FACI Corporate S.p.A.

- 6.4.6 GOVI NV

- 6.4.7 Hummel Croton Inc.

- 6.4.8 Kemipex

- 6.4.9 Peter Greven GmbH & Co. KG

- 6.4.10 PMC Biogenix, Inc.

- 6.4.11 Sinwon Chemical Co., Ltd.

- 6.4.12 Univar Solutions LLC

- 6.4.13 Valtris Specialty Chemicals

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment