|

시장보고서

상품코드

2044140

자동차용 연료 탱크 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Automotive Fuel Tank - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

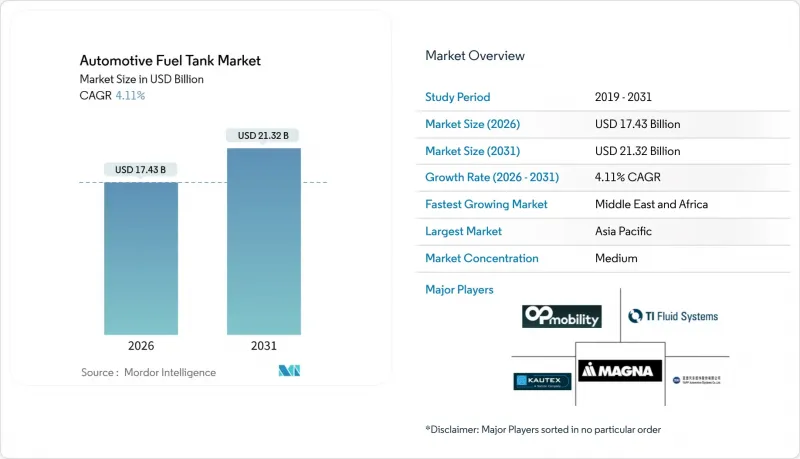

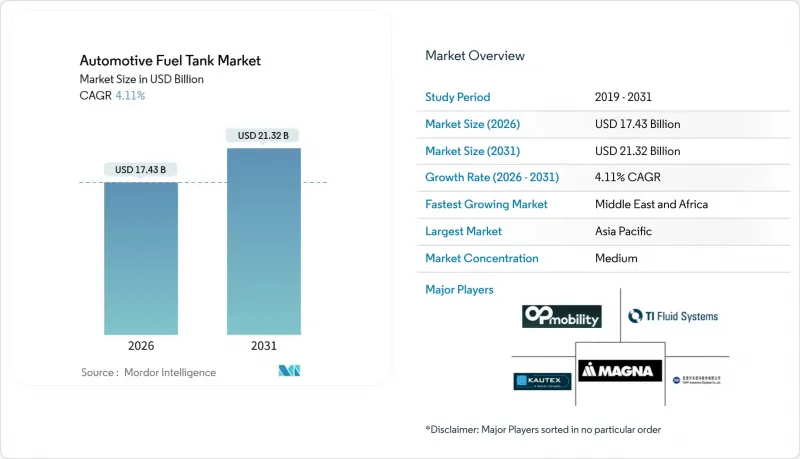

자동차용 연료 탱크 시장 규모는 2026년에 174억 3,000만 달러로 평가되고 있어 2031년까지 213억 2,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 사이에는 CAGR 4.11%를 나타낼 것으로 예측됩니다.

중국과 유럽에서 배터리 전기차의 보급이 확대되는 가운데, 아시아태평양, 남미, 중동의 내연기관차와 하이브리드 자동차의 안정적인 생산이 세계 수요를 지속적으로 뒷받침하고 있습니다. Tier 1 공급업체들은 규제 압력과 재료 혁신의 균형을 맞추면서 강철에서 다층 HDPE 시스템으로 전환하고, 수소 트럭용 복합재 유형 IV 실린더에 투자하고 있습니다. 유로 7과 LEV III의 증발성 배출가스 규제 강화로 인해 대당 15-25달러의 비용 증가가 발생하지만, 그 몇 배에 해당하는 컴플라이언스 크레딧을 얻을 수 있어 배리어 레이어 기술의 급속한 보급을 촉진하고 있습니다. 동시에 원자재 가격의 변동으로 인해 수익률이 압박을 받고 있으며, 공급업체들은 저비용 성형기지로의 전환과 수직계열화를 추진하고 있습니다.

세계 자동차용 연료탱크 시장 동향과 인사이트

경량 플라스틱 탱크가 CO2 규제 대응을 촉진

OEM 업체들은 스틸 탱크에서 30-40% 가벼운 다층 HDPE 탱크로 전환하고 있으며, 이를 통해 승용차 1대당 3-5kg의 경량화와 복합연비 효율 1% 향상을 실현하고 있습니다. 공압출 성형된 EVOH 배리어 층은 현재 HDPE 기판에 직접 통합되어 사이클 시간을 12-15% 단축하고, 유럽과 북미에서는 표준 요구사항이 되고 있습니다. 2025년에는 차량 전체 CO2 배출량에 대한 벌금이 Kg당 95 유로에 달할 것으로 예상에 따라, 장벽층이 있는 탱크는 비용 효율적인 규제 준수 수단으로 자리매김하고 있습니다. 사내에 배리어층 제조 능력을 갖추지 못한 공급업체는 OEM의 조달 패널에서 배제되는 경우가 많아지고 있으며, 최종 조립 공장 근처에 압출라인을 설치하는 것이 전략적으로 필요성이 부각되고 있습니다. 이러한 요인으로 인해 규제 대상 지역의 자동차용 연료탱크 시장 수요는 지속적으로 유지되고 있습니다.

내연기관(ICE) 및 하이브리드 자동차 생산 회복이 수요를 견인

2025년에는 BEV 증가에도 불구하고 세계 내연기관 및 하이브리드 자동차 생산이 회복되어 2020년 이전 수준에서 안정화될 것입니다. 충전 인프라가 미비한 시장, 특히 동남아시아 및 라틴아메리카에서는 하이브리드 차량이 주류를 이루고 있으며, 35-50리터 배리어 탱크에 대한 수요를 뒷받침하고 있습니다. 아시아태평양에 제조거점을 둔 공급업체는 이러한 다양한 수요의 혜택을 누리는 반면, 서유럽공급업체는 더 급격한 감소에 직면하고 있습니다. 하이브리드 자동차의 생산 호조는 자동차용 연료 탱크 시장의 중기적 성장을 뒷받침하고 있습니다.

전동화가 기존 연료 탱크 수요를 잠식할 것입니다.

2024년 1월부터 11월까지 전 세계 전기차 판매량은 1,850만 대에 달하고, 전년 동기 대비 21% 성장했습니다. 2025년 중국 내 BEV의 점유율 확대는 초기에는 수익성이 높은 세단 및 승용차 부문을 압박할 것이며, 공급업체들은 수익성이 낮은 상용차 및 오프로드 차량 수요에 의존할 수밖에 없을 것으로 보입니다. 제로에미션 규제의 가속화는 자동차용 연료 탱크 시장의 판매량 감소로 이어질 수 있으며, Tier 1 공급업체들은 배터리 열관리 시스템이나 수소 저장 시스템 등으로 다각화할 수밖에 없을 것으로 보입니다.

부문 분석

2025년 기준, 중용량(45-70리터) 연료 탱크는 전 세계 세단 및 크로스오버 차량에 채택되어 자동차용 연료 탱크 시장 점유율의 44.72%를 차지했습니다. 하이브리드 차량이 배터리 팩 탑재 공간을 확보하기 위해 소형화된 유닛을 채택함에 따라 성장이 둔화되고 있지만, 이 부문은 여전히 자동차용 연료 탱크 시장의 근간을 이루고 있습니다. 중국과 서유럽에서는 BEV가 소형차 부문을 지배하고 있기 때문에 45리터 이하의 배기량 차량에 대한 수요가 줄어들고 있습니다.

70리터 이상 카테고리는 북미 및 걸프 지역의 픽업트럭, 풀사이즈 SUV, 장거리 상용차에 힘입어 2031년까지 연평균 11.68%의 성장률을 보이며 자동차용 연료 탱크 시장 규모의 20-25%를 차지했습니다. 포드 F 시리즈와 도요타 랜드크루저의 연료 탱크 용량은 90-136리터로 항속거리 연장에 대한 기대를 뒷받침하고 있습니다. 오프로드 및 방산용 보조 금속 탱크는 30-40%의 가격 프리미엄을 수반하며 틈새 수요를 창출하고 있습니다. 지역별 연료 가격의 격차로 인해 유럽과 일본에서는 여전히 소용량을 선호하기 때문에 공급업체에게는 병렬 금형 요구 사항이 유지되고 있습니다.

2025년 기준, 플라스틱 탱크는 자동차용 연료 탱크 시장 점유율의 43.15%를 차지하고 있으며, 규제가 없는 시장을 위한 비용 효율적인 단층 HDPE와 유로 7 및 LEV III 지역을 위한 다층 배리어 유형으로 나뉩니다. 수소 및 CNG용 복합재 유형 IV 실린더는 틈새 시장이지만, 연평균 10.67%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 상업용 트럭의 자동차용 연료 탱크 시장 점유율의 고부가가치 성장을 뒷받침하고 있습니다. 알루미늄은 충돌 에너지 흡수 성능의 장점으로 고급차 및 소형 밴에서 15-20%의 점유율을 유지하고 있지만, OEM 업체들이 경량화를 추구함에 따라 이 점유율은 줄어들고 있습니다. 반면, 강재는 부식 및 중량 증가 문제로 인해 점유율이 한 자릿수대로 계속 후퇴하고 있습니다.

현재 진행 중인 인프라 구축으로 2025년까지 유럽에 150개의 수소충전소가 신설되고, 국경을 넘나드는 운송 회랑이 실현되어 복합재에 대한 수요가 더욱 증가할 것으로 예측됩니다. 공급업체들은 경화 시간을 절반으로 줄이고 비용을 최대 30%까지 절감할 수 있는 열가소성 수지 라이너를 개발하여 자동차용 연료 탱크 산업에 더 많이 적용될 수 있는 기반을 마련하고 있습니다.

지역별 분석

2025년 아시아태평양은 자동차용 연료 탱크 시장 점유율의 53.88%를 차지했습니다. 중국의 E10 의무화는 부분적이지만, 약 20억 달러 규모의 개조 수요를 창출할 수 있는 기회를 제공합니다. 일본에서는 하이브리드 자동차의 보급으로 40-55리터 탱크에 대한 안정적인 수요가 유지되고 있습니다. 한편, 한국은 2026년까지 Type IV 탱크 수출을 연간 5만대로 확대할 것으로 예측됩니다. 동남아시아에서는 이륜차 및 삼륜차용 연료 탱크 판매에 따라 수요가 급증하면서 자동차용 연료 탱크 시장을 주도하고 있습니다.

중동 및 아프리카는 가장 빠르게 성장하는 지역으로 2031년 CAGR이 10.47%를 나타낼 것입니다. 사우디는 '비전 2030'에서 밝힌 바와 같이 2030년까지 자동차 생산능력을 30만 대까지 끌어올리는 것을 목표로 하고 있으며, 이집트는 북아프리카 수출을 위한 조립능력을 확대되고 있습니다. 아랍에미레이트가 2027년까지 10개의 수소충전소를 설치하려는 계획은 복합재 탱크의 초기 시장을 창출하고 있습니다. 남아공의 유로 6d 수출 요건은 플라스틱 장벽의 채택을 촉진하고 있으며, 케냐와 나이지리아의 신흥 공장은 플라스틱 탱크의 현지 생산을 촉진하여 물류 비용을 절감하고 있습니다.

2025년에는 북미와 유럽을 합친 시장이 매출의 큰 비중을 차지했습니다. 유럽은 양극화되어 있습니다. 서유럽 시장에서는 BEV(배터리 전기자동차)의 점유율 확대에 따라 연료 탱크 수요가 연간 8-10% 감소하고 있는 반면, 중동부 유럽 공장에서는 수출용 내연기관(ICE) 차량 생산을 유지하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The automotive fuel tank market size is valued at USD 17.43 billion in 2026 and is projected to reach USD 21.32 billion by 2031, growing at a 4.11% CAGR from 2026 to 2031.

The steady output of internal-combustion and hybrid vehicles in the Asia-Pacific, South America, and the Middle East continues to anchor global demand, even as battery-electric penetration rises in China and Europe. Tier-1 suppliers are transitioning from steel to multi-layer HDPE systems and investing in composite Type IV cylinders for hydrogen trucks, striking a balance between regulatory pressure and material innovation. Tightening Euro 7 and LEV III evaporative-emission limits add USD 15-25 per unit but unlock compliance credits worth multiples of that cost, spurring rapid adoption of barrier-layer technologies. At the same time, raw material volatility has compressed margins, prompting suppliers to shift toward low-cost molding hubs and vertical integration.

Global Automotive Fuel Tank Market Trends and Insights

Lightweight Plastic Tanks Drive CO2 Compliance

OEMs are transitioning from steel to multi-layer HDPE tanks, which weigh 30-40% less, resulting in a 3-5 kg reduction per passenger car and a 1% improvement in combined-cycle efficiency. Co-extruded EVOH barriers are now integrated directly into HDPE substrates, cutting cycle time by 12-15% and becoming a baseline requirement in Europe and North America. Fleet-wide CO2 penalties reached EUR 95 per gram per kilometer in 2025, making barrier-equipped tanks a cost-effective compliance lever. Suppliers lacking in-house barrier capability are increasingly being excluded from OEM sourcing panels, underscoring the strategic need to co-locate extrusion lines near final assembly plants. This driver supports sustained demand in the automotive fuel tank market across regulated regions.

ICE and Hybrid Production Recovery Fuels Demand

Global ICE and hybrid production rebounded in 2025, stabilizing near pre-2020 levels despite gains in BEVs. Hybrid vehicles dominate markets with sparse charging infrastructure, notably Southeast Asia and Latin America, sustaining demand for 35-50 liter barrier tanks. Suppliers with Asia-Pacific manufacturing hubs benefit from this diversified volume, whereas those in Western Europe face sharper declines. The resiliency of hybrid output underpins medium-term growth for the automotive fuel tank market.

Electrification Erodes Traditional Fuel Tank Demand

During the period from January to November 2024, global EV sales amounted to 18.5 million units, reflecting a 21% growth compared to the corresponding period in the previous year. China's BEV share in 2025 will initially squeeze the high-margin sedan and city-car segments, leaving suppliers reliant on lower-margin commercial and off-road demand. Accelerating zero-emission mandates threatens a direct volume drain in the automotive fuel tank market, obliging tier-1s to diversify into battery-thermal or hydrogen-storage systems.

Other drivers and restraints analyzed in the detailed report include:

- Euro 7 Regulations Tighten Evaporative Standards

- Flex-Fuel Infrastructure Drives Barrier-Tank Adoption

- Raw Material Cost Volatility Pressures Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-capacity 45 to 70-liter tanks account for 44.72% of the automotive fuel tank market share in 2025, serving global sedans and crossovers. Growth is slowing as hybrids adopt downsized units to make room for battery packs, yet the segment remains the backbone of the automotive fuel tank market. The demand for vehicles with a displacement below 45 liters is shrinking in China and Western Europe, where BEVs are dominating the micro-car segment.

The above-70-liter category is expanding at an 11.68% CAGR through 2031, fueled by pickup trucks, full-size SUVs, and long-haul commercial vehicles in North America and the Gulf states, while holding a 20-25% share of the automotive fuel tank market size. Tanks in Ford F-Series or Toyota Land Cruiser models range from 90 to 136 liters, supporting extended range expectations. Auxiliary metal tanks for off-road and defense add niche volume at 30-40% price premiums. Regional fuel-price disparities continue to favor smaller capacities in Europe and Japan, thereby sustaining parallel tooling requirements for suppliers.

Plastic tanks captured 43.15% of the automotive fuel tank market share in 2025, split between cost-efficient single-layer HDPE for unregulated markets and multi-layer barrier variants for Euro 7 and LEV III regions. Composite Type IV cylinders for hydrogen and CNG, although niche, are climbing at a 10.67% CAGR and underpin premium growth for the automotive fuel tank market share in commercial trucks. Aluminum maintains a 15-20% foothold in luxury cars and light vans due to its crash-energy benefits, but this share erodes as OEMs pursue mass reduction. Steel continues its retreat to a single-digit share due to corrosion and weight penalties.

Ongoing infrastructure build-out added 150 European hydrogen stations in 2025, enabling cross-border corridors and reinforcing composite demand. Suppliers are developing thermoplastic liners that could halve cure times and lower cost by up to 30%, setting the stage for deeper penetration in the automotive fuel tank industry.

The Automotive Fuel Tank Market Report is Segmented by Capacity (Less Than 45 Liter, 45 To 70 Liter, Above 70 Liter), Material Type (Aluminum, Steel, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles and More), Fuel Type (Gasoline, Diesel, and More), and Geography (North America, South America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 53.88% of the automotive fuel tank market share in 2025. China's E10 mandate, although partial, presents a retrofit opportunity worth nearly USD 2 billion. In Japan, a consistent demand for 40-55 liter tanks is upheld by the country's hybrid mix. Meanwhile, South Korea is on track to boost its Type IV exports to 50,000 units annually by 2026. Southeast Asia experiences a surge in demand, with motorcycle and three-wheeler tank sales, thereby bolstering the automotive fuel tank market.

The Middle East and Africa are the fastest-growing regions, with a 10.47% CAGR through 2031. Saudi Arabia aims to reach a vehicle production capacity of 300,000 by 2030, as outlined in Vision 2030, and Egypt is expanding its assembly capabilities for exports to the North African region. The UAE's plan to establish 10 hydrogen stations by 2027 creates an early market for composite tanks. South Africa's Euro 6d export requirements are driving the adoption of plastic barriers, while nascent plants in Kenya and Nigeria are localizing plastic tanks, thereby trimming logistics costs.

North America and Europe combined accounted for a significant share of the revenue in 2025. Europe is bifurcated: Western markets see fuel tank demand decline by 8-10% annually as the BEV share accelerates, whereas Central and Eastern European plants sustain ICE output for export.

- Magna International Inc.

- OPMOBILITY SE

- TI Fluid Systems plc

- Kautex Textron GmbH & Co. KG

- YAPP Automotive Systems Co. Ltd.

- Fuel Total Systems Co. Ltd

- Sakamoto Industry Co. Ltd

- Yachiyo Industry Co. Ltd

- SRD Holdings Ltd

- Donghee Industrial Co. Ltd

- Continental AG

- Forvia (Faurecia Hydrogen Solutions)

- Hexagon Composites ASA

- Lumax Industries Ltd

- Cangzhou Mingzhu Plastic Co. Ltd

- Unipres Corporation

- SKH Metals Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweight Plastic Tanks Drive CO2 Compliance

- 4.2.2 ICE and Hybrid Production Recovery Fuels Demand

- 4.2.3 Euro 7 Regulations Tighten Evaporative Standards

- 4.2.4 Flex-Fuel Infrastructure Drives Barrier-Tank Adoption

- 4.2.5 High-Pressure Composite Tanks For Emerging Hydrogen ICE Trucks

- 4.2.6 Off-Road and Defense Demand For Long-Range Auxiliary Metal Tanks

- 4.3 Market Restraints

- 4.3.1 Electrification Erodes Traditional Fuel Tank Demand

- 4.3.2 Raw Material Cost Volatility Pressures Margins

- 4.3.3 Fire-Safety Concerns With High-Ethanol Blends in HDPE Tanks

- 4.3.4 Tank-Less Skateboard BEV Platforms Eroding OEM CAPEX

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Capacity

- 5.1.1 Less than 45 Liter

- 5.1.2 45 to 70 Liter

- 5.1.3 Above 70 Liter

- 5.2 By Material Type

- 5.2.1 Plastic - single-layer

- 5.2.2 Plastic - multi-layer/barrier

- 5.2.3 Aluminium

- 5.2.4 Steel

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Buses and Coaches

- 5.4 By Fuel Type

- 5.4.1 Gasoline

- 5.4.2 Diesel

- 5.4.3 Flex-fuel/Ethanol blends

- 5.4.4 Hydrogen

- 5.4.5 CNG and LPG

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Magna International Inc.

- 6.4.2 OPMOBILITY SE

- 6.4.3 TI Fluid Systems plc

- 6.4.4 Kautex Textron GmbH & Co. KG

- 6.4.5 YAPP Automotive Systems Co. Ltd.

- 6.4.6 Fuel Total Systems Co. Ltd

- 6.4.7 Sakamoto Industry Co. Ltd

- 6.4.8 Yachiyo Industry Co. Ltd

- 6.4.9 SRD Holdings Ltd

- 6.4.10 Donghee Industrial Co. Ltd

- 6.4.11 Continental AG

- 6.4.12 Forvia (Faurecia Hydrogen Solutions)

- 6.4.13 Hexagon Composites ASA

- 6.4.14 Lumax Industries Ltd

- 6.4.15 Cangzhou Mingzhu Plastic Co. Ltd

- 6.4.16 Unipres Corporation

- 6.4.17 SKH Metals Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment