|

시장보고서

상품코드

2044144

자동차 프론트엔드 모듈 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Front End Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

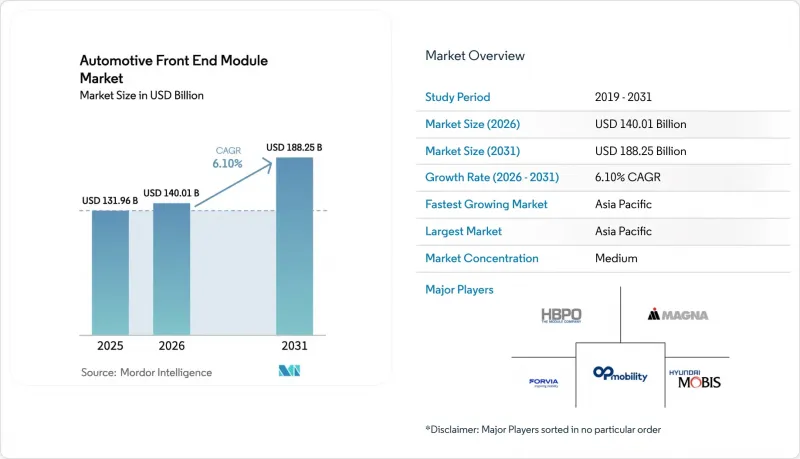

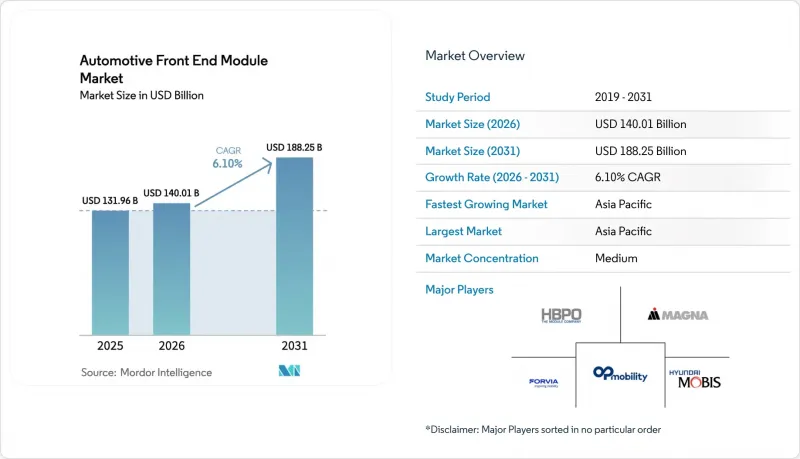

자동차 프론트엔드 모듈 시장 규모는 2025년 1,319억 6,000만 달러로 평가되었습니다. 2026년 1,400억 1,000만 달러로 확대되어 2031년까지 1,882억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR 6.10%를 나타낼 전망입니다.

완전한 볼트온 캐리어를 제공하는 1차 통합업체에 최종 조립을 아웃소싱함으로써 공장 노동력을 20-30% 절감하고, OEM의 턴키 시스템에 대한 수요가 증가하고 있습니다. 배터리 전기차(BEV)의 열 루프에 최적화된 폐쇄형 그릴 구조는 프리미엄 EV에서 양산형 부문으로 확대되고 있으며, 레이더, LiDAR, 카메라 센서용 정밀 마운팅으로 모듈은 단순한 범용 브래킷에서 소프트웨어 정의의 소프트웨어 정의 센싱 허브로 변모하고 있습니다. Euro NCAP 및 IIHS의 충돌 테스트가 강화됨에 따라 에너지를 흡수하면서도 CO2 규제를 충족할 수 있을 만큼의 경량성을 유지하는 고강도 스틸-알루미늄 하이브리드 소재에 대한 수요가 회복되고 있습니다. 북미의 니어쇼어링과 관세의 영향을 받기 쉬운 EU-영국 간 루트에서 OEM 업체들이 USMCA(미국-멕시코-캐나다 협정)에 따라 정해진 지역 부가가치 기준을 충족하는 모듈을 요구하면서 공급업체들의 거점 배치가 재편되고 있습니다.

세계의 자동차 프론트엔드 모듈 시장 동향 및 인사이트

EV 열 관리에서 통합형 밀폐형 그릴형 FEM의 필요성

배터리 전기자동차에서는 개방형 라디에이터 그릴이 범퍼 빔 뒤에 숨겨진 냉각기와 커패시터로 공기를 유도하는 밀폐형 페시아로 대체되고 있으며, 열교환기, 냉각수 매니폴드, 덕트를 하나의 구조물에 패키징한 캐리어가 요구되고 있습니다. 테슬라는 2025년형 '모델3'의 리프레시 버전에서 공기 저항을 크게 줄였습니다. 한편, BYD의 '블레이드 배터리' 플랫폼은 인룬(Yinlun)사의 수냉식 캐리어를 채택하여 ±2℃의 온도대를 유지하여 배터리 수명을 연장하고 있습니다. 아시아태평양과 미국의 선벨트 지역과 같은 고온 기후에서 열 관리의 통합은 항속거리 인증의 결정적인 요건이 되고 있습니다. 리비안은 배터리와 구동장치의 냉각을 통합하는 듀얼 루프 캐리어에 대해 발레오와 5년 계약을 체결했습니다. 이는 현재 필요한 깊은 공동 개발의 협력이 얼마나 필요한지 여실히 보여주고 있습니다. 장기적으로 2030년대 초에 BEV의 점유율이 전 세계 판매량의 50%를 넘어설 경우, EV 전용 모듈이 자동차 프론트엔드 모듈 시장 매출의 50%를 차지하게 될 것입니다.

경량화 및 강화되는 CO2 및 연비 규제

세계 배출가스 규제로 인해 자동차 제조업체들은 기존 스틸 캐리어의 경량화를 요구받고 있으며, 알루미늄 압출재, 탄소섬유 강화 열가소성 수지, 마그네슘 다이캐스팅 등의 소재 채택이 가속화되고 있습니다. 이러한 소재는 2030년까지 EU가 설정한 차량 평균 배출가스 목표를 달성하기 위해 필수적인 요소입니다. 중국에서는 규제 프레임워크에 따라 OEM 업체들은 충돌 시 에너지 흡수 성능을 유지하면서 대폭적인 경량화를 실현하는 하이브리드 프레임 모듈을 채택할 수밖에 없는 상황입니다. 미국에서는 2024년 최종 결정된 개정된 CAFE 규정에 따라 포드, GM 등 자동차 제조업체들이 멀티 머티리얼 캐리어로의 전환을 추진하고 있습니다. 이 캐리어는 크래시 레일, 쿨링 팩, 센서 플레이트 등 주요 구성 요소를 경량 설계에 통합한 캐리어입니다. ISO 14040에 기반한 라이프사이클 보고가 확산되면서 재생 알루미늄과 바이오 수지에 대한 수요가 증가하고 있으며, 공급업체들은 저탄소 소재 인증을 획득하고 ESG 크레딧과 연계된 새로운 수익 기회를 창출할 수 있게 되었습니다. 이러한 규제 동향으로 인해 2026년 이후 모든 차량 프로그램에 경량화가 포함될 것이며, 자동차 프론트엔드 모듈 시장공급업체들에게 경량화는 가장 중요한 가치 창출의 원동력으로 자리매김하고 있습니다.

철강, 폴리머, 에너지 가격의 변동으로 BOM 비용 증가

2025년, EU의 에너지 할증료로 인해 전기 아크로의 제반 비용이 상승함에 따라 열연 코일 가격은 전년 대비 상승했습니다. 같은 해, 멕시코만 연안의 불가항력적인 요인으로 인해 폴리프로필렌 가격이 크게 상승하여 1급 공급업체들의 총이익률에 악영향을 미쳤습니다. 유럽의 가스 가격 상승으로 인해 성형 에너지 비용이 크게 증가하여 하이브리드 프레임의 생산 비용을 증가시켰습니다. 섹션 232 관세로 인해 알루미늄 압출재 프리미엄 가격이 상승하여 현물 구매에 따른 리스크가 증가했습니다. 연간 고정 가격 계약을 맺은 공급업체는 수익성 문제에 직면했고, 잦은 재협상으로 인해 OEM과의 관계에 긴장이 생겨 모듈 혁신에 대한 투자에 부정적인 영향을 미칠 수 있었습니다.

부문 분석

승용차는 여전히 판매량의 대부분을 차지하고 있으며, 해치백, 세단, CUV 등 차체 스타일에 관계없이 표준화된 캐리어를 채택하여 2025년 자동차 프론트엔드 모듈 시장 규모의 59.13%를 차지했습니다. 중대형 상용차는 CAGR 8.71%를 나타낼 것으로 예측되며, 자동차 프론트엔드 모듈 시장에서 다른 어떤 차종보다 빠르게 성장할 것으로 예측됩니다. 이는 차량 소유주들이 라스트 마일 밴과 장거리 트랙터의 전동화를 추진하면서 통합형 써멀 루프와 고정밀 센서 마운트에 대한 의존도가 높아지고 있기 때문입니다. 다이믈러 트럭의 eCascadia는 조립 시간을 45분 단축하고, 알루미늄 캐리어를 채택하여 오버행(overhang)을 줄임으로써 창고 내 이동성에서 그 가치를 더욱 돋보이게 합니다.

유럽과 중국의 차량 전동화 정책 및 미국의 세제 혜택과 더불어, 상용차 OEM들은 배터리 열 관리 시스템을 도로 위의 이물질로부터 보호하고 충돌 방지를 위한 빠른 센서 보정을 가능하게 하는 밀폐형 그릴 모듈을 채택하고 있습니다. 포드 트랜짓(Ford Transit)과 램 프로마스터(Ram ProMaster)와 같은 소형 상용차에는 전방 충돌 방지 센서와 차선 유지 센서가 캐리어에 내장되어 2026년 미국 도로교통안전국(NHTSA)의 규제 요건을 준수할 수 있도록 하고 있습니다. 하이브리드 프레임 어셈블리는 18-22%의 경량화를 실현하여 배터리 무게를 상쇄하고 적재 용량을 유지하는 데 필수적이며, 예측 기간 동안 전체 물류 차량에서 그 역할을 확고히 할 수 있습니다.

2025년 기준 복합소재는 자동차 프론트엔드 모듈 시장의 44.25%를 차지했으며, Euro NCAP 및 IIHS의 새로운 테스트 기준으로 인해 금속에 대한 수요가 증가함에 따라 고강도 강철과 알루미늄의 하이브리드 소재는 CAGR 7.12%로 성장하여 2031년까지 자동차 프론트엔드 모듈 시장에서 점유율을 확대할 것으로 예측됩니다. Euro NCAP의 보다 엄격한 64km/시간 오프셋 충돌 테스트에서 부서지기 쉬운 복합재 레일이 불리하기 때문에 독일 OEM 업체들은 충돌용 레일에 특정 강종을 다시 채택하고 있습니다.

레이더 투과성이 매우 중요한 센서 영역에서는 복합소재의 채용이 각광받고 있습니다. 대신, 공급업체는 금속 서브 프레임 위에 열가소성 수지 페시아를 얹어 충격 에너지 흡수와 스타일링의 자유도를 동시에 확보했습니다. 비용에 민감한 신흥 시장에서는 플라스틱 캐리어가 주류를 이루고 있지만, EV의 가혹한 사용 조건에서 열화 위험으로 인해 그 성장이 제한되고 있습니다. 현재 규제에 따라 제조 단계의 탄소 배출량 공개가 의무화되어 있으며, 재활용 알루미늄은 무게, 충돌 성능 및 ESG 크레딧의 균형을 맞추기 위한 바람직한 절충안으로 자리매김하고 있습니다.

지역별 분석

2025년 기준 아시아태평양은 자동차 프론트엔드 모듈 시장의 46.34%를 차지했습니다. 이 시장은 2031년까지 연평균 복합 성장률(CAGR) 7.44%를 나타낼 것으로 예측됩니다. 현재 중국 승용차 생산에서 BYD와 SAIC의 대량 생산 모델에는 배터리 냉각기가 장착된 폐쇄형 그릴 캐리어가 표준 사양으로 적용되고 있습니다. 인도 자동차 산업에서는 PLI(생산연동형 인센티브) 제도에 따라 말레리, 아이신의 하이브리드 프레임 생산라인을 유치하고 있습니다. 일본의 정밀성형업체는 토요타 'bZ' 및 혼다 'e : N' 제품군에 77GHz 레이더 마운트를 내장하고 있으며, 엔저로 인한 원가경쟁력 향상에 따라 미국 공장에 수출하고 있습니다. 한국 현대모비스는 제네시스 GV60 및 기아 EV9 계약으로 2025년 모듈 수출 매출이 증가했습니다. 사이버 보안 규정 GB/T 40861과 바레트 NCAP 충돌 테스트 규정이 결합되어 진입 장벽을 높이고 센서 지원 모듈의 채택을 정착시키고 있습니다.

2025년 북미가 중요한 수익원으로 부상하고, USMCA(미국-멕시코-캐나다 협정)의 규정이 마그나와 HBPO의 사업 확장을 크게 견인했습니다. 테네시와 미시간 주에 걸친 이번 확장으로 연간 생산 능력이 크게 증가했습니다. 한편, 멕시코의 견고한 생산 수준은 과나후아토 주에 위치한 플렉스앤게이트의 금형 공장의 성장을 가속하고 있습니다. 캐나다에서는 2030년까지 ZEV(Zero Emission Vehicle) 의무화 요건을 충족하기 위한 노력으로 인해 배터리 팩의 열 효율을 높이는 밀폐형 그릴의 채택이 가속화되고 있습니다. 애프터마켓에서는 충돌 수리가 성장을 주도하고 있으며, 모듈식 캐리어가 보험사 벤치마크에 부합하는 사이클 타임을 개선하여 북미 세계 서비스 수익에서의 입지를 더욱 확고히 하고 있습니다.

2025년 수익에서 중요한 역할을 할 유럽에서는 독일, 프랑스, 스페인, 이탈리아가 주도적인 역할을 했습니다. 탈탄소화 노력의 일환으로 복합재 페시아의 후면에 액티브 셔터를 통합한 센서 지원 하이브리드 캐리어의 개발이 진행되고 있습니다. 2024년, 독일에서는 새로운 측면 기둥 충돌 시나리오를 포함한 업데이트된 충돌 테스트가 도입되어 고강도 강철 레일의 채택이 가속화되고 있습니다. 브렉시트 이후 HBPO의 선덜랜드 공장은 관세를 피함으로써 영국의 수출 경쟁력을 유지하고 있습니다. 폴비아의 프랑스 복합소재 기업 인수는 르노와 스텔란티스의 전기차 생산을 뒷받침하고 있습니다. 또한, 스페인과 이탈리아는 북아프리카 공장과의 지리적 근접성을 활용하여 물류적 우위를 확보하고 있습니다. 튀르키예와 남아공은 중동 및 아프리카 모듈 생산의 중심지이지만, 환율 변동으로 인해 자본 투자가 제한되고 있습니다. 남미에서는 하이브리드 자동차 보급을 촉진하는 현지 바이오연료 정책에 힘입어 브라질의 막대한 생산량이 수요를 견인하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The automotive front-end module market size is expected to grow from USD 131.96 billion in 2025 to USD 140.01 billion in 2026 and is forecast to reach USD 188.25 billion by 2031, growing at a CAGR of 6.10% during the forecast period (2026-2031).

Final-assembly outsourcing to tier-1 integrators that deliver complete bolt-on carriers is cutting plant labor by 20-30%, intensifying OEM demand for turnkey systems. Closed-grille architectures optimized for battery-electric thermal loops are spreading from premium EVs into volume segments, while precision mounts for radar, LiDAR, and camera sensors are transforming the module from a commodity bracket into a software-defined sensing hub. Heightened crash-test rigor under Euro NCAP and IIHS is driving a rebound in high-strength steel-aluminum hybrids that absorb energy while remaining light enough to meet CO2 rules. Near-shoring in North America and tariff-sensitive EU-UK corridors is re-shaping the supplier footprint as OEMs seek modules that meet significant regional-value thresholds under USMCA.

Global Automotive Front End Module Market Trends and Insights

EV Thermal-Management Need for Integrated, Closed-Grille FEMs

Battery-electric vehicles swap open radiator grills for sealed fascias that route air through chillers and condensers hidden behind the bumper beam, demanding carriers that package heat exchangers, coolant manifolds, and ducts in a single structure. Tesla achieved a significant drag reduction on its 2025 Model 3 refresh, while BYD's Blade Battery platform extends life by maintaining a +-2 °C band using Yinlun-supplied liquid-cooled carriers. In hot climates across Asia-Pacific and the United States Sunbelt, thermal integration is quickly becoming a gating item for range certification. Rivian has locked in a five-year contract with Valeo for dual-loop carriers consolidating battery and drive-unit cooling, illustrating the deep co-development ties now required. Long-term, EV-specific modules will underpin 50% of the automotive front-end module market revenue as BEV share breaches 50% of global sales in the early 2030s.

Lightweighting and Stricter CO2 / Fuel-Economy Regulations

Global emissions policies are driving automakers to reduce the weight of traditional steel carriers, accelerating the adoption of materials such as aluminum extrusions, carbon-fiber-reinforced thermoplastics, and magnesium die-casts. These materials are critical for meeting the EU's fleet-average emissions targets by 2030. In China, regulatory frameworks are pushing OEMs to adopt hybrid-frame modules that maintain crash energy absorption while significantly reducing weight. In the United States, updated CAFE rules finalized in 2024 are prompting automakers like Ford and GM to transition to multi-material carriers. These carriers integrate essential components such as crash rails, cooling packs, and sensor plates within a lightweight design. ISO 14040 life-cycle reporting is increasing the demand for recycled aluminum and bio-based resins, encouraging suppliers to qualify low-carbon materials and tap into new revenue opportunities tied to ESG credits. These regulatory trends are embedding lightweighting into every vehicle program from 2026 onward, establishing it as the most significant value-creation driver for suppliers in the automotive front-end module market.

Volatile Steel, Polymer and Energy Prices Inflate BOM Cost

In 2025, hot-rolled coil prices increased compared to the previous year, driven by EU energy surcharges that raised electric-arc-furnace overheads. During the same year, a force majeure on the Gulf Coast led to a significant rise in polypropylene prices, negatively impacting tier-1 gross margins. Higher European gas prices led to a notable increase in molding energy costs, adding to the production expenses for hybrid frames. Aluminum extrusion premiums rose due to Section 232 tariffs, intensifying spot-buy exposure. Suppliers with fixed-price contracts for the year faced profitability challenges, leading to more frequent renegotiations that strained relationships with OEMs and potentially affected investments in module innovation.

Other drivers and restraints analyzed in the detailed report include:

- ADAS Sensor-Mounting Demand Elevates Structural Precision Requirements

- OEM Outsourcing of Modular FEMs to Cut 20-30% Assembly Cost

- High R&D / Tooling Spend for Multi-Material Sensor-Ready Frames

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger Cars still account for the bulk of volume, with a 59.13% of the automotive front-end module market size in 2025, and adopt standardized carriers across hatchback, sedan, and CUV body styles. Medium- and heavy-duty commercial vehicles will post an 8.71% CAGR, expanding the automotive front-end module market faster than any other vehicle class as fleet owners electrify last-mile vans and long-haul tractors that rely on integrated thermal loops and precision sensor mounts. Daimler Truck's eCascadia specifies an aluminum carrier that trims assembly by 45 minutes and shortens overhang, highlighting value for depot maneuverability .

Fleet electrification policies in Europe and China, alongside U.S. tax incentives, are driving commercial OEMs toward sealed-grille modules that protect battery thermal systems from road debris while enabling quick sensor calibration for collision avoidance. Light commercial vehicles such as Ford Transit and Ram ProMaster are embedding forward-collision and lane-keep sensors into the carrier, ensuring compliance with 2026 NHTSA mandates. Hybrid-frame assemblies deliver 18-22% mass savings, essential for offsetting battery weight and retaining payload capacity, cementing their role across logistics fleets over the forecast horizon.

Composites controlled 44.25% of the automotive front-end module market in 2025, yet renewed Euro NCAP and IIHS protocols are boosting metal demand, pushing high-strength steel and aluminum hybrids toward a 7.12% CAGR and expanding their share of the automotive front-end module market through 2031. Euro NCAP's more challenging 64 km/h offset test penalizes brittle composite rails, prompting German OEMs to reinstate specific steel grades in crash rails .

Composite uptake plateaus in sensor zones where radar transparency is critical; instead, suppliers use metal subframes topped with thermoplastic facias to blend impact energy absorption with styling freedom. Plastic carriers dominate cost-sensitive emerging markets, but their growth is constrained by thermal degradation risks under high-ambient EV duty cycles. Regulations now require embodied-carbon disclosure, positioning recycled aluminum as a favored middle ground that balances weight, crash performance, and ESG credits.

The Automotive Front-End Module Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Raw Material (Metal, Plastic, and More), Product Type (Metal Frame, Plastic Frame, and More), Application (Body Structure, Cooling and Air-Conditioning, and More), End Use (OEM, Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 46.34% of the automotive front-end module market in 2025. It will grow at a 7.44% CAGR through 2031. China's passenger output now specifies closed-grille carriers with battery chillers as standard on high-volume BYD and SAIC models. India's industry attracts Marelli and Aisin hybrid-frame lines under PLI incentives. Japan's precision molders embed 77 GHz radar mounts for Toyota bZ and Honda e: N families, exporting to U.S. plants as yen depreciation improves cost competitiveness. South Korea's Hyundai Mobis grew export module revenue in 2025 due to contracts for the Genesis GV60 and Kia EV9. Cybersecurity regulation GB/T 40861 and Bharat NCAP crash test rules jointly raise barriers, cementing the adoption of sensor-ready modules.

In 2025, North America emerged as a significant contributor to revenue, with the USMCA's rules driving a major expansion for Magna and HBPO. This expansion, spanning Tennessee and Michigan, significantly increased annual production capacity. Meanwhile, Mexico's robust production levels are fostering growth in Flex-N-Gate's tool room in Guanajuato. In Canada, efforts to meet the ZEV mandate by 2030 are accelerating the adoption of sealed grilles to enhance battery-pack thermal efficiency. The aftermarket is witnessing growth led by collision repair, with modular carriers improving cycle times to align with insurer benchmarks, further strengthening North America's position in global service revenue.

Europe, a key player in 2025 revenue, is led by Germany, France, Spain, and Italy. Decarbonization initiatives are driving the development of sensor-ready hybrid carriers with active shutters integrated behind composite facias. In 2024, Germany introduced updated crash tests, including a new side-pole scenario, which is expediting the use of high-strength steel rails. Post-Brexit, HBPO's Sunderland site has maintained the UK's export competitiveness by avoiding tariffs. Forvia's acquisition of a French composite firm is supporting Renault and Stellantis's EV production. Additionally, Spain and Italy are leveraging their proximity to North African plants for logistical advantages. Turkey and South Africa are central to module production for the Middle East & Africa, though currency volatility is limiting their capital investments. In South America, Brazil's substantial production volumes are driving demand, supported by local biofuel policies that are encouraging hybrid adoption.

- HBPO GmbH

- Magna International Inc.

- Forvia SE

- OPMOBILITY SE (Plastic Omnium)

- Hyundai Mobis Co., Ltd.

- DENSO Corporation

- Valeo SA

- Marelli Holdings Co., Ltd.

- Samvardhana Motherson Group

- SL Corporation

- Flex-N-Gate Corporation

- Aisin Corporation

- Benteler Automotive

- Yinlun Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Thermal-Management Need for Integrated, Closed-Grille FEMs

- 4.2.2 Lightweighting and Stricter CO? / Fuel-Economy Regulations

- 4.2.3 ADAS Sensor-Mounting Demand Elevates Structural Precision Requirements

- 4.2.4 OEM Outsourcing of Modular FEMs to Cut 20-30% Assembly Cost

- 4.2.5 Active Grille-Shutter / Adaptive-Aero Adoption Boosting Premium FEM Content

- 4.2.6 Near-Shoring of FEM Production in Tariff-Sensitive Markets

- 4.3 Market Restraints

- 4.3.1 Volatile Steel, Polymer and Energy Prices Inflate BOM Cost

- 4.3.2 High R&D / Tooling Spend for Multi-Material Sensor-Ready Frames

- 4.3.3 Cyber-Security and Homologation Hurdles for Connected Sensor-Rich Modules

- 4.3.4 Radar-Signal Attenuation Issues with Certain Composite Mixes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power Of Suppliers

- 4.7.2 Bargaining Power Of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.2 By Raw Material

- 5.2.1 Metal

- 5.2.2 Plastic

- 5.2.3 Composite

- 5.2.4 Hybrid

- 5.3 By Product Type

- 5.3.1 Metal Frame

- 5.3.2 Plastic Frame

- 5.3.3 Hybrid Frame

- 5.4 By Application

- 5.4.1 Body Structure

- 5.4.2 Cooling and Air-Conditioning

- 5.4.3 Sensor Integration

- 5.4.4 Lighting Systems

- 5.5 By End Use

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 HBPO GmbH

- 6.4.2 Magna International Inc.

- 6.4.3 Forvia SE

- 6.4.4 OPMOBILITY SE (Plastic Omnium)

- 6.4.5 Hyundai Mobis Co., Ltd.

- 6.4.6 DENSO Corporation

- 6.4.7 Valeo SA

- 6.4.8 Marelli Holdings Co., Ltd.

- 6.4.9 Samvardhana Motherson Group

- 6.4.10 SL Corporation

- 6.4.11 Flex-N-Gate Corporation

- 6.4.12 Aisin Corporation

- 6.4.13 Benteler Automotive

- 6.4.14 Yinlun Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment