|

시장보고서

상품코드

2044148

웹 애플리케이션 방화벽 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Web Application Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

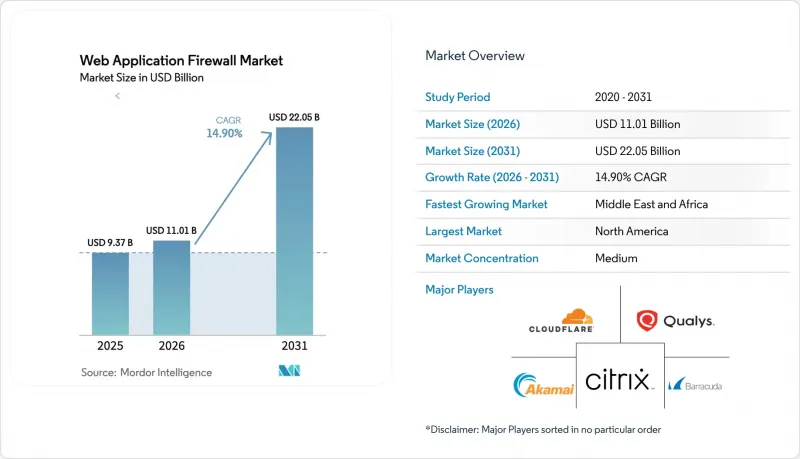

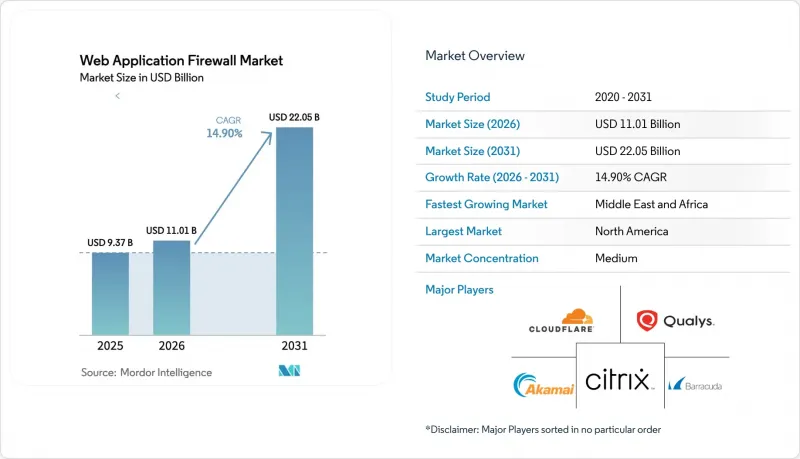

웹 애플리케이션 방화벽(WAF) 시장 규모는 2025년에 93억 7,000만 달러로 평가되었고 2026년 110억 1,000만 달러에서 2031년까지 220억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 14.9%를 나타낼 전망입니다.

이 확장은 네 가지 강력한 트렌드를 중심으로 전개되고 있습니다. GraphQL, gRPC, WebSocket 트래픽 검사를 강제하는 API 레이어에 대한 악용이 급증하고 있으며, 클라우드 네이티브 마이크로서비스로의 빠른 전환, 실시간 모니터링을 법적 요구사항으로 승화시키는 세계 프라이버시 규제 강화, 엣지 기반에서 머신러닝 분석을 적용하여 지연을 줄이는 엣지 네이티브 방어. 엣지 거점에서 머신러닝 분석을 적용하면서 지연을 줄이는 엣지 네이티브 방어입니다. 하이퍼스케일 기업들이 클라우드 구독에 네이티브 WAF를 번들로 제공하고, 전문 CDN 사업자들이 10밀리초 미만의 검사로 수익을 창출하고, 레거시 어플라이언스 벤더들이 가상 에디션을 통해 현대화를 추진하면서 경쟁이 치열해지고 있습니다. 벤처펀드는 커널 레벨의 검사를 위해 확장된 Berkeley Packet Filter(eBPF)를 통합하는 초기 단계의 스타트업을 대상으로 하고 있으며, 오픈소스 Core Rule Set의 채택으로 가격 결정력은 약화되었지만, 매니지드 SOC 통합에 대한 수요는 줄어들지 않고 있습니다. 는 줄어들지 않고 있습니다. 예산에 제약이 있는 중소기업은 클라우드 이용형 요금체계로 어플라이언스 설비투자가 불필요하고, 도입 기간이 몇 주에서 몇 시간으로 단축되면서 웹 애플리케이션 방화벽 시장에 역대 최고 속도로 진입하고 있습니다.

세계 웹 애플리케이션 방화벽 시장 동향 및 인사이트

API 공격 급증

현재 API 엔드포인트는 악성 트래픽의 대부분을 끌어들이고 있으며, 2024년에는 1,500억 건의 API 관련 이벤트가 기록됐습니다. 이 수치는 공격자들이 스키마 인트로스펙션과 일괄 처리된 변경 사항을 악용함에 따라 계속 증가하고 있습니다. 2023년 1분기부터 2024년 4분기까지 레이어 7 디도스 공격 활동은 94% 증가하여 월 1조 1,000억 건 이상의 요청이 발생하여 기본적인 HTTP 시맨틱만 분석할 수 있는 레거시 엔진에 부하를 주고 있습니다. 이에 대해 기업들은 OpenAPI 정의에 위배되는 요청을 거부하는 계약 기반 검증 기능을 추가하여 대응하고 있으며, 이러한 변화로 인해 경계 방어가 사실상 마이크로 서비스 계약까지 확대되고 있습니다. 기존 시그니처 데이터베이스는 복잡한 페이로드 구조를 이해할 수 없기 때문에 GraphQL 파서나 gRPC 디코더를 내장한 벤더들이 웹 애플리케이션 방화벽 시장에서 점유율을 확대되고 있습니다. 이에 따라 API 트래픽과 봇 관리 시그널, 자동 차단을 위한 행동 베이스라인을 상관 분석할 수 있는 플랫폼에 대한 도입이 진행되고 있습니다.

클라우드 네이티브와 마이크로서비스 확산

쿠버네티스 운영 기업의 70% 이상이 수천 개의 임시 포드를 생성하고 있으며, 각 포드는 수명이 짧은 엔드포인트를 생성하기 때문에 정적 어플라이언스 구성으로는 대응할 수 없는 상황입니다. 150밀리초 이내에 WAF 인스턴스를 시작할 수 있는 엣지 아키텍처는 서버리스 라이프사이클에 적합하고 워크로드 탄력성을 지원하여 웹 애플리케이션 방화벽 시장이 헤어핀 라우팅으로 인한 성능 저하 없이 보호 기능을 제공할 수 있도록 보장합니다. 보장하고 있습니다. 서비스 메시의 사이드카는 검사를 클러스터 내 트래픽에 직접 통합하여 네트워크 상의 우회를 제거하면서 선언형 YAML 파이프라인에서 정책을 상속합니다. 도입의 핵심은 WAF를 코드로 관리할 수 있는 능력으로, 규칙을 Infrastructure-as-Code 템플릿에 포함시켜 모든 빌드가 강화된 기본 설정을 상속할 수 있도록 하는 것입니다. 검사 기능을 하드웨어와 분리할 수 없는 벤더들은 컨테이너 네이티브 구매자들이 랙마운트 처리량보다 배포 속도를 더 중요하게 생각함에 따라 점유율 하락에 직면하고 있습니다.

높은 오감지율로 인한 업무 차질

Core Rule Set의 기본 경보 수준은 10-15%의 오감지를 유발하고, 블랙프라이데이에는 쇼핑 카트를 차단하고, 지원팀에 문의하는 건수를 증가시키고 있습니다. 소매업체들은 매출 손실과 부정행위 증가라는 '양자택일' 상황에 직면해 있으며, 샌드박스를 통한 튜닝 환경과 실시간 룰 롤백 기능에 투자할 수밖에 없는 상황에 직면해 있습니다. 머신러닝 오버레이는 균형 정확도를 45% 향상시키지만, 지속적인 재교육과 고품질 라벨이 필요하기 때문에 운영 비용이 증가합니다. 현재 상용 벤더들은 오감지율 1% 이하를 약속하는 관리형 튜닝 구독 서비스를 제공하고 있으며, 이는 웹 애플리케이션 방화벽 시장에서의 차별화 요소로 작용하고 있습니다. 구매자는 다년 계약을 체결하기 전에 플래시 세일 시뮬레이션을 통해 고객 이탈률 감소를 입증하는 실증 데이터를 요구하는 경향이 강해지고 있습니다.

부문 분석

규제 당국이 보호 대상 의료 정보와 카드 소지자 데이터는 On-Premise에 보관하고, 공개 웹사이트는 클라우드에 보관할 것을 요구하면서 하이브리드 아키텍처에 대한 인식이 높아졌습니다. 2025년 웹 애플리케이션 방화벽 시장에서 클라우드 기반 제품의 점유율은 64.11%였으나, 하이브리드는 CAGR 15.57%로 확대될 것으로 예상되며, 이는 동 카테고리에서 가장 빠른 속도로 성장할 것으로 예측됩니다. CFO는 해외에서 검사 포인트를 금지하는 감사인을 설득하면서 설비투자(CAPEX)를 억제할 수 있는 하이브리드의 능력을 평가했습니다. 하지만 On-Premise형 어플라이언스와 클라우드 콘솔은 규칙 구문이 다르기 때문에 보안 담당자의 고민은 정책의 난립입니다. 통일된 JSON 스키마를 F5 어플라이언스, AWS WAF, Azure Application Gateway에 푸시하는 중앙 관리 시스템은 설정의 편차를 줄이기 위해 중요한 구매 기준이 되고 있습니다. 멀티 클라우드 추상화 기능이 없는 벤더는 모든 적용 지점을 추적할 수 있는 단일 대시보드로의 표준화가 진행됨에 따라 고객 이탈에 직면하고 있습니다. 인도와 중국이 데이터 현지화를 의무화하면서 On-Premise 키와 번들로 제공되는 로컬 POP 배포 키트에 대한 수요가 증가하고 있으며, 하이브리드 배포와 관련된 웹 애플리케이션 방화벽 시장 규모를 확대되고 있습니다.

동시에 클라우드만 채택하는 기업은 여전히 벤더 종속성에 민감합니다. 테라폼 모듈을 통한 마이그레이션 전략이 호응을 얻고 있습니다. 이는 가격이 급등하더라도 휴대성을 보장할 수 있다고 약속하고 있기 때문입니다. 시장 기반 과금 체계는 개념증명(PoC)을 가속화하고, 팀이 1시간 이내에 종량제 WAF를 가동할 수 있게 해줍니다. 이는 하드웨어 견적을 의뢰하는 조달위원회를 경유하는 경우 불가능한 속도입니다. 그 결과, 레거시 어플라이언스의 매출은 규제가 엄격한 틈새 시장에서만 성장하는 반면, 구독 ARR(연간 반복 매출)은 새로운 마이크로 서비스가 프로덕션 환경에 투입될 때마다 확대됩니다.

2025년 솔루션이 지출의 71.29%를 차지했지만, 인력 시장의 압박으로 인해 전문 서비스 및 관리 서비스는 CAGR 15.97%로 구성 요소 중 가장 빠른 성장 궤도에 진입할 것으로 예측됩니다. 구매자는 제로데이 공격 봉쇄에 걸리는 시간, 오탐 해결에 걸리는 평균 시간 등의 지표로 공급자를 평가하며, 이러한 지표는 계약 갱신 결정에 큰 영향을 미칩니다. 매니지드 SOC 번들은 현재 WAF의 텔레메트리를 엔드포인트 및 네트워크 센서와 통합하여 대응을 가속화하는 통합된 킬체인을 구축하고 있습니다. 중견기업은 24시간 365일 체제가 부족하기 때문에 변경 자문위원회를 거치지 않고 매월 지속적인 업데이트를 제공하는 턴키형 서비스가 넘쳐나고 있으며, 이로 인해 웹 애플리케이션 방화벽 시장 전체에서 지속적인 수익이 확대되고 있습니다.

각 업체들은 자체 위협 인텔리전스 피드와 평이한 영어로 된 모드시큐리티 정규식을 자동 생성하는 언어 모델 어시스턴트를 활용해 차별화를 꾀하고 있습니다. 이러한 기능을 통해 벤더의 불투명성을 우려해 관리형 보안을 기피하던 고객들을 끌어들이고 있습니다. 로우엔드 시장에서는 화이트 라벨 플랫폼을 통해 통신사업자가 자체 브랜드 WAF를 재판매할 수 있게 되면서 유통망이 확대되고, 브로드밴드 번들에 대한 검사 기능이 더욱 심도 있게 통합되고 있습니다. 따라서 웹 애플리케이션 방화벽 시장은 '서비스형(as-a-service)'으로 전환되고 있으며, 영구 라이선스는 기존의 갱신 주기에 머물러 있는 경향이 있습니다.

지역별 분석

2025년 북미는 웹 애플리케이션 방화벽 시장 매출의 38.73%를 차지했습니다. CCPA의 확대부터 PCI DSS v4.0 의무 준수에 이르기까지 지속적인 규제 요구사항으로 인해 WAF를 단순한 선택적 애드온이 아닌 필수 인프라로 취급하는 구매 문화가 형성되고 있습니다. 하이퍼스케일러에 의한 엣지 네트워크의 포화 상태와 SOC 인력의 최고 밀도가 결합되어 전 세계 기능에 대한 기대치를 결정하는 빠른 기능 배포를 촉진하고 있습니다. 캐나다의 주별 프라이버시 법이 하이브리드 수요를 주도하고 있으며, 멕시코의 니어쇼어(Nearshore)는 새로운 전자상거래 트래픽을 미국 기반 검사 노드로 유도하여 국경 간 관리형 서비스 수익을 유지하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정), NIS2, DORA를 통해 엄격한 감독이 유지되고 있으며, 기업에게 실시간 모니터링과 24시간 사고 보고의 실증을 요구하고 있습니다. 슐렘스 II 판결로 인해 대서양 횡단 데이터 흐름이 복잡해짐에 따라 많은 기업들이 EU의 소버린 클라우드 내에 지역별로 WAF 클러스터를 구축하고 있으며, 이로 인해 웹 애플리케이션 방화벽 시장에서 유럽의 점유율이 확대되고 있습니다. 독일의 BSI와 프랑스의 ANSSI와 같은 국가 기관은 벤더의 제품 로드맵에 영향을 미치는 부문별 프레임워크를 발표했으며, 특히 언어별 형태로 제공되는 변조 방지 기능을 갖춘 감사 로그에 대한 요구 사항이 포함됩니다. 브렉시트로 인해 영국은 병행하면서도 유사한 기준을 유지하게 되었고, 다국적 은행들은 이중의 컴플라이언스 체제를 구축해야 하는 상황에 놓이게 되었습니다.

중국이 '개인정보보호법(PIPL)'과 '머신러닝 프라이버시법(MLPS 2.0)'을 시행하고, 인도가 '디지털 개인정보 보호법'을 최종 결정함에 따라 아태지역에서 가장 급격한 도입 확대가 이루어질 것으로 보입니다. 두 제도 모두 국내 검사를 의무화하고 있으며, 이로 인해 외국 벤더의 국내 데이터센터 건설을 촉진하고 있습니다. 일본 금융청의 핀테크 앱에 대한 지침과 한국의 PIPA(개인정보보호법)로 인해 전자결제 업체들 사이에서 높은 지출이 유지되고 있습니다. 인도네시아와 베트남의 스타트업 기업들은 지역별 컴플라이언스 요건과 비용 관리를 동시에 충족할 수 있는 클라우드 구독을 선호하고 있으며, 이는 아시아태평양의 웹 애플리케이션 방화벽 시장 규모를 더욱 확대할 것으로 보입니다.

중동 및 아프리카는 아랍에미리트의 DPDP법 의무화와 사우디아라비아의 사이버 보안 규제에 힘입어 2031년까지 연평균 성장률(CAGR) 15.79%로 가장 높은 성장률을 나타낼 것으로 예측됩니다. '비전 2030' 메가 프로젝트로 공공서비스가 디지털화되는 가운데, 아랍어 로그 대응과 현지 SOC(보안운영센터)와의 통합이 요구되고 있습니다. 이스라엘의 혁신 생태계에서 AI를 활용한 WAF 스타트업이 탄생하여 걸프협력회의(GCC) 회원국에 수출되고 있습니다. 남미는 브라질의 LGPD(개인정보보호법) 주도의 현대화 및 금융기관에 WAF 도입을 명시적으로 의무화한 결의안 4.893이 시장을 주도하고 있습니다. 아프리카는 아직 초기 단계에 머물러 있지만, 남아공의 POPIA(개인정보보호법)가 은행과 통신사업자들의 시범 도입에 힘을 실어주면서 전 세계 웹 애플리케이션 방화벽 시장에 점진적인 수요를 불러일으키고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Web application firewall market size was valued at USD 9.37 billion in 2025 and estimated to grow from USD 11.01 billion in 2026 to reach USD 22.05 billion by 2031, at a CAGR of 14.9% during the forecast period 2026-2031.

The expansion pivots on four powerful trends: skyrocketing API-layer abuse that forces inspection of GraphQL, gRPC and WebSocket traffic, rapid shift to cloud-native micro-services, tightening global privacy mandates that elevate real-time monitoring to a legal necessity, and edge-native defenses that lower latency while applying machine-learning analytics at the point of presence. Competitive intensity accelerates as hyperscale's bundle native WAF into cloud subscriptions, specialist CDNs monetize sub-10-millisecond inspection, and legacy appliance vendors modernize through virtual editions. Venture funding targets early-stage start-ups embedding extended Berkeley Packet Filter (eBPF) for kernel-level inspection, while open-source Core Rule Set adoption tempers pricing power but not demand for managed SOC integration. Budget-constrained small and medium enterprises enter the Web application firewall market at record pace because cloud consumption pricing removes appliance capex and reduces deployment from weeks to hours.

Global Web Application Firewall Market Trends and Insights

API-Attack Volume Surge

API endpoints now attract the majority of hostile traffic, with 150 billion API-specific events logged in 2024, a figure that continues to climb as attackers exploit schema introspection and batched mutations. Layer 7 DDoS activity rose 94% between Q1 2023 and Q4 2024, passing 1.1 trillion requests a month, pressuring legacy engines that only parse basic HTTP semantics. Enterprises respond by adding contract-driven validation that rejects requests violating OpenAPI definitions, a shift that effectively extends perimeter defense into micro-service contracts. Vendors embedding GraphQL parsers and gRPC decoders win share in the Web application firewall market as traditional signature databases fail to understand rich payload constructs. The trend drives procurement toward platforms able to correlate API traffic with bot-management signals and behavioural baselines for automated cutoff.

Cloud-Native and Micro-Services Proliferation

Seventy-plus percent of enterprises running Kubernetes generate thousands of ephemeral pods, each spawning short-lived endpoints that overwhelm static appliance configurations. Edge architectures capable of spinning a WAF instance in under 150 milliseconds now align with serverless life cycles, matching workload elasticity and ensuring the Web application firewall market provides protection without hairpin routing penalties. Service-mesh sidecars push inspection directly into intra-cluster traffic, eliminating network detours while inheriting policy from declarative YAML pipelines. Central to adoption is the ability to manage WAF as code, embedding rules inside Infrastructure-as-Code templates so every build inherits hardened defaults. Vendors unable to decouple inspection from hardware see share erosion as container-native buyers prize speed of deployment over rack-mounted throughput.

High False-Positive Business Disruption

Default paranoia levels in Core Rule Set trigger 10-15% false positives, blocking carts on Black Friday and inflating support call volume. Retailers confront a lose-lose scenario of lost revenue versus added fraud, prompting them to invest in sandbox tuning environments and real-time rule rollback features. Machine-learning overlays improve balanced accuracy by 45% but demand continuous retraining and high-quality labels, raising operational cost. Commercial vendors now package managed-tuning subscriptions that promise sub-1% false-positive rates, a differentiator within the Web application firewall market. Buyers increasingly request proof points showing decreased customer drop-offs during flash-sale simulations before signing multiyear contracts.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global Data-Protection Mandates

- Edge/CDN Integration for Performance

- Talent Gap for Advanced Tuning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures captured growing mindshare once regulators insisted that protected health information and cardholder data remain on premises while public websites stayed in cloud. The Web application firewall market share for cloud-based offerings stood at 64.11% in 2025, but hybrid is projected to advance at a 15.57% CAGR, the category's fastest pace. CFOs like hybrid's ability to cap capex while appeasing auditors who prohibit foreign inspection points. Policy sprawl, however, bedevils security staff because on-premises appliances and cloud consoles expose dissimilar rule syntax. Central managers that push a unified JSON schema to F5 appliances, AWS WAF and Azure Application Gateway reduce drift, making them a key purchase criterion. Vendors without multi-cloud abstraction see churn as buyers standardize on single dashboards that track every enforcement point. As India and China enforce data-localization, demand rises for local pop deployment kits bundled with on-premises keys, expanding the Web application firewall market size associated with hybrid rollouts.

Simultaneously, cloud-only adopters remain sensitive to vendor lock-in. Exit strategies rooted in Terraform modules gain favour because they promise portability should pricing spike. Marketplace billing accelerates proof-of-concepts, letting teams activate pay-as-you-go WAF in under an hour, a speed impossible with procurement committees requesting hardware quotes. Consequently, legacy appliance revenue grows only in regulated niches, whereas subscription ARR scales with each new micro-service pushed into production.

Solutions dominated spending at 71.29% in 2025, but tight labour markets push professional and managed services toward a 15.97% CAGR, the quickest trajectory within components. Buyers benchmark providers on time-to-contain zero-day injections and mean-time-to-resolve false positives, metrics that strongly influence renewal decisions. Managed SOC bundles now stitch WAF telemetry to endpoint and network sensors, building a unified kill chain that accelerates response. Because middle-market companies lack 24 7 coverage, they flock to turnkey offerings that issue rolling monthly updates without change-advisory boards, boosting recurring revenue across the Web application firewall market size.

Providers differentiate using proprietary threat-intelligence feeds and language-model assistants that auto-generate ModSecurity regex in plain English. Those capabilities win accounts that traditionally shunned managed security for fear of vendor opacity. Down-market, white-label platforms allow telecom carriers to resell branded WAF, widening distribution and embedding inspection deeper into broadband bundles. The Web application firewall market therefore tilts toward as-a-service consumption, relegating perpetual licenses to legacy renewal cycles.

The Web Application Firewall Market Report is Segmented by Deployment Mode (Cloud-Based WAF, On-Premises/Appliance, and Hybrid), Component (Solutions, and Professional and Managed Services), End-User Industry (BFSI, Healthcare, IT and Telecom, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America supplied 38.73% of Web application firewall market revenue in 2025. Continuous mandates from CCPA expansions to mandatory PCI DSS v4.0 compliance create a buyer culture that treats WAF as essential infrastructure rather than optional add-on. Edge-network saturation by hyperscalers, coupled with the highest density of SOC talent, fosters rapid feature rollouts that set functional expectations worldwide. Canada's provincial privacy acts drive hybrid demand, while Mexican near-shore expansions funnel new e-commerce traffic through U.S.-based inspection nodes, sustaining cross-border managed-service revenue.

Europe maintains strict oversight through GDPR, NIS2 and DORA, pushing enterprises to demonstrate real-time monitoring and 24-hour incident reporting. Schrems II rulings complicate trans-Atlantic data flows, so many firms deploy regional WAF clusters inside EU sovereign clouds, enlarging the European slice of the Web application firewall market. National agencies like Germany's BSI and France's ANSSI issue sector frameworks that influence vendor product roadmaps, especially the requirement for tamper-evident audit logs delivered in language-specific formats. Brexit leaves the United Kingdom maintaining parallel yet similar standards, forcing multinational banks to map dual compliance regimes.

Asia-Pacific shows the steepest adoption curve as China enforces PIPL and MLPS 2.0 and India finalizes its Digital Personal Data Protection Act. Both regimes require in-country inspection, stimulating domestic data-center buildouts by foreign vendors. Japan's FSA guidance for fintech apps and South Korea's PIPA sustain high spend among electronic payments providers. Start-ups in Indonesia and Vietnam prefer cloud subscriptions that remix regional compliance with cost control, further enlarging the Web application firewall market size across APAC.

The Middle East and Africa projects the highest CAGR at 15.79% through 2031, spurred by UAE DPDP Act mandates and Saudi Arabia's cybersecurity controls. Vision 2030 megaprojects digitize public services, requiring Arabic-language log support and local SOC integration. Israel's innovation ecosystem spawns AI-driven WAF start-ups that export to Gulf Cooperation Council neighbours. South America follows with LGPD-driven modernization in Brazil and resolution 4.893 that explicitly requires WAF for financial institutions. Africa remains early-stage, though South Africa's POPIA nudges banking and telecom operators toward pilot deployments, adding incremental volume to the global Web application firewall market.

- F5, Inc.

- Akamai Technologies, Inc.

- Cloudflare, Inc.

- Imperva (Thales Digital Identity and Security)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Fortinet, Inc.

- Barracuda Networks, Inc.

- Radware Ltd.

- Fastly, Inc.

- Citrix Systems, Inc.

- StackPath, LLC

- Sophos Limited

- Palo Alto Networks, Inc.

- Trend Micro Inc.

- A10 Networks, Inc.

- Reblaze Technologies Ltd.

- Datadog Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 API-Attack Volume Surge

- 4.2.2 Cloud-Native and Micro-Services Proliferation

- 4.2.3 Stricter Global Data-Protection Mandates

- 4.2.4 Edge/CDN Integration for Performance

- 4.2.5 AI-Enhanced Threat Analytics at the Edge

- 4.2.6 "Security-as-Code" DevSecOps Adoption

- 4.3 Market Restraints

- 4.3.1 High False-Positive Business Disruption

- 4.3.2 Talent Gap for Advanced Tuning

- 4.3.3 QUIC/HTTP-3 Encryption Inspection Cost

- 4.3.4 Open-Source WAF Dilution

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based WAF

- 5.1.2 On-Premises / Appliance

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Professional and Managed Services

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Retail and E-Commerce

- 5.3.6 Energy and Utilities

- 5.3.7 Manufacturing

- 5.3.8 Other End-User Industry

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 F5, Inc.

- 6.4.2 Akamai Technologies, Inc.

- 6.4.3 Cloudflare, Inc.

- 6.4.4 Imperva (Thales Digital Identity and Security)

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Google LLC

- 6.4.8 Fortinet, Inc.

- 6.4.9 Barracuda Networks, Inc.

- 6.4.10 Radware Ltd.

- 6.4.11 Fastly, Inc.

- 6.4.12 Citrix Systems, Inc.

- 6.4.13 StackPath, LLC

- 6.4.14 Sophos Limited

- 6.4.15 Palo Alto Networks, Inc.

- 6.4.16 Trend Micro Inc.

- 6.4.17 A10 Networks, Inc.

- 6.4.18 Reblaze Technologies Ltd.

- 6.4.19 Datadog Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment