|

시장보고서

상품코드

2044149

스포츠용 웨어러블 디바이스 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Wearable Devices In Sports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

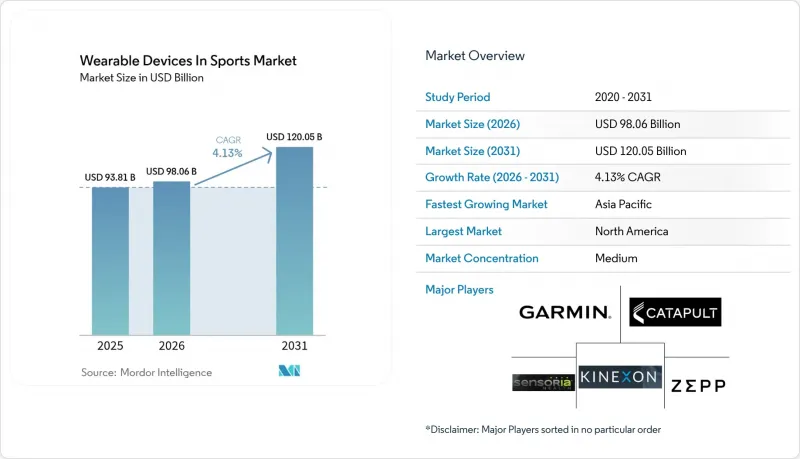

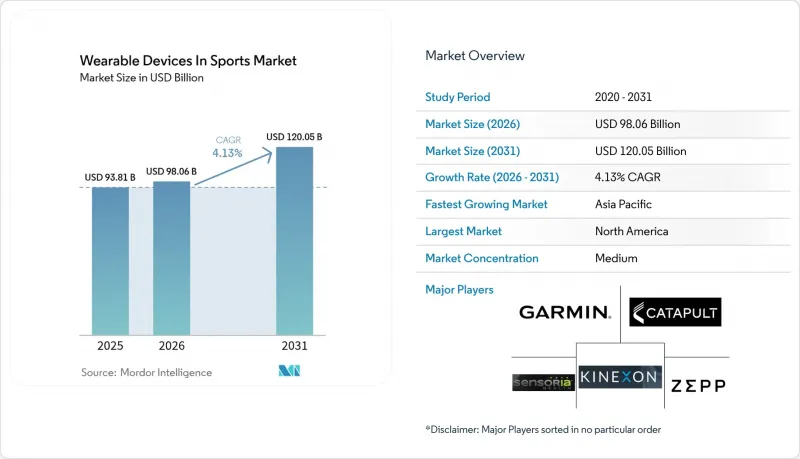

스포츠용 웨어러블 디바이스 시장 규모는 2025년 938억 1,000만 달러에서 2026년에는 980억 6,000만 달러로 확대되어 2031년까지 1,200억 5,000만 달러에 이를 것으로 예상되고 있으며 2026-2031년까지 CAGR 4.13%로 성장할 전망입니다.

현재 프로리그에서는 단체협약에 생체 측정 데이터 추적이 포함되어 있으며, 일반 사용자들 사이에서는 실시간으로 부상 위험 점수를 산출하는 AI를 활용한 코칭이 확산되고 있습니다. 소니의 2025년 STATSports 인수는 센서 하드웨어와 클라우드 분석을 통합하는 플랫폼 통합으로의 전환을 보여주는 좋은 예입니다. 움직임을 제한하지 않고 운동, 열, 전기생리학적 신호를 포착하는 섬유 일체형 센서는 이 부문을 손목 밴드의 틀을 넘어 일반 스포츠웨어와 같은 착용감 있는 웨어에 대한 수요를 뒷받침하고 있습니다. 북미에서의 우위는 NFL(National Football League)과 MLB(Major League Baseball)의 머리 충격 및 투구 생체역학 모니터링 의무화에 힘입은 바 있지만, 인도 크리켓과 중국 아카데미 프로그램에서 GPS 추적이 제도화됨에 따라 아시아태평양이 더 빠른 성장세를 보이고 있습니다. 주요 리스크는 단체협약에 포함된 새로운 데이터 프라이버시 조항에 있으며, 이로 인해 생체 데이터의 제3자 판매가 제한되어 제품 출시가 지연될 수 있습니다.

세계의 스포츠용 웨어러블 기기 시장 동향 및 인사이트

데이터 기반 성능 분석에 대한 수요 증가

현재 팀들은 생체 측정 데이터를 계약상의 성과물로 간주하고, 선수의 출전 여부 조항에 회복 점수를 반영하고 있습니다. 프로테니스선수협회(ATP)는 2024년 경기 중 웨어러블 기기 사용을 승인하여 운동량 임계값과 코트 커버리지 히트맵을 기반으로 한 실시간 코칭 조정을 가능하게 했습니다. 대학 스카우트들은 유망주들에게 다년간의 데이터 세트를 요구하고 있으며, 이로 인해 선수들의 장기적인 기록을 다루는 2차 시장이 형성되고 있습니다. 미국프로풋볼선수협회(NFLPA)는 2024년 중앙집중식 데이터 저장소를 개설하여 선수들이 익명화된 데이터를 연구자들에게 제공할 수 있도록 하는 한편, 상업적 이용에 대한 거부권을 보유할 수 있도록 했습니다. 보험사도 웨어러블 단말기의 과거 추세를 바탕으로 부상 위험에 대한 보험료를 산정하고 있으며, 계약 협상에서 분석이 더욱 강화되고 있습니다. 이러한 제도화로 인해 웨어러블 단말기는 단순한 선택적 가젯에서 필수 인프라로 변모하고 있습니다.

AI 기반 멀티 센서 웨어러블의 통합이 진전되고 있습니다.

최신 장치는 관성 측정 장치, 광맥파 측정, 생체 임피던스, 멀티 밴드 GNSS를 단일 폼 팩터에 통합하고 있습니다. 2026년 2월 출시된 삼성 '갤럭시 워치7'은 클라우드 지연 없이 운동 강도를 분류하는 온디바이스 신경망을 탑재해 운동 중 데이터 유출에 대한 우려를 줄였습니다. 가민의 HRM-600 가슴 스트랩은 심전도(ECG) 수준의 심박수 모니터링과 접지 시간을 추적하는 러닝 다이내믹스 포드를 결합하여 임상 수준의 정확성을 원하는 지구력 운동 선수를 위한 제품입니다. 키넥슨이 유로리그에 도입한 시스템은 초광대역(UWB) 앵커를 이용해 선수 위치를 10cm 이내의 정확도로 삼각측량하고, 피로 지수를 벤치 코치에게 직접 전송합니다. 엣지 프로세싱은 세션 후 분석에 대한 의존도를 낮추고, 하프타임에 국한되었던 경기 중 전술 변경을 가능하게 합니다.

높은 초기 장치 비용과 제한된 스포츠 예산

Catapult와 STATSports의 엔터프라이즈급 키트는 팀당 5만 달러 이상이며, 연간 소프트웨어 비용도 1만-3만 달러에 달하고, 디비전 II와 III 대학 프로그램에 큰 부담으로 작용하고 있습니다. 레크리에이션 운동선수들은 기본적인 트래킹 기능을 제공하는 무료 스마트폰 앱이 있는 가운데, 지속적인 구독이 포함된 300-500달러짜리 기기에 난색을 표하고 있습니다. 이러한 양극화로 인해 프리미엄급 전문가층과 상품화된 소비자층이 생겨나면서 기능적 혁신의 원천이 될 수 있는 교차 서브시디케이션이 제한되고 있습니다.

부문 분석

2025년 피트니스 및 심박수 모니터는 스포츠 웨어러블 기기 시장 점유율의 38.21%를 차지해, 이는 레크리에이션 목적의 러너와 사이클리스트들 사이에서 확고하게 자리 잡은 사용 현황을 반영합니다. 스마트웨어와 전자섬유는 CAGR 6.93%를 나타낼 것으로 예측되며, 운동선수들이 개인 가젯을 휴대할 필요가 없는 웨어러블 기기로 전환함에 따라 전체 스포츠 웨어러블 기기 시장 규모 성장률보다 더 빠른 속도로 성장할 것으로 예측됩니다. 2025년 5월에 출시된 Garmin의 Forerunner 970은 멀티 밴드 GNSS를 채택하여 밀집된 도시 지역에서도 정확도를 유지합니다. 2024년 8월에 출시된 FORM의 'Smart Swim 2' 고글은 투명한 디스플레이에 실시간 측정값을 오버레이하여 수영 중 손목을 확인하는 인지적 방해 요소를 제거합니다.

PlayerMaker의 분데스리가와의 제휴를 계기로, 과거에는 실험실에서만 사용되던 볼 접촉의 질을 측정하는 양말용 센서가 대중화되기 시작했습니다. 2026년 1월 출시된 Garmin의 'Xero L60i'와 같은 헤드 마운트형 증강현실(AR) 디스플레이는 골프 비거리를 안경 렌즈에 투사하여 헤드업 인터페이스의 대중화를 예고하고 있습니다. FDA 승인을 받은 e-Celsius 캡슐과 같은 경구용 센서는 NFL 팀을 위해 체온을 추적하고 있지만, 비용과 선수들의 수용성이라는 장벽에 직면해 있습니다. 그래핀이 함유된 직물은 세탁기로 빨 수 있는 전도성을 약속하며, 예측 기간 동안 딱딱한 센서 하우징이 필요하지 않을 수 있습니다.

축구와 미식축구는 유럽 클럽들이 포지셔닝 최적화를 위해 GPS 트래킹을 표준화하면서 2025년 매출의 26.43%를 차지했습니다. 한편, 수영과 수영 경기는 2031년까지 연평균 복합 성장률(CAGR) 7.01%를 기록하며 스포츠 시장 규모 성장에 있어 웨어러블 기기 전체를 능가할 것으로 예측됩니다. Prevent Biometrics의 마우스 가드는 미식축구에서 머리에 가해지는 충격을 기록하여 법적 책임을 줄이기 위해 뇌진탕에 대한 노출 상황을 문서화합니다. 야구계에서는 Motus Global의 mThrow 2.0 팔꿈치용 슬리브를 활용하여 투수의 척측 측부인대 부하를 모니터링하고 있습니다.

크리켓에서는 ICC의 승인을 받아 도입이 가속화되고 있으며, 인도 대표팀은 볼러의 부하 관리를 위해 캐터펄트 장비를 도입하고 있습니다. 사이클링 및 트라이애슬론 선수들은 수영, 자전거, 달리기 모드를 전환할 수 있는 장치를 요구하고 있으며, Garmin은 'Forerunner 570'을 통해 이러한 요구에 부응했습니다. 익스트림 스포츠 참가자들은 내구성과 며칠간의 배터리 지속시간을 중요시하는데, 36시간 연속 사용과 수심 40m 방수 기능을 갖춘 애플의 'Watch Ultra 3'가 이에 대응하고 있습니다. 수영 부문의 급격한 성장은 범용 추적기보다 경기용 전문 솔루션으로의 광범위한 전환을 강조하고 있습니다.

지역별 분석

북미는 2025년 매출의 41.72%를 차지해, 리그의 머리 충격 및 투구 생체역학 모니터링 의무화가 이를 견인했습니다. 디비전 I 대학들은 NCAA의 건강 가이드라인을 충족하기 위해 7자리 숫자의 예산을 투자하고 있으며, 안정적인 기업 고객층을 형성하고 있습니다. 소비자의 높은 구매력은 프리미엄 가격대의 평균 판매 가격을 유지하여 벤더의 수익성 높은 생태계를 유지합니다.

아시아태평양은 CAGR 4.98%를 나타낼 것으로 예측됩니다. 이는 중국 정부가 지원하는 아카데미가 인재 발굴을 위해 웨어러블 단말기의 표준을 채택하고, 인도 크리켓 연맹이 GPS 추적을 표준화하고 있기 때문입니다. 일본에서는 고령화에 따라 낙상 위험을 추적하는 기기의 도입이 진행되고 있으며, 한국에서는 통신사가 통신 요금제와의 세트 판매를 통해 갤럭시 워치 모델 구매를 보조하고 있습니다. 이러한 요인들로 인해 대상 시장은 경기 선수를 넘어 확대되고 있습니다.

유럽에서는 엄격한 GDPR(EU 개인정보보호규정) 요건과 프로축구 리그의 스포츠 과학에 대한 적극적인 투자가 균형을 이루고 있습니다. 영국 및 아일랜드 라이온스의 2025 워크로드 스트리밍 이니셔티브는 컴플라이언스 비용을 상쇄할 수 있는 수익화 경로를 제시합니다. 중동 국가 정부는 경제 다각화를 위해 증강현실(AR) 분석에 대응하는 경기장에 투자하고 있습니다. 남미에서는 관세로 인한 물가 상승이 계속되고 있지만, 브라질의 클럽들은 유럽의 기준을 따라잡기 위해 GPS를 도입하고 있습니다. 아프리카에서의 보급은 이제 막 시작되었고, 남아공의 럭비나 케냐의 장거리 달리기 프로그램이 중심이 되고 있지만, 단말기 비용과 통신 환경의 격차로 인해 제약을 받고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The wearable devices in sports market size is expected to increase from USD 93.81 billion in 2025 to USD 98.06 billion in 2026 and reach USD 120.05 billion by 2031, growing at a CAGR of 4.13% over 2026-2031.

Professional leagues now embed biometric tracking in collective-bargaining agreements, while recreational users adopt AI-driven coaching that assigns real-time injury-risk scores. Sony's 2025 purchase of STATSports exemplifies a shift toward platform consolidation that marries sensor hardware with cloud analytics. Textile-integrated sensors that capture kinetic, thermal, and electrophysiological signals without restricting movement move the category beyond wristbands, supporting demand for garments that feel like ordinary sportswear. North American dominance rests on National Football League and Major League Baseball mandates for head-impact and pitch-biomechanics monitoring, yet Asia-Pacific posts faster growth as Indian cricket and Chinese academy programs institutionalize GPS tracking. Headline risks center on new data-privacy clauses in collective-bargaining agreements that restrict third-party sales of biometric data and slow product rollouts.

Global Wearable Devices In Sports Market Trends and Insights

Growing Demand for Data-Driven Performance Analytics

Teams now treat biometric metrics as contractual deliverables, embedding recovery scores in player-availability clauses. The Association of Tennis Professionals approved in-competition wearables in 2024, allowing real-time coaching adjustments that rely on exertion thresholds and court-coverage heat maps. Collegiate recruiters request multi-year datasets from prospects, creating a secondary market for longitudinal performance archives. The National Football League Players Association opened a centralized repository in 2024 so athletes can license anonymized data to researchers while retaining veto rights over commercial use. Insurers also price injury risk off historical wearable trends, further embedding analytics in contract negotiations. This institutionalization transforms wearables from optional gadgets into required infrastructure.

Rising Integration of AI-Powered Multi-Sensor Wearables

Modern devices fuse inertial measurement units, photoplethysmography, bioimpedance, and multi-band GNSS into single form factors. Samsung's Galaxy Watch7, released in February 2026, houses on-device neural networks that classify workout intensity without cloud latency, mitigating data-leakage fears during live competition. Garmin's HRM-600 chest strap pairs ECG-grade heart monitoring with running-dynamics pods that track ground-contact time for endurance athletes demanding clinical-level precision. Kinexon's EuroLeague deployment uses ultra-wideband anchors to triangulate player positions within 10 cm, feeding fatigue indices directly to bench coaches. Edge processing lowers dependence on post-session analysis, enabling in-game tactical pivots once confined to halftime.

High Initial Device Cost and Tight Athletics Budgets

Enterprise-grade kits from Catapult or STATSports cost more than USD 50,000 per team, with annual software fees of USD 10,000-30,000, squeezing Division II and III college programs. Recreational athletes balk at USD 300-500 devices bundled with ongoing subscriptions when free smartphone apps deliver basic tracking. This bifurcation creates premium professional tiers and commoditized consumer segments, limiting cross-subsidization that could fund feature innovation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Global Sports Events and Fan-Engagement Platforms

- Portable and Convenient Form Factors Boosting Daily Adoption

- Escalating Consumer Data-Privacy and Security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, fitness and heart-rate monitors commanded 38.21% of wearable devices in sports market share, reflecting entrenched adoption among recreational runners and cyclists. Smart clothing and e-textiles are projected to grow at a 6.93% CAGR, outpacing the overall wearable devices in sports market size growth as athletes shift toward garments that eliminate the need to remember separate gadgets. Garmin's Forerunner 970, launched in May 2025, uses multi-band GNSS to retain accuracy in dense urban terrain. FORM's Smart Swim 2 goggles, released in August 2024, overlay live metrics onto transparent displays, removing the cognitive disruption of mid-stroke wrist checks.

Footwear sensors gained traction after PlayerMaker's Bundesliga partnership, measuring ball-contact quality that was once laboratory-bound. Head-mounted augmented-reality displays, such as Garmin's Xero L60i introduced in January 2026, project golf yardage onto eyewear lenses, hinting at wider acceptance of heads-up interfaces. Ingestible sensors like the FDA-cleared e-Celsius capsule track core temperature for NFL teams but face cost and athlete-acceptance barriers. Graphene-infused fabrics promise machine-washable conductivity, potentially rendering rigid sensor housings obsolete during the forecast horizon

Soccer and football held 26.43% of 2025 revenue as European clubs normalized GPS tracking for positional play optimization. Swimming and aquatics, however, will surpass overall wearable devices in sports market size growth, posting a 7.01% CAGR through 2031. Prevent Biometrics' mouthguard logs American-football head impacts to document concussion exposure for liability mitigation. Baseball leverages Motus Global's mThrow 2.0 elbow sleeve to monitor ulnar-collateral-ligament stress in pitchers.

Cricket adoption accelerated after ICC approvals, with India's national team deploying Catapult units for bowler workload management. Cycling and triathlon athletes demand devices that transition through swim, bike, and run modes, a gap Garmin filled with the Forerunner 570. Extreme-sports participants value ruggedness and multi-day battery life, met by Apple's Watch Ultra 3 rated for 36-hour runtime and 40-m depth. The aquatics surge underscores a wider pivot toward discipline-specific solutions over generic trackers.

The Wearable Devices in Sports Market Report is Segmented by Device Type (Fitness and Heart-Rate Monitors, Smart Clothing and E-Textiles, and More), Sport (Soccer / Football, Basketball, and More), End User(Professional Teams and Leagues, and More), Distribution Channel (Online, Specialty Sports Stores, Mass-Retail and Electronics Chains, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.72% revenue in 2025, powered by league mandates for head-impact and pitch-biomechanics monitoring. Division I universities dedicate seven-figure budgets to satisfy NCAA health guidelines, providing a captive enterprise clientele. High consumer purchasing power sustains premium average selling prices and supports a profitable ecosystem for vendors.

Asia-Pacific will grow at 4.98% CAGR as China's government-backed academies use wearable benchmarks for talent identification and India's cricket federation normalizes GPS tracking. Japan's aging population adopts devices to track fall risk, while South Korean carriers subsidize Galaxy Watch models through connectivity bundles. These factors simultaneously expand the addressable base beyond competitive athletes.

Europe balances stringent GDPR requirements with strong sports-science investments by professional football leagues. The British and Irish Lions' 2025 workload-streaming initiative illustrates monetization paths that offset compliance costs. Middle Eastern governments invest in stadiums wired for augmented-reality analytics to diversify economies. South America endures tariff-driven price inflation, though Brazilian clubs adopt GPS to keep pace with European standards. African uptake is nascent, anchored in South African rugby and Kenyan distance-running programs but constrained by device costs and connectivity gaps.

- Kinexon GmbH

- Garmin Ltd.

- Sensoria Inc.

- Zepp Health Corporation

- Catapult Group International Ltd.

- Samsung Electronics Co., Ltd.

- Alphabet Inc. (Google LLC / Fitbit LLC)

- STATSports Group Ltd.

- Whoop, Inc.

- Polar Electro Oy

- Carre Technologies Inc. (Hexoskin)

- Zephyr Technology Corporation

- Firstbeat Technologies Oy

- Apple Inc.

- Playermaker Ltd.

- Motus Global LLC

- X2 Biosystems, Inc.

- Nix, Inc.

- hDrop Technologies, Inc.

- Adidas AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Data-Driven Performance Analytics

- 4.2.2 Rising Integration of AI-Powered Multi-Sensor Wearables

- 4.2.3 Expansion of Global Sports Events and Fan-Engagement Platforms

- 4.2.4 Portable and Convenient Form-Factors Boosting Daily Adoption

- 4.2.5 League-Sanctioned Biometric-Data Monetization Frameworks

- 4.2.6 Textile-Integrated Multimodal Sensors for Injury Prevention

- 4.3 Market Restraints

- 4.3.1 High Initial Device Cost and Tight Athletics Budgets

- 4.3.2 Escalating Consumer Data-Privacy and Security Concerns

- 4.3.3 Interoperability Gaps Across Vendor Data Ecosystems

- 4.3.4 Collective-Bargaining Limits on Biometric Data Use

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Fitness and Heart-Rate Monitors

- 5.1.2 Smart Clothing and E-Textiles

- 5.1.3 GPS / GNSS Trackers

- 5.1.4 Camera-Based and Vision Wearables

- 5.1.5 Footwear and In-Shoe Sensors

- 5.1.6 Head-Mounted and AR Displays

- 5.1.7 Ingestible and Other Emerging Sensors

- 5.2 By Sport

- 5.2.1 Soccer / Football

- 5.2.2 Basketball

- 5.2.3 American Football and Rugby

- 5.2.4 Baseball / Softball

- 5.2.5 Cricket

- 5.2.6 Golf and Tennis

- 5.2.7 Cycling and Triathlon

- 5.2.8 Swimming and Aquatics

- 5.2.9 Extreme and Adventure Sports

- 5.3 By End User

- 5.3.1 Professional Teams and Leagues

- 5.3.2 Collegiate / University Programs

- 5.3.3 Amateur and Club Athletes

- 5.3.4 Recreational Fitness Enthusiasts

- 5.3.5 Sports Academies and Training Centers

- 5.3.6 Medical and Rehab Facilities

- 5.4 By Distribution Channel

- 5.4.1 Online (Direct and Marketplaces)

- 5.4.2 Specialty Sports Stores

- 5.4.3 Mass-Retail and Electronics Chains

- 5.4.4 Team / Enterprise Contracts

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kinexon GmbH

- 6.4.2 Garmin Ltd.

- 6.4.3 Sensoria Inc.

- 6.4.4 Zepp Health Corporation

- 6.4.5 Catapult Group International Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Alphabet Inc. (Google LLC / Fitbit LLC)

- 6.4.8 STATSports Group Ltd.

- 6.4.9 Whoop, Inc.

- 6.4.10 Polar Electro Oy

- 6.4.11 Carre Technologies Inc. (Hexoskin)

- 6.4.12 Zephyr Technology Corporation

- 6.4.13 Firstbeat Technologies Oy

- 6.4.14 Apple Inc.

- 6.4.15 Playermaker Ltd.

- 6.4.16 Motus Global LLC

- 6.4.17 X2 Biosystems, Inc.

- 6.4.18 Nix, Inc.

- 6.4.19 hDrop Technologies, Inc.

- 6.4.20 Adidas AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment