|

시장보고서

상품코드

2044155

어뢰 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Torpedo - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

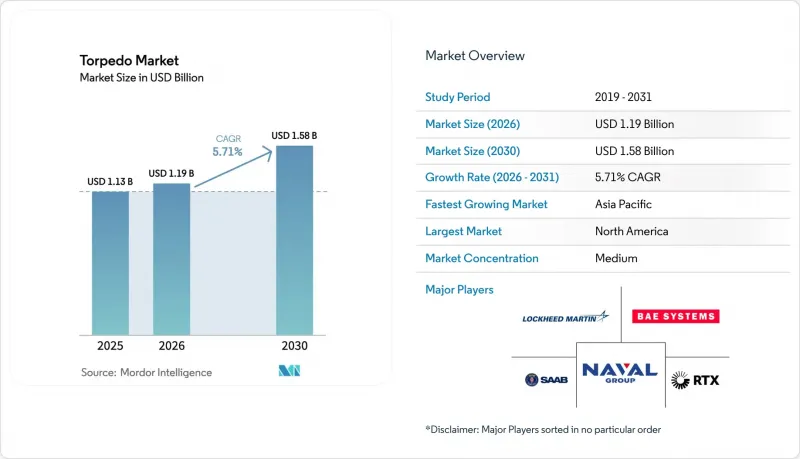

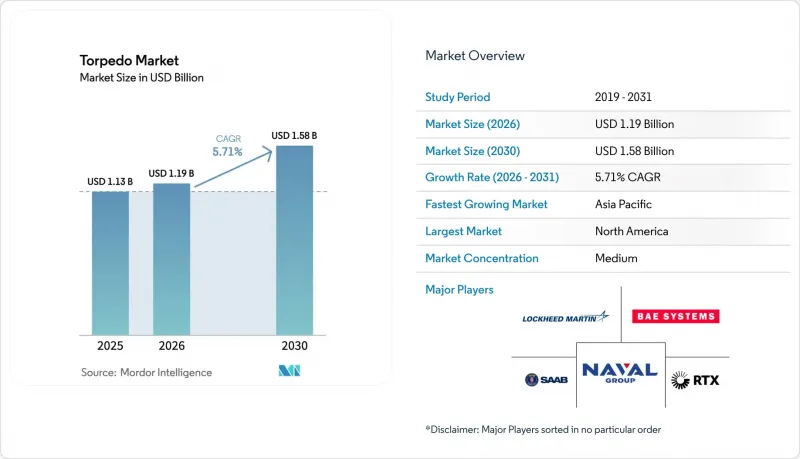

어뢰 시장 규모는 2025년 11억 3,000만 달러에서 2026년에는 11억 9,000만 달러로 확대되어 2026-2031년까지 CAGR 5.71%로 성장을 지속하여, 2031년까지 15억 8,000만 달러에 이를 것으로 예측됩니다.

최근 수요는 더 많은 원자력 및 디젤 전기 잠수함이 취역하고 있으며, 해저 위협을 막기 위해 현대화 프로그램을 통해 장비, 유도 시스템, 추진 시스템 업그레이드가 진행되고 있습니다. P-8A 포세이돈과 MH-60R의 플랫폼 통합으로 항공기의 대잠전(ASW) 커버리지가 확대되고 있으며, 고고도 어뢰 투하 키트를 통해 분쟁 지역 상공에서의 저항력도 강화되고 있습니다. 대형 시스템은 여전히 외양함대 억지력의 기반이 되고 있지만, 비용, 탑재량, 탄약고 용량 측면에서 우위를 점하고 있는 무인 플랫폼에 탑재되는 초경량급 어뢰는 더욱 빠르게 확대되고 있습니다. 중국, 인도, 일본, 한국, 대만에서 국내 어뢰 개발 계획과 잠수함 증강이 맞물려 아시아태평양이 미래 성장을 뒷받침하고 있습니다.

세계 어뢰 시장 동향과 인사이트

세계 원자력 및 디젤 전기 잠수함 도입 가속화

해군이 지역 위협 환경과 순찰 프로파일에 대응하기 위해 새로운 원자력 및 디젤 전기 플랫폼을 배치함에 따라 잠수함 획득이 여러 유형의 어뢰 수요의 주요 원동력이 되고 있습니다. 아시아태평양의 생산 속도는 여전히 높은 수준이며, 중국 조선소는 최근 몇 년 동안 미국을 능가하는 생산량을 유지하고 있으며, 장거리 및 고속 교전 프로파일에 적합한 중량급 어뢰의 재고 확보에 대한 필요성이 증가하고 있습니다. AUKUS는 호주가 2030년대 초경 버지니아급 SSN 획득을 준비하고 있어 지속적인 미래 수요를 가져오고 있으며, 이를 통해 대형 어뢰 계획과 동맹국 간 상호운용성에 활용한 10년 이상의 준비기간을 확보할 수 있게 되었습니다. 인도의 프로젝트 75와 병행하는 국산 프로그램은 구축함과 잠수함 부대 전체에 걸쳐 바르나스트라급 대형 어뢰에 지속적인 탑재를 가능하게 하고, 국산 부품의 비율과 수명주기 관리를 강화하고 있습니다. 유럽 함대는 배치중인 장비를 업그레이드하고 있으며, 독일은 212CD급 프로그램을 위해 DM2A5를 추진하여 차세대 유도 및 동력 모듈을 확보하려고 노력하고 있습니다. 브라질의 스코페네급 F21의 통합은 신흥 해군 강국의 장기적인 어뢰 결정에 있어 기술 이전과 현지 유지관리가 얼마나 중요한 요소인지 잘 보여주고 있습니다.

주요 해양 강국의 해군 함대 현대화의 지속적 추진

지속적인 현대화 예산으로 수상 함대와 잠수함 함대의 대형 및 소형 어뢰 재고를 갱신하고 있으며, 다년간의 키트 생산으로 안정적인 납품 일정을 유지하고 있습니다. 미 해군은 제너럴 다이내믹 미션 시스템즈(General Dynamics Mission Systems)와 Mk 54 Mod 1 경량 어뢰 키트 계약을 체결하고 2032년까지 납품할 예정이며, 이를 통해 동맹국 함대의 포세이돈, 시호크, 수상함에 통합할 수 있도록 지원할 예정입니다. 영국의 'Stingray Mod 2' 업그레이드 프로그램은 설계, 시제품 제작 및 수상 검사에 자금을 지원하여 최전방 플랫폼에 사이버 공격에 대한 내성을 강화한 아키텍처와 신속한 재프로그래밍 능력을 제공합니다. 걸프 지역에서는 사우디아라비아의 MU90 발주가 현지 유지관리 체제를 강화하는 동시에 유로토프사의 동 지역 사업 범위를 확장하고 있습니다. 스웨덴의 'Torpedo 47' 조달 계획은 연안 작전 및 얕은 해역의 음향 환경에 대응하며, 발트해에서 장기간 순찰 임무를 수행하도록 설계된 미래형 A26형 함정과 결합될 예정입니다. 튀르키예의 TF-2000 구축함 계획과 국산 잠수함 시리즈는 국산 'Akya' 중어뢰와 첨단 함상 발사 시스템을 결합한 하이브리드형 접근 방식을 강화하는 것입니다.

중량급 어뢰의 높은 단가로 국방 조달 예산 압박을 받고 있습니다.

첨단형 등 고성능 중어뢰는 수백만 달러 규모의 단독 투자가 필요하며, 조선, 미사일 비축, 센서 세트와 예산 경쟁을 유발합니다. 이로 인해 급증하는 조달 수요와 다지역 대응 사이클에서 예산 압박이 발생하여 구매 계획이 연기되거나 경량 어뢰에 대한 의존도가 높아지는 혼합 재고 체제로 이어질 수 있습니다. 미 해군이 검토 중인 저비용화 중어뢰는 핵심 살상 능력과 유도 기능을 손상시키지 않으면서 장기화되는 불의의 사태에 대비한 비축량을 회복하는 것을 목표로 하고 있습니다. 비용 절감은 하이엔드 분쟁의 소모에 대한 대비이기도 합니다. 저렴한 가격의 무기가 있으면 단기간의 고강도 소모전이 아닌 지속적인 작전이 가능하기 때문입니다. 경제성에 초점을 맞춘 노력은 모듈식 아키텍처를 촉진할 수 있습니다. 이를 통해 해군은 추진체계나 탄두 부분과 독립적으로 센서와 처리장치를 업그레이드할 수 있게 되어 장기적으로 어뢰 시장을 뒷받침할 수 있을 것입니다.

부문 분석

2025년 대형 어뢰는 어뢰 시장 점유율의 54.72%를 차지했습니다. 수요는 외해와 연안 수역 모두에서 정숙성이 높은 적에 대한 장거리 및 신속한 종말단계 성능을 필요로 하는 잠수함 계획에 의해 수요가 견인되고 있으며, 안정적인 수주와 중간 수명 개조가 유지되고 있습니다. 미 해군의 조선 전망은 공격형 잠수함 및 동맹국 함대에 대한 지속적인 수요를 뒷받침하고 있으며, 유도, 제어 및 추진 부문의 다년간의 생산 계획을 강화하고 있습니다. 록히드마틴의 최근 납품 및 계약 변경으로 미군과 호주군 전체 중량급 어뢰 재고를 위한 유도 및 제어 키트의 대량 생산이 유지되고 있으며, 지속적인 유지 관리의 길을 제시하고 있습니다.

초경량 어뢰는 가장 빠르게 성장하는 카테고리로 2031년 CAGR이 8.21%를 나타낼 것입니다. 이는 무인 시스템, 해안 봉쇄, 탄약고 깊이의 혁신이 분산형 해상 작전을 위한 탑재 무기 구성을 재구성하고 있기 때문입니다. 소형 어뢰급 페이로드를 탑재하는 새로운 소프트웨어 정의형 잠수정은 중어뢰의 기준 비용보다 훨씬 낮은 비용으로 UUV(무인잠수정)와 USV(무인수상정)에 대한 선택의 폭을 넓혀 포화 전술에 대한 확장 가능한 재고 체제를 뒷받침하고 있습니다. 초경량 부문의 성장은 기존 인터페이스에 다연장 소형 무기를 탑재하는 잠수함과 수상함의 탄약고 전략과 일치하며, 무리를 짓는 위협에 대한 다층적 방어 체제를 구축하고 있습니다. 튀르키예의 'ORKA' 경량급은 현대식 추진 시스템과 해안 전투에 적합한 무감각 탄두 설계로 헬리콥터와 UAV의 탑재 옵션을 확장하고 있습니다. 발트해의 특수한 요구는 스웨덴의 'Torpedo 47'이 얕은 해역의 음향 특성과 소형 플랫폼의 설치 면적을 중시하는 스웨덴의 'Torpedo 47'이 대응하고 있으며, 이는 지역적 요인이 어뢰 산업에서 부문 채택에 영향을 미치는 방식을 반영합니다.

2025년에는 해상 발사형 시스템이 62.67%의 압도적인 시장 점유율을 차지했습니다. 한편, 항공기 발사형 플랫폼은 2031년까지 7.83%의 괄목할만한 CAGR을 달성할 것으로 예측됩니다. 이러한 성장은 유인 항공기에 대한 위험을 최소화하면서 교전 능력을 확대하려는 해군에 의해 주도되고 있습니다. 이 급격한 증가는 P-8A 포세이돈 함대에 글라이드 키트를 통합하여 고고도에서의 발사가 가능해졌기 때문입니다. 이러한 전략은 분쟁 지역 상공에서의 생존성을 높일 뿐만 아니라 순찰 기간도 연장할 수 있습니다.

또한, 동맹국 군는 통일된 훈련과 정비를 위해 장비의 표준화를 추진하고 있습니다. 스텔스성을 중시하는 선제공격형 대잠전(ASW)에서는 잠수함 주도 수요가 여전히 매우 중요하지만, 수상함이나 무인자산에서도 함대 호위 및 연안지역 진입 차단을 목적으로 어뢰의 사용이 증가하고 있습니다. 무인 차량용 혁신적인 탄약고 개념과 회수 기술은 잠수함의 위치를 노출하지 않고도 해군의 존재감과 공격 능력을 강화할 수 있는 방법을 보여주고 있습니다.

항공기 발사형 시스템은 복잡한 연안 수역의 음향 환경에서 더 조용하고 기동성이 높은 목표물에 대한 효율성을 높이는 경량화 개선으로 성장하고 있습니다. Mk 54 Mod 2 프로그램은 헬리콥터와 고정익 항공기 부대를 포함한 광범위한 어뢰 시장에 혜택을 줄 수 있는 살상 능력과 신호 처리 업그레이드를 도입했습니다. 노르웨이의 대외 군사 판매는 어뢰를 포세이돈, 시호크, 수상함정과 통합하여 북대서양과 북극권에서의 상호 운용성을 강화하고 있습니다. NH90 시타이거의 출시와 새로운 무인 회전익 항공기의 개념에서 알 수 있듯이, 플랫폼의 다양성은 확대되고 있습니다. 이러한 혁신적 기술을 통해 위협이 높은 지역에서도 승무원의 안전을 해치지 않고 경량화 된 탑재물을 수송할 수 있게 되어 어뢰 시장에서 해상 발사 시스템의 우위를 더욱 공고히 할 수 있게 되었습니다.

지역별 분석

북미는 2025년 어뢰 시장 점유율의 34.71%를 차지해, 미국의 꾸준한 조달과 납기 준수를 뒷받침하는 탄탄한 공급업체 기반이 뒷받침하고 있습니다. 2032년까지 미 해군의 경량화 키트 생산과 정기적인 중량급 부품 납품은 주요 계약업체와 서브시스템 공급업체에 대한 일관된 수요의 신호로 작용하고 있습니다. 산업 인프라 프로그램에서는 병목현상을 해소하고 주요 노드에서 예측가능성을 높이기 위한 투자를 통해 2025년까지 공급업체들의 성과가 개선된 것으로 보고되고 있습니다. 추가 계약은 추진 검사 시설과 크로스 도메인 수중 시스템을 지원하며, 이를 통해 중량급 및 경량급 무기의 장기적인 생산을 강화하고 어뢰 시장에서의 즉각적인 대응력을 뒷받침하고 있습니다.

아시아태평양은 자급자족 노력, 잠수함 함대 확장, 중량급 및 경량급 채용 확대에 힘입어 2031년까지 연평균 7.77%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 아시아태평양 어뢰 시장 규모는 동맹국 및 파트너 국가의 해군이 리드타임 단축과 가용성 향상을 위해 국산 프로그램과 선택적 수입의 균형을 맞추면서 가속화될 것으로 예측됩니다. 중국의 급속한 생산 확대, 인도의 전략적 취역, 일본의 수중 공격 태세와 맞물려 예측 기간 동안 유도, 추진, 탄두 업그레이드에 대한 수요가 증가할 것으로 예측됩니다.

유럽에서는 2031년까지 완만한 성장이 예상되며, 현대화 사이클에서 국내 주요 기업 및 합작회사를 활용하여 재고를 갱신하고 차세대 기능을 통합하고 있습니다. 영국은 2030년대에도 항공기 탑재형과 함정 탑재형 대잠전 능력을 유지하기 위해 스팅레이의 고도 업그레이드를 추진했습니다. 프랑스는 동맹국과의 통합을 지원하는 실탄 사격 훈련에서 F21의 살상 능력을 입증했고, 독일은 212CD형 잠수함용 DM2A5를 개발했습니다. 중동 및 아프리카의 성장은 사우디아라비아의 MU90 계획이 뒷받침하고 있으며, 이는 어뢰 시장의 장기적인 유지관리에 물류 및 현지 서비스 역량을 추가할 것입니다. 남미는 점유율의 4%를 차지하고 있으며, 현재 진행 중인 스코펜급 잠수함과의 통합은 기술 이전과 현지 훈련이 지속적인 역량을 뒷받침하고 있음을 보여줍니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The torpedo market size is expected to grow from USD 1.13 billion in 2025 to USD 1.19 billion in 2026 and is forecasted to reach USD 1.58 billion by 2031 at a 5.71% CAGR over 2026-2031.

Recent demand is shaped by more nuclear and diesel-electric submarines entering service, with modernization programs aligning inventory, guidance, and propulsion upgrades to deter undersea threats. Platform integration across P-8A Poseidon and MH-60R fleets is broadening airborne anti-submarine warfare coverage and is adding resilience in contested airspace through high-altitude torpedo release kits. Heavyweight systems continue to anchor deterrence for blue-water fleets, yet very-light classes tied to unmanned platforms are expanding faster, driven by cost, payload, and magazine depth advantages. Asia-Pacific underpins future growth as domestic torpedo programs and submarine expansion converge across China, India, Japan, South Korea, and Taiwan.

Global Torpedo Market Trends and Insights

Accelerated Induction of Nuclear and Diesel-Electric Submarines Worldwide

Submarine acquisition is the prime engine of multi-class torpedo demand, as navies field new nuclear and diesel-electric platforms to match regional threat environments and patrol profiles. Production pace in Asia-Pacific remains elevated, with Chinese yards sustaining output that surpassed the United States in recent years, reinforcing the need for heavyweight inventories matched to long-range, high-speed engagement profiles. AUKUS adds a durable forward pipeline as Australia prepares to acquire Virginia-class SSNs around the early 2030s, which sets a decade-plus runway for heavyweight torpedo planning and allied interoperability. India's Project-75 lines and parallel indigenous programs sustain recurring fits for Varunastra-class heavyweights across destroyer and submarine fleets, amplifying domestic content and lifecycle control. European fleets are upgrading deployed inventories, with Germany advancing DM2A5 for 212CD-class programs to lock in next-generation guidance and power modules. Brazil's Scorpene-class integration of F21 underscores how technology transfer and local sustainment factor into long-term torpedo decisions among emerging naval powers.

Ongoing Naval Fleet Modernization Across Key Maritime Powers

Sustained modernization budgets are refreshing both heavyweight and lightweight inventories across surface and sub-surface fleets, with multi-year kit production keeping delivery schedules stable. The US Navy awarded General Dynamics Mission Systems a contract for Mk 54 Mod 1 lightweight torpedo kits with deliveries through 2032, supporting Poseidon, Seahawk, and surface-ship integrations across allied fleets. The UK's Sting Ray Mod 2 upgrade program funds design, prototyping, and in-water trials to deliver cyber-hardened architectures and rapid reprogramming capabilities to frontline platforms. In the Gulf, Saudi Arabia's MU90 order strengthens local sustainment pathways while widening EuroTorp's reach across the region. Sweden's Torpedo 47 procurement aligns with littoral operations and shallow-water acoustics, pairing with future A26 boats designed for high-endurance Baltic patrols. Turkey's TF-2000 destroyer program and national submarine lines bolster a blended approach that includes indigenous Akya heavyweights paired with advanced shipboard launch systems.

High Unit Costs of Heavyweight Torpedoes Strain Defense Procurement Budgets

Premium heavyweights, including advanced variants, require multi-million-dollar unit investments that compete with shipbuilding, missile stocks, and sensor suites. This creates budget pressure during surge procurement or multi-theater readiness cycles, which can lead to deferred buy profiles or mixed inventories that rely more on lightweight stocks. The US Navy's exploration of cost-reduced heavyweights aims to restore magazine depth for protracted contingencies without eroding core lethality and guidance features. Cost compression is also a hedge against attrition in high-end conflict, where affordable weapons enable sustained operations rather than short, high-intensity expenditures. Initiatives focused on affordability can catalyze modular architecture that allows navies to upgrade sensors and processing independently of propulsion or warhead sections, supporting the torpedo market in the long term.

Other drivers and restraints analyzed in the detailed report include:

- Increased Utilization of Lightweight Torpedoes in Airborne ASW Platforms

- Rising Strategic Need for Sub-Surface Deterrence in Geopolitically Contested Waters

- Extended Platform Integration and Qualification Timelines Delay Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heavyweight torpedoes commanded 54.72% of the torpedo market share in 2025. Demand is driven by submarine programs requiring long-range, rapid terminal performance against quiet adversaries in both blue-water and littoral zones, sustaining steady orders and midlife upgrades. The US Navy's shipbuilding outlook supports recurring loads for attack submarines and allied fleets, reinforcing multi-year production planning for guidance, control, and propulsion sections. Lockheed Martin's recent deliveries and contract modifications maintain guidance and control kits in serial production for heavyweight inventories across US and Australian forces, signaling durable sustainment pathways.

Very-light torpedoes are the fastest-growing category, with an 8.21% CAGR through 2031, as unmanned systems, coastal denial, and magazine-depth innovations reshape payload mixes for distributed maritime operations. New software-defined underwater vehicles carrying small torpedo-class payloads are expanding counter-UUV and counter-USV options at costs far below heavyweight baselines, supporting scalable inventories for saturation tactics. Growth within the very-light segment aligns with submarine and surface magazine strategies that pack multi-pack compact weapons into existing interfaces, building layered defenses against swarming threats. Turkey's ORKA lightweight class extends helicopter and UAV payload options with modern propulsion and an insensitive warhead design suited for littoral engagements. Baltic-specific needs are addressed through Sweden's Torpedo 47, which targets shallow-water acoustics and compact platform footprints, reflecting how geography shapes segment adoption in the torpedo industry.

Sea-launched systems commanded a dominant 62.67% market share in 2025. Meanwhile, air-launched platforms are on track to achieve a notable 7.83% CAGR through 2031. This growth is driven by navies seeking to extend their engagement capabilities while minimizing risks to crewed aircraft. This surge is attributed to the P-8A Poseidon fleet's integration of glide kits, allowing for high-altitude releases. Such a strategy not only boosts survivability in contested airspaces but also enhances patrol endurance.

Furthermore, allied forces are standardizing their inventories for unified training and maintenance. While submarine-led demand remains pivotal for stealthy first-strike ASW, surface and unmanned assets are increasingly using torpedoes for convoy protection and to deny access to littoral zones. Innovative magazine concepts and recovery techniques for unmanned vehicles highlight how navies can amplify their presence and strike capabilities without revealing submarine locations.

Air-launched systems are witnessing growth, bolstered by lightweight enhancements that boost effectiveness against quieter, more agile targets in intricate littoral acoustics. The Mk 54 Mod 2 program introduces lethality and signal-processing upgrades, benefiting the broader torpedo market across both helicopter and fixed-wing fleets. Norway's foreign military sale integrates torpedoes with Poseidon, Seahawk, and surface vessels, bolstering interoperability in the North Atlantic and Arctic regions. The diversity of platforms is expanding, as evidenced by NH90 Sea Tiger deployments and emerging unmanned rotorcraft concepts. These innovations can transport lightweight payloads without jeopardizing aircrew safety in high-threat areas, further solidifying sea-launched systems' dominance in the torpedo market.

The Torpedo Market Report is Segmented by Weight (Heavy, Light, and Very Light), Launch Platform (Sea and Air), Propulsion Type (Electric and Conventional), Guidance System (Wire-Guided, Acoustic, and Optical), Application (Anti-Submarine Warfare and Anti-Surface Warfare), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 34.71% of the torpedo market share in 2025, supported by steady US procurement and a strong supplier base that sustains on-time delivery. The US Navy's lightweight kit production through 2032 and recurring heavyweight component deliveries form a consistent demand signal for prime contractors and subsystem providers. Industrial base programs reported improved supplier performance by 2025, with targeted investments to alleviate bottlenecks and boost predictability across key nodes. Additional awards support propulsion test facilities and cross-domain undersea systems, which enhance the long-term production of heavyweight and lightweight weapons and support readiness in the torpedo market.

Asia-Pacific is the fastest-growing region with a 7.77% CAGR through 2031, underpinned by self-sufficiency drives, expanding submarine fleets, and widening adoption of both heavyweight and lightweight classes. The torpedo market size in Asia-Pacific is projected to accelerate as allied and partner navies balance indigenous programs with selective imports to reduce lead times and enhance availability. China's rapid output, India's strategic commissioning milestones, and Japan's undersea strike posture combine to elevate requirements for guidance, propulsion, and warhead upgrades through the forecast period.

Europe is expected to showcase moderate growth through 2031, with modernization cycles leveraging domestic primes and joint ventures to refresh inventories and integrate next-generation features. The UK advanced Sting Ray upgrades to keep airborne and shipborne ASW relevant into the 2030s, France validated F21 lethality in a live-fire event supporting allied integration, and Germany progressed DM2A5 for 212CD submarines. The Middle East and African growth is anchored by Saudi Arabia's MU90 pathway, which adds logistics and local service capabilities to long-term sustainment in the torpedo market. South America accounted for 4% of the share, with ongoing Scorpene-class integration demonstrating that technology transfer and local training support enduring capability.

- ATLAS ELEKTRONIK GmbH

- BAE Systems plc

- Bharat Dynamics Ltd.

- General Dynamics Mission Systems (General Dynamics Corporation)

- RTX Corporation

- Saab AB

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Naval Group

- Mitsubishi Heavy Industries, Ltd.

- ASELSAN A.S.

- LIG Nex1 Co., Ltd.

- Roketsan A.S.

- Science Applications International Corporation

- Fincantieri S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated induction of nuclear and diesel-electric submarines worldwide

- 4.2.2 Ongoing naval fleet modernization across key maritime powers

- 4.2.3 Increased utilization of lightweight torpedoes in airborne ASW platforms

- 4.2.4 Rising strategic need for sub-surface deterrence in geopolitically contested waters

- 4.2.5 Emerging demand for micro and ultra-lightweight torpedoes for unmanned maritime systems

- 4.2.6 Closed-loop manufacturing models enabled by high silver content recovery

- 4.3 Market Restraints

- 4.3.1 High unit costs of heavyweight torpedoes strain defense procurement budgets

- 4.3.2 Extended platform integration and qualification timelines delay deployment

- 4.3.3 Price instability and supply risks associated with critical minerals like silver and rare-earths

- 4.3.4 Increasing preference for long-range anti-ship missiles reduces demand for torpedoes in surface warfare

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Weight

- 5.1.1 Heavy

- 5.1.2 Light

- 5.1.3 Very Light

- 5.2 By Launch Platform

- 5.2.1 Sea

- 5.2.1.1 Surface Vessel

- 5.2.1.2 Submarine

- 5.2.1.3 Unmanned Underwater Vehicles (UUVs)

- 5.2.2 Air

- 5.2.2.1 Aircraft

- 5.2.2.2 Helicopters

- 5.2.2.3 Unmanned Aerial Vehicles (UAVs)

- 5.2.1 Sea

- 5.3 By Propulsion Type

- 5.3.1 Electric

- 5.3.2 Conventional

- 5.4 By Guidance System

- 5.4.1 Wire-Guided

- 5.4.2 Acoustic

- 5.4.3 Optical

- 5.5 By Application

- 5.5.1 Anti-Submarine Warfare (ASW)

- 5.5.2 Anti-Surface Warfare (ASuW)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ATLAS ELEKTRONIK GmbH

- 6.4.2 BAE Systems plc

- 6.4.3 Bharat Dynamics Ltd.

- 6.4.4 General Dynamics Mission Systems (General Dynamics Corporation)

- 6.4.5 RTX Corporation

- 6.4.6 Saab AB

- 6.4.7 Lockheed Martin Corporation

- 6.4.8 Northrop Grumman Corporation

- 6.4.9 Naval Group

- 6.4.10 Mitsubishi Heavy Industries, Ltd.

- 6.4.11 ASELSAN A.S.

- 6.4.12 LIG Nex1 Co., Ltd.

- 6.4.13 Roketsan A.S.

- 6.4.14 Science Applications International Corporation

- 6.4.15 Fincantieri S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment