|

시장보고서

상품코드

2044157

데이터 사이언스 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Data Science Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

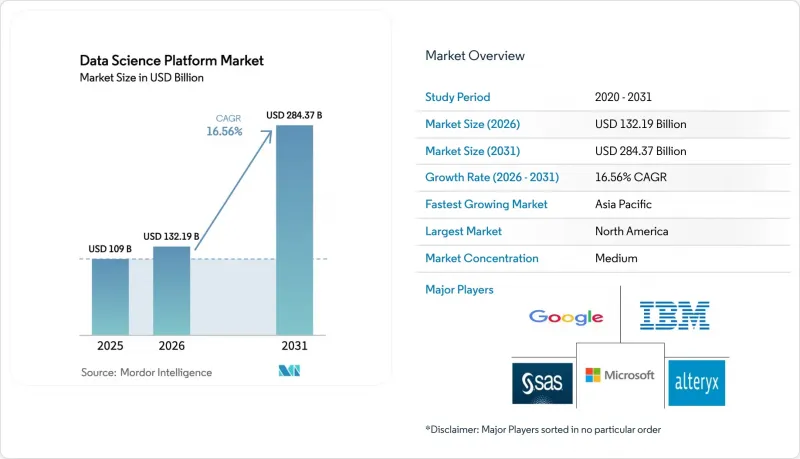

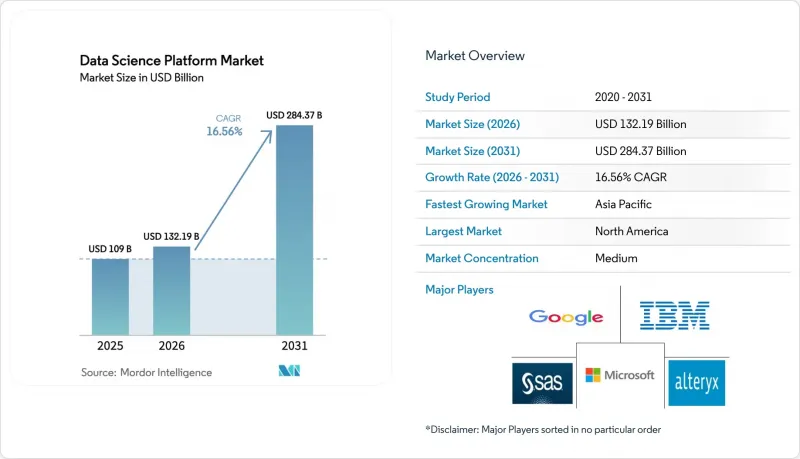

데이터 사이언스 플랫폼 시장 규모는 2025년 1,090억 달러로 평가되었습니다. 2026년 1,321억 9,000만 달러로 확대되어 2031년까지 2,843억 7,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 16.56%를 나타낼 전망입니다.

기업들이 고립된 머신러닝 파일럿 프로젝트에서 데이터 수집, 모델 훈련, 거버넌스, 엣지 추론을 통합한 프로덕션 시스템으로 전환함에 따라 꾸준한 성장세를 보이고 있습니다. 통합된 툴체인은 가치 실현 시간을 단축할 것으로 기대되는 반면, 하이퍼스케일러는 기존 클라우드 계약에 고급 기능을 통합하여 틈새 업체의 수익률을 압박하고 있습니다. 한편, 특정 분야를 위한 기반 모델이 의료 및 금융 분야의 이용 사례를 재정의하고 있으며, 국가 주도의 AI 프로그램을 통해 수십억 달러가 지역 데이터센터와 GPU 클러스터에 투입되고 있습니다. 현재 경쟁 우위는 원활한 거버넌스, 피처스토어의 성능, 그리고 대규모 RAG(Retrievable Augmented Generation) 워크로드를 처리할 수 있는 능력에 달려 있습니다.

세계의 데이터 사이언스 플랫폼 시장 동향과 인사이트

오픈소스 ML 프레임워크의 보급으로 플랫폼 통합 촉진

오픈소스 라이브러리는 AI 워크로드의 87%를 지원하며, 2024년 대비 8% 포인트 증가했습니다. 이로 인해 벤더 간 경쟁은 핵심 알고리즘보다 오케스트레이션, 거버넌스, 엔터프라이즈 지원 분야에서 더욱 치열해지고 있습니다. 기업들이 교육 오버헤드를 줄이기 위해 툴체인을 통합하는 가운데, Python은 66%의 채택률을 유지하며 여전히 지배적인 언어로 자리 잡고 있습니다. 커뮤니티 패키지의 보안 결함으로 인해 많은 구매자들이 CVE 스캔 및 라이선스 컴플라이언스를 번들로 제공하는 상용 배포판으로 전환하고 있으며, 이로 인해 엔터프라이즈급 오픈소스 지원 모델로의 전환이 가속화되고 있습니다. Databricks는 MLflow를 자사 플랫폼에 네이티브하게 탑재하여 TensorFlow, PyTorch, scikit-learn을 넘나드는 모델 버전 관리를 락인 없이 구현했습니다. 이 기능 세트는 2024년 사상 최대 규모인 100억 달러 규모의 시리즈 J 라운드를 이끌었습니다. 하이퍼스케일러들이 비슷한 툴을 한계비용으로 묶어 팔면서 틈새 AutoML 벤더들의 수익률은 계속 압박을 받고 있습니다.

모델 거버넌스 규제 강화로 매니지드 플랫폼 활성화 촉진

2024년 8월부터 시행되는 유럽연합(EU)의 AI 법은 고위험 AI 시스템에 대한 적합성 평가를 의무화하고 있으며, 조직은 감사 추적 및 설명가능성 모듈이 내장된 플랫폼으로 전환해야 합니다. 이와 상호보완적인 바젤위원회의 은행업 가이드라인은 엄격한 모델 검증과 제3자 감사를 요구하고 있습니다. 미국 식품의약국(FDA)은 2025년 1월, 의료기기로서의 소프트웨어에 대한 지침을 업데이트하고 시판 전 신청 및 시판 후 모니터링 프로토콜을 규정했습니다. 강력한 버전 관리 기능을 갖춘 플랫폼이라면 이를 보다 효율적으로 처리할 수 있습니다. 2024년 출시된 IBM의 'watsonx.governance'는 EU AI 법률 보고 업무를 자동화하고, 법적 검토 주기를 몇 주에서 며칠로 단축합니다. 전담 컴플라이언스 팀이 없는 벤더는 대기업으로부터 입찰 자격을 잃을 위험이 있습니다.

공공 부문에서 EU의 다지역화를 가로막는 데이터 거주지 장벽은 무엇인가?

GDPR(EU 개인정보보호규정) 제44조 및 각국의 법령에 따라 적절한 보호 조치가 없는 한 EU 역외로 시민 데이터를 이전하는 것은 금지되어 있습니다. Gaia-X 이니셔티브는 도입이 18개월 늦어졌고, 프랑스와 독일 정부 부처의 Azure 및 AWS로의 전환이 지연되었습니다. 프랑스 각 부처는 OVHcloud와 T-Systems가 주권형 서비스를 인증할 때까지 플랫폼 도입을 연기했습니다. EU 클라우드 행동강령은 중소 벤더들이 대응하기 어려운 추가적인 컴플라이언스 요건을 추가했습니다. 이로 인해 정부 기관은 On-Premise 또는 로컬 클라우드로 전환할 수밖에 없었고, 전 세계 공급자의 규모의 경제를 제한하고 있습니다.

부문 분석

기업들이 인력 부족에 직면한 가운데, 서비스 분야는 2031년까지 연평균 복합 성장률(CAGR) 17.8%를 나타낼 것으로 예측되며, 이는 플랫폼 분야의 거의 두 배에 달하는 속도입니다. Databricks는 레이크하우스 마이그레이션 프로젝트를 원동력으로 2024 회계연도에 전문 서비스 매출이 48% 증가했습니다. IBM은 2024년까지 12개국에 왓슨엑스(watsonx)를 구축하는 5억 달러 규모의 은행 계약을 체결했습니다. 액센츄어와 마이크로소프트는 공동 사업 부문에 2,500명의 새로운 MLOps 전문가를 채용하여 자문 서비스에 대한 수요를 반영하고 있습니다. 벤더들은 현재 라이선스 비용이 총소유비용(TCO)의 40%를 초과하는 경우가 드물다는 점을 인식하고, 연간 구독에 성공 계획, 전담 아키텍트, 분기별 검토를 포함시키고 있습니다.

플랫폼 제공업체는 또한 중견기업 구매자에게 접근하기 위해 틈새 컨설팅 회사와의 제휴를 추진하고 있습니다. Slalom과 Deloitte는 2024년에 데이터 사이언스 부서를 신설하여 하이퍼스케일러 자문팀이 여전히 주요 고객에 집중하고 있는 틈새를 메웠습니다. 이번 제휴는 데이터 사이언스 플랫폼 시장이 성과 기반 마일스톤과 지속적인 최적화를 보장하는 소프트웨어 및 서비스를 결합한 계약으로 전환하고 있음을 강조합니다.

2025년에는 클라우드 컴퓨팅이 67.50%의 점유율을 차지했으며, 클라우드 도입 관련 데이터 사이언스 플랫폼 시장 규모는 2031년까지 연평균 복합 성장률(CAGR) 18.4%로 확대될 것으로 예측됩니다. AWS SageMaker에서 700억 개의 매개변수 모델을 훈련할 경우, 1회 실행당 약 35만 달러의 비용이 들지만, On-Premise 클러스터에 필요한 1,500만 달러의 설비투자를 피할 수 있습니다. 마이크로소프트는 2024년 Azure ML에 스팟 인스턴스를 추가해 특정 교육 비용을 최대 80%까지 절감했습니다. 구글의 Vertex AI Pipelines는 자체 관리형 Kubernetes 클러스터에 비해 운영 오버헤드를 60% 절감합니다.

엄격한 규제 환경에서는 On-Premise 구축이 여전히 유효합니다. 바젤 III의 준수에 따라 금융기관은 내부 통제를 중요시하고 있습니다. Databricks Unity Catalog는 멀티 클라우드와 On-Premise 환경 전반에 걸쳐 통합된 거버넌스를 제공하는 하이브리드 설계를 통해 두 가지의 장점을 결합했습니다. HPE의 GreenLake for Machine Learning Operations는 On-Premise 하드웨어에 대해 종량제 요금제를 제공합니다.

지역별 분석

북미는 2025년 47.23%의 점유율을 차지했으며, 하이퍼스케일러 용량과 2024년 250억 달러의 벤처 자금에 힘입어 성장세를 이어갈 것으로 예측됩니다. 미국 AI 관련 대통령령은 연방 기관에 거버넌스 프레임워크 채택을 의무화하고 있으며, 이는 컴플라이언스 대응 플랫폼에 대한 수요를 촉진하고 있습니다. 캐나다의 벡터 연구소는 연간 500명의 연구 인력을 양성하고 있으며, 국내 도입을 촉진하고 있습니다.

아시아태평양은 CAGR 17.1%로 예측됩니다. 서아시아에서는 사우디아라비아가 화웨이, Oracle과 손잡고 지역 AI 인프라에 1,000억 달러를 투자하고, 아랍에미리트(UAE)는 미국 모델에 대한 의존도를 낮추기 위해 오픈소스 Falcon LLM을 공개했습니다. 일본은 AI 칩 제조와 데이터센터 건설에 2조 엔(134억 달러)을 투자하겠다고 약속했습니다. 중국 시장은 수출 규제에도 불구하고 국내 액셀러레이터에 힘입어 여전히 확대되고 있습니다. 인도의 '디지털 인디아' 이니셔티브에 힘입어 2024년 클라우드 플랫폼 도입률은 전년 대비 35% 증가했습니다.

유럽의 성장 궤도는 거주 요건으로 인해 완만하게 성장하고 있습니다. 독일은 Gaia-X의 인증 획득을 기다리며 공공 부문의 전환을 연기했습니다. 영국의 AI 안전 연구소는 강력한 안전 조치를 요구하는 테스트 프로토콜을 개발 중입니다. 남미의 성장은 사기 감지를 위해 SageMaker를 도입하는 브라질 은행을 중심으로 진행되고 있습니다. 중동의 프로그램은 스마트 시티 모빌리티에 초점을 맞추고 있으며, 두바이의 교통 최적화 모델을 통해 교통 체증을 12% 감소시켰습니다. 아프리카에서의 도입은 아직 초기 단계이며, 통신사의 해지 예측 시범사업에 국한되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Data Science Platform Market size is expected to increase from USD 109 billion in 2025 to USD 132.19 billion in 2026 and reach USD 284.37 billion by 2031, growing at a CAGR of 16.56% over 2026-2031.

Steady growth is unfolding as enterprises shift from isolated machine-learning pilots toward production systems that integrate data ingestion, model training, governance, and edge inference. Integrated toolchains promise faster time-to-value, while hyperscalers bundle advanced functionality into existing cloud contracts, compressing margins for niche vendors. Meanwhile, domain-specific foundation models are redefining use cases in healthcare and finance, and sovereign AI programs are channeling billions of dollars into regional data centers and GPU clusters. Competitive positioning now hinges on seamless governance, feature-store performance, and the ability to serve retrieval-augmented generation workloads at scale.

Global Data Science Platform Market Trends and Insights

Proliferation of Open-Source ML Frameworks Catalyzing Platform Convergence

Open-source libraries power 87% of AI workloads, up eight percentage points from 2024, intensifying vendor competition on orchestration, governance, and enterprise support rather than core algorithms. Python remains the dominant language, with 66% adoption, as firms consolidate toolchains to curb training overhead. Security gaps in community packages push many buyers toward commercial distributions that bundle CVE scanning and license compliance, adding momentum to enterprise-grade open-source support models. Databricks built MLflow natively into its platform, enabling model versioning across TensorFlow, PyTorch, and scikit-learn without lock-in, a feature set that underpinned its record USD 10 billion Series J round in 2024. As hyperscalers bundle similar tooling at marginal cost, margins for niche AutoML vendors continue to compress.

Stricter Model-Governance Regulations Boosting Managed Platforms

The European Union AI Act, in force since August 2024, requires conformity assessments for high-risk AI systems, steering organizations toward platforms with built-in audit trails and explainability modules. Complementary banking guidance from the Basel Committee demands rigorous model validation and third-party audits. The United States FDA updated software-as-a-medical-device guidance in January 2025, specifying pre-market submissions and post-market surveillance protocols that platforms with strong version control handle more efficiently. IBM's watsonx.governance, launched 2024, automates EU AI Act reporting, trimming legal review cycles from weeks to days. Vendors lacking dedicated compliance teams risk disqualification from large enterprise bids.

Data-Residency Barriers Hindering Multi-Region Roll-Outs In Public Sector EU

GDPR Article 44 and national statutes prohibit transferring citizen data to non-EU regions without adequacy safeguards. The Gaia-X initiative lagged deployment by 18 months, delaying Azure and AWS migrations for French and German ministries. France's ministries postponed platform adoption until OVHcloud and T-Systems certified sovereign offerings. The EU Cloud Code of Conduct added further compliance layers that smaller vendors struggle to absorb. Resulting fragmentation pushes agencies toward on-premise or local-cloud installations, limiting economies of scale for global providers.

Other drivers and restraints analyzed in the detailed report include:

- Edge-To-Cloud Fabric Adoption Enabling Hybrid Platforms In Manufacturing

- Unstructured Video And IoT Data Explosion Requiring Scalable Feature Stores

- Shortage Of ML-Ops Engineers Undermining Complex Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are poised for a 17.8% CAGR through 2031, nearly double that of platforms, as enterprises confront talent shortages. Databricks logged a 48% rise in professional services revenue in fiscal 2024, driven by lakehouse migration projects. IBM secured a USD 500 million banking contract in 2024 to deploy watsonx across 12 countries. Accenture and Microsoft staffed 2,500 new MLOps specialists for their joint practice, reflecting demand for advisory services. Vendors now embed success plans, dedicated architects, and quarterly reviews into annual subscriptions, recognizing that licenses rarely account for more than 40% of total cost of ownership.

Platform providers also court niche consultancies to reach mid-market buyers. Slalom and Deloitte launched dedicated data-science practices in 2024, filling a gap where hyperscaler advisory teams remain focused on flagship accounts. This collaboration underscores the Data Science Platform market's pivot toward blended software-plus-services contracts that guarantee outcome-based milestones and ongoing optimization.

Cloud computing held 67.50% share in 2025, and the Data Science Platform market size tied to cloud deployments is projected to grow at an 18.4% CAGR through 2031. Training a 70-billion-parameter model on AWS SageMaker costs roughly USD 350,000 per run and avoids the USD 15 million capital outlay for on-premises clusters. Microsoft added spot instances to Azure ML in 2024, cutting certain training costs by up to 80%. Google's Vertex AI Pipelines cut operational overhead by 60% compared with self-managed Kubernetes clusters.

On-premise deployments survive in tightly regulated environments. Basel III compliance favors in-house control among financial institutions. Hybrid designs bridge both worlds, with Databricks Unity Catalog offering unified governance across multi-cloud and on-premise estates. HPE's GreenLake for Machine Learning Operations delivers consumption-based pricing for on-premise hardware.

The Data Science Platform Market Report is Segmented by Product Offering (Platform, and Services), Deployment (On-Premise, and Cloud), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing, Energy and Utilities, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America claimed 47.23% share in 2025, supported by hyperscaler capacity and USD 25 billion in venture funding during 2024. The U.S. Executive Order on AI requires federal agencies to adopt governance frameworks, fueling demand for compliant platforms. Canada's Vector Institute trains 500 researchers a year, buoying domestic adoption.

Asia-Pacific is forecast for a 17.1% CAGR. In Western Asia, Saudi Arabia dedicated USD 100 billion to regional AI infrastructure, partnering with Huawei and Oracle, and the United Arab Emirates released open-source Falcon LLMs to reduce reliance on U.S. models. Japan pledged JPY 2 trillion (USD 13.4 billion) to AI chip fabrication and data center construction. China's market still expands despite export controls, propelled by domestic accelerators. India's Digital India initiative drove 35% year-over-year cloud-platform adoption in 2024.

Europe's trajectory is flatter due to residency mandates. Germany delayed public-sector migrations pending Gaia-X certification. The U.K. AI Safety Institute is crafting testing protocols that require robust safety guardrails. South America's growth centers on Brazilian banks deploying SageMaker for fraud detection. Middle East programs focus on smart-city mobility, as Dubai's traffic-optimization models trimmed congestion by 12%. African adoption remains nascent, limited to telecom churn-prediction pilots.

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Alteryx Inc.

- SAS Institute Inc.

- Databricks Inc.

- Snowflake Inc.

- Amazon Web Services Inc.

- The MathWorks Inc.

- RapidMiner Inc.

- DataRobot Inc.

- H2O.ai

- TIBCO Software Inc.

- KNIME GmbH

- Domino Data Lab Inc.

- Oracle Corporation

- SAP SE

- Cloudera Inc.

- Qlik Tech International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Open-Source ML Frameworks Driving Platform Convergence

- 4.2.2 Stricter Model-Governance Regulations Boosting Managed Platforms

- 4.2.3 Edge-to-Cloud Fabric Adoption Enabling Hybrid Platforms in Manufacturing

- 4.2.4 Unstructured Video and IoT Data Explosion Requiring Scalable Feature Stores

- 4.2.5 Rise of Domain-Specific Foundation Models Accelerating Vertical Platforms

- 4.2.6 GPU Supply-Chain Localisation Policies Steering Regional Platform Build-outs

- 4.3 Market Restraints

- 4.3.1 Data-Residency Barriers Hindering Multi-Region Roll-outs in Public Sector EU

- 4.3.2 Shortage of ML-Ops Engineers Undermining Complex Deployments

- 4.3.3 Escalating Cloud Bills Creating Budget Pushback for Real-Time Training

- 4.3.4 Legacy Data Silos in Energy and Utilities Delaying Platform ROI

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Offering

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Manufacturing

- 5.4.5 Energy and Utilities

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Defense

- 5.4.8 Rest of End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Google LLC (Alphabet Inc.)

- 6.4.3 Microsoft Corporation

- 6.4.4 Alteryx Inc.

- 6.4.5 SAS Institute Inc.

- 6.4.6 Databricks Inc.

- 6.4.7 Snowflake Inc.

- 6.4.8 Amazon Web Services Inc.

- 6.4.9 The MathWorks Inc.

- 6.4.10 RapidMiner Inc.

- 6.4.11 DataRobot Inc.

- 6.4.12 H2O.ai

- 6.4.13 TIBCO Software Inc.

- 6.4.14 KNIME GmbH

- 6.4.15 Domino Data Lab Inc.

- 6.4.16 Oracle Corporation

- 6.4.17 SAP SE

- 6.4.18 Cloudera Inc.

- 6.4.19 Qlik Tech International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment