|

시장보고서

상품코드

2044163

센서 퓨전 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Sensor Fusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

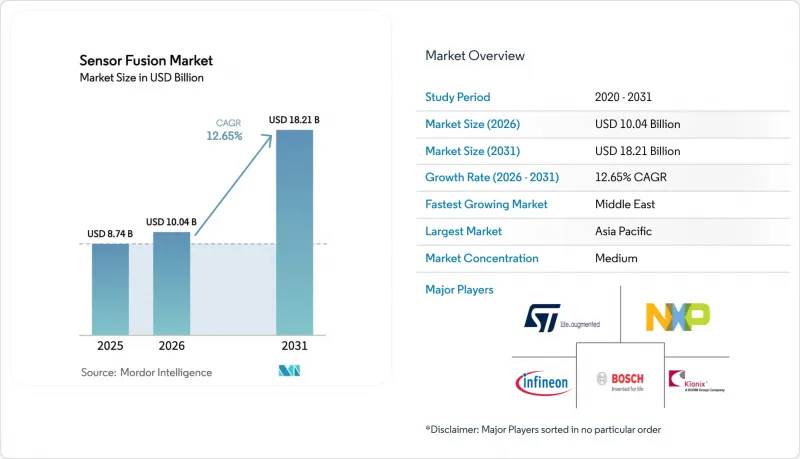

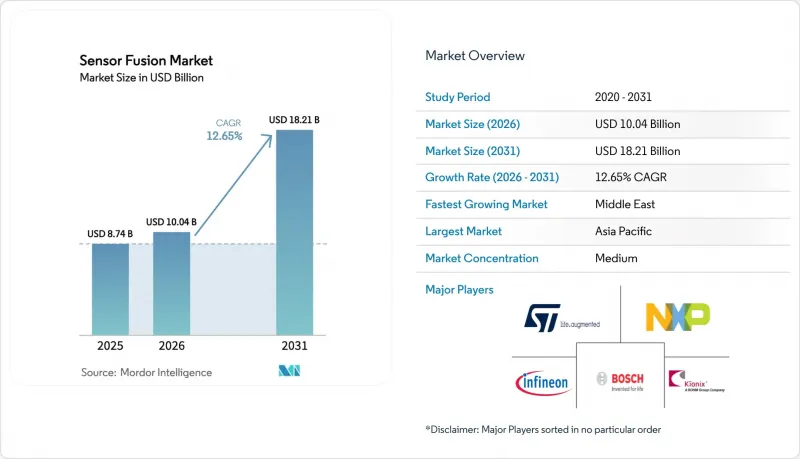

센서 퓨전 시장 규모는 2025년에 87억 4,000만 달러로 평가되었고 2026년 100억 4,000만 달러에서 2031년까지 182억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 12.65%를 나타낼 전망입니다.

솔리드 스테이트 LiDAR의 지속적인 비용 절감, Euro NCAP의 안전 기준 강화, 엣지 AI용 실리콘 기술의 발전으로 OEM의 예산은 카메라, 레이더, LiDAR, 관성 측정 장치를 단일 스택에 통합한 멀티 센서 제품군으로 이동하고 있습니다. 자동차 제조업체들은 재설계 비용을 피하기 위해 플랫폼 전반에 걸쳐 센서 퓨전 하드웨어의 표준화를 추진하고 있으며, 가전제품 제조업체들은 클라우드 지연을 줄이고 프라이버시 규제를 준수하기 위해 기기 내 추론을 채택하고 있습니다. 1티어 공급업체와 반도체 업체 간의 경쟁 심화로 하드웨어의 수익률은 압박을 받고 있지만, 이러한 추세는 구독형 융합 소프트웨어와 무선 기능 업데이트의 성장으로 상쇄되고 있습니다. 이미징 레이더 및 소프트웨어 정의 LiDAR 스타트업에 대한 자본 유입은 혁신 주기를 가속화하고, 새로운 양식을 시장에 출시하는 데 걸리는 시간을 단축하며, 중복성 전략을 강화하고 있습니다.

세계 센서 퓨전 시장 동향 및 인사이트

유로 NCAP의 5성 평가에서 센서 퓨전 의무화로 유럽 OEM의 센서 퓨전 채택 가속화

Euro NCAP의 2026년 프로토콜은 5성 등급을 획득하기 위해 레이더 카메라 또는 LiDAR 카메라의 통합을 의무화하고 있으며, 유럽 자동차 제조업체들이 양산 모델을 즉시 재설계하도록 유도하고 있습니다. 폭스바겐은 2026년 이후 MEB 플랫폼이 탑재되는 모든 차량에 레이더-카메라 융합 시스템을 탑재하고, 단일 센서 아키텍처를 폐지할 것을 확인했습니다. 자동차 제조업체들이 턴키 방식으로 규제 대응을 요구하고 있는 가운데, 인증 미들웨어를 보유한 Tier 1 공급업체들이 설계 수주를 따내고 있습니다. 이 규제로 인한 세계 파급효과는 아시아태평양 및 남미 수출에서 두드러지게 나타나고 있으며, 유럽 사양의 플랫폼을 재사용함으로써 엔지니어링상의 차이를 최소화하고 있습니다. 이러한 정책 전환으로 멀티센서를 통한 이중화는 프리미엄 옵션이 아닌 표준 사양으로 자리 잡아가고 있습니다.

솔리드 스테이트 LiDAR의 비용 절감으로 미들부문 차량에 멀티 센서 제품군 장착 가능

Hesai는 실리콘 포토닉스와 양산 규모의 이점을 활용하여 2026년 말까지 500달러 이하의 솔리드 스테이트 LiDAR를 실현하는 것을 목표로 하고 있습니다. BYD는 이미 2만 5,000달러 이하의 세단에 LiDAR, 카메라, 레이더 어레이를 탑재하고 있으며, 고급차 계층을 넘어 그 적용 범위를 넓혀가고 있습니다. 지리(Geely)의 '갤럭시(Galaxy)' 프로그램도 이 전략을 따르고 있으며, 유럽과 북미의 경쟁사들도 솔리드 스테이트 LiDAR 로드맵에 박차를 가하고 있습니다. 중국의 국내 생산량은 2027년까지 연간 200만 대를 넘어섰으며, 이는 저렴한 가격의 ADAS 보급에 있어 이 지역의 리더십을 강화하는 공급망 우위를 확보할 수 있을 것으로 보입니다.

통합된 융합 아키텍처 표준의 부재로 인한 상호운용성 저해 요소들

ADAS 센서 인터페이스에 대한 SAE 가이드라인은 여전히 임의적입니다. 한편, AUTOSAR, ROS 2, 독자 스택이 주도권을 놓고 경쟁하고 있습니다. 자동차 제조업체는 센서 공급업체를 변경할 때 높은 엔지니어링 비용을 부담하게 되고, 무선 업데이트(OTA)는 서로 다른 프로토콜 간의 재검증을 위해 많은 시간이 소요됩니다. 산업 컨소시엄은 개방형 형태 구축을 목표로 하고 있지만, 데이터 타이밍과 고장 모드 처리에 대한 합의는 2028년 이전에는 이루어지지 않을 것으로 예상되며, 플랫폼 간 확장성이 지연되고 있습니다.

부문 분석

2025년 센서 퓨전 시장 매출의 61.73%를 하드웨어가 차지하고 있으며, 이는 물리적 센싱 레이어를 구성하는 레이더, LiDAR, 카메라, IMU 모듈의 자본 집약성을 반영하고 있습니다. 레이더 모듈은 50-150달러의 가격대로 모든 기상 조건에서 견고한 성능으로 ADAS 시장을 독점하고 있습니다. 반면, 여전히 대당 500달러가 넘는 솔리드 스테이트 LiDAR는 중복성을 필요로 하는 레벨 3-5의 프로그램에 국한되어 있습니다. 이미징 센서는 스마트폰 규모의 경제 효과의 혜택을 누리고 있으며, 대당 10달러 이하의 가격으로 멀티 카메라 어레이를 구현하고 있습니다. 하드웨어에 의한 센서 퓨전 시장 규모는 꾸준히 확대될 것으로 예상되지만, 그 속도는 소프트웨어에 비해 완만할 것으로 보입니다.

OEM 업체들이 무선 기능 출시 및 구독 모델로 전환함에 따라 소프트웨어 시장은 2031년까지 연평균 복합 성장률(CAGR) 12.68%로 하드웨어 시장보다 더 빠르게 성장할 것으로 예측됩니다. Mobileye SuperVision과 같은 플랫폼은 차량 단위의 라이선스 비용을 부과하여 일회용 하드웨어 판매를 지속적인 수익으로 전환하고 있습니다. ISO 26262 검증 도구는 수익률을 더욱 향상시키고 있으며, 자동차 제조업체들은 융합 스택 인증에 플랫폼당 500만-1,000만 달러를 지출하고 있습니다. 이러한 추세에 따라 소프트웨어는 센서 퓨전 산업에서 가장 큰 가치 창출 계층으로 자리매김하고 있습니다.

레이더와 카메라의 조합은 레이더의 속도 정확도와 카메라의 물체 분류를 융합하여 2025년 센서 퓨전 시장 점유율의 43.56%를 차지했습니다. 대륙의 ARS540 4D 레이더는 고도의 해상도를 확대하여 다양한 도시 환경에서의 성능을 향상시키고 있다(CONTINENTAL.COM). 500달러 미만의 솔리드 스테이트 유닛을 기반으로 한 LiDAR와 카메라 융합은 12.72%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. Mercedes-Benz와 Stellantis는 레벨 3 기능을 구현하기 위해 Valeo의 SCALA 3 LiDAR를 도입하여 이 기술이 프로토타입에서 대량 생산으로 전환되고 있음을 보여주고 있습니다.

레이더, LiDAR, 카메라를 통합한 3센서 구성은 여전히 틈새 시장이며, 중복성이 비용을 초과하는 프리미엄 로보틱스 프로그램에 국한되어 있습니다. 한편, IMU-GPS 융합은 부품 비용에 미치는 영향이 최소화되어 드론과 스마트폰에 정착하고 있습니다. 솔리드 스테이트 LiDAR의 가격이 이미징 레이더에 근접함에 따라, 중급 차량에서도 하이브리드 접근 방식이 채택될 것으로 예상되며, 센서 퓨전 시장 규모는 고급차 계층을 넘어 확대될 것으로 보입니다.

센서 퓨전 시장은 제공 형태(하드웨어, 소프트웨어), 융합 방식(레이더+카메라 융합, LiDAR+카메라 융합, 기타), 알고리즘 유형(카르만 필터(EKF, UKF), 베이지안 네트워크, 기타), 용도, 차종, 지역별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

지역별 분석

2025년에는 아시아태평양이 40.81%를 차지하며 가장 큰 수익을 창출할 것으로 예측됩니다. 이는 중국의 적극적인 ADAS 보급, 일본의 로봇공학 생태계, 한국의 반도체 공급망에 힘입은 것입니다. 중국에서만 지역 매출의 58%를 차지하며, BYD, 지리(Geely), NIO가 전기차(EV) 전체에 멀티 센서 제품군 표준화를 추진한 것이 원동력이 되었습니다. 레벨 2 기능에 대한 보조금 지급을 조건으로 한 정부 인센티브가 도입을 더욱 확대하는 한편, 국내 LiDAR 생산 능력이 국내 완성차 업체들의 가격경쟁력을 강화하고 있습니다.

유럽은 2025년, 멀티모달 센싱을 의무화하는 엄격한 Euro NCAP 및 일반 안전 규정의 요구사항의 혜택을 받아 전 세계 매출의 상당 부분을 차지했습니다. 독일이 지역 수요를 주도하고 폭스바겐, BMW, 메르세데스-벤츠는 여러 브랜드 간 연구개발비용을 분산하기 위해 플랫폼 수준에서 센싱 융합 스택을 통합했습니다. 유럽의 센서 퓨전 시장은 2028년까지 상용차 및 이륜차까지 규제 범위가 확대됨에 따라 꾸준한 성장세를 유지할 것으로 예측됩니다.

북미는 2025년 상당한 점유율을 차지했으며, 미국 완성차 업체들의 자발적인 ADAS 도입과 5.9GHz 대역 V2X 주파수 할당에 힘입은 것으로 분석됩니다. 중동은 현재 규모는 작지만, 아랍에미리트와 사우디아라비아가 국방 예산을 강력한 융합 기술을 필요로 하는 자율형 자산에 투입하고 있어 2031년까지 연평균 복합 성장률(CAGR) 12.75%로 가장 높은 성장세를 보일 것으로 예측됩니다. 남미와 아프리카는 낮은 자동차 보유량과 LiDAR공급망 제약으로 인해 전체 매출 비중은 작지만, 광업 및 농업 자동화가 새로운 기회를 창출하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The sensor fusion market size was valued at USD 8.74 billion in 2025 and estimated to grow from USD 10.04 billion in 2026 to reach USD 18.21 billion by 2031, at a CAGR of 12.65% during the forecast period (2026-2031).

Sustained cost reductions in solid-state LiDAR, rising Euro NCAP safety mandates, and breakthroughs in edge-AI silicon are shifting original-equipment budgets toward integrated multi-sensor suites that combine cameras, radar, LiDAR, and inertial units in a single stack. Vehicle manufacturers are standardizing sensor-fusion hardware across entire platforms to avoid redesign costs, while consumer-electronics brands adopt on-device inference to cut cloud latency and comply with privacy regulations. Intensifying competition among tier-one suppliers and semiconductor leaders is compressing hardware margins, a trend offset by growth in subscription-based fusion software and over-the-air feature unlocks. Capital inflows into imaging-radar and software-defined LiDAR start-ups are accelerating innovation cycles, reducing time-to-market for new modalities and enhancing redundancy strategies.

Global Sensor Fusion Market Trends and Insights

Mandate Of Sensor Fusion For Euro NCAP 5-Star Ratings Accelerating European OEM Adoption

Euro NCAP's 2026 protocols require radar-camera or LiDAR-camera integration to secure a 5-star score, driving immediate redesigns of volume models by European brands. Volkswagen confirmed that all post-2026 MEB launches will carry radar-camera fusion, eliminating single-sensor architectures. Tier-one suppliers with certified middleware are capturing design wins as automakers seek turnkey compliance. The regulation's global ripple effect is evident in exports to Asia Pacific and South America, where reuse of Euro-spec platforms minimizes engineering divergence. This policy shift entrenches multi-sensor redundancy as a baseline rather than a premium option.

Solid-State LiDAR Cost Decline Enabling Multi-Sensor Suites in Mid-Segment Cars

Hesai is committed to sub-USD 500 solid-state LiDAR by late 2026, leveraging silicon-photonics and volume scaling. BYD already deploys LiDAR-camera-radar arrays in sedans below USD 25,000, widening adoption beyond luxury tiers. Geely's Galaxy program mirrors this strategy, prompting European and North American peers to accelerate solid-state roadmaps. China's domestic output is projected to top 2 million LiDAR units annually by 2027, establishing supply-chain leverage that reinforces the region's leadership in affordable ADAS penetration.

Lack of Uniform Fusion Architecture Standards Hindering Interoperability

SAE guidelines for ADAS sensor interfaces remain voluntary, while AUTOSAR, ROS 2, and proprietary stacks compete for dominance. Automakers incur higher engineering costs when swapping sensor suppliers, and over-the-air updates demand time-consuming revalidation across divergent protocols. Industry consortia are pursuing open formats, yet consensus on data timing and failure-mode handling is not expected before 2028, slowing cross-platform scalability.

Other drivers and restraints analyzed in the detailed report include:

- Edge-AI Chip Advancements Allowing Real-Time Multi-Modal Fusion in Mobile and XR Devices

- Deployment of AMR Robots in Smart Factories Demanding High-Accuracy Sensor Fusion

- High Computational Overhead Raising Bill-Of-Materials For Non-Automotive IoT

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 61.73% of 2025 revenue across the sensor fusion market, reflecting the capital intensity of radar, LiDAR, camera, and IMU modules that constitute the physical sensing layer. Radar modules priced between USD 50 and USD 150 dominate ADAS because of robust all-weather capabilities, whereas solid-state LiDAR, still above USD 500 per unit, is reserved for Level 3-5 programs requiring redundancy. Imaging sensors benefit from smartphone-scale economies, enabling multi-camera arrays at sub-USD 10 each. The sensor fusion market size attributed to hardware is set to increase steadily but at a slower pace than software.

Software is projected to outpace hardware with a 12.68% CAGR through 2031 as OEMs shift to over-the-air feature unlocks and subscription models. Platforms such as Mobileye SuperVision charge licensing fees per vehicle, converting one-off hardware sales into recurring revenue. ISO 26262 validation tools further enhance margins, with automakers spending USD 5-10 million per platform to certify fusion stacks. This dynamic positions software as the prime value-capture layer inside the sensor fusion industry.

Radar-camera pairing represented 43.56% of sensor fusion market share in 2025 by combining radar's velocity accuracy with camera-based object classification. Continental's ARS540 4D radar extends elevation resolution, enhancing performance in cluttered urban settings CONTINENTAL.COM. LiDAR-camera fusion, supported by sub-USD 500 solid-state units, is forecast to record the fastest 12.72% CAGR. Mercedes-Benz and Stellantis deploy Valeo's SCALA 3 LiDAR to unlock Level 3 functions, underscoring the technology's migration from prototypes to series production.

Three-sensor frameworks that integrate radar, LiDAR, and cameras remain niche, limited to premium robotaxi programs where redundancy trumps cost. Conversely, IMU-GPS fusion is entrenched in drones and smartphones due to minimal bill-of-materials impact. As solid-state LiDAR pricing converges with imaging-radar, mid-segment vehicles are expected to embrace hybrid approaches, expanding the sensor fusion market footprint beyond luxury tiers.

Sensor Fusion Market Sensor Fusion Market Segmented by Offering (Hardware, Software), Fusion Method (Radar + Camera Fusion, Lidar + Camera Fusion and More), Algorithm Type (Kalman Filter (EKF, UKF), Bayesian Networks and More), Application, Vehicle Type and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated the largest regional revenue in 2025 at 40.81%, anchored by China's aggressive ADAS penetration, Japan's robotics ecosystem, and South Korea's semiconductor supply chain. China alone accounted for 58% of regional turnover, driven by BYD, Geely, and NIO standardizing multi-sensor suites across their electric vehicles. Government incentives that tie subsidies to Level 2 functionality further expand uptake, while domestic LiDAR capacity strengthens price competitiveness for local automakers.

Europe accounted for a fair share of global revenue in 2025, benefiting from stringent Euro NCAP and General Safety Regulation mandates that require multi-modal sensing. Germany led regional demand, with Volkswagen, BMW, and Mercedes-Benz integrating fusion stacks at the platform level to amortize R&D across multiple brands. The sensor fusion market in Europe is projected to maintain steady growth as regulatory scope broadens to include commercial vehicles and motorcycles by 2028.

North America held a considerable share in 2025, driven by U.S. automakers' voluntary ADAS commitments and allocations of 5.9 GHz V2X spectrum. The Middle East, though smaller today, is forecast for the fastest 12.75% CAGR through 2031 as the United Arab Emirates and Saudi Arabia channel defense budgets into autonomous assets requiring robust fusion. South America and Africa collectively captured a small share of revenue, constrained by lower vehicle ownership and limited LiDAR supply chains, yet mining and agriculture automation is opening targeted opportunities.

- Robert Bosch GmbH

- Continental AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Texas Instruments Inc.

- Nvidia Corporation

- Qualcomm Incorporated

- Analog Devices Inc.

- Mobileye Global Inc.

- Aptiv PLC

- Renesas Electronics Corporation

- Valeo S.A.

- ZF Friedrichshafen AG

- Arbe Robotics Ltd.

- BASELABS GmbH

- LeddarTech Inc.

- TDK Corporation

- Kionix Inc. (ROHM)

- Memsic Inc.

- CEVA Inc.

- AMD Xilinx

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandate of Sensor Fusion for Euro NCAP 5-Star Ratings Accelerating European OEM Adoption

- 4.2.2 Solid-State LiDAR Cost Decline Enabling Multi-Sensor Suites in Mid-Segment Cars across China

- 4.2.3 Edge-AI Chip Advancements Allowing Real-Time Multi-Modal Fusion in Mobile and XR Devices

- 4.2.4 Deployment of AMR Robots in Smart Factories Demanding High-Accuracy Sensor Fusion

- 4.2.5 Defense Modernization Programs Funding Multi-Sensor Targeting and Navigation Systems in Middle East

- 4.2.6 Integration of V2X Data Streams into Fusion Stacks to Unlock L4 Autonomous Driving in the United States

- 4.3 Market Restraints

- 4.3.1 Lack of Uniform Fusion Architecture Standards Hindering Interoperability

- 4.3.2 High Computational Overhead Raising BoM for Non-Automotive IoT Devices

- 4.3.3 Limited LiDAR Penetration in Emerging Markets Restricts Multi-Modal Fusion Adoption

- 4.3.4 Data-Privacy and Cyber-Security Concerns Around Cloud-Aided Sensor Fusion Pipelines

- 4.4 Value Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.5.1 Technology Evolution Roadmap for Multi-Sensor Fusion Platforms

- 4.5.2 Edge-AI Integration and SoC Advancements

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers, Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Market Trends

- 4.8.1 Key Patents and Research Activities

- 4.8.2 Major and Emerging Applications

- 4.8.2.1 Adaptive Cruise Control (ACC)

- 4.8.2.2 Autonomous Emergency Braking (AEB)

- 4.8.2.3 Electronic Stability Control (ESC)

- 4.8.2.4 Forward Collision Warning (FCW)

- 4.8.2.5 Other Emerging Applications

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Fusion Method

- 5.2.1 Radar + Camera Fusion

- 5.2.2 LiDAR + Camera Fusion

- 5.2.3 Radar + LiDAR Fusion

- 5.2.4 IMU + GPS Fusion

- 5.2.5 3-Sensor Fusion (Camera + Radar + LiDAR)

- 5.3 By Algorithm Type

- 5.3.1 Kalman Filter (EKF, UKF)

- 5.3.2 Bayesian Networks

- 5.3.3 Neural Network, Deep Learning

- 5.3.4 GNSS, INS Integration

- 5.4 By Application

- 5.4.1 Advanced Driver Assistance Systems (ADAS)

- 5.4.1.1 ACC

- 5.4.1.2 AEB

- 5.4.1.3 ESC

- 5.4.1.4 FCW

- 5.4.1.5 Lane-Keep Assist (LKA)

- 5.4.2 Autonomous Driving (Level 3-5)

- 5.4.3 Consumer Electronics (AR, VR, Smartphones, Wearables)

- 5.4.4 Robotics and Drones

- 5.4.5 Industrial Automation and Smart Manufacturing

- 5.4.6 Defense and Aerospace

- 5.4.1 Advanced Driver Assistance Systems (ADAS)

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Heavy Commercial Vehicles

- 5.5.4 Other Autonomous Vehicles

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank, Share, Products and Services, Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 NXP Semiconductors N.V.

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Texas Instruments Inc.

- 6.4.7 Nvidia Corporation

- 6.4.8 Qualcomm Incorporated

- 6.4.9 Analog Devices Inc.

- 6.4.10 Mobileye Global Inc.

- 6.4.11 Aptiv PLC

- 6.4.12 Renesas Electronics Corporation

- 6.4.13 Valeo S.A.

- 6.4.14 ZF Friedrichshafen AG

- 6.4.15 Arbe Robotics Ltd.

- 6.4.16 BASELABS GmbH

- 6.4.17 LeddarTech Inc.

- 6.4.18 TDK Corporation

- 6.4.19 Kionix Inc. (ROHM)

- 6.4.20 Memsic Inc.

- 6.4.21 CEVA Inc.

- 6.4.22 AMD Xilinx

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment