|

시장보고서

상품코드

2044165

통풍 치료제 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Gout Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

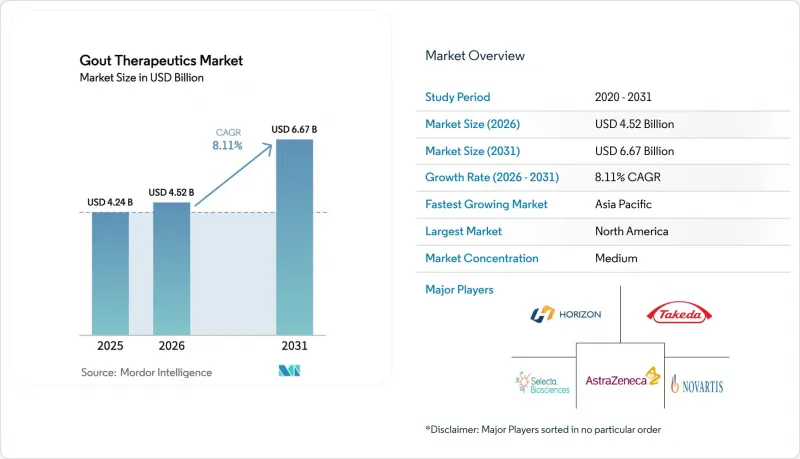

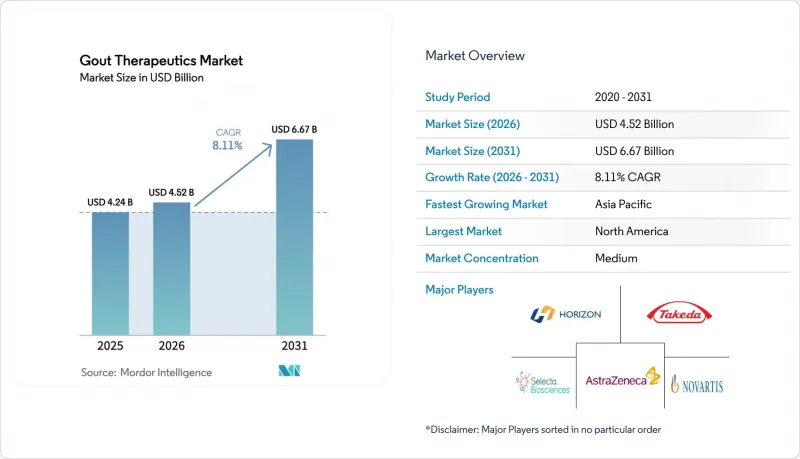

통풍 치료제 시장 규모는 2025년에 42억 4,000만 달러, 2026년에 45억 2,000만 달러가 되어, 2031년까지 66억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 CAGR 8.11%로 성장할 전망입니다.

수요는 고령화, 비만 관련 고요산혈증 증가, 목표치 달성에 중점을 둔 혈청 요산 수치 임계치를 설정한 최신 임상 가이드라인에 의해 주도되고 있습니다. 난치성 질환에 대한 생물학적 제의 도입은 의사의 치료 선택권을 확대하는 동시에 높은 가격 책정의 기회를 가져오고 있습니다. 한편, 제네릭 의약품의 가격 하락으로 수익률이 압박을 받는 가운데, 고정용량 경구용 복합제는 시장 점유율을 방어할 수 있는 위치에 있습니다. 스마트폰용 요산 측정기와 알고리즘에 의한 발작 예측 기능을 통합한 디지털 모니터링 도구는 진단을 빠르게 하는 동시에 고가의 응급실 방문을 줄이려는 보험사의 전략과도 부합합니다. 그러나 페북소스타트 관련 심혈관계 안전성 경고, 보험사의 페그로티카세 사전 승인 요건, 크산틴옥시다아제 억제 계열의 제네릭 의약품과의 경쟁으로 인해 성장 전망은 제한적일 수밖에 없습니다.

세계 통풍 치료제 시장 동향 및 인사이트

고령화와 비만으로 인한 질병 유병률 증가

2025년까지 전 세계 통풍 환자 수는 4,100만 명에 달했으며, 비만율이 30% 이상인 고소득 국가에서 가장 빠른 증가세를 보이고 있습니다. 고인슐린혈증은 신장의 요산 제거를 감소시키고, 과당 대사는 퓨린 대사를 촉진하여 혈청 요산 수치를 상승시킵니다. 중국에서는 2015년부터 2024년까지 통풍 진단 건수가 두 배로 증가했으며, 이는 도시 지역의 식습관이 붉은 육류와 당분이 함유된 음료로 전환된 결과입니다. 통풍 환자 인구통계학적 특성도 변화하고 있으며, 전통적인 추세인 60대 남성이 아닌 30, 40대에 발병하는 것이 일반화되어 있습니다. 이러한 인구 통계학적 변화로 인해 치료 대상 인구는 매년 확대되고 있으며, 치료 기간도 길어지고 있습니다. 일본에서는 2025년 건강 통계에서 통풍은 50세 이상 남성의 만성 외래 질환 상위 10위 안에 들었으며, 그 유병률은 고혈압, 당뇨병과 동등한 수준입니다.

근거에 기반한 요산강하 치료 가이드라인 채택

미국류마티스학회(ACR)의 2024년 개정판에서는 모든 통풍 환자의 혈청 요산 수치 목표치를 6mg/dL 이하, 토피가 동반된 환자의 경우 5mg/dL 이하로 정하고 있습니다. 마찬가지로, 유럽 가이드라인에서도 기존의 경과 관찰 접근법 대신 진단 후 몇 주 이내에 크산틴 산화효소 억제를 조기에 투여할 것을 강조하고 있습니다. 2025년 메디케어 청구 데이터 분석에 따르면, 상당한 개선이 이루어질 것으로 보입니다. 미국에서 새로 통풍 진단을 받은 환자의 68%가 90일 이내에 요산강하요법을 시작했으며, 이는 2019년의 42%에서 크게 증가한 수치입니다. 가이드라인에서 권장하는 병용요법에 부합하도록 설계된 고정용량 경구용 병용요법은 개발이 진행 중이지만, 규제 당국은 용량 조절이 가능한 단독요법 대비 우월성에 대한 증거를 요구하고 있습니다. 독일과 영국에서는 현재 류마티스 전문의에 대한 인센티브가 혈청 요산 수치 목표치의 전자 기록과 연동되어, 진료 시점의 검사 장비 도입을 촉진하고 있습니다.

기존 및 신규 치료법에 대한 안전성 우려 사항

페북소스타트에 대해서는 CARES 검사에서 알로퓨리놀 대비 심혈관 사망이 34% 증가한 것으로 나타나 상자 경고(박스 경고)가 부착되어 있습니다. EMA의 2024년 부속서 개정으로 2차 치료제로 사용이 제한되면서 EU의 배합 추세는 알로퓨리놀로 이동하고 있습니다. 페그로티카세의 경우, 아나필락시스의 위험이 있기 때문에 정맥주사 센터에서 모니터링이 필요하며, 1회 투여당 1,500-2,000달러의 시설비용이 추가됩니다. 신기능 장애 환자에서 콜히친의 과다 투여로 인해 2025년 FDA가 안전성 경고를 발령하면서 치료 범위가 좁다는 점이 주목받았습니다. 이러한 신호로 인해 지불 기관의 승인 주기가 길어지고, 사전 승인 지연은 평균 12일에 달하며, 치료 시작 전 환자 이탈의 원인이 되고 있습니다.

부문 분석

크산틴산화효소 억제는 알로퓨리놀의 광범위한 사용과 심혈관 위험이 관리 가능한 경우 페북소스타트의 선택적 사용으로 인해 2025년 통풍 치료제 시장 매출의 46.34%를 차지했습니다. 요산배설촉진제는 병용요법 프로토콜 채택 확대와 신장 안전성 프로파일이 개선된 차세대 URAT1 길항제 출시 전망에 힘입어 CAGR 9.54%의 견조한 성장이 예상됩니다. 2025년 기준 재조합 우리카제는 시장 규모의 5% 미만을 차지했지만, Krystexxa의월약 1만 8,000달러의 높은 가격에 힘입어 큰 가치를 창출했습니다. 또한, 카나키누맙과 같은 IL-1 표적치료제는 NSAIDs나 콜히친에 내성이 있는 환자를 위한 급성 발작 예방 분야에 대응하고 있으며, 요산 수치를 직접적으로 낮추지 않고도 요산 수치를 낮출 수 있는 치료 옵션을 확장하고 있습니다.

가격 압력으로 인해 경구 치료 부문은 재편되고 있으며, 대부분 시장에서 콜히친 제네릭 의약품의 가격은 1정당 0.50달러 이하로 떨어지고 있습니다. NSAIDs와 코르티코스테로이드의 경우, 임상 가이드라인에서 만성적인 사용이 점점 더 권장되지 않기 때문에 장기적인 가치에 대한 기여는 제한적입니다. 한편, 식이 유래 퓨린체를 대사하는 마이크로바이옴 유래 효소는 1상 시험의 안전성 결과가 양호하다면 생물학적 제를 대체할 수 있는 잠재적인 경구용 치료제로 떠오르고 있습니다. 그러나 마이크로바이옴 치료의 규제적 평가지표에 대한 FDA의 가이드라인이 부족하다는 점은 개발사들에게 큰 도전이 되고 있습니다. 또한, 페북소스타트 제네릭 의약품 세계 시장 진입이 가속화되고 있는 가운데, 특허 만료가 임박함에 따라 기존의 크산틴옥시다아제 억제 전략을 넘어서는 혁신이 절실히 필요함을 강조하고 있습니다.

지역별 분석

북미는 2025년 세계 통풍 치료제 시장 규모의 42.43%를 차지했습니다. 미국 일부 주에서 40%를 상회하는 높은 비만 유병률과 메디케어 파트 B의 정맥주사형 생물학적 제에 대한 메디케어 파트 B 적용이 프리미엄 수요를 뒷받침하고 있습니다. 민간 보험사들은 병원 운영비용을 절감하기 위해 외래 수액센터와 계약을 맺어 치료 장소의 선택권을 넓히고 있습니다. 캐나다의 공공 의료 시스템에서는 제네릭 의약품의 도입이 빠르지만, 민간 보험 플랜 외에는 바이오 의약품의 보급이 늦어 환자들의 접근성에 격차가 발생하고 있습니다. 멕시코는 여전히 가격 민감도가 높고, 제네릭 알로퓨리놀이 주류를 이루고 있으며, 바이오의약품은 대도시권 전문병원에 국한되어 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 8.43%로 성장을 견인할 것으로 예측됩니다. 중국의 통풍 환자 수는 2025년 1,700만 명을 넘어섰으며, 해산물과 알코올 섭취가 가장 많은 부유한 해안 지방에 집중되어 있습니다. 일본은 전 국민 건강보험과 '목표치 달성 요법'의 조기 도입의 혜택을 받고 있으며, 전 세계적으로 안전성에 대한 우려에도 불구하고 펩콕소스타트의 판매는 견조한 성장세를 보이고 있습니다. 인도에는 여전히 진단 격차가 존재합니다. 류마티스 전문의의 밀도는 인구 10만 명당 0.1명 이하이며, 브랜드 생물의약품의 가격은 월수입을 초과하는 경우도 흔합니다. 그러나 도시지역 원격 류마티스 진료 시범사업을 통해 미충족 수요가 점차 해소되기 시작했습니다.

유럽의 상환심사기관(NICE, 독일의 G-BA 등)은 생물학적 제에 대해 엄격한 비용효과성 검사를 시행하고 있습니다. 페그로티카세 접근은 경구 요법에 반응하지 않는 경우에만 가능하며, 투여량이 제한되어 있습니다. 남유럽 시장에서는 저가의 콜히친이 선호되고 있으며, 프랑스에서는 2024년 특허 만료에 따라 지역 약국에서 페북소스타트 제네릭 의약품의 판매가 호조를 보이고 있습니다. 동유럽에서는 수요가 증가하고 있지만, 전문의에 대한 접근성이 제한적이고 환자 부담금에 대한 제약이 걸림돌로 작용하고 있습니다. 중동 및 아프리카의 수익은 미미합니다. 걸프 지역에서는 서유럽와 유사한 치료 패턴을 보이는 반면, 사하라 이남 시장에서는 아직 초기 단계에 머물러 있습니다. 남미에서는 브라질과 아르헨티나를 중심으로 공적 의약품 목록에서 제네릭 의약품이 상환 대상이며, 환자 지원 프로그램을 통해 생물학적 제 비용 부담의 격차를 해소하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Gout Therapeutics Market size is projected to be USD 4.24 billion in 2025, USD 4.52 billion in 2026, and reach USD 6.67 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031.

Demand is being driven by an aging population, increasing cases of obesity-related hyperuricemia, and updated clinical guidelines that emphasize treat-to-target serum urate thresholds. The introduction of biologics for treatment-refractory conditions is expanding therapeutic options for physicians while enabling premium pricing opportunities. At the same time, fixed-dose oral combinations are positioned to protect market share as generic price erosion pressures margins. Digital monitoring tools, integrating smartphone urate meters with algorithm-based flare prediction, are accelerating diagnostics and aligning with payer strategies to reduce costly emergency department visits. However, growth prospects are tempered by cardiovascular safety warnings linked to febuxostat, payer-imposed prior-authorization requirements for pegloticase, and increasing generic competition within the xanthine oxidase inhibitor class.

Global Gout Therapeutics Market Trends and Insights

Rising Disease Prevalence Due to Aging and Obesity

By 2025, the global prevalence of gout reached 41 million cases, with high-income economies experiencing the fastest growth due to obesity rates exceeding 30%. Hyperinsulinemia reduces renal urate clearance, while fructose metabolism accelerates purine catabolism, collectively driving higher serum urate levels. In China, shifting urban dietary preferences toward red meat and sugary beverages led to a twofold increase in gout diagnoses between 2015 and 2024. The demographic profile of gout patients has also evolved, with cases now commonly emerging in individuals in their thirties and forties, rather than in men in their sixties as in historical trends. This demographic shift is expanding the treated population annually and extending the duration of therapeutic interventions. In Japan, 2025 health statistics rank gout among the top ten chronic outpatient conditions for men over 50, equating its prevalence with that of hypertension and diabetes.

Adoption of Evidence-Based Urate-Lowering Treatment Guidelines

The American College of Rheumatology's 2024 update establishes serum urate targets of <6 mg/dL for all gout patients and <5 mg/dL for those with tophi. Similarly, European guidelines emphasize the early initiation of xanthine oxidase inhibitors within weeks of diagnosis, replacing prior wait-and-see approaches. A 2025 Medicare claims analysis highlights a significant improvement: 68% of newly diagnosed U.S. patients initiated urate-lowering therapy within 90 days, compared to 42% in 2019. Fixed-dose oral combinations, designed to align with guideline-recommended dual therapy, are progressing through late-stage pipelines, although regulatory bodies require evidence of superiority over titrated monotherapy. In Germany and the United Kingdom, reimbursement frameworks now link rheumatologist incentives to the electronic documentation of serum-urate targets, driving the adoption of point-of-care testing devices.

Safety Concerns with Existing and Emerging Therapies

Febuxostat carries a boxed cardiovascular warning after the CARES trial showed a 34% rise in cardiac death versus allopurinol. The EMA's 2024 label update restricts use to second-line therapy, redirecting EU prescriptions toward allopurinol. Pegloticase requires infusion-center monitoring because of anaphylaxis, adding USD 1,500-2,000 in facility fees per dose. Colchicine overdoses in renally impaired patients prompted a 2025 FDA safety alert, spotlighting its narrow therapeutic index. These signals lengthen payer approval cycles, with prior-authorization delays averaging 12 days and contributing to patient attrition before therapy begins.

Other drivers and restraints analyzed in the detailed report include:

- Introduction of Novel Mechanisms of Action

- Expansion of Digital Health and Tele-Rheumatology Channels

- Suboptimal Patient Adherence to Long-Term Gout Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Xanthine oxidase inhibitors, dominated by the widespread use of allopurinol and selective utilization of febuxostat in cases with manageable cardiovascular risks, captured 46.34% of the gout therapeutics market revenue in 2025. Uricosurics are projected to grow at a strong 9.54% CAGR, driven by the increasing adoption of combination treatment protocols and the anticipated launch of next-generation URAT1 antagonists with improved renal safety profiles. Although recombinant uricase accounted for less than 5% of the market size in 2025, it delivered significant value, supported by Krystexxa's premium pricing of approximately USD 18,000 per month. Furthermore, IL-1 targeted agents, such as canakinumab, are addressing the flare-prophylaxis segment for patients intolerant to NSAIDs and colchicine, thereby expanding treatment options without directly reducing urate levels.

Pricing pressures are reshaping the oral therapeutics segment, with colchicine's generic price dropping below USD 0.50 per tablet in most markets. NSAIDs and corticosteroids contribute limited long-term value as clinical guidelines increasingly discourage their chronic use. Meanwhile, microbiome-based enzymes that metabolize dietary purines are emerging as potential oral alternatives to biologics, contingent on successful phase-I safety outcomes. However, the lack of FDA guidance on regulatory endpoints for microbiome therapeutics presents a significant challenge for sponsors. With additional febuxostat generics entering global markets, the impending patent cliffs highlight the critical need for innovation beyond traditional xanthine oxidase inhibition strategies.

The Gout Therapeutics Market Report is Segmented by Drug Class (Xanthine Oxidase Inhibitors, and More), Route of Administration (Oral and Injectable), Disease Type (Acute Gout, Chronic Refractory Gout, and Tophaceous Gout), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.43% of 2025 global gout therapeutics market value. High obesity prevalence above 40% in several U.S. states and Medicare Part B coverage for infused biologics sustain premium demand. Private payers are expanding site-of-care options, contracting with ambulatory-infusion centers to trim hospital overhead. Canada's publicly funded systems list generics readily, but biologic uptake lags outside private plans, creating disparate patient access. Mexico remains price-sensitive; generic allopurinol dominates, with biologics confined to metropolitan specialty hospitals.

Asia-Pacific is forecast to lead growth at an 8.43% CAGR through 2031. China's gout population exceeded 17 million in 2025, clustered along affluent coastal provinces where seafood and alcohol intake are highest. Japan benefits from universal insurance and early adoption of treat-to-target practice, supporting steady febuxostat sales despite global safety concerns. India's diagnosis gap persists; rheumatologist density is under 0.1 per 100,000 inhabitants, and branded biologics often exceed monthly household income. However, tele-rheumatology pilots in urban centers are beginning to chip away at unmet need.

Europe's reimbursement gatekeepers, including NICE and Germany's G-BA, subject biologics to stringent cost-effectiveness tests. Pegloticase access is restricted to oral-therapy failures, capping volume. Southern European markets favor low-cost colchicine, while France's community pharmacies report brisk generic febuxostat turnover following 2024 patent expiry. Eastern Europe shows nascent demand, handicapped by limited specialist access and share-of-wallet constraints. The Middle East and Africa contribute modest revenue; Gulf states mirror Western therapy patterns among expatriate populations, whereas sub-Saharan markets remain early in epidemiologic transition. South America centers on Brazil and Argentina, where public formularies reimburse generics, and patient-assistance programs bridge affordability gaps for biologics.

- Arthrosi Therapeutics

- AstraZeneca (Ardea Biosciences)

- Atom Bioscience

- Boehringer Ingelheim

- Hanmi Pharmaceutical

- Horizon Biosciences (Verinurad)

- Horizon Therapeutics (Amgen)

- JW Pharmaceutical

- Mitsubishi Tanabe Pharma

- Novartis

- Pfizer

- Protalix BioTherapeutics

- Regeneron Pharmaceuticals

- Sanofi

- Selecta Biosciences

- Sobi

- Takeda Pharmaceutical Co.

- Teijin Pharma

- UCB

- XORTX Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Disease Prevalence Due to Aging and Obesity

- 4.2.2 Adoption of Evidence-Based Urate-Lowering Treatment Guidelines

- 4.2.3 Introduction of Novel Mechanisms of Action

- 4.2.4 Expansion of Digital Health and Tele-Rheumatology Channels

- 4.2.5 Advances in Personalized Medicine and Biomarker Monitoring

- 4.2.6 Emergence of Microbiome-Based Therapeutics and Enzyme Therapies

- 4.3 Market Restraints

- 4.3.1 Safety Concerns with Existing and Emerging Therapies

- 4.3.2 Suboptimal Patient Adherence to Long-Term Gout Management

- 4.3.3 Generic Competition and Price Erosion Reducing Profitability

- 4.3.4 Regulatory Actions Limiting Promotion of High-Purine Diets and Alcohol

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat Of New Entrants

- 4.7.2 Bargaining Power Of Suppliers

- 4.7.3 Bargaining Power Of Buyers

- 4.7.4 Threat Of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Xanthine Oxidase Inhibitors

- 5.1.2 Uricosurics

- 5.1.3 Recombinant Uricase

- 5.1.4 IL-1 Inhibitors

- 5.1.5 Colchicine

- 5.1.6 NSAIDs

- 5.1.7 Corticosteroids

- 5.1.8 Other Classes

- 5.2 By Route Of Administration

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.3 By Disease Type

- 5.3.1 Acute Gout

- 5.3.2 Chronic Refractory Gout

- 5.3.3 Tophaceous Gout

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)}

- 6.3.1 Arthrosi Therapeutics

- 6.3.2 AstraZeneca (Ardea Biosciences)

- 6.3.3 Atom Bioscience

- 6.3.4 Boehringer Ingelheim

- 6.3.5 Hanmi Pharmaceutical

- 6.3.6 Horizon Biosciences (Verinurad)

- 6.3.7 Horizon Therapeutics (Amgen)

- 6.3.8 JW Pharmaceutical

- 6.3.9 Mitsubishi Tanabe Pharma

- 6.3.10 Novartis AG

- 6.3.11 Pfizer Inc.

- 6.3.12 Protalix BioTherapeutics

- 6.3.13 Regeneron Pharmaceuticals

- 6.3.14 Sanofi

- 6.3.15 Selecta Biosciences

- 6.3.16 Sobi

- 6.3.17 Takeda Pharmaceutical Co.

- 6.3.18 Teijin Pharma

- 6.3.19 UCB Pharma

- 6.3.20 XORTX Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment