|

시장보고서

상품코드

2044175

하이퍼컨버지드 인프라 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hyper-Converged Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

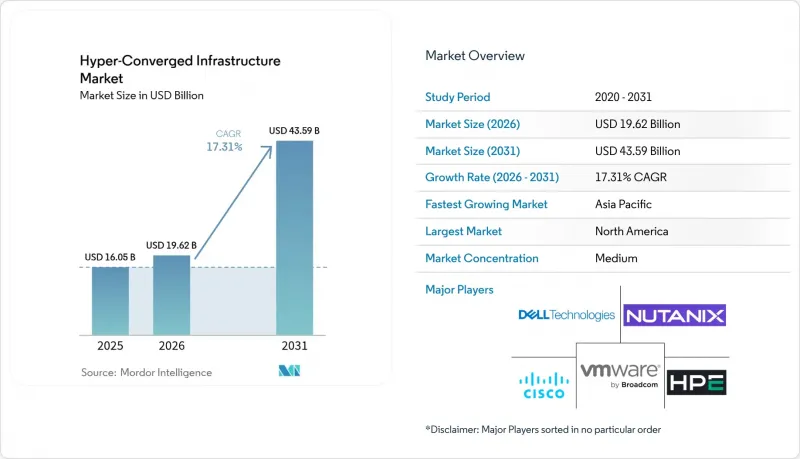

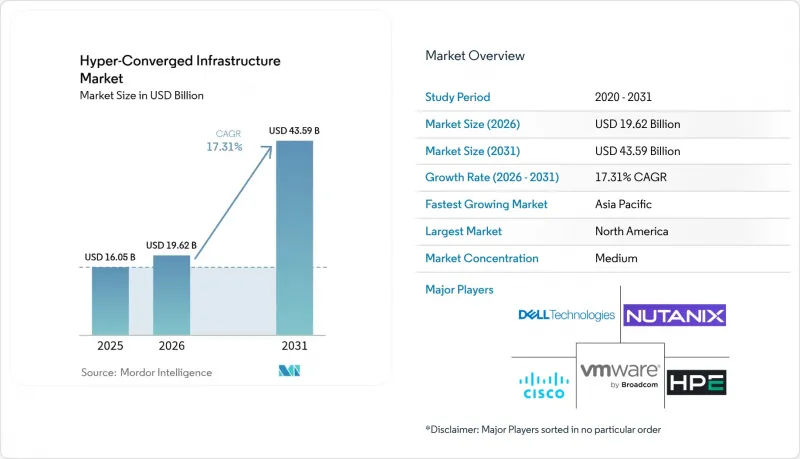

하이퍼컨버지드 인프라 시장 규모는 2025년 160억 5,000만 달러에서 2026년에는 196억 2,000만 달러로 확대되어 2031년까지 435억 9,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 17.31%로 성장할 전망입니다.

브로드컴의 2024년 VMware 영구 라이선스 폐지 결정으로 20년간의 가상화 경제성이 바뀌면서 x86 서버 통합 이후 가장 큰 규모의 플랫폼 전환 물결이 일어나고 있으며, 기업 구매 담당자들은 리프레시 주기를 앞당기고 있습니다. 하고 있습니다. 정부 주도의 AI 도입 의무화, 유통업계의 엣지 구축, RISC-V 어플라이언스의 등장으로 하드웨어의 규모가 아닌 오픈소스의 유연성을 무기로 경쟁하는 신규 시장 진출기업들이 등장하고 있으며, Nutanix, Microsoft Azure Stack HCI, Microsoft Azure Stack HCI, Nutanix Scale Computing에 우위가 기울고 있습니다. 구매자들은 특히 전력 요금과 전력망 대기 시간이 전력 예산을 제한하는 상황에서 소프트웨어 정의 스토리지, 쿠버네티스 네이티브 오케스트레이션, NVMe의 성능 밀도를 결정적인 차별화 요소로 꼽고 있습니다. 이러한 상황을 종합하면, 민첩한 공급업체는 점유율을 확대할 수 있는 위치에 있고, 기존 3층형 공급업체는 축소되어 가격에 민감한 틈새 시장을 보호하게 될 것입니다.

세계 하이퍼컨버지드 인프라 시장 동향과 인사이트

데이터센터 통합의 물결

금융 서비스, 의료, 정부 기관은 분산된 3층 스택을 컨버지드 노드로 통합하여 바닥 면적을 회수하고 냉각 비용을 크게 절감하고 있습니다. Nutanix의 발표에 따르면, 대안을 고려하는 VMware 고객의 85%가 락인 리스크와 예측 불가능한 가격 책정을 이유로 꼽았으며, 이 중 48%는 2024년 내로 개념증명(PoC)을 시작할 계획이라고 밝혔습니다. JPMorgan Chase는 2025년까지 1,200개 지점을 Azure Stack HCI로 전환하여 연간 유지보수 비용을 1,800만 달러 절감했습니다. Mayo Clinic은 전자의무기록을 Nutanix로 전환한 후 15개 캠퍼스에서 99.99%의 가동률을 달성하고 재해복구용 하드웨어를 60% 절감했습니다. 규제 산업의 갱신 주기가 3-5년이기 때문에 전환이 시작되면 하이퍼컨버지드 인프라 시장은 장기적인 전망을 누릴 수 있습니다.

클라우드 네이티브 워크로드 도입 급증

컨테이너화된 용도는 이미 기업의 신규 워크로드의 90%를 차지하고 있으며, 98%의 조직이 하이브리드 모드에서 쿠버네티스를 운영하고 있습니다. Dell의 VxRail 8.0에는 Red Hat OpenShift가 내장되어 있어 외부 어레이 없이도 스테이트풀 컨테이너를 위한 영구적인 스토리지를 구현할 수 있습니다. Microsoft는 Azure Arc의 거버넌스를 Azure Stack HCI로 확장하여 관리자가 수천 개의 엣지 클러스터에 통일된 정책을 적용할 수 있도록 했습니다. 멀티클러스터의 라이프사이클 관리에 따른 운영 부담으로 인해 턴키 노드의 매력이 높아지고 있습니다. 특히 GenAI를 시범 도입한 기업의 85%가 벡터 데이터베이스에 대한 레이턴시가 거의 없는 On-Premise LLM 추론을 요구하고 있는 상황에서는 더욱 그렇다. 그 결과, 하이퍼컨버지드 인프라 시장은 데이터 주권 및 성능 제약으로 인해 퍼블릭 리전에 배치할 수 없는 클라우드 네이티브 워크로드의 기본 기반이 되고 있습니다.

하이엔드 워크로드에서 노드 단위의 확장성 한계에 대한 자료입니다.

대부분의 하이퍼컨버지드 플랫폼은 클러스터를 64개 호스트, 호스트당 200개의 VM으로 제한하고 있어 AI 트레이닝, HPC 또는 수 페타바이트 규모의 데이터베이스에 대한 적합성을 제한하고 있습니다. VMware vSAN, Dell VxRail, Nutanix도 메타데이터의 일관성을 유지하기 위해 유사한 제한을 두고 있습니다. 이에 클리블랜드 클리닉은 8페타바이트 규모의 EHR 환경에 컴포저블 인프라를 도입했습니다. 수백 개의 GPU에 걸친 올 리듀스 연산에서는 여전히 NVIDIA DGX급 클러스터가 유리하며, CXL 지원 메모리 패브릭이 성숙하기 전까지는 하이엔드 시장에서 하이퍼컨버지드 인프라의 점유율 확대는 제한적일 것으로 보입니다.

부문 분석

2025년 기준 하드웨어가 하이퍼컨버지드 인프라 시장의 58.84%를 차지했지만, 소프트웨어 분야는 2031년까지 연평균 복합 성장률(CAGR) 18.21%로 확대될 것으로 예측됩니다. Nutanix의 GPT-in-a-Box II와 Microsoft의 Azure Arc와의 통합은 워크로드를 전용 하이퍼바이저에서 분리하는 턴키 오케스트레이션 스택에 대한 수요를 상징합니다. 컨테이너 스토리지 인터페이스(CSI)의 도입으로 개발자들이 스토리지를 코드로 취급할 수 있게 되면서, 어레이 중심의 설계에서 소프트웨어 중심으로의 전환이 가속화되고 있습니다.

다년간의 감가상각 스케줄을 실행하는 기존 인프라에서 하드웨어는 여전히 필수적이지만, 어플라이언스의 매출 비중은 점차 지속적인 소프트웨어 구독으로 전환되고 있습니다. 서비스가 이 간극을 메워주고 있습니다. 마이그레이션 도구, AI 모델 최적화, 컴플라이언스 감사는 자본 예산을 늘리지 않고도 평균 거래액을 증가시키는 프리미엄 요금이 책정되어 있습니다. 구매자들이 On-Premise 환경에서 클라우드와 같은 유연성을 추구함에 따라, 소프트웨어 구독과 연계된 하이퍼컨버지드 인프라 시장 규모는 전체 시장 성장률을 상회하는 속도로 계속 확대될 것입니다.

2025년에는 전문 서비스가 전체 수익의 64.98%를 차지했습니다. 그러나 매니지드 서비스는 CAGR 17.88%로 증가하여 중소기업의 종량제 운영에 대한 선호도가 높아지고 있음을 보여줍니다. 이러한 추세는 중소기업의 운영 요구에 부합하는 유연하고 확장 가능한 솔루션에 대한 수요가 증가하고 있음을 보여줍니다. HPE의 GreenLake는 2024 회계연도 4분기에 16억 달러의 놀라운 매출을 달성했으며, 이 중 하이퍼컨버지드 노드가 35%를 차지했습니다. 이 같은 실적은 기업들이 IT 환경을 최적화하기 위해 하이퍼컨버지드 인프라 솔루션의 채택이 확대되고 있음을 반영합니다.

매니지드 서비스 제공업체는 패치 적용, 용량 텔레메트리, 재해복구 등 일련의 서비스를 제공하며, 노드당 월 500-2,000달러의 요금을 책정하고 있습니다. 이를 통해 예측 불가능한 설비투자(CAPEX)를 안정적인 운영비(OPEX)로 전환하여 기업은 재무적 예측 가능성과 관리성을 높일 수 있습니다. 260개 매장을 운영하는 Royal Farms는 현장 기술자의 필요성을 없애고 연간 180만 달러의 비용을 절감하는 데 성공했습니다. 이 사례는 분산형 사업을 전개하는 기업에서 매니지드 서비스의 비용 절감 가능성을 여실히 보여주고 있습니다. 원격 관리 API가 성숙함에 따라 하이퍼컨버지드 인프라(HCX) 분야의 초점이 변화하고 있습니다. 업계는 단발성 기기 판매로 인한 매출 총이익에 의존하지 않고, 지속적인 수익(Annuity Revenue)으로 전환하고 있으며, 이러한 움직임은 벤더들의 밸류에이션 배율을 크게 끌어올리고 있습니다. 이러한 전환은 벤더의 수익 안정성을 향상시킬 뿐만 아니라 장기적인 가치와 지원을 원하는 고객의 진화하는 요구에 부합하는 것입니다.

지역별 분석

2025년 북미는 전 세계 매출의 39.93%를 차지했습니다. 이는 미국 연방정부의 제로 트러스트 의무화, 하이퍼스케일러의 엣지 허브 설립(Verizon이 1,000개 저지연 사이트 운영)에 힘입은 것입니다. 이러한 의무화와 허브는 하이퍼컨버지드 인프라 시장에서 이 지역의 우위에 크게 기여하고 있습니다. 한편, 캐나다의 엄격한 데이터 주권법에 따라 은행과 병원은 클라우드 네이티브 거버넌스 프레임워크에 따라 On-Premise에서 워크로드를 관리할 수밖에 없는 상황입니다. 이러한 규제 환경으로 인해 차입 비용 상승에도 불구하고, 컴플라이언스와 운영 효율성을 우선시하는 조직들이 하이퍼컨버지드 인프라 솔루션에 대한 수요는 여전히 높은 수준을 유지하고 있습니다.

아시아태평양은 상승세를 보이고 있으며, CAGR은 18.69%로 성장을 지속하고 있습니다. 이 지역의 성장은 중국의 자국산 가상화 스택 개발, 인도의 통신 핵심 네트워크 현대화 노력, 일본의 프라이빗 5G 네트워크를 통한 공장 자동화 노력에 힘입어 성장하고 있습니다. 특히 화웨이의 'FusionCube'는 중국 국가 프로젝트의 최전선에 있으며, 시장에서 화웨이의 우위를 보여주고 있습니다. 마찬가지로, Reliance Jio는 1만 개의 통신 타워에 Nutanix를 도입하여 인도의 통신 인프라 확장에 집중하고 있음을 보여주고 있습니다. 또한, 도요타는 조립 공장에 후지쯔의 PRIMEFLEX를 도입하여 일본이 산업 자동화를 위한 첨단 기술 활용에 주력하고 있음을 보여주고 있습니다. 이 지역의 다양한 멀티 벤더 환경은 혁신을 가속화할 뿐만 아니라 벤더 전환의 장벽을 높여 경쟁적이고 역동적인 시장 환경을 조성하고 있습니다.

유럽에서는 프랑크푸르트, 런던, 암스테르담, 파리, 더블린을 포함한 FLAP-D 대도시권에서 7-10년의 전력망 대기자 명단에 직면해 있습니다. 이러한 문제로 인해 구매자들은 전력 효율이 높은 ARM 및 RISC-V 노드로 전환하고, 에너지 제약을 완화하기 위해 코로케이션 제휴를 추진하고 있습니다. 독일은 탄탄한 자동차 AI 이니셔티브에 힘입어 이 지역 지출의 28%를 차지하며 첨단 기술 도입에 있어 선도적인 역할을 하고 있습니다. 한편, 프랑스는 원자력을 통한 기저부하 전력을 활용하여 소버린 클라우드의 워크로드를 유치하여 시장의 주요 기업로 자리매김하고 있습니다. 북유럽은 수력 발전과 폐열 재사용을 위한 노력으로 하이퍼스케일 기업들의 관심을 끌고 있지만, 요금 상승으로 인해 북유럽 하이퍼컨버지드 인프라 시장의 CAGR은 여전히 0.7% 하락할 것으로 예측됩니다. 이러한 요인들이 복합적으로 작용하여 유럽 시장 역학을 형성하고 있으며, 이해관계자들에게 기회와 도전을 동시에 제공합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The hyper-converged infrastructure market size is expected to increase from USD 16.05 billion in 2025 to USD 19.62 billion in 2026 and reach USD 43.59 billion by 2031, growing at a CAGR of 17.31% over 2026-2031.

Enterprise buyers are accelerating refresh cycles because Broadcom's 2024 decision to retire VMware perpetual licenses upended twenty years of virtualization economics and triggered the largest platform-migration wave since x86 server consolidation began. Sovereign-AI mandates, retail edge roll-outs, and the arrival of RISC-V appliances have drawn new entrants that compete on open-source flexibility rather than raw hardware scale, tilting advantage toward Nutanix, Microsoft Azure Stack HCI, and Scale Computing. Buyers view software-defined storage, Kubernetes-native orchestration, and NVMe performance density as decisive differentiators, especially where electricity prices or grid queues cap power budgets. Taken together, these conditions position agile vendors to enlarge share while incumbent three-tier suppliers defend shrinking, price-sensitive niches.

Global Hyper-Converged Infrastructure Market Trends and Insights

Data-center Consolidation Wave

Financial-services, healthcare, and government agencies are collapsing scattered three-tier stacks into converged nodes to reclaim floor space and slash cooling overhead. Nutanix disclosed that 85% of VMware customers assessing alternatives cited lock-in risk and unpredictable pricing, prompting 48% to launch proofs of concept during 2024. JPMorgan Chase migrated 1,200 branches to Azure Stack HCI in 2025, cutting annual maintenance by USD 18 million. Mayo Clinic achieved 99.99% uptime across 15 campuses after shifting electronic health records to Nutanix, reducing disaster-recovery hardware 60%. Because refresh windows in regulated industries run three to five years, the hyper-converged infrastructure market enjoys durable visibility once conversions begin.

Surging Cloud-native Workload Adoption

Containerised applications already represent 90% of new enterprise workloads, with 98% of organizations running Kubernetes in hybrid mode. Dell's VxRail 8.0 embeds Red Hat OpenShift, enabling persistent storage for stateful containers without external arrays. Microsoft extended Azure Arc governance to Azure Stack HCI, letting administrators impose uniform policy across thousands of edge clusters. The operational burden of multicluster lifecycle management makes turnkey nodes attractive, especially where 85% of enterprises piloting GenAI demand on-prem LLM inference with near-zero latency to vector databases. Consequently, the hyper-converged infrastructure market is becoming the default substrate for cloud-native workloads that cannot reside in public regions because of data-sovereignty or performance constraints.

Per-node Scalability Ceiling for High-end Workloads

Most hyper-converged platforms cap clusters at 64 hosts and 200 VMs per host, limiting suitability for AI training, HPC, or multi-petabyte databases. VMware vSAN, Dell VxRail, and Nutanix enforce similar boundaries to maintain metadata consistency. Cleveland Clinic therefore selected composable infrastructure for its 8-petabyte EHR footprint. All-reduce operations across hundreds of GPUs still favour NVIDIA DGX-class clusters, curbing high-end share for the hyper-converged infrastructure market until CXL-enabled memory fabrics mature.

Other drivers and restraints analyzed in the detailed report include:

- Lower TCO Versus Legacy Three-tier Architecture

- Edge Computing Roll-outs in Telco and Retail

- Vendor Lock-in Concerns for Enterprise Buyers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software category is expanding at an 18.21% CAGR through 2031, even though hardware still held 58.84% of the hyper-converged infrastructure market share in 2025. Nutanix's GPT-in-a-Box II and Microsoft's Azure Arc integration exemplify demand for turnkey orchestration stacks that decouple workloads from proprietary hypervisors. Container Storage Interface adoption lets developers treat storage as code, accelerating software substitution for array-centric designs.

Hardware remains essential for latent installed bases executing multi-year depreciation schedules, yet appliance revenue is gradually ceding mix toward recurring software subscriptions. Services bridge the gap; migration tooling, AI model optimization, and compliance audits command premium rates that elevate average deal value without inflating capital budgets. As buyers pursue cloud-like flexibility on-prem, the hyper-converged infrastructure market size attached to software subscriptions will continue compounding above overall growth.

In 2025, professional services accounted for 64.98% of total revenue. However, managed services are on the rise, boasting a 17.88% CAGR, underscoring the growing preference of SMBs for pay-as-you-go operations. This trend highlights the increasing demand for flexible and scalable solutions that align with the operational needs of small and medium-sized businesses. HPE's GreenLake achieved a notable USD 1.6 billion in revenue for Q4 FY2024, with hyper-converged nodes contributing to 35% of this figure. This performance reflects the growing adoption of hyper-converged infrastructure solutions as businesses seek to optimize their IT environments.

Managed-service providers offer a suite of services, including patching, capacity telemetry, and disaster recovery, charging between USD 500 to 2,000 monthly per node. This approach transforms unpredictable capital expenditures into consistent operational expenses, providing businesses with greater financial predictability and control. Royal Farms, with its deployment across 260 stores, successfully eliminated the need for on-site technicians, resulting in annual savings of USD 1.8 million. This case study exemplifies the cost-saving potential of managed services for enterprises with distributed operations. With the maturation of remote management APIs, the hyper-converged infrastructure sector is shifting its focus. Instead of relying solely on one-time appliance gross margins, the industry is now leaning towards annuity revenue, a move that significantly boosts vendor valuation multiples. This transition not only enhances revenue stability for vendors but also aligns with the evolving needs of customers seeking long-term value and support.

The Hyper-Converged Infrastructure Market Report is Segmented by Component (Hardware, Software, and Services), Service (Professional, and Managed), Organization Size (Large Enterprise, and Small and Medium Enterprise), End-User Industry (IT and Telecommunication, BFSI, Healthcare, Retail, Government and Defence, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America accounted for 39.93% of global revenue, driven by U.S. federal zero-trust mandates and the establishment of hyperscaler edge hubs, with Verizon operating 1,000 low-latency sites. These mandates and hubs have significantly contributed to the region's dominance in the hyper-converged infrastructure market. Meanwhile, Canada's stringent data-sovereignty laws compel banks and hospitals to manage workloads on-premises, albeit under cloud-native governance frameworks. This regulatory environment has led to a sustained premium demand for hyper-converged infrastructure solutions, even in the face of rising borrowing costs, as organizations prioritize compliance and operational efficiency.

Asia-Pacific is on an upward trajectory, boasting an 18.69% CAGR. The region's growth is fueled by China's focus on developing indigenous virtualization stacks, India's efforts to modernize its telecommunications cores, and Japan's initiatives to automate factories through private 5G networks. Notably, Huawei's FusionCube is at the forefront of Chinese state projects, showcasing its dominance in the market. Similarly, Reliance Jio has expanded Nutanix across 10,000 towers, demonstrating India's commitment to scaling its telecommunications infrastructure. Additionally, Toyota has integrated Fujitsu's PRIMEFLEX into its assembly plants, highlighting Japan's focus on leveraging advanced technologies for industrial automation. This diverse multi-vendor landscape in the region not only accelerates innovation but also heightens the barriers to switching vendors, creating a competitive and dynamic market environment.

Europe grapples with 7-10 year grid queues in its FLAP-D metropolitan areas, which include Frankfurt, London, Amsterdam, Paris, and Dublin. This challenge is steering buyers towards more power-efficient ARM or RISC-V nodes and fostering co-location partnerships to mitigate energy constraints. Germany, driven by its robust automotive AI initiatives, represents 28% of the region's spending, underscoring its leadership in adopting advanced technologies. France, on the other hand, is capitalizing on its nuclear baseload energy to attract sovereign-cloud workloads, positioning itself as a key player in the market. While Nordic regions are drawing hyperscale attention with hydro and waste-heat recycling initiatives, rising tariffs are still curbing the hyper-converged infrastructure market's CAGR in the continent by 0.7%. These factors collectively shape Europe's market dynamics, presenting both opportunities and challenges for stakeholders.

- Nutanix Inc.

- Dell Technologies Inc.

- VMware Inc.

- Hewlett Packard Enterprise Development LP

- Cisco Systems Inc.

- Microsoft Corporation

- Huawei Technologies Co. Ltd.

- IBM Corporation

- NetApp Inc.

- Lenovo Group Limited

- Fujitsu Limited

- Hitachi Vantara LLC

- NEC Corporation

- Super Micro Computer Inc.

- Scale Computing Inc.

- StarWind Software Inc.

- DataCore Software Corporation

- Maxta Inc.

- Pivot3 Inc.

- Sangfor Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-center Consolidation Wave

- 4.2.2 Surging Cloud-native Workload Adoption

- 4.2.3 Lower TCO Versus Legacy Three-tier Architecture

- 4.2.4 Edge Computing Roll-outs in Telco and Retail

- 4.2.5 RISC-V and ARM Based HCI Appliances

- 4.2.6 Modular Data-center Demand in Emerging Africa

- 4.3 Market Restraints

- 4.3.1 Per-node Scalability Ceiling for High-end Workloads

- 4.3.2 Vendor Lock-in Concerns for Enterprise Buyers

- 4.3.3 Supply Chain Risk Around Custom ASICs

- 4.3.4 Escalating Datacenter Power Tariffs in Europe

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Service

- 5.2.1 Professional

- 5.2.2 Managed

- 5.3 By Organization Size

- 5.3.1 Large Enterprise

- 5.3.2 Small and Medium Enterprise

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunication

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Retail

- 5.4.5 Government and Defence

- 5.4.6 Rest of End-user Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nutanix Inc.

- 6.4.2 Dell Technologies Inc.

- 6.4.3 VMware Inc.

- 6.4.4 Hewlett Packard Enterprise Development LP

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Huawei Technologies Co. Ltd.

- 6.4.8 IBM Corporation

- 6.4.9 NetApp Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Fujitsu Limited

- 6.4.12 Hitachi Vantara LLC

- 6.4.13 NEC Corporation

- 6.4.14 Super Micro Computer Inc.

- 6.4.15 Scale Computing Inc.

- 6.4.16 StarWind Software Inc.

- 6.4.17 DataCore Software Corporation

- 6.4.18 Maxta Inc.

- 6.4.19 Pivot3 Inc.

- 6.4.20 Sangfor Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment