|

시장보고서

상품코드

2044176

일회용 주사기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Disposable Syringes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

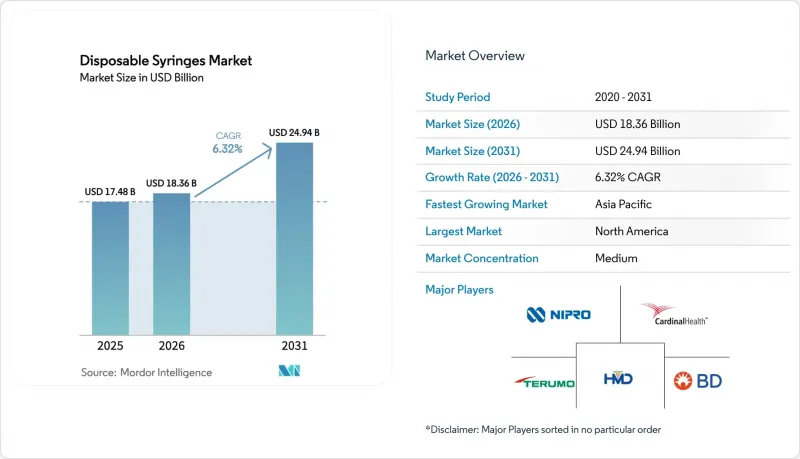

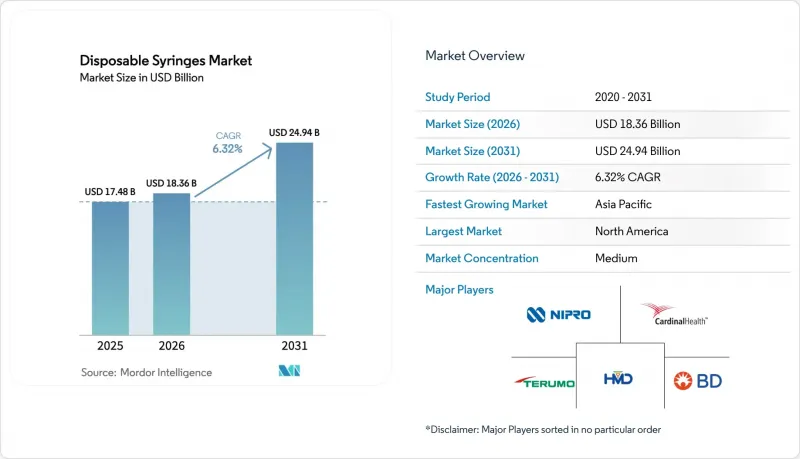

일회용 주사기 시장 규모는 2025년 174억 8,000만 달러에서 2026년에는 183억 6,000만 달러로 확대되어 2031년까지 249억 4,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 6.32%로 성장할 전망입니다.

일회용 안전 메커니즘을 권장하는 규제 요건, 중저소득 국가에서의 예방접종 활동의 지속, 생물학적 제제 및 GLP-1 수용체 작용제에서 프리필드 제제의 사용 확대 등이 현재의 성장을 뒷받침하고 있습니다. 병원의 구매량이 여전히 가장 많지만, 보험사가 환자의 자가 투약 키트 비용을 상환하고 원격 의료 플랫폼이 복약 순응도를 추적함에 따라 재택 진료는 점점 더 많은 추진력을 얻고 있습니다. 재료 선택도 유동적이며, 비용 측면에서 폴리프로필렌이 여전히 주류인 반면, 초기 단계의 생분해성 블렌드가 시험적으로 사용되기 시작했습니다. 경쟁 전략은 현재 생산 능력 확대, 생산 라인의 자동화, 바늘에 찔린 사고에 대한 법적 책임을 줄이고 공동 구매 계약을 체결하기 위해 차별화된 안전 기술에 중점을 두고 있습니다.

세계 일회용 주사기 시장 동향과 인사이트

전 세계 예방접종 및 부스터 접종 프로그램 확대

WHO의 '예방접종 아젠다 2030'은 필수 소아 백신 접종률 90%를 목표로 하고 있으며, 이 목표를 달성하기 위해서는 매년 최대 100억 개의 일회용 주사기가 필요합니다. 2023년'빅 캐치업'에서 5억 달러의 기부자 자금이 동원되었고, 2025년 자동 비활성화 주사기 출하량은 20억 개를 넘어섰습니다. 코로나19, 독감 및 MPOX(Monkeypox) 부스터 접종 프로그램으로 인해 일회용 의료기기가 표준 관행으로 자리 잡았습니다. 유니세프의 2025년 공급 부문은 자동 폐쇄형 주사기 주문이 22% 증가했으며, 그 중 65%가 중저소득 국가에 공급되고 있다고 지적했습니다. 제약회사는 현재 백신을 프리필드시린지에 결합하여 조제 오류를 줄이고 콜드체인 물류를 강화하는 등 백신을 미리 채워진 주사기에 결합하고 있습니다.

주사 요법이 필요한 만성 질환 증가

당뇨병, 류마티스 관절염, 다발성 경화증, 심혈관 질환을 합치면 15억 명 이상이 영향을 받고 있으며, 새로운 치료 프로토콜은 주사제가 주류를 이루고 있습니다. GLP-1 작용제는 2025년 500억 달러의 매출을 기록해, 노보 노디스크와 일라이 릴리는 프리필드시린지 생산 능력을 3분의 1 이상 확대했습니다. 미국 질병예방통제센터(CDC)의 집계에 따르면, 2024년 미국의 인슐린 사용자는 870만 명으로 연간 약 32억 주사기 단위의 인슐린을 소비하고 있습니다. 일본, 독일, 이탈리아는 고령화가 진행되어 65세 이상 환자가 주사제 처방의 60%를 차지하게 되면서 수요가 더욱 증가하고 있습니다.

엄격한 폐기물 및 플라스틱 폐기물 관리 규정

EU의 '일회용 플라스틱 지침'에 따라 회원국들은 생산자책임제도 도입을 확대 추진했습니다. 프랑스에서는 현재 주사기 공급업체가 지방자치단체의 날카로운 물건 회수 프로그램 비용의 절반을 부담하도록 의무화하고 있습니다. 독일 포장법에 따르면, 2028년까지 폴리프로필렌 의료기기에 30%의 재활용 소재를 포함하도록 의무화되어 있습니다. 캘리포니아주는 2025년 의료기기 스튜어드십법을 통과시켜 제조업체에 회수 프로그램 시행을 의무화했습니다. 컴플라이언스 비용은 대량 생산되는 기존 주사기의 수익률을 압박하고 있습니다.

부문 분석

2025년 기준, 안전형 일회용 주사기는 매출 점유율의 53.53%를 차지했습니다. 재사용 위험이 없고 WHO 표준을 준수하는 자동 폐쇄형 주사기는 2031년까지 연평균 복합 성장률(CAGR) 9.45%를 기록하며 다른 모든 형태를 능가할 것으로 예측됩니다. 비용을 중시하는 검사실에서는 여전히 기존 제품이 사용되고 있습니다. 개폐식 안전 설계는 신속한 폐기 및 법적 책임의 경감을 원하는 응급처치 부서에서 선호하고 있습니다. 프리필드 제품은 판매량은 적지만 현재 매출의 30% 이상을 차지하고 있습니다. 스마트 커넥티드 모델은 사이버 보안 검증으로 인해 제품화까지의 기간이 길어지고 있어 아직 시험 단계에 머물러 있습니다.

각 제조업체들은 단가 절감을 위해 64캐비티 금형과 자동 조립라인에 대한 투자를 진행하고 있습니다. 벡톤디킨슨앤컴퍼니(BD)의 'BD Integra'는 공동구매 계약을 통해 미국 병원 계약의 12%를 확보하며 기능 차별화가 점유율 확대로 이어진다는 것을 보여주고 있습니다. 2024년부터 2025년까지 1억 2,000만 달러의 벤처 펀딩을 유치한 것은 복약 순응도를 위해 클라우드 분석을 활용할 수 있는 커넥티드 디바이스에 대한 투자자들의 신뢰를 보여줍니다.

2025년 매출의 62.55%는 치료용 주사가 차지해, 피하 투여에 의존하는 당뇨병 및 종양학 치료 요법이 이를 주도할 것으로 예측됩니다. 예방접종용 주사는 팬데믹으로 인한 지연을 만회하려는 움직임으로 2031년까지 연평균 9.22% 성장할 것으로 예측됩니다. 채혈장치는 금액은 작지만 사용 빈도가 높은 분야입니다.

블록버스터급 단일클론항체의 피하투여 제형 변경으로 연간 약 5억 개의 주사기가 추가될 것으로 예측됩니다. 현장 진료 시 마이크로 샘플링은 정맥 채혈 수요를 점차적으로 빼앗아 갈 수 있지만, 그 도입은 여전히 자원이 풍부한 진료소에만 국한되어 있습니다.

'일회용 주사기 시장 보고서'는 제품 유형(재래식, 안전형(개폐식 안전 주사기 등), 기타), 용도(예방접종, 치료, 채혈), 최종 사용자(병원, 혈액센터, ASC, 재택의료), 재료(플라스틱, 유리, 생분해성), 기술(수동형, 기타), 지역(북미, 기타), 기타로 분류됩니다. 지역(북미, 기타)으로 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

2025년 북미는 전 세계 매출의 37.12%를 차지했습니다. 벤더관리재고(VMI) 계약을 통해 미국 전략국가비축물자(SNS)는 1억 5,000만 개의 주사기를 롤링베이스로 보유할 수 있게 되어 안정적인 수주 기반이 형성되어 있습니다. CMS(미국 의료보험의료서비스센터)의 상환제도는 안전하게 설계된 의료기기를 우대하고 있으며, 재택의료에서의 채택을 가속화하고 있습니다. 캐나다는 2024년 국가 비상 전략 비축량을 8,000만 병으로 확대했습니다. 멕시코 IMSS는 2025년까지 1억 2,000만 개의 주사기를 조달하고, 국내 산업 활성화를 위해 현지 조립 조항을 포함시켰습니다.

아시아태평양은 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 8.03%로 예측됩니다. 힌두스탄 주사기 및 의료기기 회사는 5,000만 달러의 투자를 통해 자동 비활성화 기능을 갖춘 제품의 생산 능력을 두 배로 늘리고 유니세프(UNICEF) 및 WHO의 입찰 수주를 목표로 하고 있습니다. 니프로의 웨일즈 확장으로 유럽 공급망에 12억 개가 추가되었습니다. 중국 국가약품감독관리국(NMPA)은 2024년 기준을 WHO의 기준과 일치시켜 현지 제조업체에게 세계 시장 진출의 문을 열어주었습니다. 일본의 고령화에 따라 재택 인슐린 투여 및 GLP-1 요법용 프리필드 디바이스에 대한 수요가 증가하고 있습니다.

유럽에서는 MDR 클래스 IIa에 대한 적합성이 의무화되어 신규 진입 장벽이 높아지고 있습니다. 독일, 프랑스, 영국, 이탈리아, 스페인이 유럽 수요의 3분의 2를 차지합니다. 영국 국민보건서비스(NHS)는 2030년까지 의료기기의 25%를 바이오 제품으로 만드는 것을 목표로 하고 있습니다. 프랑스 법령에 따라 공급업체는 날카로운 물건 회수 비용의 절반을 부담해야 하며, 단위당 비용이 증가하고 있습니다. 중동 및 아프리카에서는 공급 체제가 구축되어 있습니다. GCC 국가들은 2025년 8,000만 개의 주사기를 주문했고, 남아공은 BD사와 1억 5,000만 개 규모의 계약을 체결했습니다. 남미에서는 브라질의 SUS가 2억 병을 구매했고, 아르헨티나는 2024년 예방접종 계획에 따라 대상 범위를 확대했습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Disposable Syringes Market size is expected to increase from USD 17.48 billion in 2025 to USD 18.36 billion in 2026 and reach USD 24.94 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

Regulatory mandates that favor single-use safety mechanisms, continuing immunization drives in low- and middle-income countries, and greater use of prefilled formats for biologics and GLP-1 receptor agonists anchor current growth. Hospitals still purchase the largest volumes, yet home-based care is gathering pace as payers reimburse patient self-administration kits and telehealth platforms track adherence. Material selection is also in flux as polypropylene remains dominant on cost grounds while early biodegradable blends enter pilot use. Competitive strategy now centers on capacity expansions, line automation, and differentiated safety technologies that lower needlestick liability and win group-purchasing contracts.

Global Disposable Syringes Market Trends and Insights

Rising Global Immunization & Booster Programs

WHO's Immunization Agenda 2030 targets 90% coverage for essential childhood vaccines, a goal that demands up to 10 billion single-use syringes every year.The 2023 "Big Catch-Up" mobilized USD 500 million in donor funding and lifted 2025 auto-disable syringe shipments above 2 billion units. Booster programs for COVID-19, influenza, and mpox cement single-use devices as standard practice. UNICEF's 2025 Supply Division noted a 22% jump in auto-disable orders, with 65% flowing to low- and middle-income countries. Pharmaceutical companies now bundle vaccines in prefilled syringes, reducing reconstitution errors and tightening cold-chain logistics.

Increasing Prevalence of Chronic Diseases Requiring Injectable Therapies

Diabetes, rheumatoid arthritis, multiple sclerosis, and cardiovascular diseases together affect more than 1.5 billion people, and injectables dominate new treatment protocols. GLP-1 agonists generated USD 50 billion in 2025 sales, prompting Novo Nordisk and Eli Lilly to expand prefilled syringe capacity by over one-third. The CDC counted 8.7 million U.S. insulin users in 2024, consuming roughly 3.2 billion syringe units yearly. An aging Japanese, German, and Italian population amplifies demand because patients over 65 now hold 60% of injectable prescriptions.

Stringent Disposal & Plastic-Waste Regulations

The EU's Single-Use Plastics Directive spurred member states to launch extended producer responsibility schemes; France now makes syringe suppliers fund half of municipal sharps collection programs. Germany's Packaging Act requires 30% recycled content in polypropylene medical devices by 2028. California passed a Medical Device Stewardship Act in 2025 that obliges manufacturers to run take-back programs. Compliance costs compress margins on high-volume conventional syringes.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates Promoting Single-Use Safety-Engineered Devices

- Growing Demand for Prefilled & Self-Administered Syringes

- High-Cost Sensitivity for Safety Syringes in Low-Income Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Safety disposable syringes held 53.53% revenue share in 2025. Auto-disable syringes, insulated from reuse risk and compliant with WHO standards, will post a 9.45% CAGR to 2031, surpassing all other formats. Conventional units persist in cost-sensitive laboratories. Retractable safety designs appeal to emergency departments seeking fast disposal and lower liability. Prefilled devices now capture over 30% of revenue despite lower volumes. Smart connected models remain at pilot scale because cybersecurity validation stretches product timelines.

Producers invest in 64-cavity molds and automated assembly to cut per-unit costs. Becton, Dickinson and Company's BD Integra has secured 12% of U.S. hospital contracts through group-purchasing deals, illustrating how feature differentiation wins share. Venture funding of USD 120 million in 2024-2025 signals investor confidence in connected devices that may leverage cloud analytics for adherence.

Therapeutic injections controlled 62.55% of 2025 revenue, propelled by diabetes and oncology regimens relying on subcutaneous delivery. Immunization injections will grow 9.22% annually to 2031 as catch-up drives close pandemic gaps. Blood-collection devices account for small value but high frequency.

Subcutaneous reformulation of blockbuster monoclonal antibodies adds an estimated 500 million syringes annually. Point-of-care microsampling may chip away at venous draws, yet adoption remains limited to high-resource clinics.

The Disposable Syringes Market Report is Segmented by Product Type (Conventional, Safety [Non-Retractable Safety Syringes and More], and More, Application (Immunization, Therapeutic, Blood Collection), End User (Hospitals, Blood Centers, Ascs, Home Healthcare), Material (Plastic, Glass, Biodegradable), Technology (Passive, and More), and Geography (North America, and More)). Market Forecasts are Provided in Value (USD).

Geography Analysis

North America contributed 37.12% of global revenue in 2025. Vendor-managed inventory contracts allow the U.S. Strategic National Stockpile to hold 150 million syringes on a rolling basis, creating a stable baseline of orders. CMS reimbursement favors safety-engineered devices and accelerates home-care uptake. Canada expanded its National Emergency Strategic Stockpile to 80 million units in 2024. Mexico's IMSS procured 120 million syringes in 2025, incorporating local assembly clauses to spur domestic industry.

Asia-Pacific is forecast at an 8.03% CAGR from 2026-2031. Hindustan Syringes & Medical Devices will double auto-disable capacity after a USD 50 million investment, aiming at UNICEF and WHO tenders. Nipro's Welsh expansion added 1.2 billion units to European supply chains. China's NMPA harmonized standards with WHO criteria in 2024, opening global markets for local producers. Japan's aging population encourages prefilled devices for home-based insulin delivery and GLP-1 therapy.

Europe enforces MDR Class IIa conformity, raising barriers for new entrants. Germany, France, the U.K., Italy, and Spain make up two-thirds of European demand. The NHS aims for 25% bio-based devices by 2030. France's decree obliges suppliers to fund half of sharps collection, increasing per-unit costs. The Middle East and Africa build capacity: GCC states ordered 80 million syringes in 2025, while South Africa inked a 150 million-unit contract with BD. In South America, Brazil's SUS bought 200 million units and Argentina expanded coverage under its 2024 immunization plan.

- B. Braun

- Baxter

- Beckton Dickinson

- Cardinal Health

- Fresenius

- Gerresheimer

- Henke Sass Wolf

- Hindustan Syringes & Medical Devices Ltd.

- Jiangsu Kanghua (KDL) Medical Devices

- Medtronic

- Nipro

- Novo Nordisk

- Poly Medicure

- Retractable Technologies

- SCHOTT

- Smiths Group

- Stevanato Group

- Terumo

- Weigao Group Medical Polymer Co. Ltd.

- West Pharmaceutical Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Immunization & Booster Programs

- 4.2.2 Increasing Prevalence of Chronic Diseases Requiring Injectable Therapies

- 4.2.3 Regulatory Mandates Promoting Single-Use Safety-Engineered Devices

- 4.2.4 Growing Demand for Prefilled & Self-Administered Syringes

- 4.2.5 Government Pandemic Stockpiling & Strategic Syringe Reserves

- 4.2.6 Biodegradable & Smart-Connected Syringe Innovations Gaining Traction

- 4.3 Market Restraints

- 4.3.1 Stringent Disposal & Plastic-Waste Regulations

- 4.3.2 High-Cost Sensitivity for Safety Syringes in Low-Income Settings

- 4.3.3 Gradual Substitution by Glass Syringes for Sensitive Biologics

- 4.3.4 Recall Risks from Heparin/Contaminant Events Undermining Confidence

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Conventional Disposable Syringes

- 5.1.2 Safety Disposable Syringes

- 5.1.2.1 Non-Retractable Safety Syringes

- 5.1.2.2 Retractable Safety Syringes

- 5.1.3 Auto-Disable Syringes

- 5.1.4 Prefilled Disposable Syringes

- 5.1.5 Smart / Connected Disposable Syringes

- 5.2 By Application

- 5.2.1 Immunization Injections

- 5.2.2 Therapeutic Injections

- 5.2.3 Blood Collection & Diagnostics

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Blood Collection Centres & Diagnostic Labs

- 5.3.3 Ambulatory Surgical Centres

- 5.3.4 Home Healthcare

- 5.4 By Material

- 5.4.1 Plastic (Polypropylene, Polycarbonate, COP/COC)

- 5.4.2 Glass

- 5.4.3 Biodegradable / Bio-polymer Blends

- 5.5 By Technology / Safety Mechanism

- 5.5.1 Passive Needle-Guard Safety

- 5.5.2 Manual Retractable Safety

- 5.5.3 Automatic Retractable Safety

- 5.5.4 Auto-Disable Mechanism

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 B. Braun Melsungen AG

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton, Dickinson and Company (BD)

- 6.3.4 Cardinal Health, Inc.

- 6.3.5 Fresenius Kabi AG

- 6.3.6 Gerresheimer AG

- 6.3.7 Henke-Sass, Wolf GmbH

- 6.3.8 Hindustan Syringes & Medical Devices Ltd.

- 6.3.9 Jiangsu Kanghua (KDL) Medical Devices

- 6.3.10 Medtronic plc

- 6.3.11 Nipro Corporation

- 6.3.12 Novo Nordisk A/S

- 6.3.13 Poly Medicure Ltd

- 6.3.14 Retractable Technologies, Inc.

- 6.3.15 Schott AG

- 6.3.16 Smiths Medical (ICU Medical)

- 6.3.17 Stevanato Group

- 6.3.18 Terumo Corporation

- 6.3.19 Weigao Group Medical Polymer Co. Ltd.

- 6.3.20 West Pharmaceutical Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment