|

시장보고서

상품코드

2044184

유럽의 매니지드 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

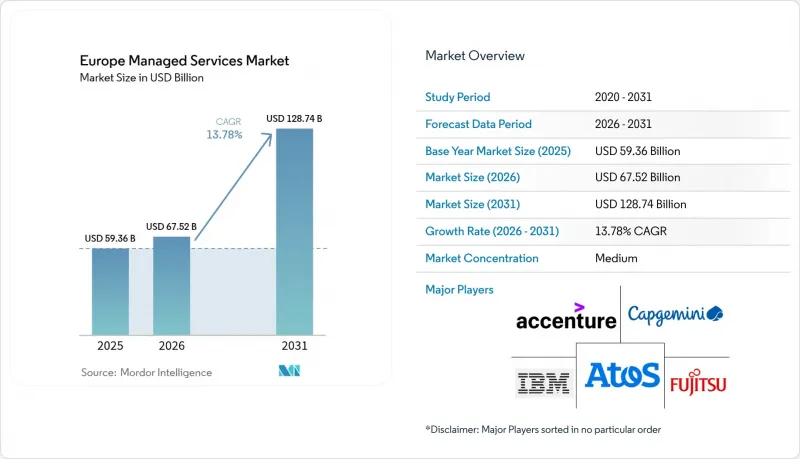

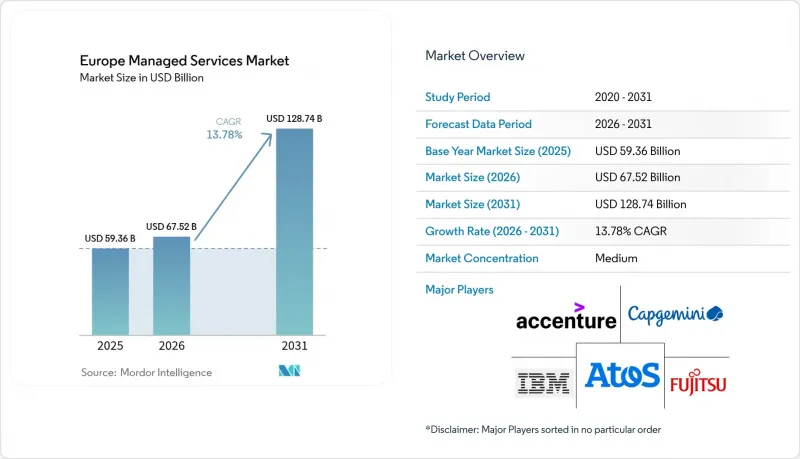

유럽의 매니지드 서비스 시장 규모는 2025년에 593억 6,000만 달러, 2026년에 675억 2,000만 달러되어, 2031년까지 1,287억 4,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 13.78%로 성장할 전망입니다.

조직이 자본 집약적인 데이터센터 자산에서 인프라, 보안, 용도 관리를 통합한 예측 가능한 운영 비용 계약으로 전환함에 따라 수요가 가속화되고 있습니다. 하이브리드 및 멀티 클라우드 전략은 기업이 지연 시간, 컴플라이언스, 비용의 균형을 유지하면서 엄격한 EU의 데이터 주권법에 대응할 수 있도록 도와주기 때문에 주류가 되고 있습니다. 사이버 위협의 급증, NIS2 지침, DORA(Digital Operational Resilience Act)로 인해 관리형 보안은 가장 빠르게 성장하는 서비스 분야가 되고 있으며, EU의 중소기업(SME) 디지털화 지원 보조금으로 인해 고객 기반이 확대되고 있습니다. 동시에, 주권 관할권 내에 위치한 엣지 클라우드 데이터센터는 공급자가 제조, 금융 거래, 원격 의료를 위한 저지연 워크로드를 지원할 수 있도록 돕고 있습니다. 경쟁의 강도는 여전히 중간 정도에 머물러 있으며, 세계 시스템 통합사업자, 통신사, 인도 IT 서비스 업체들이 하이퍼스케일러와의 플랫폼에 구애받지 않는 제휴를 통해 다년간의 계약을 따내기 위해 경쟁하고 있습니다.

유럽 매니지드 서비스 시장 동향 및 인사이트

하이브리드 및 멀티 클라우드 아키텍처 도입 가속화

유럽 기업들은 성능과 컴플라이언스 요건을 모두 충족하기 위해 On-Premise 자산, 프라이빗 클라우드, 그리고 여러 퍼블릭 클라우드 플랫폼에 워크로드를 분산시키는 추세가 증가하고 있습니다. PwC의 조사에 따르면, 2025년 68%의 기업이 최소 3개의 클라우드를 운영하고 있지만, 22%만이 아이덴티티 페더레이션, 네트워크 자동화, 재해복구 워크플로우를 통합할 수 있는 충분한 내부 기술을 보유하고 있는 것으로 나타났습니다. 매니지드 서비스 제공업체들은 쿠버네티스 컨트롤 플레인, 통합 가시성, 데이터 이식성을 유지하는 클라우드 브로커 레이어를 제공함으로써 진입하고 있으며, 이러한 움직임은 EU 데이터 법의 잠금 방지 조항에 의해 촉진되고 있습니다. 금융기관은 이러한 추세를 반영하여 트랜잭션 데이터를 On-Premise에 보관하면서 분석 처리를 Deutsche Telekom이 운영하는 주권 구역에 맡기고 있습니다. 이는 10밀리초 미만의 연결성과 SD-WAN 오버레이가 왜 이제 필수 기능이 되었는지를 여실히 보여줍니다. 통신사업자들은 지연시간에 대한 엄격한 허용 오차 범위로 인해 전용 상호접속을 번들형 관리형 서비스의 일부로 수익화하고 있으며, 네트워크와 보안 SLA를 단일 계약으로 통합하고 있습니다.

비용 최적화 및 예측 가능한 OPEX에 대한 수요 증가

클라우드에 대한 과도한 지출로 인해 당초 클라우드 전환을 정당화했던 비용 절감 효과가 훼손되고 있습니다. 딜로이트 보고서에 따르면, 유럽 CFO의 54%가 2024년 클라우드 예산을 20% 이상 초과한 것으로 나타났습니다. 매니지드 서비스에 내장된 FinOps 모듈은 지속적으로 컴퓨팅 리소스를 최적화하고, 비용 가시성을 위한 태깅을 통해 비용 가시성을 확보하며, 오프피크 시에는 비번타임 워크로드를 휴지시킴으로써 리팩토링 없이도 15-30%의 비용 절감을 실현합니다. 이러한 번들형 서비스는 조달팀이 없는 중소기업에게 매력적이며, 본질적으로 예측할 수 없는 자본 지출을 안정적인 월정액 요금으로 전환할 수 있습니다. 공적 자금은 이 효과를 더욱 증폭시킵니다. 유럽투자은행은 2025년 중소기업의 클라우드 도입을 지원하기 위해 12억 유로(12억 8,000만 달러)를 출자했습니다. 보조금을 받기 위해서는 인증된 MSP와 계약을 맺어야 합니다. 북유럽에 비해 중소기업의 디지털화가 늦은 스페인, 이탈리아, 폴란드에서는 보조금으로 진입장벽이 크게 낮아져 가장 가파른 도입 곡선을 보이고 있습니다.

복잡한 EU의 데이터 주권 및 개인정보 보호 규제

GDPR(EU 개인정보보호규정), EU 데이터법, 의료기기 규정과 같은 산업별 프레임워크가 공존하는 상황에서 MSP는 별도의 인프라 스택을 유지해야 하고, 이로 인해 컴플라이언스 부담이 가중되고 있습니다. 독일 BSI는 공공 부문의 워크로드가 EU에 본사를 둔 사업자가 관리하는 주권 클라우드 외부로 유출되는 것을 금지하고 있습니다. 프랑스의 SecNumCloud 인증은 더욱 엄격한 규제를 적용하고 있으며, 취득까지 18개월이 소요될 수 있습니다. 각 회원국이 약간씩 다른 감사 기준을 적용하고 있기 때문에 이러한 단편화로 인해 법적 비용이 증가하고 조달 주기가 길어지고 있습니다. 인증 조정을 위한 자발적인 CISPE 이니셔티브는 아직 시범 운영 단계에 있으며, 규제 혼란으로 인해 매니지드 서비스 출시가 여전히 지연되고 있습니다.

부문 분석

2025년 기준 하이브리드 및 호스팅 환경은 유럽 매니지드 서비스 시장 점유율의 46.32%를 차지하고 있으며, 클라우드 전용 환경은 2031년까지 연평균 복합 성장률(CAGR) 14.18%의 견조한 성장세를 보일 것으로 전망됩니다. 기업들은 GDPR(EU 개인정보보호규정) 준수를 위해 기밀성이 높은 데이터 세트를 On-Premise에 보관하는 한편, 클라우드의 폭발적인 용량을 분석에 활용하고 있습니다. 통신 교환국 내 에지 클라우드 존은 5밀리초 미만의 지연시간과 주권 인증을 제공하며, 제공업체는 성능과 컴플라이언스의 균형을 맞출 수 있습니다. 멀티테넌트 리스크가 없고 예측 가능한 요금 체계를 선호하는 중견기업들 사이에서 호스트형 도입이 지속적으로 확대되고 있습니다. 특히 프랑크푸르트와 암스테르담의 경우, 2025년에 코로케이션 용량이 확대되었습니다. 유럽 매니지드 서비스 시장 규모에서 On-Premise에 대한 지출 비중은 감소하는 추세지만, 독일 제조업과 이탈리아 은행들이 완전한 클라우드 전환이 아닌 매니지드 인프라 계약을 통해 하드웨어를 갱신하고 있기 때문에 절대적인 금액은 보합세를 유지하고 있습니다. 유지하고 있습니다.

Gaia-X 연합은 클라우드 규모와 데이터 거주성 보장을 결합한 상호 운용 가능한 서비스를 인증함으로써 시장 구조를 변화시키고 있습니다. MSP는 현재 Gaia-X 호환 오케스트레이션 계층을 통합하고, 주권 영역과 하이퍼스케일러의 영역 간 워크로드를 이동시킴으로써 하이브리드 환경을 장기적인 표준으로 정착시키고 있습니다. 중소기업은 설비투자 예산이 부족해 클라우드로의 전환을 가속화하고 있지만, 백업이나 기밀성이 높은 인사 데이터는 로컬에서 운영하는 등 가벼운 하이브리드 형태를 채택하는 경우가 많습니다. 그 결과, 유럽 매니지드 서비스 시장에서는 이러한 하이브리드 환경 전반에 걸쳐 워크로드 배치를 최적화할 수 있는 공급자가 지속적으로 선호되고 있습니다.

매니지드 시큐리티는 2025년 매출 점유율 29.54%를 차지하며 CAGR 15.58%로 가장 빠르게 성장하는 분야가 될 것으로 예측됩니다. 규제 기한, 랜섬웨어 위험, 이사회 차원의 감시로 인해 기업들은 24시간 365일 모니터링, 사고 대응, 포렌식 분석을 보다 광범위한 인프라 계약에 포함시켜야 하는 상황에 직면해 있습니다. 매니지드 데이터센터 서비스는 런던, 프랑크푸르트, 파리의 거래소에 저 지연 및 근접한 환경을 필요로 하는 거래 허브에 선호되고 있습니다. 한편, SD-WAN 및 캐리어 중립적 상호 연결과 같은 매니지드 네트워크 서비스는 On-Premise, 엣지, 멀티 클라우드 영역을 통합하고 있습니다. 통신 및 협업 서비스는 원격근무 붐 이후 성장이 정점을 찍고 있으며, 벤더들은 실시간 번역과 컨택센터용 AI에 초점을 맞추었습니다.

관리형 인프라 및 호스팅은 여전히 기본 서비스이지만, 하이퍼스케일러가 코드 템플릿을 통해 서버 프로비저닝을 자동화함에 따라 상품화의 압력에 직면하고 있습니다. 그 결과, 공급자들은 재해복구 훈련과 예측적 용량 계획을 통합하여 차별화를 꾀하고 있습니다. 매니지드 모빌리티는 원격 디바이스 프로비저닝과 컴플라이언스 준수가 미션 크리티컬한 의료 및 현장 서비스 분야에서 성장하고 있습니다. 관리형 보안과 네트워크 운영의 통합으로 MSP는 단일 콘솔에서 위협 인텔리전스와 트래픽 이상 징후를 대조할 수 있게 되었습니다. 이는 DORA에 따라 규제 당국이 필수적인 기능으로 간주하기 시작한 기능입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Europe managed services market size is projected to be USD 59.36 billion in 2025, USD 67.52 billion in 2026, and reach USD 128.74 billion by 2031, growing at a CAGR of 13.78% from 2026 to 2031.

Demand is accelerating as organizations migrate from capital-intensive data-center assets to predictable operating-expense agreements that bundle infrastructure, security, and application management. Hybrid and multi-cloud strategies dominate because they let firms balance latency, compliance, and cost while still meeting strict EU data-sovereignty laws. Escalating cyber-threat volumes, the NIS2 Directive, and the Digital Operational Resilience Act are turning managed security into the fastest-growing service line, while EU grants for SME digitalization are widening the customer base. At the same time, edge-cloud data-centers positioned inside sovereign jurisdictions are helping providers support low-latency workloads for manufacturing, financial trading, and telemedicine. Competitive intensity remains moderate; global systems integrators, telecom carriers, and Indian IT services companies are racing to lock in multi-year contracts, often through platform-agnostic alliances with hyperscalers.

Europe Managed Services Market Trends and Insights

Accelerated Adoption of Hybrid and Multi-Cloud Architectures

European enterprises are increasingly distributing workloads across on-premises assets, private clouds, and several public-cloud platforms to align performance with compliance mandates. A PwC survey showed that 68% managed at least three clouds in 2025, but only 22% had enough in-house skills to integrate identity federation, network automation, and disaster-recovery workflows. Managed service providers are stepping in with Kubernetes control planes, unified observability, and cloud brokerage layers that keep data portable, an outcome reinforced by the EU Data Act's anti-lock-in clauses. Financial institutions exemplify the trend by keeping transaction data on-premises while pushing analytics to sovereign zones run by Deutsche Telekom, illustrating why sub-10 ms connectivity and SD-WAN overlays are now must-have features. Because latency budgets are tight, telecom carriers monetize dedicated interconnects as part of bundled managed services, blending network and security SLAs in a single contract.

Rising Demand for Cost Optimization and Predictable OPEX

Cloud overspending is eroding the savings that initially justified migration; Deloitte reported that 54% of European CFOs blew past their 2024 cloud budgets by more than 20%. FinOps modules embedded within managed services continuously right-size compute, enforce tagging for cost show-back, and park non-production workloads during off-peak hours, delivering 15-30% savings without refactoring. Bundled offerings appeal to SMEs that lack procurement teams, essentially converting unpredictable capital outlays into steady monthly fees. Public money amplifies the effect. The European Investment Bank issued EUR 1.2 billion (USD 1.28 billion) in 2025 to subsidize SME cloud uptake, with certified MSP engagement mandated for grant eligibility. Spain, Italy, and Poland, where SME digitization lags Northern Europe, are showing the steepest adoption curves because subsidies sharply lower entry barriers.

Complex EU Data-Sovereignty and Privacy Regulations

The coexistence of GDPR, the EU Data Act, and sector-specific frameworks such as the Medical Device Regulation forces MSPs to maintain separate infrastructure stacks, raising compliance overhead. Germany's BSI bars public-sector workloads from traveling outside sovereign clouds controlled by EU-headquartered operators. France's SecNumCloud certificate adds even stricter controls and can take 18 months to earn. Fragmentation inflates legal costs and stretches procurement cycles because each member state enforces slightly different audit standards. A voluntary CISPE initiative to harmonize certifications is still in pilot, so managed-services rollouts remain slowed by regulatory sprawl.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Cybersecurity Threats Driving Managed Security Uptake

- Shortage of In-House IT Talent Across Europe

- Integration Complexity with Legacy Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid and hosted environments captured 46.32% of Europe managed services market share in 2025, while cloud-only setups are recording a brisk 14.18% CAGR to 2031. Enterprises keep sensitive datasets on-premises to meet GDPR while exploiting cloud burst capacity for analytics. Edge-cloud zones inside telecom exchanges offer sub-5 ms latency and sovereign certifications, letting providers strike a balance between performance and compliance. Hosted deployments keep growing among mid-sized firms that prefer predictable fees without multitenancy risk, particularly in Frankfurt and Amsterdam where colocation capacity expanded in 2025. Although on-premises spending is declining as a share of the Europe managed services market size, absolute dollars remain steady because German manufacturers and Italian banks refresh hardware through managed-infrastructure contracts instead of full cloud migrations.

The Gaia-X federation is reshaping the landscape by certifying interoperable services that combine cloud scale with data-residency guarantees. MSPs now embed Gaia-X-compliant orchestration layers to move workloads among sovereign zones and hyperscaler regions, reinforcing hybrid as the long-term norm. SMEs accelerate straight to cloud because they lack capex budgets, but even they often adopt a light hybrid stance by running backups or sensitive HR data locally. Consequently, the Europe managed services market continues to favor providers that can optimize workload placement across this hybrid continuum.

Managed security held 29.54% revenue share in 2025 and is projected to remain the fastest-growing line at 15.58% CAGR. Regulatory deadlines, ransomware risk, and board-level scrutiny push enterprises to embed 24X7 monitoring, incident response, and forensic analysis within wider infrastructure contracts. Managed data-center services appeal to trading hubs that need low-latency proximity to exchanges in London, Frankfurt, and Paris, while managed network services such as SD-WAN and carrier-neutral interconnects weave together on-premises, edge, and multi-cloud domains. Communications and collaboration services have plateaued after the remote-work boom, causing vendors to shift focus toward real-time translation and contact-center AI.

Managed infrastructure and hosting remain baseline offerings but face commoditization as hyperscalers automate server provisioning through code templates. Consequently, providers differentiate by layering disaster-recovery drills and predictive capacity planning. Managed mobility is growing in healthcare and field services, where remote device provisioning and compliance enforcement are mission-critical. The convergence of managed security and network operations lets MSPs map threat intelligence to traffic anomalies in a single console, a feature regulators are starting to deem essential under DORA.

The Europe Managed Services Market Report is Segmented by Deployment Model (On-Premises, Cloud, and Hybrid/Hosted), Service Type (Managed Data Centre, Managed Security, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Vertical (BFSI, Manufacturing, and More), and Country (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- IBM Corporation

- Fujitsu Limited

- Capgemini SE

- Atos SE

- Accenture plc

- AT&T Inc.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Microsoft Corporation

- Deutsche Telekom AG

- Orange S.A. (Orange Business Services)

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- NTT Data Corporation

- Tech Mahindra Limited

- DXC Technology Company

- Rackspace Technology, Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- Sopra Steria Group SA

- CGI Inc.

- Kyndryl Holdings, Inc.

- Capita plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of Hybrid and Multi-Cloud Architectures

- 4.2.2 Rising Demand for Cost Optimization and Predictable OPEX

- 4.2.3 Increasing Cybersecurity Threats Driving Managed Security Uptake

- 4.2.4 Shortage of In-House IT Talent Across Europe

- 4.2.5 Emergence of Edge-Cloud Zonal Datacentres for Data-Sovereign Workloads

- 4.2.6 MSP Bundling of AI Ops and FinOps Platforms to Automate Cost Governance

- 4.3 Market Restraints

- 4.3.1 Complex EU Data-Sovereignty and Privacy Regulations

- 4.3.2 Integration Complexity with Legacy Systems

- 4.3.3 Rising Energy Costs Squeezing Data-Centre Service Margins

- 4.3.4 Escalating Carbon-Accounting Scrutiny on Outsourced Workloads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid/Hosted

- 5.2 By Service Type

- 5.2.1 Managed Data Centre

- 5.2.2 Managed Security

- 5.2.3 Managed Network

- 5.2.4 Managed Communication and Collaboration

- 5.2.5 Managed Infrastructure and Hosting

- 5.2.6 Managed Mobility

- 5.2.7 Managed Cloud and Application

- 5.2.8 Managed Workplace / Service Desk

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Government and Public Sector

- 5.4.6 IT and Telecom

- 5.4.7 Energy and Utilities

- 5.4.8 Rest of End-User Verticals

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Sweden

- 5.5.8 Russia

- 5.5.9 Poland

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Fujitsu Limited

- 6.4.3 Capgemini SE

- 6.4.4 Atos SE

- 6.4.5 Accenture plc

- 6.4.6 AT&T Inc.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Microsoft Corporation

- 6.4.10 Deutsche Telekom AG

- 6.4.11 Orange S.A. (Orange Business Services)

- 6.4.12 Tata Consultancy Services Limited

- 6.4.13 Wipro Limited

- 6.4.14 Cognizant Technology Solutions Corporation

- 6.4.15 Nokia Corporation

- 6.4.16 Telefonaktiebolaget LM Ericsson

- 6.4.17 NTT Data Corporation

- 6.4.18 Tech Mahindra Limited

- 6.4.19 DXC Technology Company

- 6.4.20 Rackspace Technology, Inc.

- 6.4.21 Verizon Communications Inc.

- 6.4.22 Vodafone Group Plc

- 6.4.23 Sopra Steria Group SA

- 6.4.24 CGI Inc.

- 6.4.25 Kyndryl Holdings, Inc.

- 6.4.26 Capita plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment