|

시장보고서

상품코드

2044187

목초액 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Wood Vinegar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

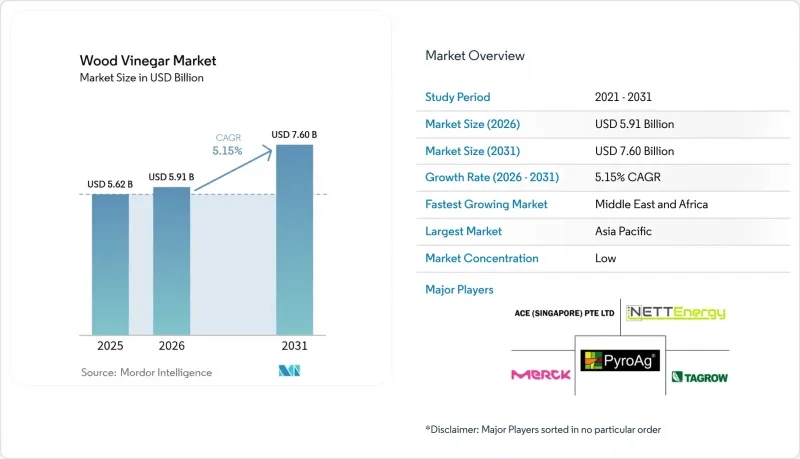

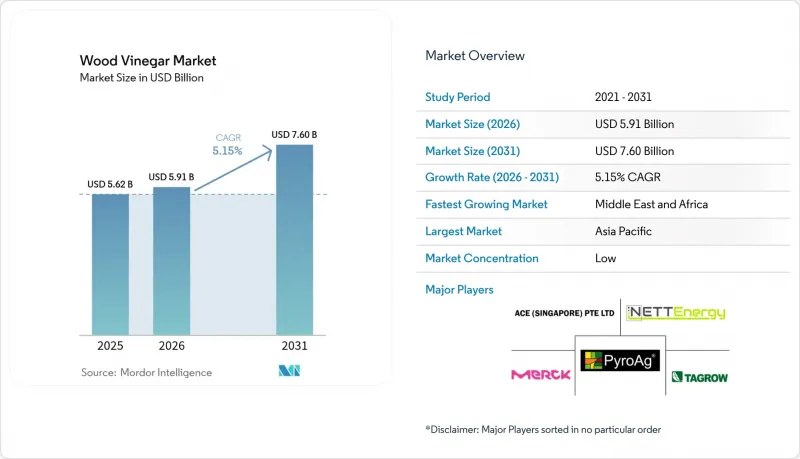

목초액 시장 규모는 2025년에 56억 2,000만 달러로 평가되었고 2026년 59억 1,000만 달러에서 2031년까지 76억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.15%를 나타낼 전망입니다.

농업, 식품가공, 특수화학 분야에서 바이오 원료에 대한 수요 증가가 주요 촉진요인으로 작용하고 있으며, 합성화학물질 사용을 억제하는 환경 규제 강화로 인해 더욱 강화되고 있습니다. 순환 경제 비즈니스 모델에 대한 강력한 정책적 지원, 열분해 시스템의 급속한 기술 혁신, 그리고 양식업과 화장품 분야에서의 이용 사례 확대는 상업적 전망을 더욱 넓혀주고 있습니다. 아시아태평양은 중국, 일본, 동남아시아의 확립된 생산 클러스터를 통해 세계 매출을 지속적으로 뒷받침하고 있으며, 중동 및 아프리카은 지속 가능한 농업에 대한 노력과 대상별 지원 프로그램을 통해 가장 빠른 시장 확대가 예상됩니다. 주요 경쟁 동향으로는 지속적인 시장 세분화, 수직적 통합의 여지가 충분하다는 점, 고온 열분해 반응기 및 단계적 증류 시스템의 특허 활동 활성화 등을 꼽을 수 있습니다.

세계 목초액 시장 동향 및 인사이트

천연 식품 방부제 및 향미증진제에 대한 수요 증가

식품 및 음료 산업에서 천연 방부제로의 전환은 목초액에 대한 수요 추세를 재구성하고 있으며, FDA의 GRAS(일반적으로 안전하다고 인정되는) 프레임워크는 식품 용도에 대한 규제적 명확성을 제공합니다. 주로 아세트산 함량과 페놀 화합물에 기인하는 목초액의 항균 특성은 통조림, 소스, 유제품에서 식품 제조업체에 합성 방부제의 천연 대체품을 제공합니다. 최근 연구에 따르면 리치(Litchi chinensis)에서 추출한 목초액은 비타민 C에 필적하는 광범위한 항균 활성을 나타내며, 식품 안전 기준을 유지하면서 보존 기간을 연장하는 우수한 항산화 작용을 가지고 있다고 합니다. 이 화합물의 천연 유래라는 특성은 클린 라벨 제품을 원하는 소비자의 선호와 일치하여 기존 방부제 대체품보다 높은 채택률을 보이고 있습니다. 이러한 추세는 천연 성분이 가격 프리미엄을 가져오는 프리미엄 식품 부문에서 특히 두드러지며, 목초액 생산자에게 지속 가능한 수익원을 창출하고 있습니다. 중국에서 화장품 용도로 대나무 식초의 규제 승인은 소비재에서 목초액 유도체가 널리 받아들여지고 있으며, 이는 기존의 식품 용도를 넘어 시장 기회를 확대할 수 있음을 시사합니다.

정부 지원 정책과 환경 규제

규제 프레임워크는 합성 화학 물질보다 바이오 대안을 점점 더 선호하고 있으며, 여러 관할권에서 목초액에 대한 구조적 수요를 견인하는 요인이 되고 있습니다. 스페인 카스티야 라 만차 지방에서 천연 바이오 제초제로서 목초액을 홍보하는 유럽연합(EU)의 노력은 지속 가능한 농업 관행에 대한 정부의 지원을 보여주며, 다양한 시험에서 3,000리터 이상의 목초액이 사용되어 인체 건강에 대한 안전성을 유지하면서 잡초에 대한 효능을 확인했습니다. 확인되었습니다. 합성농약 감축을 위한 환경 규제는 특히 식품 내 화학물질 잔류 기준이 엄격한 지역에서 목초액 채택을 가속화하고 있습니다. 순환 경제 실천에 대한 정부의 인센티브는 농업 폐기물을 이용한 목초액 생산을 더욱 촉진하여 폐기물 관리와 지속 가능한 농업이라는 두 가지 목표를 모두 충족시키고 있습니다. 이러한 정책적 틀은 장기적인 시장 안정을 가져오고, 생산능력 확대에 대한 투자를 촉진할 수 있습니다.

합성 대체품과의 경쟁

기존의 합성화학 산업은 성숙한 공급망, 표준화된 제품, 검증된 효능 프로파일을 통해 강력한 경쟁자가 되어 목초액 시장 침투를 막고 있습니다. 합성 농약과 방부제는 수십 년에 걸친 연구개발 투자로 인해 예측 가능한 성능 특성을 가진 고도로 최적화된 제형이 개발되었습니다. 많은 최종 사용자들은 천연 유래 대체품보다 이러한 제품을 선호하는 경향이 있습니다. 합성화학산업의 규모의 경제로 인해 경쟁력 있는 가격 책정이 가능해졌고, 목초액 생산자들은 이를 따라잡기 위해 고군분투하고 있습니다. 특히 비용 측면의 고려가 지속가능성의 이점보다 우선시되는 범용 농업용도에서 이러한 경향은 더욱 두드러집니다. 합성화학물질에 대한 규제 승인 절차는 이미 확립되어 있고 업계 관계자들도 잘 알고 있지만, 목초액의 경우 새로운 규제 경로가 필요한 경우가 많아 불확실성을 야기하고 시장 진입을 지연시키고 있습니다. 합성 대체품의 일관된 성능은 입증되지 않은 천연 대체품으로 인한 작황 부진과 제품 품질 문제를 용인할 수 없는 상업적 사용자들에게 위험을 줄일 수 있습니다.

부문 분석

2025년, 느린 열분해법은 이미 구축된 인프라와 우수한 목초액 수율을 활용하여 목초액 시장에서 58.12%의 압도적인 점유율을 차지하고 있습니다. 이 방법은 에너지 소비를 최소화하면서 액체 제품의 회수를 극대화할 수 있기 때문에 전통적으로 시장을 독점해 왔습니다. 저속 열분해는 안정적인 생산량과 비용 효율성을 보장하기 때문에 특히 대규모 상업 생산에서 선호됩니다. 기존 시스템과의 호환성도 보급을 더욱 촉진하고 있으며, 대대적인 설비 교체 없이 증가하는 수요에 대응하고자 하는 생산자에게 신뢰할 수 있는 선택이 되고 있습니다.

한편, 급속 열분해는 목초액 시장에서 빠르게 성장하고 있으며, 2026년부터 2031년까지 예측 기간 동안 CAGR 7.14%를 나타낼 것으로 예측됩니다. 이러한 성장은 생산 효율을 높이고 제품 품질을 향상시키는 기술적 진보에 의해 주도되고 있습니다. 반응기 설계의 혁신과 공정 최적화는 높은 품질 기준을 유지하면서 처리 시간을 크게 단축하기 위해 고속 열분해의 채택을 촉진하는 중요한 요인이 되고 있습니다. 이러한 발전은 사업 규모를 확장하고 변화하는 시장 수요에 효율적으로 대응하고자 하는 생산자들에게 고속 열분해가 점점 더 매력적인 선택이 되고 있습니다.

지역별 분석

2025년 아시아태평양은 39.87%의 압도적인 시장 점유율을 차지했습니다. 이는 다년간의 농업 분야에서의 이용 실적과 더불어 기존 목탄 제조에서 통합형 바이오리파이너리 사업으로 전환한 생산 인프라가 뒷받침하고 있습니다. 이러한 성장은 유기농업과 바이오 농약에 대한 정부의 강력한 지원으로 더욱 촉진되고 있습니다. 일본은 최첨단 열분해 기술과 엄격한 품질 관리 시스템을 통해 목초액 생산에 있어 세계 표준을 확립하고 있습니다. 한편, 동남아시아 국가들은 풍부한 코코넛 껍질과 대나무 자원을 활용하여 효율적이고 비용 효율적인 생산 시스템을 구축하고 있습니다. 또한, 이 지역의 양식업은 중요한 성장 동력으로 부상하고 있으며, 특히 새우 양식에서 수질 개선과 어류 건강 증진에 목초액의 역할을 강조하는 연구 결과가 보고되고 있습니다.

중동 및 아프리카은 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.72%의 놀라운 성장률을 기록하며 시장을 주도하고 있습니다. 이러한 급격한 성장은 가뭄에 대한 내성을 높이고 토양 황폐화에 대응하는 등 농업 문제 해결에 목초액의 효과에 대한 지역 내 인식이 높아진 것이 주요 원인으로 분석됩니다. 또한, 이 지역에 풍부한 대추야자 잔여물은 목초액의 지속 가능한 원료로 활용되고 있습니다. 이 연구는 농업 폐기물을 가치 있는 바이오 제품으로 전환하고, 토양의 성질을 개선하며, 순환 경제의 원칙을 촉진하는 노력의 성공을 강조하고 있습니다. 지속 가능한 농업과 유기 농업을 장려하는 정부 정책에 힘입어 이 지역에는 목초액 도입에 적합한 환경이 조성되어 있습니다. 또한, 국제 개발 프로그램은 생산 능력을 강화하기 위해 기술 지원과 자금 지원을 모두 제공하는 국제 개발 프로그램이 이러한 모멘텀을 촉진하고 있습니다.

성숙한 시장을 가진 북미와 유럽에서는 엄격한 규제 상황에 직면해 있습니다. 이들 지역에서는 특히 식품, 의약품, 고부가가치 농업에서 목초액의 프리미엄 용도를 우선적으로 고려하고 있습니다. 미국에서는 FDA의 GRAS(Generally Recognized as Safe) 프레임워크가 목초액을 식품에 사용할 수 있는 명확한 경로를 제시하고 있습니다. 대서양을 사이에 둔 유럽에서는 규제가 바이오 유래 대체품에 점점 더 기울어지고 합성화학물질은 제쳐두고 있습니다. 한편, 남미의 농업 환경은 성장 잠재력으로 가득 차 있습니다. 이 지역 국가들은 유기 농업을 장려하고 있을 뿐만 아니라, 특히 규제 감시가 강화되는 가운데 합성 농약의 지속가능한 대안을 모색하고 있습니다. 풍부한 바이오매스 자원과 확립된 농업 체제를 배경으로 남미는 강력한 시장 확대의 기세가 높아지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSThe wood vinegar market size was valued at USD 5.62 billion in 2025 and estimated to grow from USD 5.91 billion in 2026 to reach USD 7.6 billion by 2031, at a CAGR of 5.15% during the forecast period (2026-2031).

Rising demand for bio-based inputs in agriculture, food processing, and specialty chemicals is the primary catalyst, reinforced by tightening environmental regulations that discourage synthetic chemical use. Strong policy support for circular-economy business models, rapid technology upgrades in pyrolysis systems, and expanding end-use cases in aquaculture and cosmetics further broaden commercial prospects. Asia-Pacific continues to anchor global revenues through well-established production clusters in China, Japan, and Southeast Asia, while Middle East and Africa registers the quickest uptake due to sustainable-farming initiatives and targeted donor programs. Key competitive dynamics include persistent fragmentation, ample room for vertical integration, and escalating patent activity in high-temperature pyrolysis reactors and sequential distillation systems.

Global Wood Vinegar Market Trends and Insights

Increasing demand for natural food preservatives and flavor enhancers

The food and beverage industry's pivot toward natural preservatives is reshaping wood vinegar demand dynamics, with the FDA's GRAS framework providing regulatory clarity for food applications. Wood vinegar's antimicrobial properties, primarily attributed to its acetic acid content and phenolic compounds, offer food manufacturers a natural alternative to synthetic preservatives in canned foods, sauces, and dairy products. Recent research demonstrates that wood vinegar from Litchi chinensis exhibits broad-spectrum antibacterial activity comparable to vitamin C, with significant antioxidant properties that extend shelf life while maintaining food safety standards. The compound's natural origin aligns with consumer preferences for clean-label products, driving adoption rates that exceed traditional preservative alternatives. This trend is particularly pronounced in premium food segments where natural ingredients command price premiums, creating sustainable revenue streams for wood vinegar producers. The regulatory approval of bamboo vinegar for cosmetic applications in China signals broader acceptance of wood vinegar derivatives in consumer products, potentially expanding market opportunities beyond traditional food applications.

Supportive government policies and environmental regulations

Regulatory frameworks increasingly favor bio-based alternatives over synthetic chemicals, creating structural demand drivers for wood vinegar across multiple jurisdictions. The European Union's initiative promoting wood vinegar as a natural bio-herbicide in Castilla-La Mancha, Spain, demonstrates government support for sustainable agricultural practices, with over 3,000 liters applied in various trials showing effectiveness against weeds while maintaining safety for human health . Environmental regulations targeting synthetic pesticide reduction are accelerating wood vinegar adoption, particularly in regions implementing stringent chemical residue limits in food products. Government incentives for circular economy practices further support wood vinegar production from agricultural waste, addressing both waste management and sustainable agriculture objectives. These policy frameworks create long-term market stability and encourage investment in production capacity expansion.

Competition from synthetic alternatives

Established synthetic chemical industries present formidable competition through mature supply chains, standardized products, and proven efficacy profiles that challenge wood vinegar market penetration. Synthetic pesticides and preservatives benefit from decades of research and development investment, resulting in highly optimized formulations with predictable performance characteristics that many end-users prefer over natural alternatives. The synthetic chemical industry's economies of scale enable competitive pricing that wood vinegar producers struggle to match, particularly in commodity agricultural applications where cost considerations often outweigh sustainability benefits. Regulatory approval processes for synthetic chemicals are well-established and understood by industry participants, while wood vinegar applications often require novel regulatory pathways that create uncertainty and delay market entry. The performance consistency of synthetic alternatives provides risk mitigation for commercial users who cannot afford crop failures or product quality issues associated with unproven natural alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Rising demand for bio-based pesticides

- Expanding use in aquaculture

- High production costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, slow pyrolysis holds a commanding 58.12% share of the wood vinegar market, leveraging its established infrastructure and superior yields of wood vinegar. This method has traditionally dominated the market due to its ability to maximize liquid product recovery while minimizing energy consumption. Slow pyrolysis is particularly favored for large-scale commercial operations, as it ensures consistent output and cost efficiency. Its widespread adoption is further supported by its compatibility with existing systems, making it a reliable choice for producers aiming to meet growing demand without significant operational overhauls.

Conversely, fast pyrolysis is experiencing rapid growth in the wood vinegar market, with a projected CAGR of 7.14% during the forecast period of 2026-2031. This growth is driven by technological advancements that enhance production efficiency and improve product quality. Innovations in reactor design and process optimization are key factors propelling the adoption of fast pyrolysis, as they significantly reduce processing time while maintaining high-quality standards. These advancements make fast pyrolysis an increasingly attractive option for producers seeking to scale operations and meet evolving market demands efficiently.

The Wood Vinegar Market Report is Segmented by Production Method (Slow Pyrolysis, Intermediate Pyrolysis, and Fast Pyrolysis), Feed Stock (Bamboo, Hardwood, Softwood, and More), Application (Agriculture, Food and Beverage, Animal Feed, Pharmaceuticals, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region commands a dominant 39.87% market share, bolstered by its long-standing agricultural applications and a production infrastructure that has transitioned from traditional charcoal manufacturing to integrated biorefinery operations. This growth is further fueled by robust government backing for organic farming and bio-based pesticides. Japan sets global standards in wood vinegar production with its cutting-edge pyrolysis technologies and stringent quality control systems. Meanwhile, Southeast Asian nations capitalize on their rich reserves of coconut shells and bamboo, crafting efficient and cost-effective production systems. Additionally, the region's aquaculture sector is emerging as a pivotal growth engine, with studies highlighting wood vinegar's role in enhancing water quality and fish health, particularly in shrimp farming.

The Middle East and Africa lead the pack with the highest growth rate, achieving a notable 7.72% CAGR from 2026 to 2031. This surge is largely attributed to the region's growing acknowledgment of wood vinegar's efficacy in tackling agricultural hurdles, such as bolstering drought resilience and combating soil degradation. Furthermore, the region's plentiful date palm residues serve as a sustainable feedstock for wood vinegar. Research underscores the successful transformation of agricultural waste into valuable bio-products, enhancing soil properties and championing circular economy principles. Bolstered by government policies that advocate for sustainable agriculture and organic farming, the region fosters a conducive environment for wood vinegar adoption. Additionally, international development programs bolster this momentum, offering both technical assistance and funding to enhance production capacities.

North America and Europe, with their mature markets, grapple with stringent regulatory landscapes. These regions prioritize premium applications of wood vinegar, especially in food, pharmaceuticals, and high-value agriculture. In the U.S., the FDA's GRAS framework delineates a clear path for wood vinegar's entry into food applications. Across the Atlantic, European regulations are increasingly leaning towards bio-based alternatives, sidelining synthetic chemicals. Meanwhile, South America's agricultural landscape is ripe with growth potential. Countries in the region are not only championing organic farming but are also on the lookout for sustainable substitutes to synthetic pesticides, especially as these face mounting regulatory scrutiny. With its rich biomass resources and a well-established agricultural framework, South America is poised for a robust market expansion.

- Ace (Singapore) Pte Ltd

- Nettenergy B.V.

- Tagrow Co. Ltd

- Merck KGaA

- PyroAg Pty Ltd (PyroAg)

- Byron Biochar

- Earth Systems (Green Man Char )

- NewCarbon

- Shijiazhuang Hongsen Activated Carbon Co., Ltd.

- VerdiLife Inc.

- Nara Tanka Industries Co., Ltd.

- New Life Agro

- Tex Cycle

- Xi'An Hj Herb Biotechnology Co., Ltd.

- The Green Side of the Fence Ltd

- Haiqi Environmental Protection Technology Co.,ltd.

- Sane Shell Carbon

- Aspire Renoil Associates Co

- Qingdao Re-green Biological Technology Co.,Ltd.

- Penta Fine Ingredients, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for natural food preservatives and flavor enhancers

- 4.2.2 Supportive government policies and environmental regulations

- 4.2.3 Shift toward organic and sustainable agriculture

- 4.2.4 Rising demand for bio-based pesticides

- 4.2.5 Advancements in wood vinegar production technology

- 4.2.6 Expanding use in aquaculture

- 4.3 Market Restraints

- 4.3.1 High production costs

- 4.3.2 Competition from synthetic alternatives

- 4.3.3 Low scientific validation and research

- 4.3.4 Distribution and scale-up challenges

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Production Method

- 5.1.1 Slow Pyrolysis

- 5.1.2 Intermediate Pyrolysis

- 5.1.3 Fast Pyrolysis

- 5.2 By Feedstock

- 5.2.1 Bamboo

- 5.2.2 Hardwood

- 5.2.3 Softwood

- 5.2.4 Agricultural Residues

- 5.2.5 Coconut Shells

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Agriculture

- 5.3.1.1 Crop Nutrition

- 5.3.1.2 Crop Protection

- 5.3.2 Food and Beverage

- 5.3.2.1 Canned Food

- 5.3.2.2 Sauces

- 5.3.2.3 Dairy Products

- 5.3.2.4 Other Food and Beverage Applications

- 5.3.3 Animal Feed

- 5.3.4 Pharmaceuticals

- 5.3.5 Other Applications

- 5.3.1 Agriculture

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Spain

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Columbia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Egypt

- 5.4.5.5 Morocco

- 5.4.5.6 Nigeria

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ace (Singapore) Pte Ltd

- 6.4.2 Nettenergy B.V.

- 6.4.3 Tagrow Co. Ltd

- 6.4.4 Merck KGaA

- 6.4.5 PyroAg Pty Ltd (PyroAg)

- 6.4.6 Byron Biochar

- 6.4.7 Earth Systems (Green Man Char )

- 6.4.8 NewCarbon

- 6.4.9 Shijiazhuang Hongsen Activated Carbon Co., Ltd.

- 6.4.10 VerdiLife Inc.

- 6.4.11 Nara Tanka Industries Co., Ltd.

- 6.4.12 New Life Agro

- 6.4.13 Tex Cycle

- 6.4.14 Xi'An Hj Herb Biotechnology Co., Ltd.

- 6.4.15 The Green Side of the Fence Ltd

- 6.4.16 Haiqi Environmental Protection Technology Co.,ltd.

- 6.4.17 Sane Shell Carbon

- 6.4.18 Aspire Renoil Associates Co

- 6.4.19 Qingdao Re-green Biological Technology Co.,Ltd.

- 6.4.20 Penta Fine Ingredients, Inc.