|

시장보고서

상품코드

2044198

광학식 3차원 측정기 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Optical Coordinate Measuring Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

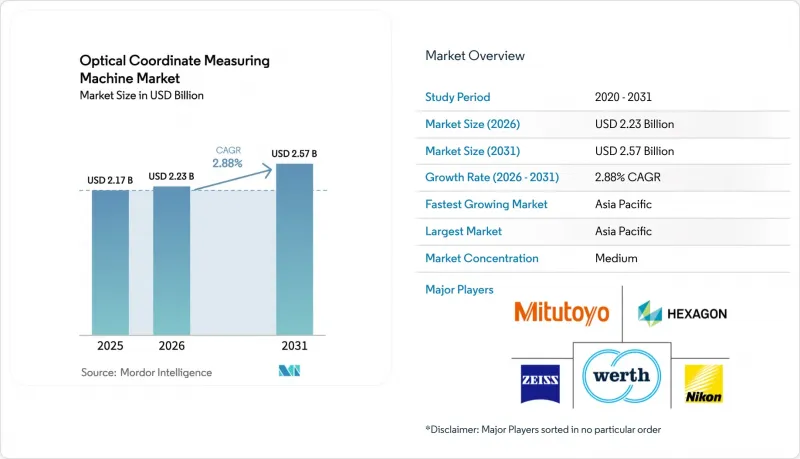

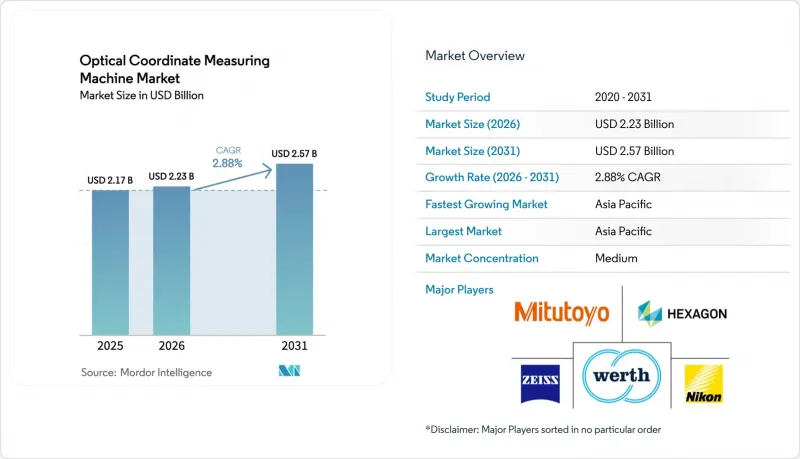

광학식 3차원 측정기 시장 규모는 2025년 21억 7,000만 달러, 2026년 22억 3,000만 달러에서 2031년까지 25억 7,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 2.88%를 나타낼 전망입니다.

자동차, 항공우주, 반도체 제조 분야의 비접촉식 검사에 대한 지속적인 수요는 일부 성숙한 제조 거점의 설비 투자 예산 압박에도 불구하고 이러한 꾸준한 성장을 뒷받침하고 있습니다. 적층조형, 경량 복합재료, 전자기기의 소형화로의 구조적 변화로 인해 광학 시스템은 현장의 품질관리 루프의 중심에 자리 잡고 있습니다. 접촉식 프로브는 표면 손상 및 미립자 오염의 위험이 있기 때문입니다. 따라서 각 벤더들은 하드웨어의 강성을 단계적으로 향상시키는 것보다 소프트웨어에 의한 정밀도 보정이나 디지털 트윈과의 연계를 중요시하고 있습니다. 이러한 전환은 이미 광학식 3차원 측정기 시장에서 구독 수익의 점유율 확대라는 형태로 나타나고 있습니다. 이와 함께 지역적 다양화도 진행되고 있습니다. 아시아태평양의 전자 산업이 빠르게 성장하면서 북미와 유럽의 성장 문제를 상쇄하고 있으며, 소규모 탁상형 시스템은 의료기기 제조업체와 위탁 가공업체와 같은 새로운 사용자층을 고객층으로 끌어들이고 있습니다.

세계 광학식 3차원 측정기 시장 동향과 인사이트

인더스트리 4.0의 제품 디자인의 변화

격자 구조, 다재료 주조 및 프레스 성형 알루미늄 배터리 하우징의 급속한 보급으로 인해 기존의 측정기기로는 치수 확인이 불충분합니다. 현재 자동차 1등급 공급업체의 60% 이상이 전기자동차 배터리 팩의 용접 피팅의 무결성을 확인하기 위해 광학 시스템을 채택하고 있으며, 0.1mm를 초과하는 편차는 IP 등급을 위협하는 요인으로 작용합니다. 항공우주 산업의 주요 제조업체들은 복합재 기체 섹션에 비접촉식 스캐닝을 지정하여 공구 팁의 편향으로부터 섬세한 라미네이트 소재를 보호하고 있습니다. 공적 자금도 이러한 변화를 반영하고 있습니다. '호라이즌 유럽'은 2024년부터 2025년까지 첨단 계측 기술 연구개발에 1억 2,000만 유로(1억 3,928만 달러)를 배정했습니다. EV의 양산이 확대됨에 따라 중기적 모멘텀은 지속되겠지만, 2028년 이후 설계의 반복이 안정화되면 보급 속도는 둔화될 것으로 예측됩니다.

인라인 검사 및 자동화 도입

각 제조업체들은 광학 시스템을 온도 관리형 실험실에서 자동화 생산 셀로 전환하여 생산라인을 멈추지 않고 100% 검사를 실현하고 있습니다. 독일과 중국의 바디샵에서는 현재 90초 이내에 전체 화이트 바디의 측정을 완료하여 재작업 작업을 40%까지 줄였다고 합니다. 비전 스캐너가 탑재된 협동 로봇의 도입량은 2024년 18% 증가했습니다. 단기적인 영향은 인건비가 높은 지역에서 가장 두드러지지만, 비용에 최적화된 로컬 솔루션으로 인해 아시아태평양에서도 도입이 가속화되고 있습니다.

높은 설비투자 및 TCO

엔트리급 광학 유닛은 5만 달러 내외부터 시작하지만, 하이엔드 멀티센서 브리지는 50만 달러 이상이며, 필수 ISO 10360 재검증을 위해 사이클당 5,000-1만 5,000달러의 추가 비용이 발생합니다. 따라서 많은 중소기업은 사이클 시간이 길어짐에도 불구하고 접촉식 게이지를 선호하고 있습니다. 구독형 패키지도 등장했지만, 그 이용은 여전히 북미와 서유럽에 거의 한정되어 있습니다.

부문 분석

레이저 스캐닝 플랫폼은 2025년 매출의 38.12%를 차지했으며, 화이트 바디 및 터빈 블레이드 검사에서 검증된 정확성을 인정받고 있습니다. 반면, 구조화된 광학 시스템은 CAGR 3.13%로 성장하고 있으며, 측정 주기를 몇 분에서 몇 초로 단축하는 고속 전 영역 캡처 기능이 강조되고 있습니다. 가장 많이 채택되고 있는 분야는 적층 가공 부품과 EV용 배터리 트레이이며, 사용자는 처리량을 우선시하는 대신 ±0.02mm의 불확실성을 허용하고 있습니다. 이에 따라 광학식 3차원 측정기 시장에서는 전자기기 케이스에 0.01mm의 정밀도를 실현한 니콘의 500만 화소 시스템 등 구조화 광학 제품 라인업을 확충하고 있습니다.

대형 항공우주 구조물의 경우, 여전히 레이저 스캐닝이 주류를 이루고 있으며, 반사성 복합재료의 투과와 2m 이상의 측정 범위에 대응하고 있습니다. 한편, 멀티센서 하이브리드 기계는 현재 부품을 이동하지 않고 단일 스테이션에서 알루미늄 주물과 플라스틱 페시아를 검사해야 하는 1등급 자동차 공급업체들 사이에서 인기를 끌고 있습니다. 모든 기술에서 ISO 10360-8 표준을 엄격하게 준수하여 품질 관리 책임자를 안심시키고, 광학식 3차원 측정기 시장을 하이브리드 아키텍처로 더욱 발전시키고 있습니다.

화강암 베이스의 강성과 3m의 측정 범위에서 ±2㎛의 정확도를 실현한 브리지형 측정기는 2025년 매출의 41.53%를 차지하였습니다. 한편, 휴대용 벤치탑형 유닛은 공장에서 CNC 가공 센터 바로 옆에서 측정하여 처리 시간을 단축할 수 있어 연간 3.47%의 성장이 예상됩니다. FARO의 관절식 암 매출은 항공우주 분야의 유지보수 수요에 힘입어 2024년 11% 증가했습니다. 이러한 변화는 다품종 생산 환경에서 광학식 3차원 측정기 시장이 최고 정밀도보다 기동성을 중시하고 있음을 보여줍니다.

브리지형 모델은 온도 및 습도 관리 하에서 서브마이크론 수준의 재현성이 요구되는 교정 실험실 및 항공우주용 지그에서 여전히 필수적인 모델입니다. 반면, 벤치탑형 유닛은 설치 면적이 적고, 정가가 브릿지형 대비 40-60% 저렴해 중소기업(SME)이라는 새로운 고객층을 개척하고 있습니다. 갠트리형 플랫폼은 기체, 선체, 풍력발전용 블레이드 측정 업무에서 여전히 중요한 역할을 하고 있으며, 헥사곤의 18m급 Leitz PMM-Xi 시리즈가 이러한 대형 프로젝트를 확보하고 있습니다.

광학식 3차원 측정기 시장은 제품 유형(멀티 센서, 2D 비전 측정기 등), 기계 유형(브리지형, 갠트리형 등), 구성 요소(하드웨어, 소프트웨어, 서비스), 측정 체적 범위(소형, 중형, 대형), 최종 사용자 산업(항공우주 및 방위, 자동차 등), 지역별로 세분화되어 있습니다. 및 지역별로 세분화되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 34.41%를 차지했으며, 2031년까지 연평균 3.68%의 성장률을 보일 것으로 전망됩니다. 2024년, 반도체 제조 공장이 웨이퍼 레벨 측정이 필요한 3nm 이하 공정에서 수율 향상을 추구한 결과, 중국의 반도체 제조 장비 구매가 22% 급증했습니다. 일본은 뛰어난 광학 기술을 활용하여 국내 CMM 생산량의 68%를 수출했습니다. 한국에서는 배터리 및 로직 칩 생산 확대로 인해 2024년 광학기기 도입량이 14% 증가했습니다. 인도와 아세안 국가들은 뒤쳐져 있지만, 중국 연안에서 전자제품 위탁생산(OEM)이 이전함에 따라 꾸준히 증가하고 있습니다.

북미는 항공우주 및 방위 분야에서 확고한 입지를 유지하고 있습니다. 보잉사의 수주잔고가 1만4000여 대를 넘어서면서 기체 및 주익 검사에 대한 기초적인 수요가 뒷받침되고 있습니다. 배터리 전기자동차(BEV) 플랫폼은 미국 자동차 공장의 신규 도입을 촉진하고 있으며, 2024년 독일에서 82억 유로의 EV 설비투자가 이루어질 것으로 예상에 따라 이러한 모멘텀은 더욱 가속화될 것입니다. 유럽에서는 ISO 10360 및 CE 마킹을 엄격하게 준수하기 때문에 가격이 높게 유지되고 있지만 최고 품질 요구 사항과 밀접하게 연결되어 있습니다.

남미, 중동, 아프리카를 합해도 광학식 3차원 측정기 시장에서 차지하는 비중은 한 자릿수에 불과합니다. 브라질의 조립 사업에서는 다국적 기업의 공장 내에서 광학 솔루션이 채택되고 있지만, 국내 Tier 2 기업들은 도입을 꺼려하고 있습니다. 걸프 국가들은 항공우주 MRO 허브에 자금을 지원하고 날개 위 터빈 점검용 휴대용 암을 구매하고 있지만, 그 도입량은 동종업계에 비해 뒤쳐져 있습니다. 아프리카 GDP에서 제조업이 차지하는 비중이 11%에 불과하기 때문에 대규모 계측 기술에 대한 투자가 억제되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The optical coordinate measuring machine market size is projected to expand from USD 2.17 billion in 2025 and USD 2.23 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 2.88% between 2026 to 2031.

Continuous demand for non-contact inspection in automotive, aerospace, and semiconductor production supports this steady climb, even as capital budgets tighten in several mature manufacturing hubs. Structural shifts toward additive manufacturing, lightweight composites, and electronics miniaturization place optical systems at the center of shop-floor quality loops, because tactile probes risk surface damage or particulate contamination. Vendors are therefore emphasizing software-driven accuracy compensation and digital-twin connectivity over incremental gains in hardware rigidity, a pivot that is already visible in the rising share of subscription revenue inside the optical coordinate measuring machine market. In parallel, regional diversification is underway, Asia Pacific's electronics boom offsets flatter conditions in North America and Europe, while small-volume benchtop systems pull new medical-device and contract-machining users into the customer base.

Global Optical Coordinate Measuring Machine Market Trends and Insights

Changing Product Designs in Industry 4.0

Rapid adoption of lattice structures, multi-material castings, and stamped aluminum battery enclosures has made traditional gauges insufficient for dimensional confirmation. More than 60% of automotive tier-1 suppliers now apply optical systems to check weld-seam integrity in electric-vehicle packs, where deviations above 0.1 mm threaten IP-ratings. Aerospace primes specify non-contact scanning for composite fuselage sections, protecting delicate lamina from tool-tip deflection. Public funding echoes this shift. Horizon Europe earmarked EUR 120 million (USD 139.28 million) for advanced-metrology R&D in 2024-2025. Medium-term momentum persists as serial EV production scales, although penetration slows once design iterations stabilize after 2028.

Adoption of In-Line Inspection and Automation

Manufacturers are relocating optical systems from climate-controlled labs to automated production cells, enabling 100% inspection without pausing throughput. German and Chinese body-shops now finish full body-in-white measurement in under 90 seconds, trimming rework by 40%. Collaborative-robot installations housing vision scanners jumped 18% in 2024. The short-term impact is strongest where labor is expensive, but cost-optimized local solutions are accelerating adoption in Asia Pacific as well.

High Capital Expenditure and TCO

Entry-level optical units start near USD 50 000, while high-end multi-sensor bridges exceed USD 500 000, and mandatory ISO 10360 reverification adds USD 5 000-15 000 per cycle. Many small firms, therefore, favor tactile gauges, despite longer cycle times. Subscription bundles are emerging but remain largely confined to North America and Western Europe.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Composite Parts Require Optical Metrology

- High-Precision Additive Manufacturing Demand

- Lack of Skilled Metrology Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser scanning platforms delivered 38.12% of 2025 revenue, favored for proven accuracy in body-in-white and turbine-blade checks. Conversely, structured-light systems will pace at 3.13% CAGR, prized for rapid full-field capture that compresses measurement cycles from minutes to seconds. Adoption is strongest in additive-manufactured components and EV battery trays, where users accept +-0.02 mm uncertainty in exchange for throughput. The optical coordinate measuring machine market responds by widening structured-light product lines, such as Nikon's 5-MP system that achieves 0.01 mm accuracy for electronics casings.

Large-volume aerospace structures still rely on laser scanning to penetrate reflective composites and handle envelopes above 2 m. Multi-sensor hybrids now find traction in tier-1 automotive suppliers needing a single station to check aluminum castings and plastic fascias without relocating parts. Tight ISO 10360-8 conformance across technologies reassures quality managers, further propelling the optical coordinate measuring machine market toward hybrid architectures.

Bridge machines held 41.53% of 2025 takings thanks to granite-base rigidity and +-2 µm accuracy over 3 m volumes. Portable benchtop units, however, will expand 3.47% annually as factories pull measurement next to CNC centers, trimming handling time. FARO's articulated arm revenue grew 11% in 2024 on aerospace maintenance demand. This shift underscores how the optical coordinate measuring machine market values agility over maximum precision in high-mix settings.

Bridge models remain indispensable for calibration labs and aerospace jigs that demand sub-micrometer repeatability under climate control. Yet benchtop units unlock new SME customers because floor-space needs shrink and list prices fall 40-60% below bridge equivalents. Gantry platforms stay relevant for fuselage, ship hull, and wind-blade tasks; Hexagon's 18-m Leitz PMM-Xi line secures these outsize jobs.

Optical Coordinate Measuring Machine Market is Segmented by Product Type (Multi-Sensor, 2D Vision Measurement Machine, and More), Machine Type (Bridge, Gantry, and More), Component (Hardware, Software, and Services), Measurement Volume Range (Small, Medium, and Large), End-User Industry (Aerospace and Defense, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 34.41% of global sales in 2025 and will climb at 3.68% CAGR through 2031. China's semiconductor equipment buy surged 22% in 2024 as fabs chased sub-3 nm yields that require wafer-level metrology. Japan exported 68% of domestic CMM output, leveraging elite optical know-how. South Korea's battery and logic chip expansions pushed optical installs up 14% in 2024. India and ASEAN nations trail but rise steadily as contract-electronics manufacturing migrates from coastal China.

North America retains a stronghold in aerospace and defense. Boeing's backlog above 14 000 jets protects baseline demand for fuselage and wing inspections. Battery-electric platforms fuel new installs in U.S. auto plants, amplified by EUR 8.2 billion EV cap-ex in Germany during 2024. Europe's strict conformity to ISO 10360 and CE marking keeps prices high yet lock-step with premium quality requirements.

South America, the Middle East, and Africa collectively represent single-digit percentages of the optical coordinate measuring machine market. Brazil's assembly operations adopt optical solutions inside multinational plants but domestic tier-2 firms hesitate. Gulf states fund aerospace MRO hubs, buying portable arms for on-wing turbine checks, yet volumes lag industrial peers. Africa's 11% manufacturing share of GDP undercuts large-scale metrology investment.

- Hexagon AB

- Carl Zeiss AG

- Mitutoyo Corp.

- Nikon Metrology NV

- Werth Messtechnik GmbH

- OGP (Quality Vision International, Inc.)

- Micro-Vu Corp.

- Keyence Corp.

- Renishaw plc

- FARO Technologies Inc.

- Creaform Inc. (AMETEK)

- Perceptron Inc. (Atlas Copco)

- LK Metrology Ltd.

- Coord3 S.r.l.

- Automated Precision Inc. (API)

- Wenzel Group GmbH and Co. KG

- Vision Engineering Ltd.

- Metronor AS

- Helmel Engineering Products Inc.

- Aberlink Ltd.

- InspecVision Ltd.

- Innovative Optical Measuring Systems (IOMS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Changing Product Designs in Industry 4.0

- 4.2.2 Adoption of In-Line Inspection and Automation

- 4.2.3 Lightweight Composite Parts Require Optical Metrology

- 4.2.4 High-Precision Additive Manufacturing Demand

- 4.2.5 Regulatory Push for First-Article Inspection

- 4.2.6 AI-Driven Error-Compensation Algorithms

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure and TCO

- 4.3.2 Lack of Skilled Metrology Workforce

- 4.3.3 Environmental Sensitivity on Shop-Floor

- 4.3.4 Cyber-Security and IP-Leakage Concerns

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Multi-Sensor

- 5.1.2 2D Vision Measurement Machine

- 5.1.3 3D Vision Measurement Machine

- 5.1.4 Laser Scanning Optical CMM

- 5.1.5 Structured-Light Optical CMM

- 5.2 By Machine Type

- 5.2.1 Bridge

- 5.2.2 Gantry

- 5.2.3 Articulated Arm

- 5.2.4 Horizontal

- 5.2.5 Portable Benchtop

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Measurement Volume Range

- 5.4.1 Small (? 500 mm)

- 5.4.2 Medium (500-2 000 mm)

- 5.4.3 Large (> 2 000 mm)

- 5.5 By End-User Industry

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Medical Device and Orthopedics

- 5.5.4 Heavy Machinery and Metal Fabrication

- 5.5.5 Electronics and Semiconductor

- 5.5.6 Energy and Power Generation

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Hexagon AB

- 6.4.2 Carl Zeiss AG

- 6.4.3 Mitutoyo Corp.

- 6.4.4 Nikon Metrology NV

- 6.4.5 Werth Messtechnik GmbH

- 6.4.6 OGP (Quality Vision International, Inc.)

- 6.4.7 Micro-Vu Corp.

- 6.4.8 Keyence Corp.

- 6.4.9 Renishaw plc

- 6.4.10 FARO Technologies Inc.

- 6.4.11 Creaform Inc. (AMETEK)

- 6.4.12 Perceptron Inc. (Atlas Copco)

- 6.4.13 LK Metrology Ltd.

- 6.4.14 Coord3 S.r.l.

- 6.4.15 Automated Precision Inc. (API)

- 6.4.16 Wenzel Group GmbH and Co. KG

- 6.4.17 Vision Engineering Ltd.

- 6.4.18 Metronor AS

- 6.4.19 Helmel Engineering Products Inc.

- 6.4.20 Aberlink Ltd.

- 6.4.21 InspecVision Ltd.

- 6.4.22 Innovative Optical Measuring Systems (IOMS)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment