|

시장보고서

상품코드

2044199

조강(Crude Steel) 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Crude Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

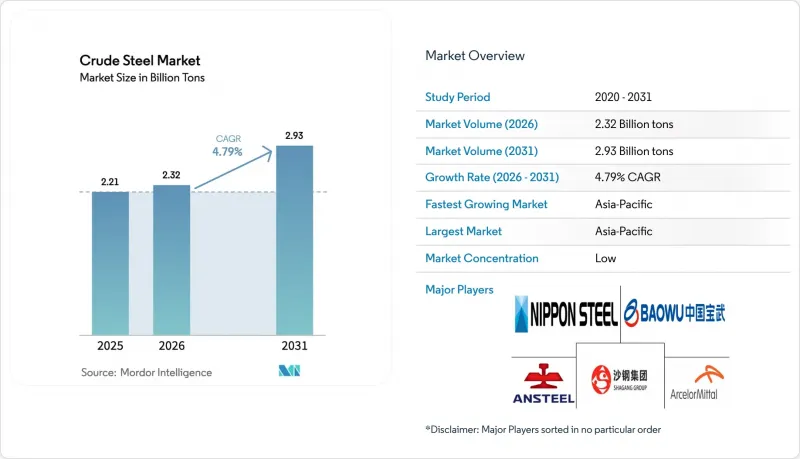

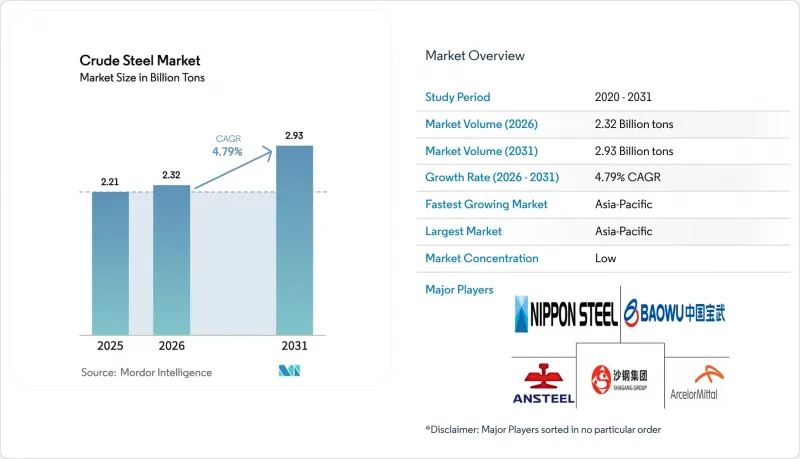

2026년 조강(Crude Steel) 시장 규모는 23억 2,000만 톤과 추산 되고 있으며 2025년 22억 1,000만 톤으로부터 확대해, 2031년에는 29억 3,000만 톤에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.79%를 나타낼 것으로 예측됩니다.

탈탄소화 목표의 강화, 스크랩 회수 시스템의 성숙, 재생 가능 전력의 가격 하락에 따라 전기 아크로(EAF) 기술이 고로/기본 산소로(BOF) 공정을 대체하고 있습니다. 아시아태평양은 대규모 도시 인프라 계획을 통해 수요의 대부분을 차지하고 있지만, 인도의 생산 능력 확대와 아세안의 메가 프로젝트가 중국의 부동산 경기 둔화를 점점 더 상쇄하고 있습니다. 최종 사용자 동향을 살펴보면, 공공 인프라와 주택이 연간 생산량의 절반 이상을 차지하고 있으며, 교통의 전동화, 기계 교체, 재생에너지의 정비 등이 생산량 증가에 기여하고 있습니다. 경쟁 환경은 전기로(EAF)에 대한 투자 러시, 수소를 이용한 직접 환원법 시범사업, 그리고 탄소국경조정세와 구매자의 탈탄소화 요구사항에 대비한 저탄소 생산 체제를 확보하기 위한 대형 인수합병으로 형성되고 있습니다. 이에 따라 통합 제조업체들은 미래 자산 좌초 및 그린 프리미엄의 불확실성에 대한 헤지 수단으로 고로 전환, 전자기 강판 생산 라인 및 공정 열 솔루션에 사상 최대 규모의 자본을 투입하고 있습니다.

세계 조강 시장 동향과 인사이트

주요 20개 철강사의 탈탄소화 관련 설비투자 경쟁

2030년까지 완공 예정인 저탄소 고로 전환, 수소를 이용한 직접 환원 설비, 전자기 강판 생산 라인에 2,000억 달러 이상이 배정되어 있습니다. 앨라배마 주에 건설될 12억 달러 규모의 알세롤 메탈(ArcelorMetal)의 전해강판 공장과 2030년까지 CO2 배출량 30% 감축을 목표로 하는 티센크루프의 'tkH2Steel' 프로그램은 선구자적 우위를 강조하고 있습니다. 2026년 초로 예정된 시범운영을 통해 재생에너지의 가격이 화석연료와 동등해지면 기존 생산 경로와의 비용 동등성을 입증할 수 있을 것으로 예측됩니다. 조기 도입 기업은 Scope 3 배출량 감축을 열망하는 자동차 및 가전업체와의 가격 협상에서 우위를 점할 수 있는 반면, 후발주자는 탄소국경세 강화에 따라 고로 자산이 '좌초 자산'이 될 수 있는 위험을 감수해야 합니다.

2030년까지 인도와 아세안의 건설 슈퍼 사이클

2047년까지 조강 생산 능력을 5억 톤으로 늘리겠다는 인도의 목표는 2025년 3억 1,800만 톤에 달하는 국내 철광석 생산량에 힘입어 장강 및 구조용 강재 분야에서 지역적 호황을 누리고 있습니다. 인도네시아 누산타라 수도 계획, 태국 동부 경제회랑 등 아세안 메가 프로젝트들은 금세기 10년 동안 총 5,000만 톤 이상 수요를 필요로 합니다. SteelAsia를 필두로 한 지역 투자자들은 가치사슬을 단축하고 고부가가치 가공 사업을 확보하기 위해 여러 전기로(EAF) 라인에 650억 필리핀 페소를 투자하고 있습니다. 지속적인 성장은 지속적인 재정지출과 외국인 직접투자의 유입에 달려있지만, 금리 사이클과 원자재 가격 변동이 하방 위험요인으로 작용하고 있습니다.

예상보다 더딘 중국 부동산 시장 회복

2024년 9월 중국의 월간 신규 주택 판매량은 전년 동월 대비 37.7% 감소하여, 2019년 최고치(2억 9,600만 톤)에서 이미 반토막 난 주택용 철강재 수요를 더욱 감소시켰습니다. 그 결과, 중국 제철소의 수출 확대로 인해 지역 가격이 하락하고, 특히 동남아시아에서 무역 마찰을 일으키고 있습니다. 장기적인 수요의 감소는 인구의 두드림과 공실률의 상승과 관련이 있으며, 이는 순환적 조정이라기보다는 구조적 조정이라는 것을 시사하고 있습니다.

부문 분석

2025년, 킬드강은 조강 시장 점유율의 54.18%를 차지하여 현대 슬래브 생산의 거의 전부를 차지하는 연속 주조 라인에 필수 불가결한 존재임을 반영합니다. 알루미늄 및 실리콘계 탈산제는 가스 발생을 억제하여 표면의 기공을 최소화하고 수율을 향상시킵니다. 자동차 제조업체들이 경량 섀시 부품에 대한 화학 성분의 편석을 제어하고자 하는 가운데, 세미 킬드 강종은 2031년까지 연평균 복합 성장률(CAGR) 4.9%로 전체 시장 성장률을 상회할 것으로 예측됩니다. 림드강과 캡드강은 틈새 강판 및 강대 이용 사례에서 계속 사용되고 있지만, 통합 제철소가 수율과 청결을 우선시함에 따라 구조적으로 감소하는 추세에 있습니다.

전기 아크로(EAF) 운영자들은 합금 회수율을 극대화하고 재작업을 줄이기 위해 킬강 사양을 늘려 이 부문에서 우위를 점하고 있습니다. 한편, 세미 킬드강에 대한 관심이 높아지는 것은 자동차 제조업체들이 정밀한 미량 합금화를 필요로 하는 고급 고강도 강으로 전환하는 것과 일치합니다. 규제 요인은 조성 선택에 직접적인 영향을 거의 미치지 않지만, 에너지 집약도 측면에서 제철소는 경제적 이익을 얻기 위해 탈산 공정의 합리화 및 알루미늄 첨가제 회수를 촉진하고 있습니다.

"조강 시장 보고서는 조강 유형(킬드강 및 반킬드강), 제조 공정(기본산소로(BOF) 및 전기 아크로(EAF)), 최종 이용 산업(건축 및 건설, 운송, 기타 최종 이용 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 수량(톤) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 출하량의 73.52%를 차지하며, 인도의 연간 생산능력 5억 톤 확대 계획과 아세안 국가들의 건설 프로젝트 진행에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 4.86%를 나타낼 것으로 예측됩니다. 중국 주택시장 주도의 경기둔화로 인한 공급과잉으로 인해 수출시장으로 향하는 물량이 점점 증가하고 있으며, 남아시아와 라틴아메리카 전역에서 반덤핑 조치가 취해지고 있습니다. 일본과 한국은 강력한 정부 보조금을 배경으로 전자기강판 특화 생산과 수소대응로에 집중하고 있습니다.

북미에서는 '초당적 인프라법' 및 '인플레이션 억제법'에 따라 수요 전망이 밝아지고 있지만, 공급 측면에서는 신일철주금의 149억 달러 규모의 US스틸 인수와 같은 대형 프로젝트를 중심으로 재편이 진행되고 있습니다. 풍부한 스크랩과 재생가능 전력은 전기로(EAF) 생산능력 확대에 유리한 조건이며, 캐나다는 수력 발전망을 활용하고, 멕시코는 생산 회귀(리쇼어링)에 따른 자동차용 강재 수주를 확보하고 있습니다.

유럽에서는 에너지 가격 급등이라는 역풍에 대해 효율화 추진, EU 철강기금의 보조금, 수입품의 가격경쟁력 시정을 위한 탄소국경조정세 등을 통해 대응하고 있습니다. 남미와 중동 및 아프리카는 인프라 및 자원 가공 플랜트를 기반으로 한 한 자릿수 중반의 성장이 예상되지만, 자금 조달의 제약으로 인해 프로젝트 파이프라인이 제한적일 것으로 예측됩니다. 운임 상승과 Scope 3 배출량 산정을 계기로 한 공급망 지역화는 전 세계 제철소 입지 및 제품 구성 결정에 영향을 미치는 공통된 주제입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 및 수량)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02Crude Steel market size in 2026 is estimated at 2.32 billion tons, growing from 2025 value of 2.21 billion tons with 2031 projections showing 2.93 billion tons, growing at 4.79% CAGR over 2026-2031.

Electric-arc-furnace (EAF) technology is steadily displacing blast-furnace/basic-oxygen-furnace (BOF) routes as decarbonization targets tighten, scrap collection systems mature, and renewable electricity becomes more affordable. Asia-Pacific commands the bulk of demand through large-scale urban infrastructure programs, while India's capacity expansion and ASEAN mega-projects increasingly counterbalance China's easing property cycle. End-user trends show public infrastructure and housing absorbing more than half of annual volume, with transportation electrification, machinery upgrades, and renewable-energy build-outs adding incremental tonnage. Competitive dynamics are shaped by a wave of EAF investments, hydrogen-based direct-reduction pilots, and headline acquisitions that aim to secure low-carbon production footprints in anticipation of carbon-border levies and buyer decarbonization mandates. Integrated producers therefore channel record capital into furnace conversions, electrical-steel lines, and process-heat solutions to hedge against future asset stranding and green-premium uncertainty.

Global Crude Steel Market Trends and Insights

Decarbonization-Linked Capex Race Among Top 20 Steelmakers

More than USD 200 billion has been earmarked for low-carbon furnace conversions, hydrogen-based direct-reduction units, and electrical-steel lines scheduled for completion before 2030. ArcelorMittal's USD 1.2 billion electrical-steel plant in Alabama and thyssenkrupp's tkH2Steel program targeting a 30% CO2 cut by 2030 highlight the first-mover premium. Pilot operations scheduled for early 2026 are expected to validate cost parity with conventional routes once renewable electricity prices converge with fossil alternatives. Early adopters gain price-negotiation leverage with automotive and appliance buyers eager to shrink Scope 3 emissions, while late movers risk stranded blast-furnace assets under tightening carbon-border taxes.

Construction Super-Cycle in India and ASEAN Through 2030

India's target of boosting installed crude-steel capacity to 500 million tons by 2047 anchors a regional boom in long and structural steel, underpinned by domestic iron-ore output that rose to 318 million tons in 2025. Parallel ASEAN megaprojects-such as Indonesia's Nusantara capital and Thailand's Eastern Economic Corridor-collectively require more than 50 million tons in the current decade. Regional investors led by SteelAsia are deploying PHP 65 billion across multiple EAF lines to shorten supply chains and capture value-added fabrication. Sustained growth rests on continued fiscal spending and foreign-direct-investment inflows, although interest-rate cycles and raw-material price swings pose downside risk.

Slower-Than-Expected Chinese Real-Estate Recovery

Monthly new-home sales in China fell 37.7% year-on-year in September 2024, trimming residential-steel demand that had already halved from its 2019 peak of 296 million tons. The resulting export push by Chinese mills depresses regional prices and sparks trade friction, particularly in Southeast Asia. Long-term demand destruction is tied to demographic plateauing and higher vacancy rates, pointing to a structural rather than cyclical adjustment.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting Push Reviving Value-Added Flat Steel

- Green-Hydrogen Project Pipelines Lowering Long-Run Power Cost

- Trade-Remedy Proliferation Hampering Cross-Border Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Killed steel captured 54.18% of the crude steel market share in 2025, reflecting its indispensability to continuous casting lines that account for nearly all modern slab production. Aluminum and silicon deoxidizers suppress gas evolution, which minimizes surface voids and improves yield. Semi-killed grades are expected to outpace overall growth at a 4.9% CAGR through 2031 as automakers seek controlled chemical segregation for lightweight chassis components. Rimmed and capped steels continue to serve niche sheet and strip use cases but remain in structural decline as integrated mills prioritize yield and cleanliness.

EAF operators increasingly specify killed grades to maximize alloy recovery and reduce rework, reinforcing the segment's predominance. Meanwhile, semi-killed steel's rising profile aligns with automakers' transition to advanced high-strength steels requiring precise micro-alloying. Regulatory factors exert minimal direct influence on composition choice, though energy-intensity considerations encourage mills to streamline deoxidation practices and recover aluminum additions for economic gain.

The Crude Steel Market Report is Segmented by Composition (Killed Steel and Semi-Killed Steel), Manufacturing Process (Basic Oxygen Furnace (BOF) and Electric Arc Furnace (EAF)), End-User Industry (Building and Construction, Transportation, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 73.52% of 2025 shipments and is projected to grow at 4.86% CAGR to 2031, supported by India's planned scale-up to 500 million tons of annual capacity and ASEAN construction pipelines. China's housing-driven soft patch generates a surplus that increasingly targets export markets, prompting anti-dumping actions across South Asia and Latin America. Japan and South Korea shift focus to electrical-steel specialisms and hydrogen-ready furnaces backed by strong governmental subsidies.

North America's demand outlook brightens under the Bipartisan Infrastructure Law and the Inflation Reduction Act, though the region's supply side is consolidating around headline deals such as Nippon Steel's USD 14.9 billion take-over of U.S. Steel. Abundant scrap and renewable electricity create fertile ground for EAF capacity, with Canada leveraging hydro-powered grids and Mexico capturing reshoring-induced auto-steel orders.

Europe combats energy-price headwinds via efficiency upgrades, EU steel fund grants, and carbon-border tariffs aimed at leveling imports. South America and Middle East-Africa present mid-single-digit growth rooted in infrastructure and resource-processing plants, though financing constraints limit project pipelines. Regionalization of supply chains, triggered by freight-cost inflation and Scope 3 accounting, is a unifying theme influencing mill location and product-mix decisions worldwide.

- ArcelorMittal

- China Ansteel Group Corporation Limited

- China BaoWu Steel Group Corporation Limited

- Fangda Special Steel Technology

- HBIS Group

- Hunan Valin Iron and Steel Co., Ltd.

- Hyundai Steel

- JFE Steel Corporation

- Jiangsu Shagang Group

- JSW

- Nippon Steel Corporation

- NLMK Group

- Nucor Corporation

- POSCO HOLDINGS

- Rizhao Steel Holding Group CO., LTD.

- SAIL

- Tata Steel

- Techint Group

- United States Steel Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation-Linked Capex Race Among Top 20 Steelmakers

- 4.2.2 Construction Super-Cycle in India and ASEAN Through 2030

- 4.2.3 Automotive Lightweighting Push Reviving Value-Added Flat Steel

- 4.2.4 Green-Hydrogen Project Pipelines Lowering Long-Run Power Cost

- 4.2.5 Rapid Build-Out of Small Modular Reactors for Process Heat

- 4.3 Market Restraints

- 4.3.1 Slower-Than-Expected Chinese Real-Estate Recovery

- 4.3.2 Trade-Remedy Proliferation Hampering Cross-Border Flows

- 4.3.3 Green-Premia Uncertainty Delaying Offtake Agreements

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Supply Analysis

- 4.7 Regulatory Policy Analysis

- 4.8 Trade Analysis

- 4.9 Price Trend Analysis

- 4.10 Production Cost Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Composition

- 5.1.1 Killed Steel

- 5.1.2 Semi-killed Steel

- 5.2 By Manufacturing Process

- 5.2.1 Basic Oxygen Furnace (BOF)

- 5.2.2 Electric Arc Furnace (EAF)

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Transportation

- 5.3.3 Tools and Machinery

- 5.3.4 Energy

- 5.3.5 Consumer Goods

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 China Ansteel Group Corporation Limited

- 6.4.3 China BaoWu Steel Group Corporation Limited

- 6.4.4 Fangda Special Steel Technology

- 6.4.5 HBIS Group

- 6.4.6 Hunan Valin Iron and Steel Co., Ltd.

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corporation

- 6.4.9 Jiangsu Shagang Group

- 6.4.10 JSW

- 6.4.11 Nippon Steel Corporation

- 6.4.12 NLMK Group

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO HOLDINGS

- 6.4.15 Rizhao Steel Holding Group CO., LTD.

- 6.4.16 SAIL

- 6.4.17 Tata Steel

- 6.4.18 Techint Group

- 6.4.19 United States Steel Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment