|

시장보고서

상품코드

2044201

상업용 주방 기기 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Commercial Kitchen Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

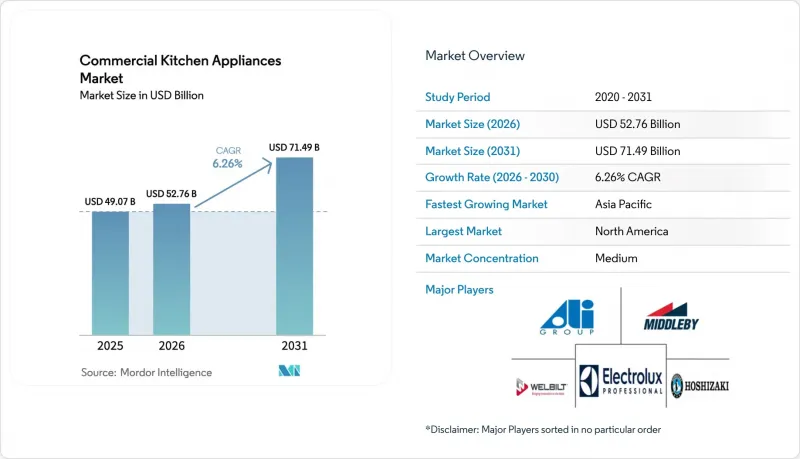

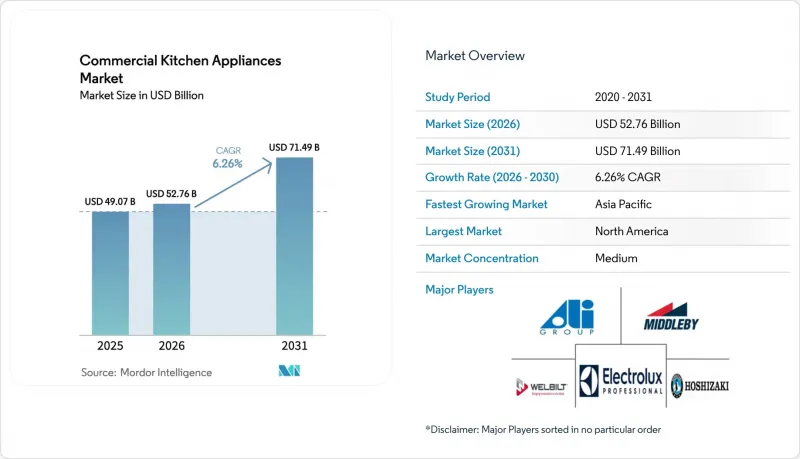

상업용 주방 기기 시장 규모는 2025년에 490억 7,000만 달러로 평가되었고 2026년 527억 6,000만 달러에서 2031년까지 714억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.26%를 나타낼 전망입니다.

사업자들은 공간 절약, 에너지 비용 절감, 중앙 집중식 주문 및 서비스 플랫폼과의 연계가 가능한 다기능, 네트워크 연결 장비로 기존 장비를 교체하고 있으며, 이로 인해 단일 기능 장비에 대한 자본 배분이 감소하고 있습니다. 주요 퀵서비스 체인의 확장 계획은 각 체인이 표준화 된 IoT 지원 백 오피스 시스템을 확장하고 처리 능력을 향상시키고 거래 당 인건비를 절감하기 때문에 계속해서 강력한 수요를 주도하고 있습니다. 이와 함께, 가장 빠르게 성장하는 응용 분야는 클라우드 키친과 고스트 키친으로, 배달을 우선시하는 업태가 소형의 고처리량 조리, 보온, 냉장 플랫폼을 선호함에 따라 2031년까지 연평균 복합 성장률(CAGR) 10.32%를 나타낼 것으로 예측됩니다. 또한, 대형 체인이 대량 구매를 통한 가격 우대 및 라이프사이클 서비스 일괄 제공을 보장하기 위해 직접 조달로 전환함에 따라 유통 모델도 진화하고 있으며, 규제 및 공급 변화에 대한 내성을 높이고 있습니다.

세계 상업용 주방 기기 시장 동향 및 인사이트

QSR 체인 및 외식산업 확대

대형 퀵서비스 업체들은 적극적인 신규 매장 건설 및 리노베이션을 진행하고 있으며, 조리, 냉장, 식기 세척 등 각 카테고리의 상업용 주방 장비 구매 수요를 뒷받침하고 있습니다. 맥도날드는 설비투자를 늘리고, 2025년까지 약 2,200개 매장을 오픈하겠다는 계획을 밝혔습니다. 이는 30억-32억 달러의 설비 투자 규모와 2027년까지 50,000개 매장으로 확대한다는 다년간의 목표에 따라, 성숙 시장과 개발도상국 시장 모두에서 표준화된 고처리 용량 장비에 대한 수요가 직접적으로 증가하고 있습니다. Brands는 2025년 3분기 디지털 매출 100억 달러(디지털 비중 60%)를 달성하고, 같은 기간 분기 사상 최대인 1,131개의 신규 매장을 오픈하며 커넥티드 프라이어, 오븐, KDS 통합 플랫폼에 대한 조달 수요를 창출했습니다. 운영자가 거래당 처리 속도 향상과 인건비 절감을 요구하고, 다국적 체인이 광범위한 매장 기반에서 통일된 결과를 필요로 하는 상황에서 연결성과 자동화는 현재 프리미엄 가치를 창출하고 있습니다. 인도와 아시아태평양에서는 도시 지역의 소득 증가와 인구 밀집 지역으로 인해 QSR(Quick Service Restaurant) 형태의 매장이 빠르게 증가하고 있으며, 이는 상업용 주방 장비 시장에서 다년간의 장비 교체 주기의 기반이 되고 있습니다. 메뉴의 현지화가 진행되고 디지털 주문의 흐름이 활발해짐에 따라, 장비 사양은 일관성, 빠른 복구 시간 및 서비스 중단 시간을 단축하는 원격 진단이 우선시되고 있으며, 이로 인해 사업자들이 신규 출점 시 채택하는 플랫폼의 선택이 강화되고 있습니다. 되고 있습니다.

호스피탈리티 업계에서 건설 붐이 일어나고 있습니다.

호텔, 리조트, 서비스 아파트가 다양한 고객 및 이벤트 요구에 적합한 주방을 구축함에 따라 호스피탈리티 분야의 설비투자는 다년간의 설비 수요를 지속적으로 창출하고 있습니다. 사우디의 딜리야 개발을 포함한 중동의 프로젝트 흐름은 여전히 크고, 건설 단계에 따라 오븐, 냉장고, 대용량 식기 세척기 등에 대한 대규모의 단계별 조달 일정이 수년까지 수립되어 있습니다. 장기 체류형 시설에서는 간이 주방과 공용 조리공간에 대한 지출 비중이 높아지고 있으며, 언더 카운터형 냉장고, 소형 IH 쿡탑, 효율적인 식기 세척기에 대한 수요가 증가하고 있습니다. 인도에서는 국내 관광 및 비즈니스 여행과 관련된 신규 및 개조된 호텔 시설에서 검증된 성능 지표를 갖춘 에너지 절약형 가전제품을 채택하고 있으며, 이는 부품 및 서비스에 쉽게 접근할 수 있는 장수명 기기를 우선시하는 조달 프레임워크에 부합하는 것입니다. 여러 시설을 운영하는 그룹사에서는 일원화된 구매 체계와 표준화된 주방 설계를 통해 단위 비용 절감과 설치 일정의 효율화를 꾀하고 있으며, 이에 따라 컴플라이언스 관련 서류 제공과 시운전 지원을 대규모로 할 수 있는 벤더가 우위를 점하고 있습니다. 인플레이션과 자금 조달 환경이 여전히 어려운 가운데, 운영사들은 명확한 광열비 및 유지보수 비용 절감을 기대할 수 있는 장비를 우선적으로 선택하고 있으며, 측정 가능한 투자 회수 효과가 입증된 ENERGY STAR 인증 모델에 대한 안정적인 수요가 유지되고 있습니다.

중소기업은 고가의 초기 설비투자에 어려움을 겪고 있습니다.

기업 수준의 할인이나 유리한 융자 조건을 협상할 수 없는 중소규모 사업자에게는 자금 조달 접근성과 비용 인플레이션이 여전히 구조적인 제약으로 작용하고 있습니다. 캐나다의 조사 데이터에 따르면, 중소기업의 69%가 설비비용을 설비투자 억제요인으로 꼽았고, 50%는 현금 흐름의 제약, 47%는 높은 차입비용을 지적하였습니다. 또한, 65%는 여전히 평균 10만 8,000달러에 달하는 팬데믹 관련 부채를 보유하고 있으며, 이는 신규 설비 예산을 압박하고 있습니다. 융자 심사 기준의 상향 조정과 심사 기준의 강화로 인해 명확한 투자 회수가 기대되는 것, 초기 비용이 많이 드는 에너지 절약형 및 IoT 지원 장비의 구매에 대한 장벽이 높아지고 있습니다. 인도의 독립 레스토랑과 클라우드 키친 스타트업도 비슷한 예산 조정에 직면해 있습니다. 설비 니즈가 기본적인 조리용 장비에 그치지 않고 식품 안전 기준을 충족하기 위한 냉장, 식기 세척, 온도 기록용 하드웨어까지 확대되고 있기 때문입니다. 이에 따라 사업자들은 중요도 및 투자 회수 기간에 따라 단계적으로 설비를 교체하는 경우가 많으며, 이로 인해 교체 주기가 길어지고 있습니다. 향후 초기 비용을 절감할 수 있는 혁신적인 자금 조달 수단과 벤더의 서비스 패키지가 상업용 주방 장비 시장에서의 도입을 촉진할 수 있습니다.

부문 분석

2025년에는 냉장고가 34.36%의 시장 점유율을 차지하며 제품 구성에서 1위를 차지했습니다. 이는 오랜 기간 외식업계의 사업에서 워크인 냉장고, 리치인 냉장고, 언더카운터형 냉장고의 지속적인 교체 수요를 반영한 것입니다. 조리기기는 컴팩트한 면적에 다기능성을 집약한 고효율 프라이어, 철판, 콤비 오븐 등 수요를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 8.24%로 확대될 것으로 예측됩니다. 상업용 스팀 쿠커 및 식기 세척기와 같은 장비는 측정 가능한 연간 에너지 및 물 사용량을 절감하고 매장 수준의 경제성을 향상시키기 때문에 입증된 효율성은 여전히 조달에 있어 중요한 요소로 작용합니다. 전기화 추진 노력과 건축 기준에 따라 신규 프로젝트가 백오브하우스(주방)의 완전 전기화 구성으로 이어질 경우, 유도가열식 오븐과 첨단 오븐이 우선순위를 차지하게 됩니다. 이 접근 방식은 대기 질과 안전을 중시하는 인도의 대도시 지역에서 호응을 얻고 있습니다. 또한, 센서와 클라우드 연결을 기반으로 한 제품 에코시스템은 다점포 사업자의 온도 프로파일, 재고 재고, 유지보수 간격 모니터링을 지원하여 상업용 주방 기기 시장에서 모든 설비의 컴플라이언스 준수와 가동률 향상에 기여하고 있습니다.

베이커리, 케이터링, QSR(퀵 서비스 레스토랑) 및 상업용 주방에서는 처리 능력, 균일성 및 유지 보수 용이성에 따라 제품 선택이 점점 더 다양해지고 있으며, 각 주방은 처리 능력, 균일성 및 유지 보수 용이성에 대해 서로 다른 가중치를 부여하고 있습니다. 전자레인지와 임핑지먼트 기술을 결합한 고속 오븐의 변형은 급증하는 배송 수요에 대응하고, 견고한 컨벡션 유닛은 배치 처리의 필수품으로 자리 잡았습니다. ENERGY STAR 인증 식기세척기는 에너지와 물을 모두 절약할 수 있으며, 이는 물 부족 지역에 위치한 시설에서 물 사용량이 급증할 경우 요금 체계가 페널티를 부과하는 중요한 요소입니다. 예측 기간 동안 통합 제어 시스템을 통한 교육 시간 단축과 재현성 향상으로 인해 조리 장비는 상업용 주방 기기 시장에서 점유율을 확대할 것으로 예측됩니다. 인도에서는 매장 내 음식과 배달 채널을 동시에 운영하는 체인점들이 호환 가능한 냉장 및 난방 장비 패키지의 표준화를 추진하고 있으며, 그 결과 상업용 주방 장비 업계에서 형식에 관계없이 부품, 교육, 서비스 절차가 공통화되어 있습니다.

지역별 분석

2025년 북미는 전 세계 매출의 26.38%를 차지했습니다. 이는 이 지역의 다점포 레스토랑 시스템의 탄탄한 기반과 커넥티드 및 에너지 효율이 높은 장비의 광범위한 도입을 반영합니다. 미국 AIM법이 GWP가 높은 냉매의 사용을 제한하고 대용량 시스템에 대해 보다 엄격한 누출 감지 및 수리 프로토콜을 의무화함에 따라 2026년까지 정책적 요인이 구매 패턴에 계속 영향을 미칠 것입니다. 이에 따라 외식업용 냉장실 및 워크인 냉장고의 장비 교체 수요가 증가하고 있습니다. 캐나다의 중소기업들은 지속적인 자금 압박과 팬데믹 기간 동안 부채 부담으로 인해 초기 투자에 대한 의욕이 떨어졌다고 보고하고 있습니다. 그 결과, 금융 및 서비스 주도형 모델에 대한 관심은 높은 수준을 유지하고 있습니다. 또한, 이 지역의 규제 프레임워크와 식품 안전 기준도 성능이 입증된 로그 기록 기능을 갖춘 장비의 도입을 촉진하고 있습니다. 중기적으로 이러한 요인들은 상업용 주방 기기 시장에서 교체 및 업그레이드 수요의 안정적 기반을 계속 유지할 것입니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 6.87%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이는 중국, 인도, 동남아시아의 도시화, 소득 증가, QSR(Quick Service Restaurant) 및 배달 우선형 포맷의 확대로 인해 장비 수요가 심화되고 있기 때문입니다. Brands는 전 세계적으로 수천 개의 매장을 순증하고 있으며, 그 중 상당수가 아시아태평양에 집중되어 있습니다. 또한, 디지털 주문량 증가에 따라 처리 능력 중심의 장비에 대한 수요가 증가하고 있습니다. 인도에서는 2급 및 3급 도시의 성장과 함께 식품 안전 기준을 충족하기 위한 표준화된 조리 장비 패키지와 온도 기록 기능을 갖춘 신뢰할 수 있는 냉장 장비에 대한 수요가 증가하고 있습니다. 설비 선정에는 현지의 규제와 전기화의 진전도 반영되어 있으며, 설치가 빠르고 열 제어가 안정적이라는 장점으로 인해 도시 지역의 주방에서는 유도가열의 채택이 증가하고 있습니다. 이러한 추세는 업소용 주방기기 시장 전체에서 매장당 설비 도입률의 향상과 보다 안정적인 교체 주기를 뒷받침하는 기반이 되고 있습니다.

유럽, 중동 및 아프리카에서는 그 기세가 엇갈리고 있습니다. 유럽 사업자들은 에너지 비용과 신규 및 개조 시스템에서 자연 냉매로의 전환을 촉진하는 F가스 규정 개정에 적응하고 있습니다. CO2 및 탄화수소 솔루션으로의 전환은 이미 유럽 소매용 냉장 분야에서는 이미 자리를 잡았으며, 호텔 업계 사업자들은 이러한 노하우를 푸드서비스용 냉장실과 리치인 냉장고에 적용하고 있습니다. 중동에서는 사우디아라비아의 딜리야 프로젝트와 같은 대규모 개발이 호텔과 복합 시설에서 대량의 주방 장비를 흡수하는 다년간의 조달 주기와 집중적인 설치 프로그램을 형성하고 있습니다. 아프리카 수요 기반은 여전히 고르지 않지만, 주요 거점에서는 지역 진출을 뒷받침하는 유통 인프라가 구축되고 있습니다. EMEA 전역의 상업용 주방 장비 시장에서 공급업체 선택의 핵심은 지속가능성, 규정 준수, 수명주기 동안의 유지보수성이며, 이는 앞으로도 장비 교체 시기 및 제품 구성 선택에 영향을 미칠 것입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The commercial kitchen appliances market size was valued at USD 49.07 billion in 2025 and is estimated to grow from USD 52.76 billion in 2026 to reach USD 71.49 billion by 2031, at a CAGR of 6.26% during the forecast period (2026-2031).

Operators continue to replace legacy setups with multifunctional, connected appliances that reduce space, lower energy costs, and sync with centralized order and service platforms, which is shifting capital allocation away from single-function equipment. Expansion programs by leading quick-service chains remain a strong demand anchor as chains scale standardized, IoT-ready back-of-house systems that raise throughput and compress labor per transaction. In parallel, the fastest-growing application segment is cloud and ghost kitchens, which are on track for a 10.32% CAGR through 2031 as delivery-first formats favor compact, high-throughput cooking, holding, and refrigeration platforms. Distribution models are also evolving as large chains shift to direct procurement to secure volume pricing and bundled lifecycle services, supporting higher resilience to regulatory and supply changes.

Global Commercial Kitchen Appliances Market Trends and Insights

QSR Chains and Out-of-Home Dining are Expanding

Large quick-service companies are executing aggressive new-unit builds and remodels that sustain commercial kitchen purchasing across cooking, refrigeration, and warewashing categories. McDonald's lifted capital expenditures and outlined plans consistent with the opening of around 2,200 restaurants in 2025, supported by a USD 3.0-3.2 billion capex range and a multi-year goal of scaling to 50,000 locations by 2027, which directly raises demand for standardized, high-throughput equipment in both mature and developing markets. Yum! Brands reported USD 10 billion in digital sales for Q3 2025 with a 60% digital mix, while achieving a quarterly record of 1,131 gross new units in the period, creating procurement momentum for connected fryers, ovens, and KDS-integrated platforms. Connectivity and automation now command a premium as operators seek faster throughput and lower labor per transaction, and as multi-country chains require uniform outcomes across a broad store base. In India and across the Asia-Pacific, rising urban incomes and dense catchment areas enable QSR formats to scale unit counts quickly, which anchors multi-year equipment replacement cycles within the commercial kitchen appliances market. As menus localize and digital order flows remain elevated, equipment specifications prioritize consistency, rapid recovery times, and remote diagnostics that reduce service downtimes, reinforcing platform choices that operators carry into successive waves of openings.

Hospitality Sector Is Witnessing a Construction Boom

Hospitality capital expenditure continues to create multi-year equipment demand as hotels, resorts, and serviced apartments build kitchens suited to varied guest and event needs. Project flows in the Middle East, including Saudi Arabia's Diriyah development, remain significant and translate into large, staged procurement schedules for ovens, refrigerators, and high-capacity dishwashers across several years to match construction phasing. Extended-stay properties allocate proportionally higher spend on kitchenettes and communal prep spaces, increasing demand for undercounter refrigeration, compact induction hobs, and efficient warewashing. In India, new and upgraded hotel properties tied to domestic tourism and business travel continue to specify energy-saving appliances with verified performance metrics, aligning with procurement frameworks that favor long-life equipment with ready access to parts and service. For multi-property groups, centralized purchasing and template kitchen designs compress unit costs and tighten installation schedules, which benefits vendors able to deliver compliance documentation and commissioning support at scale. As inflation and financing conditions remain tight, operators prioritize equipment choices with clear utility and maintenance savings, maintaining a steady preference for ENERGY STAR-qualified models that demonstrate measurable paybacks.

SMEs Grapple with High Upfront Capex

Capital access and cost inflation remain structural constraints for small and midsize operators that cannot negotiate enterprise-level discounts or favorable lending terms. Survey data in Canada indicate that 69% of SMEs identify equipment costs as a deterrent to capital investment, 50% cite cash-flow constraints, and 47% point to high borrowing costs, while 65% continue to manage pandemic-related debt that averages USD 108,000, which crowds out new-equipment budgets. Higher funding thresholds and stricter underwriting standards elevate the hurdle for energy-efficient or IoT-enabled equipment purchases that offer clear paybacks but require upfront cash. Independent restaurants and cloud-kitchen start-ups in India face similar budget balancing as equipment needs expand beyond basic cooking to include refrigeration, warewashing, and temperature-logging hardware that satisfies food-safety practices. As a result, operators often phase equipment upgrades based on criticality and return horizon, which elongates replacement cycles. Over time, financing innovations and vendor service bundles that reduce upfront payments can improve adoption within the commercial kitchen appliances market.

Other drivers and restraints analyzed in the detailed report include:

- Kitchens are Becoming Energy-Efficient And Iot-Enabled

- Cloud And Ghost Kitchens are on the Rise

- Navigating Complex Safety and Fire Certifications Proves Challenging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerators led the type mix with 34.36% market share in 2025, reflecting the sustained replacement needs for walk-ins, reach-ins, and undercounter units in longstanding foodservice operations. Cooking appliances are forecast to advance at 8.24% CAGR through 2031 on the strength of high-efficiency fryers, griddles, and combi platforms that concentrate multi-function capability within smaller footprints. Verified efficiency remains central to procurement, as equipment like commercial steam cookers and dishwashers delivers measurable annual energy and water savings that improve site-level economics. Induction and advanced ovens are prioritized where electrification agendas and building codes steer new projects toward all-electric back-of-house configurations, an approach that is gaining traction in dense Indian metros that prioritize air quality and safety. Product ecosystems built around sensors and cloud connectivity also help multi-unit operators monitor temperature profiles, cycle counts, and service intervals, tightening compliance and uptime across fleets within the commercial kitchen appliances market.

Product choice is increasingly context-specific, with bakery, catering, QSR, and institutional kitchens placing different weights on throughput, consistency, and maintenance access. High-speed oven variants that combine microwave and impingement technologies support delivery surges, while robust convection units remain staples for batch processes. ENERGY STAR-qualified dishwashers reduce both energy and water, which is relevant for facilities in water-stressed regions where tariff structures penalize usage spikes. Over the forecast period, cooking appliances are positioned to capture a rising share of the commercial kitchen appliances market as integrated controls shorten training time and improve repeatability. In India, chains that balance dine-in and delivery channels increasingly standardize on compatible refrigeration and hot-side packages so parts, training, and service procedures remain common across formats in the commercial kitchen appliances industry.

The Commercial Kitchen Appliances Market Report is Segmented by Type (Refrigerators, Cooking Appliances, Cooktops & Cooking Ranges, and More), Application (QSR, FSR, Cloud/Ghost Kitchens, and More), Distribution Channel (Direct From the Manufacturers and Dealers/Distributors), and Geography (North America, South America, Asia-Pacific, Europe, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 26.38% of global revenue in 2025, reflecting the region's strong base of multi-unit restaurant systems and broad adoption of connected, energy-efficient equipment. Policy drivers will continue to influence purchasing patterns through 2026, as the U.S. AIM Act limits high-GWP refrigerants and mandates stricter leak detection and repair protocols for large-charge systems, which increases replacement activity in foodservice cold rooms and walk-ins. In Canada, small and midsize enterprises report ongoing capital constraints and pandemic-era debt burdens that reduce appetite for large upfront purchases, which keeps interest in financing and service-led models elevated. The region's regulatory frameworks and food-safety codes also reinforce the adoption of equipment with verified performance and logging features. Over the medium term, these factors sustain a steady base of replacements and upgrades within the commercial kitchen appliances market.

Asia-Pacific is the fastest-growing region with a projected 6.87% CAGR through 2031 as urbanization, rising incomes, and expanding QSR and delivery-first formats deepen equipment demand across China, India, and Southeast Asia. Expansion by global chains has been robust, with Yum! Brands reporting thousands of net new units globally, many in Asia-Pacific, alongside rising digital order volumes that require throughput-focused equipment. In India, growth in Tier-2 and Tier-3 cities is elevating demand for standardized hot-side packages and reliable cold storage with temperature logging to meet food-safety practices. Equipment selection also reflects local codes and electrification trajectories, with induction gaining exposure in urban kitchens that benefit from faster installs and consistent heat control. These trends underpin increasing equipment penetration per site and steadier replacement cycles across the commercial kitchen appliances market.

Europe, the Middle East, and Africa show mixed momentum, with European operators adapting to energy costs and updated F-gas rules that push toward natural refrigerants in new and retrofit systems. The shift to CO2 and hydrocarbon solutions is now well established in European retail refrigeration, and hospitality operators are drawing on those learnings for foodservice cold rooms and reach-ins. In the Middle East, mega-developments such as Saudi Arabia's Diriyah project are shaping multi-year procurement cycles and concentrated installation programs that absorb large volumes of kitchen equipment across hotels and mixed-use venues. Africa's demand base remains uneven, though key hubs are developing distribution infrastructure that supports regional rollouts. Across EMEA, sustainability, compliance, and lifecycle serviceability remain central to supplier selection in the commercial kitchen appliances market and will continue to drive replacement timing and product mix choices.

- Ali Group

- Electrolux Professional

- Middleby Corporation

- Hoshizaki Corporation

- Welbilt (Manitowoc)

- Carrier Commercial Refrigeration

- Rational AG

- Meiko International

- Duke Manufacturing Co.

- Vulcan

- Hobart

- Hamilton Beach Commercial

- Alto-Shaam

- True Manufacturing

- Turbo Air

- Southbend

- Fagor Group

- Falcon Foodservice Equipment

- Interlevin Refrigeration Ltd

- The Vollrath Company

- Panasonic Commercial

- Garland (Welbilt)

- Blodgett

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of QSR chains & out-of-home dining

- 4.2.2 Hospitality construction boom

- 4.2.3 Energy-efficient & IoT-enabled kitchens

- 4.2.4 Rise of cloud/ghost kitchens

- 4.2.5 Natural-refrigerant retrofits

- 4.2.6 Demand for multi-function compact units

- 4.3 Market Restraints

- 4.3.1 Smes Grapple with High Upfront CAPEX

- 4.3.2 Navigating Complex Safety and Fire Certifications Proves Challenging

- 4.3.3 Shortages Plague the Electronics Supply Chain

- 4.3.4 Energy Prices Experience Notable Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Refrigerators

- 5.1.1.1 Walk-in

- 5.1.1.2 Reach-in

- 5.1.1.3 Undercounter & Prep-table

- 5.1.2 Cooking Appliances

- 5.1.2.1 Fryers

- 5.1.2.2 Griddles & Charbroilers

- 5.1.2.3 Steamers

- 5.1.3 Cooktops & Cooking Ranges

- 5.1.3.1 Gas

- 5.1.3.2 Electric

- 5.1.3.3 Induction

- 5.1.4 Ovens

- 5.1.4.1 Convection

- 5.1.4.2 Combi

- 5.1.4.3 High-speed

- 5.1.5 Dishwashers

- 5.1.5.1 Undercounter

- 5.1.5.2 Conveyor

- 5.1.6 Heated Holding & Banquet Equipment

- 5.1.7 Food-Preparation Equipment

- 5.1.8 Smart Connected Equipment

- 5.1.1 Refrigerators

- 5.2 By Application

- 5.2.1 Quick-Service Restaurants (QSR)

- 5.2.2 Full-Service Restaurants (FSR)

- 5.2.3 Cloud / Ghost Kitchens

- 5.2.4 Institutional Canteens

- 5.2.5 Resorts & Hotels

- 5.2.6 Hospitals & Healthcare

- 5.2.7 Railway Dining

- 5.2.8 Catering Services

- 5.3 By Distribution Channel

- 5.3.1 Direct from the Manufacturers

- 5.3.2 Dealers/Distributors

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Ali Group

- 6.4.2 Electrolux Professional

- 6.4.3 Middleby Corporation

- 6.4.4 Hoshizaki Corporation

- 6.4.5 Welbilt (Manitowoc)

- 6.4.6 Carrier Commercial Refrigeration

- 6.4.7 Rational AG

- 6.4.8 Meiko International

- 6.4.9 Duke Manufacturing Co.

- 6.4.10 Vulcan

- 6.4.11 Hobart

- 6.4.12 Hamilton Beach Commercial

- 6.4.13 Alto-Shaam

- 6.4.14 True Manufacturing

- 6.4.15 Turbo Air

- 6.4.16 Southbend

- 6.4.17 Fagor Group

- 6.4.18 Falcon Foodservice Equipment

- 6.4.19 Interlevin Refrigeration Ltd

- 6.4.20 The Vollrath Company

- 6.4.21 Panasonic Commercial

- 6.4.22 Garland (Welbilt)

- 6.4.23 Blodgett

7 Market Opportunities & Future Outlook

- 7.1 Rapid expansion of quick-service restaurants (QSRs)