|

시장보고서

상품코드

2044204

모다크릴 섬유 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Modacrylic Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

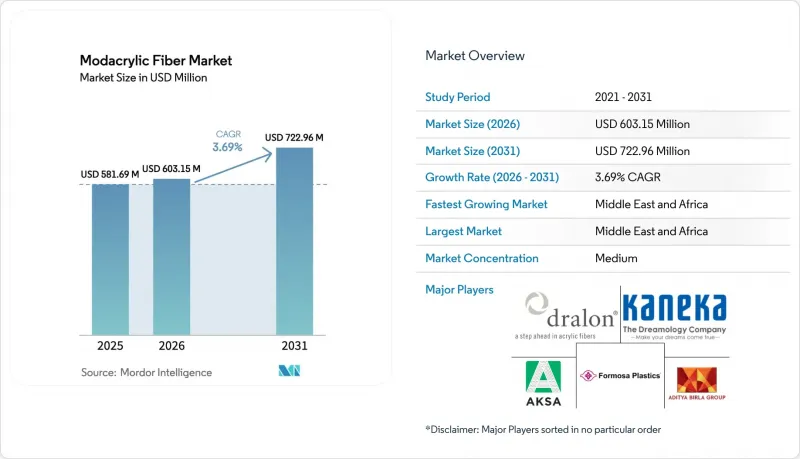

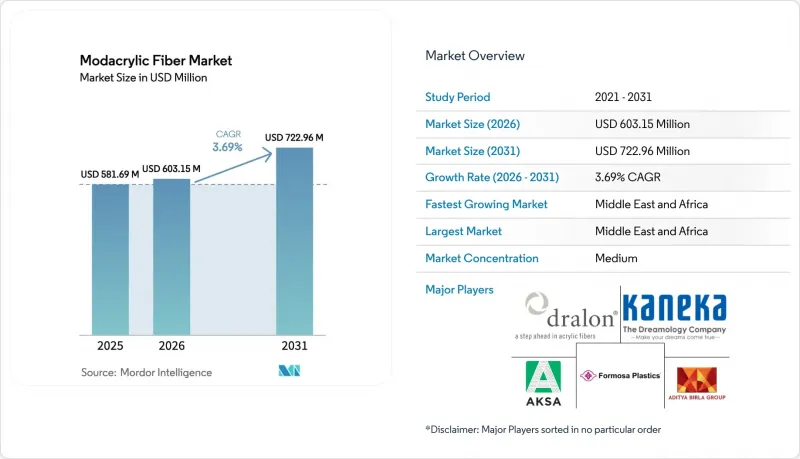

모다크릴 섬유 시장 규모는 2025년 5억 8,169만 달러에서 2026년에는 6억 315만 달러로 확대되어 2026년부터 2031년까지 CAGR 3.69%로 성장을 지속하여, 2031년에는 7억 2,296만 달러에 이를 것으로 예측됩니다.

사하라 사막 이남 아프리카의 소비자층 확대와 더불어 높은 스타일링 온도에 견딜 수 있는 내열성 합성 익스텐션에 대한 중동 수요가 모발 섬유 수요의 급격한 증가를 견인하고 있습니다. 영국과 북미에서는 강화된 화재 방지 규정으로 인해 보호복과 실내 장식에 대한 수요가 증가하고 있습니다. 폐쇄 루프 방식의 아크릴로니트릴 회수를 활용하는 공급업체는 미국 환경보호청(EPA)의 유해물질 규제법(TSCA) 관련 컴플라이언스 비용으로부터 수익률을 효과적으로 보호할 수 있습니다. 공급 구조는 중간 정도의 집중도를 보이고 있으며, 상위 4개 생산업체가 세계 생산능력의 대부분을 차지하고 있지만, 소규모 혁신기업들도 에너지 효율이 높은 습식방적 기술과 저탄소 원료를 활용하여 경쟁력을 유지하고 있습니다. 2026년부터 2031년까지의 예측 기간은 특히 전기자동차의 방음재와 리튬 이온 배터리용 단열재에 있어 유망한 시장 전망을 보여주고 있습니다. 그러나 모다크릴이 이러한 기회를 활용하기 위해서는 먼저 폴리에스터, 아라미드 등 업계 주력 소재와 원가 경쟁력을 갖춰야 합니다.

세계 모다크릴 섬유 시장 동향과 인사이트

가구의 방화 규제 강화에 따라 가구 제조업체들이 난연성 소재로 전환

2025년 영국은 국내 가구 규정을 개정하여 할로겐계 첨가제에서 본질적으로 난연성이 있는 모다크릴 파일로 전환을 추진했습니다. 매사추세츠 주정부가 유기 할로겐계 및 유기 인계 난연제를 금지함에 따라 북미의 가구 제조업체들은 무할로겐 대체 소재로 전환하고 있습니다. 2024년, 유럽화학물질청(ECHA)은 고위험물질(SVHC) 목록에 난연제를 추가하여 첨가제 선택권을 더욱 제한하고, 모다크릴에 대한 규제적 강조를 강화했습니다. 그러나 모다크릴의 보급에는 가공된 폴리에스테르에 비해 가격이 비싸다는 문제가 있습니다. 공급업체들은 혁신을 통해 추가 마감 처리 없이 NFPA 260 클래스 I 기준을 충족하는 400 gsm 미만의 경량 더미를 개발하여 비용 대비 성능의 격차를 해소하고 가구 OEM 제조업체의 지지를 얻을 수 있는 체제를 갖추고 있습니다.

생산 시 독성을 감소시키는 저시아노계 바이오 유래 아크릴로니트릴 제조법 등장

Trillium Renewables와 NREL의 파일럿 플랜트는 글리세롤과 3-하이드록시프로피온산을 아크릴로니트릴로 전환하는 데 앞장서고 있습니다. 이 혁신적인 접근 방식은 프로파일렌의 탈산화에 흔히 발생하는 시안화물의 부산물을 피하고 온실 가스 배출을 줄일 수 있는 혁신적인 방법입니다. 미국 환경보호청(EPA)이 2024년 아크릴로니트릴을 최우선 과제로 지정함에 따라, 업계 관계자들은 규제 준수 비용을 줄이기 위해 이러한 바이오 유래 제조 경로를 열심히 모색하고 있습니다. 현재 수율은 아직 경제적인 임계치에 도달하지 못했지만, 기존 습식 방적 라인 근처에 모듈식으로 건설할 수 있는 가능성은 촉매 기술의 발전과 함께 설비 투자를 줄일 수 있는 기회를 가져다 줄 것입니다. 조기 도입 기업은 잔류 단량체 농도 감소의 이점을 누릴 수 있으며, REACH 인증 획득을 위한 경로가 원활해지고, 의류 브랜드에 대한 제한 물질에 대한 감사가 빨라질 수 있습니다.

PPE 분야에서 자체 난연성 비스코스 혼방 소재와 경쟁하는 PPE 분야

석유, 가스 및 유틸리티 부문에서 산업용 작업복 구매자는 점점 더 많은 비스코스-아라미드 혼방사를 선택하고 있습니다. 이 혼방사는 NFPA 2112 표준을 충족할 뿐만 아니라 원단 비용도 절감할 수 있습니다. TenCate는 Tecasafe Plus를 지정된 무게로 판매하고 있지만, 인 강화 비스코스 원사를 사용하여 현재 유사한 한계 산소 지수(LOI) 값을 달성할 수 있다는 점을 강조하는 것이 중요합니다. 이 강화 원사는 내구성이 뛰어나며, 산업용 세탁 사이클을 여러 번 반복해도 견딜 수 있습니다. 이에 대한 전략적 대응으로 모다크릴 공급업체들은 고데니어, 고강도 폴리아미드와 세번수 원사를 혼방하여 사용하고 있습니다. 이 개선은 인열 강도와 내마모성을 향상시켜 고급 의류 시장에서의 입지를 유지하기 위한 것입니다. 그러나 저가형 범용 커버올 시장에서는 비스코스계 대체 소재에 점유율을 내주고 있습니다.

부문 분석

2025년, 모발 섬유는 총 매출액의 54.22%를 차지할 것으로 예상되며, 2026년부터 2031년까지 예측 기간 동안 CAGR 6.15%를 나타낼 것으로 예측됩니다. 이러한 급격한 성장은 주로 아프리카 전역의 전자상거래 플랫폼에 생생한 내열성 브레이드 제품을 적극적으로 공급하고 있는 카네카 말레이시아 지사가 주도하고 있습니다. 매출 경쟁에서 방호복은 중요한 위치를 차지하고 있으며, 북미 정유시설와 유럽 유틸리티에서 시행되는 엄격한 NFPA 및 ISO 표준의 혜택을 누리고 있습니다. 그러나 그 성장에는 특히 가성비가 뛰어난 비스코스-아라미드 혼방 소재와의 경쟁으로 인한 어려움이 있습니다.

실내 장식 및 가정용품 부문의 성장은 여전히 완만하게 성장하고 있으며, 이는 주로 영국과 매사추세츠 주에서 첨가형 난연제를 금지하는 규제의 영향을 받고 있습니다. 이러한 규제 움직임에 따라 가구 OEM 업체들은 천연 난연성을 갖춘 모다크릴 파일로 전환하고 있습니다. 그러나 가공된 폴리에스테르에 비해 모다크릴은 가격 프리미엄이 있기 때문에 채택률이 둔화되고 있습니다. 산업용 직물과 모다크릴 파일은 매출의 큰 비중을 차지하고 있으며, 자동차 헤드라이너와 상업용 시트가 주요 틈새 시장으로 부상하고 있습니다. 또한, 전기자동차(EV)용 흡음펠트 및 배터리용 방염패드에서 초기 모멘텀을 보이며 잠재적인 성장 기회를 시사하고 있습니다. Aksa가 Armora 라인을 확장하기로 결정한 것은 다중 위험 대응 의류 및 산업용 직물, 특히 난연성과 내마모성을 겸비한 제품에 대한 업계의 신뢰를 보여줍니다.

지역별 분석

2025년 중동 및 아프리카은 고품질 합성모섬유에 대한 강한 수요에 힘입어 2026년부터 2031년까지 예측 기간 동안 CAGR 6.49%를 기록하며 전 세계 매출의 45.67%를 차지할 것으로 예측됩니다. 나이지리아, 남아프리카공화국, 케냐 등 주요 국가에서는 분산된 오프라인 매장에서 온라인 소매로의 전환이 진행되고 있습니다. 고온 환경에 직면한 걸프만 석유 수출국에서는 난연성 작업복의 채택이 확대되고 있으며, 그 편안함 때문에 모다크릴 혼방 소재가 선호되고 있습니다.

일본의 전문 공급업체와 중국의 탄탄한 아크릴 가치사슬에 힘입어 아시아태평양이 중요한 기여 지역으로 부상하고 있습니다. 중국에서는 장쑤성과 저장성의 생산기지가 자동화에 대한 투자를 진행하고 있으며, 이는 인건비 및 용제 회수 비용의 대폭적인 절감으로 이어지고 있습니다. 일본 도레이는 2026 회계연도 섬유 및 직물 부문에서 전년 대비 매출 증가를 보고하고 있으며, 고수익성 특수재종에 대한 지역적 수요 회복을 강조하고 있습니다. 향후 인도가 합성섬유의 보급률 향상을 목표로 하고 있어 범용 의류용 원사 수요가 둔화되는 가운데, 보호복 수요 증가를 견인할 것으로 예측됩니다.

북미와 유럽은 가구 수요와 개인보호장비(PPE) 관련 규제를 배경으로 한 자릿수 초중반의 성장세를 보이고 있습니다. 영국에서는 가연성 감소 의무와 캘리포니아 주 TB 117-2013 표준 준수에 영향을 받아 국내 가구용 실내장식재 제조업체들이 무할로겐 솔루션으로 전환하도록 촉구하고 있습니다. 의류 브랜드도 Scope 3의 목표를 더욱 엄격하게 적용하고 있으며, 매스밸런스 인증 또는 재생가능 전력 인증을 받은 모다크릴을 제공하는 방적업체를 선호하는 경향이 있습니다. 남미에서는 전체 소비량은 적지만, 브라질 자동차 업계는 주로 유럽 수출용 모델에 모다크릴 헤드라이너를 채택하고 있습니다. 유럽에서는 내장재에 대한 내화시험 규정이 엄격하기 때문입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Modacrylic Fiber Market size is expected to grow from USD 581.69 million in 2025 to USD 603.15 million in 2026 and is forecast to reach USD 722.96 million by 2031 at 3.69% CAGR over 2026-2031.

Sub-Saharan Africa's expanding consumer base, coupled with the Middle-East's demand for heat-stable synthetic extensions that endure high styling temperatures, is fueling the surge in hair fiber demand. In the U.K. and North America, stricter fire codes are amplifying the need for protective apparel and upholstery. Suppliers harnessing closed-loop acrylonitrile recovery are effectively shielding their margins from the compliance costs tied to the U.S. EPA's Toxic Substances Control Act. The supply landscape reveals a moderate concentration: the top four producers dominate a substantial share of global capacity, yet smaller innovators are maintaining competitiveness with energy-efficient wet-spinning techniques and low-carbon feedstocks. The forecast period of 2026-2031 presents a promising horizon for the market, particularly in the electric-vehicle acoustic insulation and thermal barriers for lithium-ion batteries. However, for modacrylic to capitalize on these opportunities, it must first align its costs with industry stalwarts such as polyester and aramid.

Global Modacrylic Fiber Market Trends and Insights

Shift of Upholstery Makers toward Low-Flammability Materials for Stricter Furniture Fire Codes

In 2025, the United Kingdom shifted its domestic furniture regulations, moving from halogenated additives to the inherently flame-resistant modacrylic pile. Massachusetts followed suit, banning organohalogen and organophosphorus retardants, steering North American upholstery makers towards halogen-free alternatives. In 2024, the European Chemicals Agency (ECHA) expanded its list of substances of very high concern (SVHC) to include more flame retardants, further limiting additive choices and reinforcing the regulatory emphasis on modacrylic. However, the uptake of modacrylic faces challenges due to its premium pricing over treated polyester. Suppliers are innovating, creating lighter piles under 400 gsm that achieve NFPA 260 Class I compliance without added finishes, positioning themselves to bridge the cost-performance gap and win favor with furniture OEMs.

Emergence of Low-Cyano Bio-Based Acrylonitrile Routes Cutting Production Toxicity

Trillium Renewables and NREL's pilot plants are at the forefront, converting glycerol and 3-hydroxypropionic acid into acrylonitrile. This innovative approach avoids the cyanide by-products common in propylene ammoxidation and promises a reduction in greenhouse gas emissions. With the EPA flagging acrylonitrile as a high-priority concern in 2024, industry players are keenly exploring these bio-routes to cut compliance costs. Although current yields do not yet meet economic thresholds, the potential for modular construction near existing wet-spinning lines presents an opportunity to lower capital expenditures as catalyst technology progresses. Early adopters can benefit from reduced residual monomer levels, easing the path to REACH authorizations and speeding up audits for apparel brands concerning restricted substances.

Competition from Inherently Flame-Retardant Viscose Blends in PPE

In the oil, gas, and utilities sectors, buyers of industrial workwear are increasingly opting for viscose-aramid blends. These blends not only meet NFPA 2112 standards but also come at a reduced fabric cost. While TenCate markets its Tecasafe Plus at a designated weight, it is important to highlight that similar Limiting Oxygen Index (LOI) values can now be achieved using phosphorus-enhanced viscose yarns. These enhanced yarns are durable, withstanding multiple industrial wash cycles. In a strategic response, modacrylic suppliers are co-spinning finer denier with high-tenacity polyamide. This enhancement aims to elevate tear strength and abrasion resistance, ensuring their continued presence in premium garments. However, they are yielding the low-cost commodity coveralls market to viscose alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Modacrylic Acoustic Insulation in Electric-Vehicle Interiors

- Rising Use of Modacrylic Felts in Li-Ion Battery Fire-Safety Separators

- High Energy Intensity of Wet-Spinning Raises Scope-3 Emissions Scores

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hair fiber accounted for 54.22% of total revenue, charting a course with a 6.15% CAGR through the forecast period of 2026-2031. This surge is primarily fueled by Kaneka's Malaysian hub, which is actively supplying vibrant, heat-stable braids to e-commerce platforms across Africa. In the revenue race, protective apparel takes a significant spot, reaping benefits from the stringent NFPA and ISO standards enforced in refineries across North-America and utilities in Europe. However, its growth faces challenges, notably from competition with more budget-friendly viscose-aramid blends.

Growth in the upholstery and household sector remains modest, largely influenced by regulations in the United Kingdom and Massachusetts that ban additive flame retardants. This regulatory push is steering furniture OEMs toward adopting a naturally flame-retardant modacrylic pile. However, the adoption rate is slowed by the modacrylic's price premium compared to treated polyester. Industrial fabric and the modacrylic pile represent a significant share of the revenue, with automotive headliners and contract seating emerging as key niches. Additionally, there is early momentum in electric vehicle (EV) acoustic felts and battery fire-safety pads, signaling potential growth opportunities. Aksa's decision to expand its Armora line highlights industry confidence in multi-hazard garments and industrial fabrics, particularly those combining flame resistance with abrasion durability.

The Modacrylic Fiber Market Report is Segmented by Application (Protective Apparel, Hair Fiber, Industrial Fabric, Modacrylic Pile, Upholstery and Household, and Other Applications) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Middle-East and Africa accounted for 45.67% of global revenue, driven by a strong demand for premium synthetic hair fiber and a projected CAGR of 6.49% through the forecast period of 2026-2031. Key players, including Nigeria, South Africa, and Kenya, are transitioning from fragmented brick-and-mortar outlets to online retail. Gulf oil exporters, facing high ambient heat, are increasingly adopting flame-resistant workwear, with a preference for modacrylic blends due to their comfort.

The Asia-Pacific region, supported by specialty suppliers in Japan and a robust acrylic value chain in China, emerges as a significant contributor. In China, capacity clusters in Jiangsu and Zhejiang are investing in automation, leading to significant reductions in labor and solvent-recovery costs. Japan's Toray, reporting a year-over-year revenue increase in fibers and textiles for FY 2026, highlights a regional resurgence in demand for higher-margin specialty grades. Looking forward, India's goal to boost man-made fiber penetration is set to drive a rise in protective apparel, even as commodity apparel yarns face a slowdown.

North America and Europe are seeing growth in the low-to-mid single digits, driven by furniture demand and PPE regulations. The U.K. is steering its domestic upholstery producers towards halogen-free solutions, influenced by a mandate for lower ignition propensity and California's TB 117-2013 harmonization. Apparel brands are also tightening their Scope-3 targets, showing a preference for mills that provide mass-balance or renewable-electricity certified modacrylic. In South America, while overall consumption is modest, Brazil's automotive sector is adopting modacrylic headliners, mainly for export models heading to Europe, where fire-testing regulations for interior materials are stringent.

- Aditya Birla Management Corporation Pvt. Ltd

- Aksa Akrilik Kimya Sanayi AS

- China Petrochemical Corporation

- CNPC

- Dralon

- FCFA

- Formosa Plastics Corporation

- Fushun Huifu Fire Resistant Fibre Co. Ltd

- Fushun Rayva Fiber Co. Ltd

- Grupo Kaltex SA de CV

- Japan Industrial Co. Ltd

- Jiangsu Jinmao International E-Commerce Co. Ltd

- Kaneka Corporation

- Pasupati Acrylon Ltd

- TenCate Protective Fabrics

- Tianjin GT New Material Technology Co. Ltd

- Toray Industries Inc.

- Zhangjiagang Hengfeng Textile Co. Ltd

- Zhejiang Wangzhuo Knitting Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Widening adoption of synthetic hair extensions and wigs

- 4.1.2 Shift of upholstery makers toward low-flammability materials for stricter furniture fire codes

- 4.1.3 Emergence of low-cyano bio-based acrylonitrile routes cutting production toxicity

- 4.1.4 Expansion of modacrylic acoustic insulation in electric-vehicle interiors

- 4.1.5 Rising use of modacrylic felts in Li-ion battery fire-safety separators

- 4.2 Market Restraints

- 4.2.1 Stringent EPA/REACH limits on residual acrylonitrile monomers

- 4.2.2 Competition from inherently flame-retardant viscose blends in PPE

- 4.2.3 High energy intensity of wet-spinning raises Scope-3 emissions scores

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Protective Apparel

- 5.1.2 Hair Fiber

- 5.1.3 Industrial Fabric

- 5.1.4 Modacrylic Pile

- 5.1.5 Upholstery and Household

- 5.1.6 Other Applications

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Aditya Birla Management Corporation Pvt. Ltd

- 6.4.2 Aksa Akrilik Kimya Sanayi AS

- 6.4.3 China Petrochemical Corporation

- 6.4.4 CNPC

- 6.4.5 Dralon

- 6.4.6 FCFA

- 6.4.7 Formosa Plastics Corporation

- 6.4.8 Fushun Huifu Fire Resistant Fibre Co. Ltd

- 6.4.9 Fushun Rayva Fiber Co. Ltd

- 6.4.10 Grupo Kaltex SA de CV

- 6.4.11 Japan Industrial Co. Ltd

- 6.4.12 Jiangsu Jinmao International E-Commerce Co. Ltd

- 6.4.13 Kaneka Corporation

- 6.4.14 Pasupati Acrylon Ltd

- 6.4.15 TenCate Protective Fabrics

- 6.4.16 Tianjin GT New Material Technology Co. Ltd

- 6.4.17 Toray Industries Inc.

- 6.4.18 Zhangjiagang Hengfeng Textile Co. Ltd

- 6.4.19 Zhejiang Wangzhuo Knitting Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment