|

시장보고서

상품코드

2044206

자동차용 흡음재 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Acoustic Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

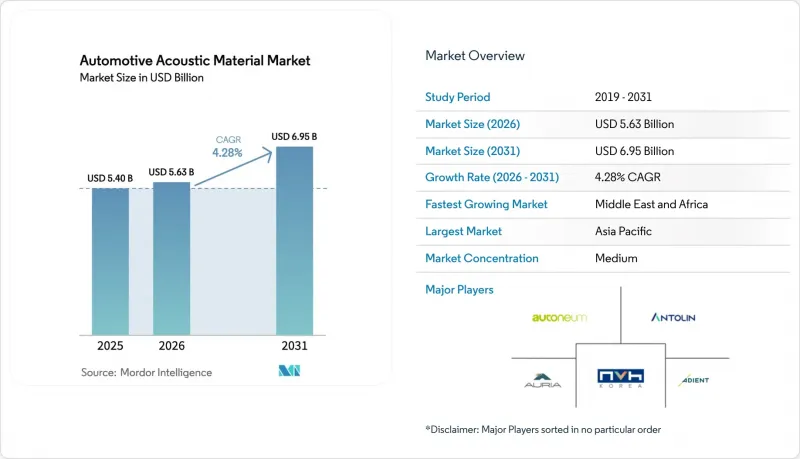

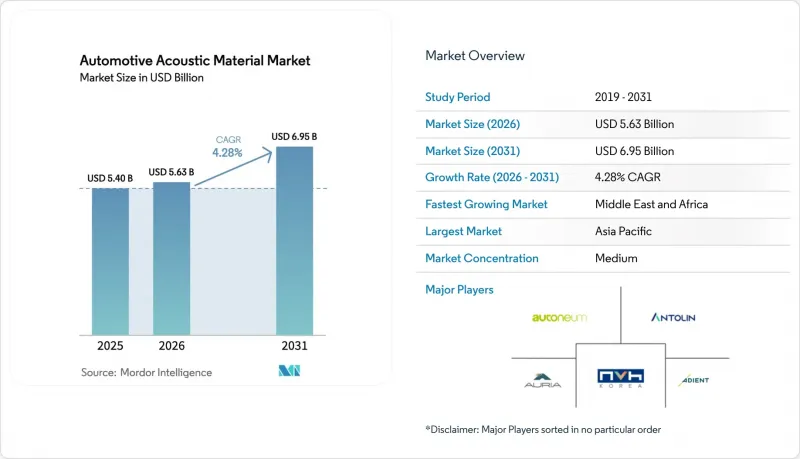

자동차용 흡음재 시장 규모는 2025년 54억 달러에서 2026년에는 56억 3,000만 달러로 확대되어 2031년까지 69억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026년부터 2031년) CAGR은 4.28%를 나타낼 전망입니다.

전기자동차(EV) 생산 증가, 차량 내 소음 규제 강화, 경량화 및 다기능 복합소재에 대한 수요 증가가 이러한 꾸준한 성장을 뒷받침하고 있습니다. OEM 업체들은 엄격한 차내 소음 기준을 충족시키면서 스케이트보드형 EV 플랫폼의 공간을 확보하기 위해 단열 및 방음 기능을 단층 패키지에 통합하는 데 주력하고 있습니다. 폴리우레탄은 검증된 제진 성능으로 여전히 선도적인 위치를 유지하고 있지만, 재활용 규제가 강화되면서 폴리프로필렌에 대한 수요도 증가하고 있습니다. 지역별 성장세는 아시아태평양이 중심이지만, 중동 및 아프리카는 새로운 조립 공장의 생산 개시와 함께 세계 평균을 상회하는 성장률을 보이고 있습니다. 경쟁의 격화는 재료과학의 발전, 지역 내 사업 기반 확대 및 제품 포트폴리오의 다각화를 위한 전략적 인수로 인해 더욱 심화되고 있습니다.

세계 자동차용 흡음재 시장 동향과 인사이트

EV 및 HEV에 대한 전 세계 차량 내 소음 규제 강화 추세

전기자동차(EV) 및 하이브리드 자동차(HEV) 모델은 현재 EU 규정 540/2014 및 중국 GB 1495-2024 표준에 따라 차량 내 소음 상한선에 직면하고 있으며, 고밀도 폼, 다층 라미네이트 및 정밀하게 조정된 주파수 흡수재에 대한 수요가 급증하고 있습니다. OEM 업체들은 2년 이내에 인증된 재료를 확보해야 하며, 이로 인해 이미 인증을 획득한 공급업체는 가격 협상에서 우위를 점할 수 있습니다. 제품 선정에 있어서는 발밑 공간을 희생하지 않고 인버터의 소음을 차단하는 얇은 두께의 폴리우레탄 복합재에 대한 관심이 높아지고 있습니다. 규제는 현재 애프터마켓에도 영향을 미치고 있으며, 교체용 부품도 순정과 동일한 음향 사양을 충족해야 하기 때문에 잠재적인 총 수요는 확대되고 있습니다. 인증 일정에 맞추어 연구개발 파이프라인을 조정할 수 있는 공급업체는 프리미엄 가격을 책정하고 다년 계약을 체결할 수 있습니다.

OEM의 경량, 다기능 음향-단열 복합소재로의 전환

각 제조업체들은 NVH 댐퍼와 단열재를 단일 패널에 통합하여 기존의 다층 적층 구조에 비해 대폭적인 경량화를 실현하고 있습니다. 폴리프로필렌이 풍부한 매트릭스가 선호되는 이유는 유럽의 '순환 경제 행동 계획'에서 정한 재활용 가능성 기준을 충족하기 때문입니다. 이러한 변화로 인해 화학업체와 첨단 접착라인을 보유한 Tier 1 컨버터와의 전략적 제휴가 가속화되고 있습니다. 이러한 복합소재는 평방미터당 비용이 상당히 높지만, OEM 업체들은 패스너 수 감소, 택트 타임 단축, EV의 항속거리 증가를 통해 비용을 회수하고 있습니다. 컴파운딩과 라미네이팅 설비를 통합한 공급업체는 한 번의 생산 공정에서 엄격한 치수 공차와 이중 특성 목표를 달성함으로써 경쟁 우위를 확보할 수 있습니다.

발포체용 석유화학 원료 공급망의 변동성

폴리우레탄의 주요 전구체인 톨루엔디 이소시아네이트의 가격은 중동의 생산에 영향을 미친 지정학적 긴장으로 인해 2025년에 크게 변동했습니다. 헤지 수단이 없는 중소형 컨버터의 수익률은 크게 축소되었습니다. OEM 업체들은 이중 소싱이나 비용 전가 조항의 협상으로 대응했지만, 이로 인해 조달의 복잡성이 증가했습니다. 바이오 원료 루트는 안정성을 약속하지만 여전히 비용 증가 요인이 되고, 생산 능력에도 한계가 있습니다. 화학 부문을 후방 통합하거나 장기 계약을 맺은 공급업체는 단기적인 충격으로부터 자신을 보호하고 우선 공급업체로서의 지위를 유지하고 있습니다.

부문 분석

폴리우레탄은 신뢰할 수 있는 감쇠 성능, 확립된 공급망, 그리고 광범위한 OEM의 평가로 인해 2025년에도 40.25%의 점유율을 유지하며 시장의 근간을 이루었습니다. 자동차용 흡음재 시장은 특정 주파수 대역에 맞는 고유한 셀 구조를 가능하게 하는 폴리우레탄의 다재다능한 조정 가능성의 혜택을 누리고 있습니다. 그러나 재활용 가능성에 대한 압력과 저밀도화 추구가 폴리프로필렌의 CAGR 6.55%를 견인하고 있으며, 폴리프로필렌은 두드러진 성장의 견인차 역할을 하고 있습니다. 공급업체들은 난연성 기준을 충족시키면서 무게를 크게 줄일 수 있는 PP 고함량 블렌드로 전환을 추진하고 있습니다. 바이오 유래 원료도 등장하고 있지만, 대량 계약에 대응하기 위해서는 규모 확대가 필요하기 때문에 현재로서는 파일럿 단계에 머물러 있습니다.

폴리우레탄 제조업체들은 EU의 REACH 규제 기준을 준수하는 재생 가능한 폴리올 등급과 저 VOC 배합으로 이에 대응하고 있습니다. 폴리우레탄 자동차용 흡음재 시장 규모는 점진적인 혁신의 견고한 기반을 반영하여 더욱 확대될 것으로 예측됩니다. 폴리프로필렌의 부상으로 통합형 석유화학 콤비네이션이 수지 비용을 절감하고 있는 아시아 지역에서는 생산능력 확대가 진행되고 있습니다. 유리 섬유와 특수 섬유는 각각 상용차 및 고급차 인테리어에서 틈새 역할을 하며 비용, 무게, 미학의 균형을 맞추고 있습니다.

2025년에는 인테리어 솔루션이 매출의 53.18%를 차지할 것으로 예상되며, 승객의 편안함과 규정 준수에 대한 오랜 노력의 결실을 맺게 될 것입니다. 도어 패널, 바닥 카펫, 대시보드용 단열재는 안정적인 대량 생산 프로그램을 형성하여 공급업체의 현금 흐름을 지원하고 있습니다. 자동차용 흡음재 시장은 디자인 측면에서도 기능하는 복합 펠트를 통해 인테리어 트림의 혁신을 지속하고 있으며, 이를 통해 조립이 용이하고 품질감이 향상되고 있습니다. 그러나 EV의 공기역학적 성능과 풍절음 규제를 배경으로 외장 부문은 CAGR 7.58%로 더 빠르게 성장하고 있습니다.

언더바디 쉴드, 휠 아치 라이너, A필러 트림은 폴리프로필렌과 열성형 PET 블렌드를 사용하여 돌의 충격에 견디고 광대역 소음을 줄여줍니다. 외장 부품에 할당된 자동차용 흡음재 시장 규모는 2031년까지 크게 확대될 것으로 예측됩니다. 통합형 공기역학 및 흡음 모듈은 항력을 줄이고 소용돌이 발생으로 인한 소음을 억제하여 하나의 어셈블리로 OEM의 항속거리 및 차량 내 정숙성 목표 달성에 기여합니다. 각 공급업체들은 열 순환과 도로용 염분에 노출되어도 음향 특성이 저하되지 않고 장기적인 내구성을 보장할 수 있는 내후성 복합재료를 개발하고 있습니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 38.16%를 차지했습니다. 이는 중국의 전기차 생산량 1,240만 대와 인도의 확대되는 조립 거점들이 뒷받침하고 있습니다. 현지 음향 부품 공급업체는 적시 납품 목표를 달성하고 지역 기후 조건에 맞게 배합을 조정하기 위해 상하이, 푸네, 울산의 OEM 공장 근처에 거점을 두고 있습니다. 중국의 자동차용 음향재료 시장도 현지 조달 규제의 영향을 받고 있으며, 외자기업들은 생산능력 확대를 위해 합작투자에 나서고 있습니다. 일본의 하이브리드 기술에 대한 전문 지식은 듀얼 모드 배리어 흡수 패널에 대한 수요를 뒷받침하고 있으며, 수출 지향적인 한국 OEM 업체들은 북미 및 유럽 시장을 위해 세계 표준에 부합하는 솔루션을 지정하고 있습니다.

중동 및 아프리카은 아랍에미리트의 산업 발전과 '비전 2030'에 포함된 사우디아라비아의 제조업 지원책에 힘입어 CAGR 5.75%로 가장 빠른 성장세를 보이고 있습니다. 이집트와 모로코에 신설된 CKD(완전조립키트) 공장은 고온 환경에 대응하는 대시보드용 단열재와 도어실링에 대한 현지 수요를 창출하고 있습니다. 남아공은 유럽으로의 수출 루트를 활용하고 있으며, EU의 소음 규제 및 재활용 지침에 부합하는 인증된 재료를 요구하고 있습니다. 인프라의 제약은 여전히 남아 있지만, 풍부한 석유화학 원료가 지역 폼 생산을 뒷받침하고 있어 현지 가공업체들의 원료 가격 변동 위험을 완화하고 있습니다.

유럽의 프리미엄 브랜드는 이 지역을 음향 기술의 최전선에 계속 자리매김하고 있습니다. 독일 OEM 업체들은 NVH(소음, 진동, 유해성)와 지속가능성 기준을 모두 충족하는 초경량 라미네이트를 요구하고 있으며, 공급업체들은 폐쇄형 재활용이 가능한 단일 소재 필름 개발을 추진하고 있습니다. 프랑스와 이탈리아는 순환경제 목표에 부합하는 재생섬유 펠트를 우선시하고 있으며, 영국은 에어로겔 하이브리드 흡음재 연구를 위한 스타트업 기업을 지원하고 있습니다. 북미에서 전기 픽업트럭으로의 전환에 따라 타이어의 굉음을 억제하기 위한 휠 아치 및 차체 제진에 대한 요구가 증가하고 있으며, 이는 미국 공장에 새로운 생산량을 가져오고 있습니다. 지역과 상관없이 자동차용 흡음재 시장에서는 NOx 및 소음 배출을 억제하기 위한 규제 거리의 차이에 대응할 수 있도록 배합을 조정하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The automotive acoustic material market size is expected to increase from USD 5.40 billion in 2025 to USD 5.63 billion in 2026 and reach USD 6.95 billion by 2031, reflecting a 4.28% CAGR during the forecast period (2026 to 2031). Increasing electric vehicle production, intensifying interior noise regulations, and the push for lightweight multifunctional composites underpin this steady advance. OEMs focus on integrating thermal and acoustic functions into single-layer packages to free up space in skateboard EV platforms while meeting stringent cabin-noise limits. Polyurethane retains its lead because of proven damping performance, yet polypropylene gains traction as recycling mandates tighten. Geographic growth remains anchored in Asia-Pacific, but the Middle East and Africa outpace global averages as new assembly plants start production. Competitive intensity is shaped by material science breakthroughs and strategic acquisitions that expand regional footprints and diversify product portfolios.

Global Automotive Acoustic Material Market Trends and Insights

Stringent Global Interior Noise Regulations for EVs and HEVs

Electric and hybrid models now face cabin-noise caps under Regulation (EU) 540/2014 and China's GB 1495-2024 standards, driving an immediate spike in demand for high-density foams, multilayer laminates, and precision-tuned frequency absorbers . OEMs must secure certified materials within a two-year window, creating pricing leverage for suppliers already validated. Product selection increasingly revolves around low-thickness polyurethane composites that block inverter whine without sacrificing foot-well space. Regulations now spill into the aftermarket, compelling replacement parts to match original acoustic specifications, thereby enlarging total addressable demand. Suppliers that align R&D pipelines with certification schedules can command premiums and lock in multiyear contracts.

OEM Shift Toward Lightweight, Multifunctional Acoustic-Thermal Composites

Manufacturers are merging NVH dampers with thermal barriers into single panels that deliver notable mass savings over legacy multilayer stacks. Polypropylene-rich matrices are preferred because they meet recyclability thresholds emerging in Europe's Circular Economy Action Plan. The shift accelerates strategic partnerships between chemical companies and Tier 1 converters that control advanced bonding lines. Although such composites cost significantly more per square meter, OEMs recoup expenses through reduced fastener counts, faster takt times, and improved range in EVs. Suppliers with integrated compounding and laminating assets gain a competitive edge by hitting tight dimensional tolerances and dual-property targets in one production pass.

Supply-Chain Volatility in Petrochemical Feedstocks for Foams

Prices for toluene diisocyanate, a key polyurethane precursor, swung significantly during 2025 because of geopolitical tensions affecting Middle Eastern production. Margins for smaller converters without hedging mechanisms experienced a significant contraction. OEMs responded by dual-sourcing and negotiating pass-through clauses, raising procurement complexity. While bio-feedstock routes promise stability, they remain cost-additive and limited in capacity. Suppliers with backward-integrated chemical lines or long-term contracts insulate themselves from near-term shocks and retain preferred-vendor status.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization Spurring Demand for In-Cabin Comfort in Emerging Asia

- Growing Ride-Sharing and Robo-Taxi Fleets Prioritizing Durable NVH Interiors

- Space Constraints in Skateboard EV Platforms Limiting Insulation Thickness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane remained the anchor at 40.25% share in 2025 because of reliable damping, established supply chains, and broad OEM validation. The automotive acoustic material market benefits from polyurethane's tuning versatility, enabling bespoke cell structures for specific frequency bands. Yet recyclability pressures and the search for lower density drive polypropylene's 6.55% CAGR, positioning it as the standout growth vector. Suppliers pivot to PP-rich blends that trim significant mass while meeting flammability codes. Bio-sourced feedstocks emerge but require scaling to match volume contracts, keeping them in pilot phases for now.

Polyurethane producers respond with renewable polyol grades and low-VOC formulations that align with EU REACH thresholds. The automotive acoustic material market size for polyurethane is set for further expansion, reflecting a solid base for incremental innovation. Polypropylene's rise invites capacity expansions in Asia, where integrated petrochemical complexes cut resin costs. Fiberglass and specialty textiles hold niche roles in commercial and premium interiors, respectively, balancing cost, weight, and aesthetics.

Interior solutions delivered 53.18% revenue in 2025, a testament to long-standing focus on occupant comfort and regulatory compliance. Door panels, floor carpets, and dash insulators form stable, high-volume programs that anchor supplier cash flows. The automotive acoustic material market continues to innovate in interior trims through composite felts that double as design surfaces, easing assembly and enhancing perceived quality. However, the exterior segment grows faster at 7.58% CAGR, propelled by EV aerodynamics and wind-noise management mandates.

Underbody shields, wheel-arch liners, and A-pillar trims leverage polypropylene and thermoformed PET blends that resist stone impact while dampening broadband noise. The automotive acoustic material market size assigned to exterior components is forecast to grow significantly by 2031. Integrated aero-acoustic modules lower drag and suppress vortex-induced noise, feeding OEM range and cabin-quietness targets in one assembly. Suppliers refine weather-stable composites able to survive thermal cycling and road-salt exposure without acoustic drift, locking in long-term durability claims.

The Automotive Acoustic Material Market Report is Segmented by Material Type (Polyurethane, Polypropylene, Polyvinyl Chloride, Fiberglass, and More), Application Area (Interior and Exterior), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), and More), Sales Channel (OEM and Aftermarket), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 38.16% of global revenue in 2025, anchored by China's 12.4 million electric car production count and India's expanding assembly clusters . Local acoustic suppliers co-locate near OEM plants in Shanghai, Pune, and Ulsan to meet just-in-time targets and adapt formulations to regional climate conditions. The automotive acoustic material market in China also absorbs local content rules, pushing foreign firms toward joint ventures for capacity scaling. Japan's hybrid expertise sustains demand for dual-mode barrier-absorber panels, while South Korea's export-focused OEMs specify global-compliant solutions to serve North American and European destinations.

The Middle East and Africa post the fastest expansion at 5.75% CAGR, led by the industrial development in the United Arab Emirates and Saudi Arabian manufacturing incentives embedded in Vision 2030. New CKD plants in Egypt and Morocco create localized demand for dash insulators and door seals tuned for high ambient temperatures. South Africa leverages established export channels to Europe, requiring materials certified to EU noise and recycling directives. Although infrastructure limitations persist, abundant petrochemical feedstocks underpin regional foam production, cushioning feedstock volatility on local converters.

Europe's premium brands keep the region at the forefront of acoustic technology. Germany's OEMs demand ultralight laminates that meet both NVH and sustainability thresholds, spurring suppliers to develop mono-material films compatible with closed-loop recycling. France and Italy prioritize felts made from recycled textile fibers, fitting circular-economy goals, while the United Kingdom nurtures start-ups exploring aerogel-hybrid absorbers. North America's transition toward electric pickup trucks intensifies the need for wheel-arch and underbody damping to manage tire roar, injecting fresh volume into plants in the United States. Across geographies, the automotive acoustic material market adapts formulations to match varying regulatory distances to curb NOx and noise emissions.

List of Companies Covered in this Report:

- Autoneum Holding AG

- Grupo Antolin

- Auria Solutions

- 3M Company

- BASF SE

- Continental AG

- Henkel AG & Co. KGaA

- NVH Korea Inc.

- Adient plc

- Compagnie de Saint-Gobain S.A.

- Toray Industries Inc.

- Sumitomo Riko Co. Ltd.

- Lear Corporation

- Forvia SE (Faurecia SE)

- Owens Corning

- Johns Manville Corporation

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- LyondellBasell Industries N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global Interior Noise Regulations for EVs and HEVs

- 4.2.2 OEM Shift Toward Lightweight, Multifunctional Acoustic-Thermal Composites

- 4.2.3 Rapid Urbanization Spurring Demand for In-Cabin Comfort in Emerging Asia

- 4.2.4 Growing Ride-Sharing and Robo-Taxi Fleets Prioritizing Durable NVH Interiors

- 4.2.5 Emergence of Bio-Based Foams and Recycled Textiles Aligned With ESG Mandates

- 4.2.6 Integrated Acoustic Packages Enabling Vehicle Audio-System Downsizing

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Volatility in Petrochemical Feedstocks for Foams

- 4.3.2 Space Constraints in Skateboard EV Platforms Limiting Insulation Thickness

- 4.3.3 Escalating End-of-Life Recycling Mandates Increasing Material Complexity

- 4.3.4 Rising Popularity of Active Noise Cancellation Cutting Passive-Material Demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Material Type

- 5.1.1 Polyurethane

- 5.1.2 Polypropylene

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Fiberglass

- 5.1.5 Textiles

- 5.1.6 Rubber

- 5.1.7 Foam

- 5.1.8 Others

- 5.2 By Application Area

- 5.2.1 Interior

- 5.2.2 Exterior

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles (LCVs)

- 5.3.3 Medium and Heavy Commercial Vehicles (MHCVs)

- 5.3.4 Buses and Coaches

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Autoneum Holding AG

- 6.4.2 Grupo Antolin

- 6.4.3 Auria Solutions

- 6.4.4 3M Company

- 6.4.5 BASF SE

- 6.4.6 Continental AG

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 NVH Korea Inc.

- 6.4.9 Adient plc

- 6.4.10 Compagnie de Saint-Gobain S.A.

- 6.4.11 Toray Industries Inc.

- 6.4.12 Sumitomo Riko Co. Ltd.

- 6.4.13 Lear Corporation

- 6.4.14 Forvia SE (Faurecia SE)

- 6.4.15 Owens Corning

- 6.4.16 Johns Manville Corporation

- 6.4.17 Covestro AG

- 6.4.18 Dow Inc.

- 6.4.19 Huntsman Corporation

- 6.4.20 LyondellBasell Industries N.V.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment