|

시장보고서

상품코드

2044221

초광대역 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ultra Wideband - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

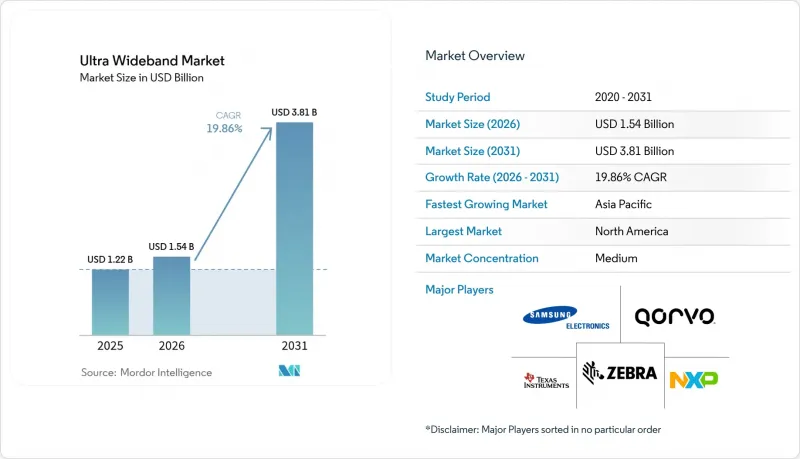

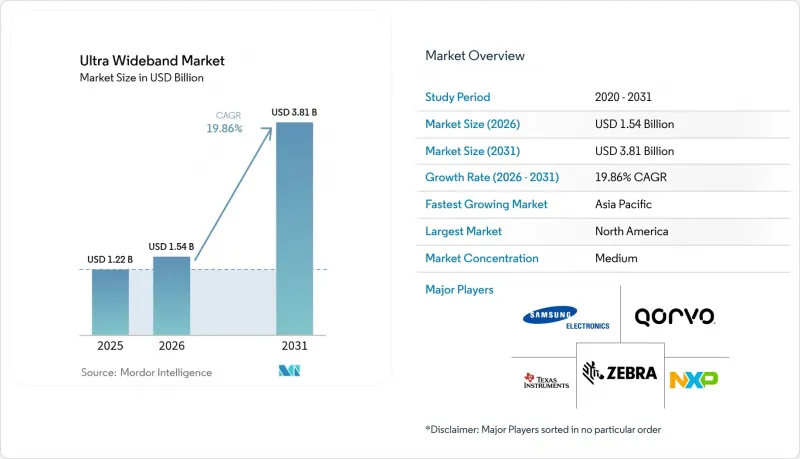

초광대역(UWB) 시장 규모는 2025년에 12억 3,000만 달러로 평가되었고 2026년 15억 4,000만 달러에서 2031년까지 38억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 19.86%를 나타낼 전망입니다.

센티미터 단위의 위치 정확도로 인해 이 기술은 스마트폰의 새로운 기능에서 인더스트리 4.0의 자동화, 항만 물류, 릴레이 공격에 강한 디지털 키의 필수 요소로 전환되고 있습니다. 제조업체들은 10센티미터 미만의 정확도로 자산을 추적하는 시스템을 도입한 후 지게차 충돌 사고에 대한 보험금 청구가 30%-40% 감소했음을 확인했습니다. 한편, 차량 리스 보험사는 UWB 기반 패시브 엔트리 시스템을 장착한 차량에 대해 보험료를 최대 12% 인하했습니다. 특히 유럽연합(EU) 결정 2024/1467과 중국 공업정보화부(MIIT)의 규정에 따라 실외 허용 통신 거리가 2배로 확대되고, 성(省)급 인증 지연이 해소되면서 대규모 인프라 구축에 대한 인센티브가 생겼습니다. 반면, BLE(Bluetooth Low Energy) 도착각 측정 시스템은 UWB용 반도체의 3분의 1의 비용으로 50센티미터의 정확도를 실현하고 있어, 순수한 정확도보다 비용이 주요 경쟁의 초점이 되고 있습니다. 파운드리 업체들이 수익성이 높은 스마트폰용 프로세서를 우선시함에 따라 28나노미터 이하 칩 공급이 여전히 부족하여 모듈 리드타임이 18주까지 늘어났으며, 칩 제조업체들은 대체 생산능력을 확보하거나 더 미세한 공정으로 전환해야 하는 상황에 처해 있습니다.

세계 초광대역(UWB) 시장 동향 및 인사이트

인더스트리 4.0 공장에서 RTLS 수요 폭발적으로 증가

자동차 및 개별 부품 제조업체들은 바코드 스캔을 SAP 제조 실행 시스템에 직접 통합된 UWB 앵커로 대체한 결과, 작업 중 재고가 18%-25% 감소하고 90초 이내에 팔레트 배송을 시작할 수 있게 되었다고 보고하고 있습니다. 2025년에는 독일 공급업체에서만 120만 평방미터의 바닥 면적에 앵커가 도입되었습니다. 일본의 전자기기 조립업체는 UWB를 협동로봇의 안전 영역까지 확장했습니다. IEEE 802.15.4z에 의한 보안 거리 측정 기술이 위장된 비상 정지 비활성화를 방지합니다. 모듈 가격이 1만개 단위 로트당 3.50달러 이하로 떨어지면서 주요 비용 장벽이 제거되었고, 한국의 반도체 팹에서는 공정 베이에서 오배송을 방지하기 위해 클린룸 내 공구 추적을 시범 운영하고 있습니다. 그 결과, 개념증명(PoC)에서 전 세계 공장 네트워크 전체에 걸친 기업 규모의 도입으로 구조적인 전환이 진행되고 있습니다.

스마트폰 OEM의 공간인식 기능 의무화

애플은 2025년 모든 아이폰 라인업에 UWB를 탑재하여 AirTag의 정밀한 위치 파악, 공간 오디오의 헤드 트래킹, 릴레이 공격에 강한 결제 기능을 구현했습니다. 삼성도 갤럭시 S25 Ultra와 Z Fold 6를 통해 이를 따랐고, 샤오미의 15S Pro는 UWB와 BYD 및 NIO 자동차의 디지털 키를 결합했습니다. 이에 대해 보험사들은 UWB 보안 범위 칩이 탑재된 단말기에 5-8% 할인을 제공함으로써 하이엔드 스마트폰에 대한 수요를 촉진했습니다. 구글은 안드로이드 15의 Matter 호환 스마트홈 설정에 UWB 초기 설정 기능을 추가하여 베타 테스트에서 설정 시간을 40% 단축했습니다. FiRa 컨소시엄프로파일에 따른 상호운용성 압박으로 인해 브랜드 간 호환성은 모든 플래그십 단말기에 필수적인 요구사항이 되었습니다.

50cm 미만의 정확도에서 BLE AoA/AoD의 비용 이점

1.20달러 내외의 가격대의 블루투스 포지셔닝 모듈은 소매점 내에서 50센티미터 미만의 정확도를 달성하여 비용에 민감한 사업자에게 UWB를 대체할 수 있는 현실적인 대안이 되고 있습니다. 수만 개의 자산을 추적하는 병원의 경우, 태그 1개당 2달러의 비용을 절감할 수 있으며, 이는 수십만 달러 규모의 설비 투자 비용 절감으로 이어집니다. 2025년 소매 업계의 파일럿 프로젝트에서 BLE가 통로 단위의 재고 검색에 충분하다는 것이 확인되었고, UWB의 도입이 정당화되는 것은 도난 방지에만 국한된 것으로 밝혀졌습니다. 블루투스 SIG의 6.0 로드맵에 따라 정확도 차이는 20cm까지 좁혀졌고, 가격 경쟁은 더욱 치열해지고 있습니다. UWB 공급업체들은 현재 보안 거리 측정 및 릴레이 공격에 대한 저항성을 강조하고 있지만, 이러한 장점은 자동차 및 금융 업계에서 높이 평가되는 것이지 범용 시장에서는 그다지 중요하지 않습니다.

부문 분석

초광대역(UWB) 시장의 성장 모멘텀은 하드웨어의 우위에 의존하고 있지만, 기업들은 네트워크 캘리브레이션과 펌웨어 업데이트를 아웃소싱하는 경향이 증가하고 있으며, 이로 인해 서비스 부문은 2031년까지 20.22%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 여러 건물에 200-500개의 앵커를 설치하는 시설의 경우, 예측 전파 모델로는 금속 랙이나 컨베이어 벨트의 영향을 포착하지 못해 공장당 5만-15만 달러의 비용이 소요되는 현장 조정이 필요한 것으로 나타났습니다. 하드웨어 가격이 빠르게 하락하고, DW3000 모듈 비용은 2023년에서 2025년 사이에 40% 하락하여 수익률에 압력을 가하고 있습니다.

소프트웨어 분야(시장 점유율 15% 내외)에서는 원시 좌표를 AGV 배차와 같은 업무상 트리거로 변환하고 있습니다. 한편, 프랙탈 및 세라믹 설계를 통한 안테나 혁신으로 설치 면적이 50% 감소하여 스마트 워치 및 이어폰에 적용이 가능해졌습니다. 칩, 안테나, 전원 관리 기능을 통합한 모듈로 인증 획득 기간이 절반으로 단축되었습니다. 일반적으로 도입 비용의 12%-18%를 차지하는 정기 유지보수 계약은 인티그레이터에게 예측 가능한 현금 흐름을 보장합니다.

스마트 빌딩에의 도입이 UWB 시장을 주도하고 있으며, LEED 플래티넘 인증 리노베이션 공사에서는 HVAC 부하 최적화를 위한 재실감지가 요구되고 있습니다. 상업용 부동산 소유주들은 공간 활용률이 20-30% 향상되어 고가의 확장 공사를 미루게 되었다는 보고를 하고 있습니다. 2025년 매출에서 가전제품이 27.42%로 1위를 차지했지만, UWB가 표준 플래그십 기능으로 자리 잡으면서 그 성장세가 둔화되고 있습니다.

UWB 액세스 제어는 보안 거리 측정 기능을 통해 배지 복제를 방지할 수 있기 때문에 높은 보안 시설에서 UWB 액세스 제어가 기본 선택이 되고 있습니다. 자동차 및 물류 분야에서는 디지털 키와 V2I(차량 대 인프라) 측위를 통해 두 자릿수 점유율을 유지하고 있으며, 의료 분야에서는 주입 펌프와 휠체어 추적을 통해 분실로 인한 손실을 줄이고 있습니다. 지속적인 분석 사용료가 스마트빌딩의 수익률을 높이고, 하드웨어가 상품화되어도 지속적인 투자를 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 매출의 36.93%를 차지해, 미국 보험사는 UWB 디지털 키 장착 차량에 대해 8%-12%의 차량 보험료 할인을 적용하고, 1,500만 평방피트 규모의 앵커 설치 공장은 UWB 디지털 키 장착 차량에 대한 보험료 할인을 적용합니다. 캐나다는 주파수 할당 지연으로 인해 늦게 출발했지만, 이는 2026년 1월에 겨우 시정되었습니다. 한편, 멕시코에서는 니어쇼어링 붐으로 인해 도입 초기부터 RTLS가 도입되었습니다. 비용 중심의 업계에서는 BLE를 선호하고 있으며, 반도체 부족으로 인해 자동차 업계의 납기 지연이 심화되고 있습니다.

아시아태평양은 CAGR 21.01%를 나타낼 것으로 예측되며, 이는 세계에서 가장 빠른 속도입니다. 중국의 7163-8812MHz 대역의 통일된 규제로 인해 스마트폰의 승인 주기가 8주로 단축되었고, 플래그십 모델에는 UWB와 EV용 디지털 키가 결합되어 있습니다. 일본의 2024년 ARIB 표준 개정으로 2026년 3월부터 도쿄 지하철 역에서 하루 5만 건의 UWB 결제가 가능해졌습니다. 한국에서의 규제 통일로 인해 삼성은 별도의 인증 없이 UWB를 지원하는 갤럭시 S25 울트라를 출시할 수 있었습니다. 인도와 동남아시아의 대부분은 가격에 민감하기 때문에 아직 초기 단계에 있지만, 싱가포르와 쿠알라룸푸르의 실증 실험에서 보행자 흐름이 30% - 40% 개선되었습니다. 호주 및 뉴질랜드는 EU의 기준을 준수하고 광업 분야에서의 도입을 촉진했습니다.

유럽에서는 실외 사용을 금지하고 출력 제한을 높인 결정 2024/1467호 덕분에 2025년 20%대 중반의 점유율을 기록했습니다. 독일은 자동차 분야에서의 의무화와 RTLS를 도입한 800만 평방피트 규모의 공장을 보유하여 선도하고 있습니다. 프랑스와 영국에서는 이중 인증이 필요해 시장 진입이 최대 12주까지 지연되고 있습니다. 스페인과 이탈리아는 온도 관리가 필요한 의약품 물류에 집중하고 있으며, 러시아는 무역 제한으로 인해 첨단 칩셋에 대한 접근이 제한되어 있습니다. 두바이와 아부다비의 GCC 항구에서는 20cm 단위의 컨테이너 추적이 시범적으로 도입되었지만 아프리카에서는 이제 막 도입되기 시작했으며 남아프리카공화국에서는 광업 안전 프로그램에 뒤쳐져 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Ultra-Wideband market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.54 billion in 2026 to reach USD 3.81 billion by 2031, at a CAGR of 19.86% during the forecast period (2026-2031).

Centimeter-level positioning accuracy is shifting the technology from smartphone novelty to an indispensable layer in Industry 4.0 automation, port logistics, and relay-attack-resistant digital keys. Manufacturers observed a 30%-40% drop in forklift-collision insurance claims after adopting sub-10-centimeter asset tracking, while fleet-leasing insurers cut premiums by up to 12% for vehicles fitted with UWB-based passive-entry systems. Regulatory momentum, notably European Union Decision 2024/1467 and China MIIT rules, doubled permissible outdoor range and removed provincial certification delays, creating an incentive for large-scale infrastructure rollouts. Meanwhile, BLE angle-of-arrival systems now reach 50-centimeter precision at one-third of UWB silicon cost, positioning cost as the main competitive battleground rather than raw accuracy. Chip supply below 28 nanometers remains tight because foundries prioritize higher-margin smartphone processors, extending module lead times to 18 weeks and forcing chipmakers to secure alternative capacity or migrate to finer geometries.

Global Ultra Wideband Market Trends and Insights

Explosive RTLS Demand Across Industry 4.0 Plants

Automotive and discrete-parts manufacturers documented 18%-25% cuts in work-in-progress inventory after replacing barcode scans with UWB anchors that integrate directly into SAP manufacturing execution systems, triggering pallet delivery within 90 seconds. German suppliers alone deployed anchors across 1.2 million m2 of floor space in 2025. Japanese electronics assemblers extended UWB to collaborative-robot safety zones where IEEE 802.15.4z secure ranging prevents spoofed emergency-stop overrides. Module price erosion to below USD 3.50 at 10,000-unit volumes removed a key cost barrier, and South Korean semiconductor fabs are piloting cleanroom tool tracking to avert process-bay misrouting. The result is a structural transition from proof-of-concept to enterprise-wide adoption across global factory networks.

Smartphone OEM Mandate for Spatial-Awareness Features

Apple shipped iPhones with UWB across its entire 2025 lineup, enabling precise AirTag finding, spatial audio head-tracking, and relay-attack-resistant payments. Samsung followed with Galaxy S25 Ultra and Z Fold 6, and Xiaomi's 15S Pro paired UWB with digital keys for BYD and NIO vehicles. Insurers responded by offering 5%-8% discounts on devices carrying UWB secure-ranging chips, catalysing demand in premium-tier smartphones. Google added UWB commissioning to Android 15's Matter-compliant smart-home setup, shortening onboarding time by 40% in beta trials. Interoperability pressure from FiRa Consortium profiles made cross-brand compatibility table stakes for any flagship handset.

BLE AoA/AoD Cost Advantage Under 50 cm Accuracy

Bluetooth direction-finding modules priced near USD 1.20 achieved sub-50-centimeter precision inside retail stores, giving budget-conscious operators a viable alternative to UWB. Hospitals tracking tens of thousands of assets save USD 2 per tag, translating into six-figure capital savings. Retail pilots in 2025 confirmed BLE sufficiency for aisle-level inventory searches, with UWB justified only for theft prevention. Bluetooth SIG's 6.0 roadmap narrows the accuracy gap to 20 centimeters, intensifying price pressure. UWB suppliers now emphasize secure ranging and relay-attack resistance, benefits that resonate in automotive and finance but less so in horizontal markets.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Green-Lights for Sub-GHz UWB in Europe and Asia-Pacific

- Automotive Shift to Digital Keys and In-Cabin Radar

- Chip Supply Bottlenecks Below 28 nm

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ultra-wideband market size momentum rests on hardware dominance, yet enterprises increasingly outsource network calibration and firmware updates, driving services toward a 20.22% CAGR through 2031. Facilities installing 200-500 anchors across multiple buildings learned that predictive propagation models fail to capture metal racks and conveyor belts, requiring on-site tuning that often costs USD 50,000-USD 150,000 per plant. Hardware price erosion is rapid; DW3000 module costs fell 40% between 2023 and 2025, putting pressure on margins.

Software's mid-teens slice translates raw coordinates into business triggers such as AGV dispatch, while antenna innovation from fractal and ceramic designs trims footprint 50%, enabling smartwatch and earbud use cases. Modules that bundle chips, antennas, and power management now cut certification time in half. Recurring maintenance contracts, typically 12%-18% of deployment cost, secure predictable cash flows for integrators.

Smart-building deployments propel the ultra-wideband market as LEED Platinum retrofits demand occupancy sensing to optimize HVAC loads. Commercial landlords reported 20%-30% space-utilization gains, postponing costly expansions. Consumer electronics led 2025 revenue at 27.42%, yet its growth is plateauing as UWB becomes a standard flagship feature.

Secure ranging prevents badge cloning, making UWB access control the default choice in high-security facilities. Automotive and logistics maintain double-digit share via digital keys and vehicle-to-infrastructure positioning, while healthcare tracks infusion pumps and wheelchairs to reduce loss write-offs. Recurring analytics fees bolster smart-building margins, supporting continued investment even as hardware commoditizes.

The Ultra Wideband Market Report is Segmented by Component (Hardware, Software, and Services), End-User Vertical (Consumer Electronics, Automotive and Transportation, and More), Device Type (Smartphones, and More), Frequency Band (3. 1-4. 8 GHz, and 6-10. 6 GHz), Range Capability (Short-Range, and More), Application (RTLS, Secure Digital Keys, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 36.93% of 2025 revenue, with United States insurers granting 8%-12% fleet-premium cuts for UWB digital-key vehicles and factories covering 15 million ft2 with anchors. Canada lagged due to delayed spectrum allocation, corrected only in January 2026, while Mexico's nearshoring boom deployed RTLS from day one. Cost-sensitive verticals lean toward BLE, and semiconductor shortages exacerbate automotive wait times.

Asia-Pacific is forecast to register a 21.01% CAGR, the fastest globally. China's unified 7163-8812 MHz rules shortened smartphone approval cycles to eight weeks, and flagship phones paired UWB with EV digital keys. Japan's 2024 ARIB update enabled 50,000 daily UWB payments at Tokyo metro stations starting March 2026. South Korea's rule harmonization let Samsung launch UWB-enabled Galaxy S25 Ultra without extra certification. India and most of Southeast Asia remain early-stage due to price sensitivity, though Singapore and Kuala Lumpur pilots improved pedestrian flow 30%-40%. Australia and New Zealand mirrored EU standards, easing mining-sector adoption.

Europe captured a mid-twenties share in 2025 thanks to Decision 2024/1467 that opened outdoor use and raised power limits. Germany leads with automotive mandates and 8 million ft2 of RTLS-equipped plants. France and United Kingdom face dual certification, slowing market entry by up to 12 weeks. Spain and Italy focus on temperature-controlled pharma logistics, while Russia's access to advanced chipsets is limited by trade restrictions. GCC ports in Dubai and Abu Dhabi piloted 20-centimeter container tracking, whereas African adoption is nascent, with South Africa trailing mining safety programs.

- Apple Inc.

- Qorvo Inc.

- NXP Semiconductors NV

- Zebra Technologies Corp.

- Texas Instruments Inc.

- Samsung Electronics Co. Ltd.

- Sony Group Corporation

- STMicroelectronics NV

- Infineon Technologies AG

- Qualcomm Inc.

- Broadcom Inc.

- Pulse-Link Inc.

- Humatics Corp.

- Alereon Inc.

- Fractus SA

- Johanson Technology Inc.

- BeSpoon SAS

- Sewio Networks s.r.o.

- Decawave Ltd. (Qorvo)

- Nanotron Technologies GmbH

- Ubisense Ltd.

- Murata Manufacturing Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive RTLS Demand Across Industry 4.0 Plants

- 4.2.2 Smartphone OEM Mandate for Spatial-Awareness Features

- 4.2.3 Regulatory Green-Lights for Sub-GHz UWB in Europe and Asia-Pacific

- 4.2.4 Automotive Shift to Digital Keys and In-Cabin Radar

- 4.2.5 Open-Source UWB Firmware Lowering Entry Barriers

- 4.2.6 National Infrastructure Funding for Smart Ports and Airports

- 4.3 Market Restraints

- 4.3.1 BLE AoA/AoD Cost Advantage Under 50 cm Accuracy

- 4.3.2 Chip Supply Bottlenecks Below 28 nm

- 4.3.3 Fragmented Regional Spectrum Rules Slowing Certification

- 4.3.4 Sophisticated Micro-Location Spoofing and Side-Channel Attacks

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 ICs/Chipsets

- 5.1.1.2 Antennas

- 5.1.1.3 Modules

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By End-User Vertical

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive and Transportation

- 5.2.3 Healthcare

- 5.2.4 Manufacturing and Industrial

- 5.2.5 Retail and Warehousing

- 5.2.6 Defense and Public Safety

- 5.2.7 Smart Buildings

- 5.3 By Device Type

- 5.3.1 Smartphones

- 5.3.2 Wearables and Hearables

- 5.3.3 Vehicles

- 5.3.4 Drones and Robots

- 5.3.5 Fixed Infrastructure (Gateways, Beacons)

- 5.4 By Frequency Band

- 5.4.1 3.1-4.8 GHz

- 5.4.2 6-10.6 GHz

- 5.5 By Range Capability

- 5.5.1 Short-Range (Less than 10 m)

- 5.5.2 Mid-Range (10-30 m)

- 5.5.3 Long-Range (More than 30 m)

- 5.6 By Application

- 5.6.1 Real-Time Location Systems (RTLS)

- 5.6.2 Secure Digital Keys

- 5.6.3 Augmented and Virtual Reality (AR/VR) Mapping

- 5.6.4 Asset Tracking and Inventory Management

- 5.6.5 Smart Home and Building Automation

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Southeast Asia

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 GCC

- 5.7.5.2 Turkey

- 5.7.5.3 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Qorvo Inc.

- 6.4.3 NXP Semiconductors NV

- 6.4.4 Zebra Technologies Corp.

- 6.4.5 Texas Instruments Inc.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 Sony Group Corporation

- 6.4.8 STMicroelectronics NV

- 6.4.9 Infineon Technologies AG

- 6.4.10 Qualcomm Inc.

- 6.4.11 Broadcom Inc.

- 6.4.12 Pulse-Link Inc.

- 6.4.13 Humatics Corp.

- 6.4.14 Alereon Inc.

- 6.4.15 Fractus SA

- 6.4.16 Johanson Technology Inc.

- 6.4.17 BeSpoon SAS

- 6.4.18 Sewio Networks s.r.o.

- 6.4.19 Decawave Ltd. (Qorvo)

- 6.4.20 Nanotron Technologies GmbH

- 6.4.21 Ubisense Ltd.

- 6.4.22 Murata Manufacturing Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment