|

시장보고서

상품코드

2044225

스마트폰 카메라 렌즈 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Smartphone Camera Lens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

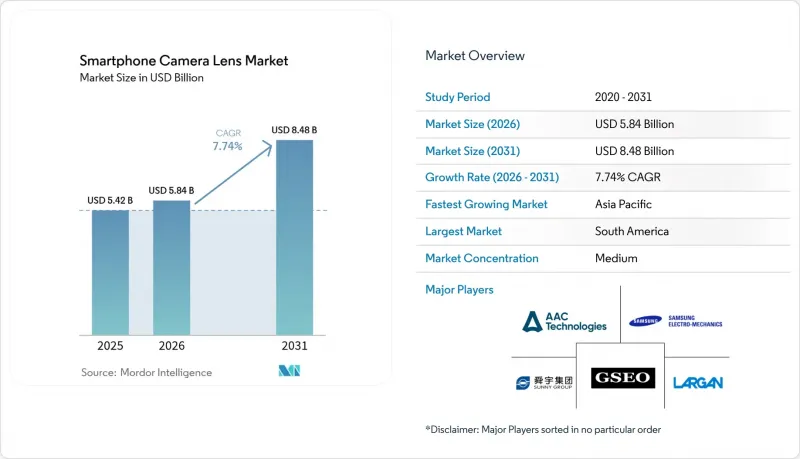

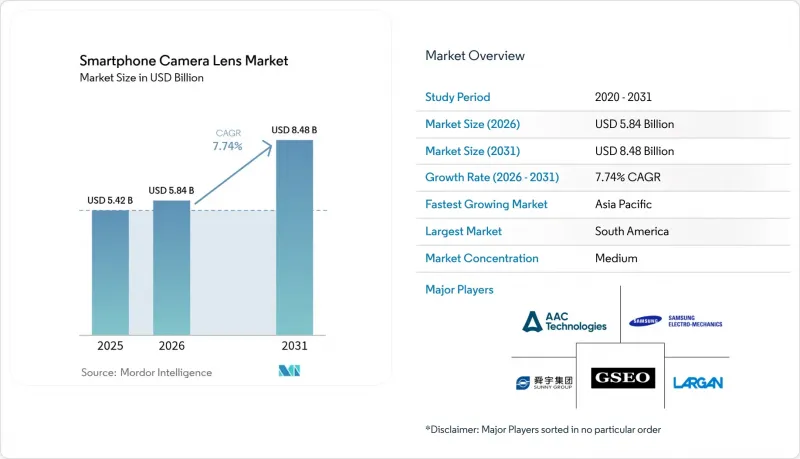

스마트폰 카메라 렌즈 시장 규모는 2025년에 54억 2,000만 달러로 평가되었고 2026년 58억 4,000만 달러에서 2031년까지 84억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.74%를 나타낼 전망입니다.

장치 제조업체들이 기본 플라스틱 광학을 7매 또는 8매 구성의 유리-플라스틱 하이브리드로 대체함에 따라 렌즈 모듈의 평균 판매 가격은 계속 상승하고 있으며, 특히 잠망경 및 가변 조리개 어셈블리의 경우 더욱 그러합니다. 망원 줌 기능은 중급형 스마트폰에도 확대되고 있으며, 공급업체에게는 전 세계 스마트폰 출하량 증가에 대한 우려를 보완할 수 있는 유망한 경로가 되고 있습니다. 또한, AI 기반 컴퓨테이셔널 포토그래피를 지원하기 위해 초광각, 매크로, 심도 렌즈를 필요로 하는 멀티 카메라 구성도 수요를 촉진하고 있습니다. 이미 가동률이 거의 만반에 가까운 정밀 유리 성형 능력은 단위당 불량률이 기존 광각 모듈에 비해 여전히 높기 때문에 더욱 타이트해질 것으로 예측됩니다.

세계 스마트폰 카메라 렌즈 시장 동향과 인사이트

망원경 및 망원 모듈의 급속한 확산

망원 모듈은 2025년 1,000달러짜리 플래그십 모델에서 400-600달러짜리 단말기로 보급 범위를 넓혀 프리미엄 단말기와 중저가 단말기의 광학 줌 성능 격차를 좁혀가고 있습니다. 각 어셈블리는 7-8개의 유리-플라스틱 하이브리드 렌즈와 프리즘으로 구성되어 있기 때문에 페리스코프 줌이 추가되면 평균 판매가격이 18-22% 상승합니다. 대립정밀(Largan Precision)의 출하량은 전년 대비 34% 증가했지만, 프리즘의 정렬 공차가 5마이크로미터 이하이기 때문에 불량률은 광각렌즈에 비해 약 12-15% 포인트 더 높습니다. 현재 OEM 업체들의 마케팅은 5배에서 10배의 광학 줌을 주요 기능으로 강조하고 있으며, 이로 인해 소비자의 렌즈 품질에 대한 인식이 높아지고 있습니다. 정밀 유리 성형의 생산 능력의 제약으로 인해 2027년까지도 페리스코프의 보급이 계속 진행되어 공급업체들의 수익률을 계속 끌어올릴 것으로 예측됩니다.

5,000만 화소 이상의 메가픽셀 경쟁으로 렌즈 평균 판매 가격 상승

소니의 2억 화소 LYT-901 센서는 100 lp/mm에서 0.6 이상의 변조 전달 함수(MTF) 값이라는 광학 벤치마크를 설정하여 렌즈 제조업체에 비구면 유리와 고급 코팅을 사용하도록 압박하고 있습니다. 삼성의 ISOCELL HP5는 카메라 스택을 얇게 만들었지만, 모듈 비용을 높여 플래그십 모델의 광학 서브시스템 단가를 대당 80-100달러로 끌어올렸습니다. 고급형과 보급형 광학장치의 가격 차이는 현재 3-6배에 달하며, 세계 휴대폰 출하량이 정체된 상황에서도 각 업체들은 프리미엄 프로젝트를 우선시하고 있습니다. 화소수 증가는 이미지 서클의 확대로 이어져 렌즈 직경의 대형화 및 렌즈 요소의 추가가 불가피하게 되었습니다. 이러한 요구 사항은 2025년 하이브리드 렌즈가 시장의 거의 절반을 차지할 것으로 예상되는 이유를 설명합니다.

전 세계 스마트폰 출하량 1위

2025년에는 교체 주기가 3년을 넘기면서 전 세계 출하량이 12억 대 내외로 정체되고, 인도 시장은 1% 축소되었습니다. TechInsights의 조사에 따르면, 2025년 상반기 전 세계 출하량 증가율은 4%에 불과한 반면, 600달러 이상 단말기의 매출은 8% 증가하여 양보다 질을 중시하는 경향이 두드러졌습니다. 이러한 포화상태로 인해 프리미엄 계층의 호조에도 불구하고 렌즈 수요 증가율은 한 자릿수 성장에 그치고 있습니다. 플래그십 모델은 출하량의 4분의 1 이하임에도 불구하고 렌즈 관련 수익의 거의 절반을 차지하기 때문에 공급업체는 수익 집중화 위험에 직면해 있습니다. 따라서 프리미엄 계층 수요가 조금이라도 줄어들면 수익률은 빠르게 압박을 받을 수 있습니다.

부문 분석

망원 렌즈는 2031년까지 연평균 복합 성장률(CAGR) 8.58%를 기록하며 전체 기술 중 가장 빠른 속도로 성장하고 있어, 스마트폰 단말기 출하량 증가에도 불구하고 스마트폰 카메라 렌즈 시장에서의 점유율이 확대되고 있습니다. 400-600달러짜리 스마트폰에 탑재된 페리스코프식 줌 모듈이 출하량이 증가하면서 각 브랜드는 5배에서 10배의 광학 줌을 주류 기능으로 홍보할 수 있게 되었습니다. 광각 렌즈는 2025년에도 스마트폰 카메라 렌즈 시장 점유율의 42.36%를 차지했지만, 혁신에 대한 투자가 보조 카메라로 옮겨가면서 성장세가 주춤했습니다. AI에 의한 직선 보정 기술로 120도 화각이 실현되면서 초광각 설계의 중요성이 높아진 반면, 고해상도 망원 렌즈로 접사 촬영이 가능해지면서 매크로 센서는 사라지고 있습니다. 캐논의 26단 다이나믹 레인지를 가진 SPAD 프로토타입은 미래의 망원 렌즈에 95% 이상의 광 투과율을 요구하고 있으며, 이는 렌즈 스택에 더 많은 유리를 포함하게 될 것임을 시사합니다.

렌즈 요소 증가와 프리즘 어셈블리의 채택으로 망원 모듈의 가격은 광각 유닛보다 40-50% 더 비싸기 때문에 Largan과 Sunny Optical과 같은 공급업체들은 수익성이 높은 이 제품 구성에 생산 능력을 집중하고 있습니다. 각 잠망경 렌즈에는 7-8개의 유리-플라스틱 하이브리드 요소가 필요하며, 이는 금형의 복잡성과 수율 위험을 모두 증가시킵니다. 프리즘의 정렬 공차가 5마이크로미터 이하이기 때문에 단위당 불량률은 기존 모듈보다 약 12-15% 포인트 높지만, 페리스코프 줌이 추가될 때마다 평균 판매 가격(ASP)이 18-22% 상승하기 때문에 수익률은 여전히 매력적입니다. 직선 보정 알고리즘으로 강화된 초광각 모듈은 기존 플라스틱 설계보다 25-30% 더 비싼 프리폼 비구면 유리를 채택하고 있습니다. 매크로 기능과 심도 기능을 고해상도 보조 렌즈에 통합하여 센서 수를 줄이면서 스마트폰 1대당 렌즈의 총 판매량을 유지하고 있습니다.

유리-플라스틱 하이브리드는 2025년 매출의 47.89%를 차지했으며, CAGR 8.39%로 2028년까지 스마트폰 카메라 렌즈 시장 점유율에서 전체 플라스틱 설계를 추월할 것으로 예측됩니다. 하이브리드 스택은 2-3개의 유리 요소와 4-5개의 플라스틱 요소를 결합하여 색수차 제어와 경량화를 동시에 실현합니다. 전유리 렌즈는 7장 구성의 유리 스택이 15-20% 더 무겁고, 제조 비용이 최대 40% 더 비싸기 때문에 접이식 단말기나 초고가 모델에 한정되어 있습니다. 전체 플라스틱 광학계는 200달러 이하의 단말기에 머물러 있지만, 중저가 제조업체들이 카메라 차별화를 위해 하이브리드 사양의 업그레이드를 내놓으면서 그 점유율이 줄어들고 있습니다. 화웨이, OPPO, vivo의 멀티 엘리먼트 망원 렌즈 출시로 인해 Sunny Optical의 하이브리드 렌즈 매출은 2025년상반기에 두 배 이상 증가했습니다.

제조 공정의 능력이 승패를 가르는 요소입니다. 라간의 정밀 유리 성형 기술은 플라스틱으로는 불가능한 0.2 마이크로미터 이하의 표면정밀도를 실현하고 있으며, 이를 통해 2억 화소 센서에서 100 lp/mm에서 0.6 이상의 MTF를 확보하고 있습니다. 새로운 폴리머 배합으로 열팽창률이 70ppm/°C에서 50ppm/°C로 감소하여 유리와의 초점 편차 차이가 줄어들었지만, 여전히 잠망경 설계에는 충분하지 않습니다. 폴더블 스마트폰에서도 플라스틱은 힌지 쪽의 무게를 줄일 수 있어 하이브리드를 선호하지만, 유리는 반복적인 접힘을 견디기 위해 스택을 단단하게 만듭니다. AI 이미지 처리로 투과율 목표치가 92% 이상이 되면, 하이브리드 렌즈는 중-고급 기계식 렌즈의 표준이 되어 스마트폰 카메라 렌즈 시장에서 주류가 될 수 있는 길을 굳건히 할 수 있습니다.

지역별 분석

아시아태평양은 렌즈 제조 및 조립 분야에서 중국의 우위로 인해 2025년 매출의 64.22%를 차지했으며, 광둥성과 장쑤성이 전 세계 생산 능력의 대부분을 차지했습니다. 인도의 생산 연동형 인센티브 제도로 인해 카메라 모듈 생산이 타밀나두 주와 카르나타카 주로 이동하고 있으며, 애플과 삼성의 리드타임이 단축되고 있습니다. Tata Electronics의 Wistron의 아이폰 공장 인수는 이러한 변화를 상징하며, 렌즈와 액추에이터의 현지 조달을 가속화하고 있습니다. 베트남은 LG이노텍의 V3 증설로 현지 생산량이 두 배로 늘어나며 제2의 거점으로 부상하고 있습니다.

남미는 CAGR 8.79%로 가장 빠르게 성장하고 있는 지역으로, 5G 보급과월평균 9GB에 달하는 모바일 동영상 수요 증가가 그 원동력이 되고 있습니다. 중국 OEM인 HONOR, OPPO, vivo는 브라질, 아르헨티나, 칠레에서 점유율을 확대되고 있습니다. 이들 국가에서는 2024년 200달러 이하 스마트폰 출하량이 두 배로 증가했으며, 미화 600달러 이상의 프리미엄 부문도 확대되고 있습니다. 이러한 양극화는 비용 중심의 모듈과 고수익률의 하이브리드 제품에 대한 렌즈 수요를 촉진하고 있습니다.

북미와 유럽을 합치면 세계 전체 매출의 약 3분의 1을 차지하지만 교체 주기가 3.5년을 넘기 때문에 CAGR은 6.5-7.0%에 그쳐 세계 전체 성장률에 미치지 못하는 상황입니다. 중동 및 아프리카의 총 점유율은 10% 미만입니다. 5G 네트워크에 대한 투자로 보급률이 상승하고 있지만, 가격 제약으로 인해 렌즈의 평균 판매 가격(ASP)은 8-12달러에 불과하며, 주로 플라스틱 소재의 렌즈가 주류를 이루고 있습니다. 나이지리아와 이집트의 환율 변동과 관세도 추가적인 억제요인으로 작용하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The smartphone camera lens market size was valued at USD 5.42 billion in 2025 and estimated to grow from USD 5.84 billion in 2026 to reach USD 8.48 billion by 2031, at a CAGR of 7.74% during the forecast period (2026-2031).

Average selling prices for lens modules continue to climb as device makers replace basic plastic optics with 7- or 8-element glass-plastic hybrids, especially in periscope and variable-aperture assemblies. Telescopic zoom capability is expanding into mid-range handsets, giving suppliers a lucrative path to offset stagnant global smartphone shipments. Demand also benefits from multi-camera configurations that require ultra-wide, macro, and depth lenses to support AI-driven computational photography. Precision glass-molding capacity, already operating near full utilization, is set to tighten further as per-unit defects remain higher than conventional wide-angle modules.

Global Smartphone Camera Lens Market Trends and Insights

Rapid Adoption of Periscope and Telephoto Modules

Periscope telephoto modules moved from USD 1,000 flagships to USD 400-600 handsets in 2025, shrinking the optical-zoom gap between premium and mid-range devices. Each assembly relies on 7- or 8-element glass-plastic hybrids plus a prism, so average selling prices jump 18-22% when periscope zoom is added. Shipments rose 34% year over year at Largan Precision, yet prism alignment tolerances below 5 µm keep reject rates roughly 12-15 points higher than for wide-angle lenses. OEM marketing now highlights 5x to 10x optical zoom as a headline feature, reinforcing consumer awareness of lens quality. Capacity constraints in precision glass molding suggest that periscope penetration will continue to lift supplier margins through 2027.

Megapixel Race Above 50 MP Lifting Lens ASPs

Sony's 200 MP LYT-901 sensor sets an optical benchmark of modulation-transfer-function values above 0.6 at 100 lp/mm, forcing lens makers to use aspheric glass and advanced coatings. Samsung's ISOCELL HP5 keeps camera stacks thinner but raises module cost, pushing flagship optical subsystems toward USD 80-100 per phone. The gulf between high-end and entry optics now reaches a 3-6X price multiple, so vendors prioritize premium projects even while global handset volumes flatten. Higher pixel counts also widen image circles, which drives larger lens diameters and additional elements. These requirements explain why hybrid lenses gained nearly half the market in 2025.

Global Smartphone Unit Saturation

Worldwide shipments stalled near 1.2 billion units and India's market slid 1% in 2025, as replacement cycles stretched beyond three years. TechInsights tracked only 4% global unit growth in 1H 2025 versus 8% revenue growth for devices above USD 600, highlighting a shift to value over volume. This saturation caps lens demand growth at single-digit rates even while premium tiers thrive. Suppliers face revenue concentration risk because flagship models represent under one-quarter of units yet almost half of lens income. Any downturn in premium demand could therefore compress margins quickly.

Other drivers and restraints analyzed in the detailed report include:

- AI-Centric Computational Photography Requirements

- Proliferation of Multi-Camera Smartphones

- Aggressive Pricing Pressure in Mid- and Low-Tier Handsets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telephoto optics posted an 8.58% CAGR to 2031, the quickest pace among all technologies, so their slice of the smartphone camera lens market size is expanding even as total handset units plateau. Shipments rose when periscope zoom modules migrated into USD 400-600 phones, allowing brands to advertise 5x to 10x optical zoom as a mainstream feature. Wide-angle lenses still held 42.36% smartphone camera lens market share in 2025, but their growth stalled because innovation dollars now chase auxiliary cameras. Ultra-wide designs gained relevance after AI rectilinear correction unlocked 120-degree fields of view, while macro sensors began to disappear as high-resolution telephotos can crop in for close-ups. Canon's 26-stop-range SPAD prototype suggests future telephotos will demand >95% light transmission, which pushes even more glass into lens stacks.

Higher element counts and prism assemblies lift telephoto module prices 40-50% above wide units, so suppliers such as Largan and Sunny Optical funnel capacity toward this richer mix. Each periscope lens requires 7-8 glass-plastic hybrid elements, raising both tooling complexity and yield risk. Prism alignment tolerances under 5 µm keep per-unit defect rates roughly 12-15 points above conventional modules, yet profit margins remain attractive because ASPs rise 18-22% whenever periscope zoom is added. Ultra-wide modules, bolstered by rectilinear algorithms, now feature free-form aspheric glass that costs 25-30% more than earlier plastic designs. Macro and depth functions consolidate into higher-resolution secondaries, trimming sensor counts while sustaining total lens revenue per phone.

Glass-plastic hybrids captured 47.89% of 2025 revenue, and their 8.39% CAGR means they will overtake all-plastic designs in smartphone camera lens market share before 2028. Hybrid stacks mix two or three glass elements with four or five plastic ones, marrying chromatic-aberration control to weight savings. All-glass lenses remain confined to foldables and ultra-premium models because a seven-element glass stack weighs 15-20% more and costs up to 40% extra to build. All-plastic optics linger in sub-USD 200 devices, but their share erodes as mid-range makers tout hybrid upgrades for camera differentiation. Sunny Optical more than doubled hybrid-lens revenue in 1H 2025 as Huawei, OPPO, and vivo launched multi-element telephotos.

Process capability is the swing factor. Precision glass molding from Largan achieves surface accuracy below 0.2 µm, impossible with plastics, which ensures MTF above 0.6 at 100 lp/mm for 200 MP sensors. New polymer formulas cut thermal expansion from 70 ppm / °C to 50 ppm / °C, narrowing the focus-shift gap with glass, yet not enough for periscope designs. Foldable phones also favor hybrids because plastic keeps hinge-side weight down, while glass stiffens the stack to withstand repeated folding. As AI imaging pushes transmission targets past 92%, hybrids become the default for mid- and high-end tiers, locking in their path to majority status in the smartphone camera lens market size.

The Smartphone Camera Lens Market Report is Segmented by Lens Technology (Telephoto, Macro/Depth, and More), Lens Material (All-Glass, All-Plastic, and More), Camera Position (Rear-Primary, Rear-Secondary, Front/Facing), Manufacturing Process (Injection Moulding, Precision Glass Moulding, and More), Smartphone Tier (Flagship, Mid-Range, Entry-Level), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 64.22% of 2025 revenue thanks to China's dominance in lens fabrication and assembly, with Guangdong and Jiangsu provinces hosting a majority of global capacity. India's Production-Linked Incentive scheme is redirecting camera module work to Tamil Nadu and Karnataka, trimming lead times for Apple and Samsung. Tata Electronics' takeover of Wistron's iPhone plant exemplifies this shift, accelerating localized sourcing of lenses and actuators. Vietnam is emerging as a secondary center as LG Innotek's V3 expansion doubles local output.

South America is the fastest-growing region at an 8.79% CAGR, propelled by 5G rollouts and a rising preference for mobile video that averages 9 GB per month. Chinese OEMs HONOR, OPPO, and vivo capture share in Brazil, Argentina, and Chile, where smartphones priced under USD 200 doubled shipments in 2024 yet a premium segment above USD 600 is also expanding. This bifurcation fuels lens demand for both cost-sensitive modules and high-margin hybrids.

North America and Europe together account for roughly one-third of global revenue but trail the worldwide growth rate at 6.5-7.0% CAGR because replacement cycles now exceed 3.5 years. Middle East and Africa collectively hold under 10% share; 5G network investments lift penetration, yet affordability keeps lens ASPs in the USD 8-12 range and supports mainly all-plastic designs. Currency volatility and tariffs in Nigeria and Egypt add further constraints.

- Largan Precision Co. Ltd.

- Sunny Optical Technology (Group) Co. Ltd.

- Samsung Electro-Mechanics Co. Ltd.

- Genius Electronic Optical Co. Ltd.

- AAC Technologies Holdings Inc.

- LG Innotek Co. Ltd.

- Kantatsu Co. Ltd.

- Sekonix Co. Ltd.

- Asia Optical Co. Inc.

- Kinko Optical Co. Ltd.

- Haesung Optics Co. Ltd.

- OFILM Group Co. Ltd.

- Newmax Technology Co. Ltd.

- KMOT Co. Ltd.

- Tianyang Optical Technology Co. Ltd.

- Ability Opto-Electronics Technology Co. Ltd.

- Tamron Co. Ltd.

- Hoya Group

- Nidec Sankyo Corp.

- Calin Technology Co. Ltd.

- Fujinon Corporation

- Sekonic Holdings

- Light Co.

- Truemax Engineering Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Multi-Camera Smartphones

- 4.2.2 Megapixel Race Above 50 MP Lifting Lens ASPs

- 4.2.3 Rapid Adoption of Periscope and Telephoto Modules

- 4.2.4 AI-Centric Computational Photography Requirements

- 4.2.5 Localised Lens Supply-Chain Build-Out in India and Vietnam

- 4.2.6 Glass-Plastic Free-Form Lenses for Foldables and Wearables

- 4.3 Market Restraints

- 4.3.1 Global Smartphone Unit Saturation

- 4.3.2 Aggressive Pricing Pressure in Mid- and Low-Tier Handsets

- 4.3.3 High-Layer Hybrid Lens Yield Challenges

- 4.3.4 Export-Control Risk on Precision Glass-Moulding Tools

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Lens Technology

- 5.1.1 Wide/Primary

- 5.1.2 Ultra-Wide

- 5.1.3 Telephoto

- 5.1.4 Macro/Depth

- 5.2 By Lens Material

- 5.2.1 All-Glass

- 5.2.2 All-Plastic

- 5.2.3 Glass-Plastic Hybrid

- 5.3 By Camera Position

- 5.3.1 Rear-Primary

- 5.3.2 Rear-Secondary

- 5.3.3 Front/Facing

- 5.4 By Manufacturing Process

- 5.4.1 Glass Compression Moulding

- 5.4.2 Injection Moulding

- 5.4.3 Precision Glass Moulding

- 5.4.4 Other Manufacturing Process

- 5.5 By Smartphone Tier

- 5.5.1 Flagship

- 5.5.2 Mid-Range

- 5.5.3 Entry-Level

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Largan Precision Co. Ltd.

- 6.4.2 Sunny Optical Technology (Group) Co. Ltd.

- 6.4.3 Samsung Electro-Mechanics Co. Ltd.

- 6.4.4 Genius Electronic Optical Co. Ltd.

- 6.4.5 AAC Technologies Holdings Inc.

- 6.4.6 LG Innotek Co. Ltd.

- 6.4.7 Kantatsu Co. Ltd.

- 6.4.8 Sekonix Co. Ltd.

- 6.4.9 Asia Optical Co. Inc.

- 6.4.10 Kinko Optical Co. Ltd.

- 6.4.11 Haesung Optics Co. Ltd.

- 6.4.12 OFILM Group Co. Ltd.

- 6.4.13 Newmax Technology Co. Ltd.

- 6.4.14 KMOT Co. Ltd.

- 6.4.15 Tianyang Optical Technology Co. Ltd.

- 6.4.16 Ability Opto-Electronics Technology Co. Ltd.

- 6.4.17 Tamron Co. Ltd.

- 6.4.18 Hoya Group

- 6.4.19 Nidec Sankyo Corp.

- 6.4.20 Calin Technology Co. Ltd.

- 6.4.21 Fujinon Corporation

- 6.4.22 Sekonic Holdings

- 6.4.23 Light Co.

- 6.4.24 Truemax Engineering Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment