|

시장보고서

상품코드

2044239

사이리스터 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Thyristor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

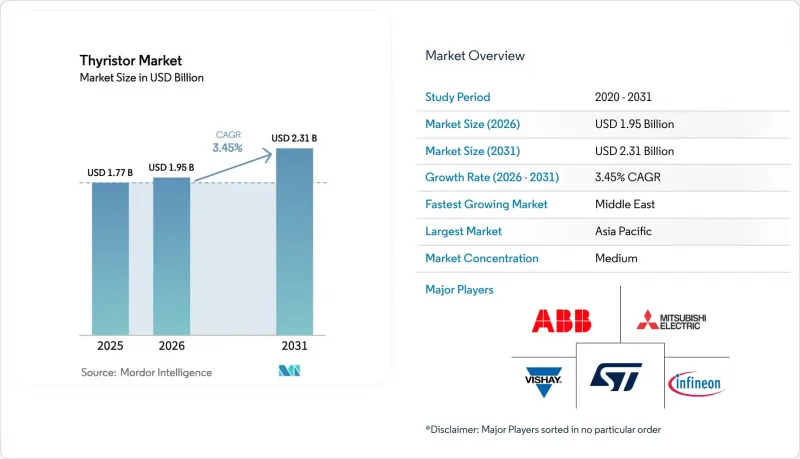

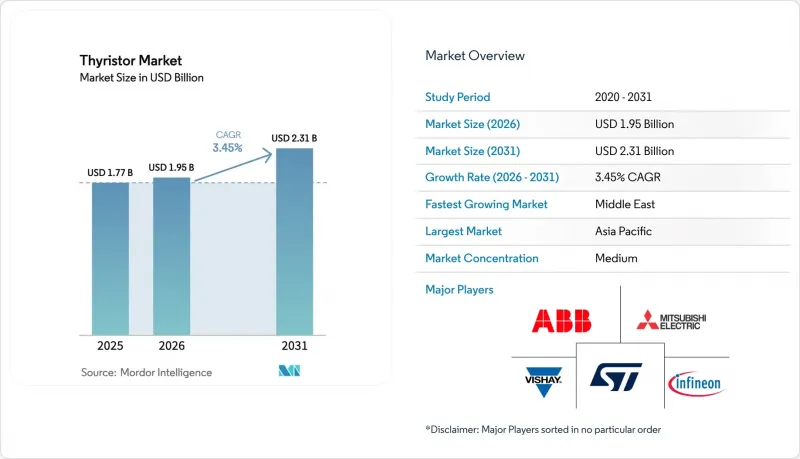

사이리스터 시장 규모는 2025년에 17억 7,000만 달러로 평가되었고 2026년 19억 5,000만 달러에서 2031년까지 23억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 3.45%를 나타낼 전망입니다.

실리콘 카바이드 금속산화막 반도체 전계효과 트랜지스터(SiC MOSFET)가 자동차 및 고주파 산업용 드라이브 시장에서 점유율을 확대하는 한편, 전력회사들이 여전히 수 기가 와트급 고압직류송전(HVDC) 회선에서 라인 정류형 밸브를 선호하고 있어 수요는 여전히 견조합니다. 견조한 수요를 유지하고 있습니다. 조달 주기는 몇년후까지 수주를 확보하는 대규모 송전망 프로젝트에 의해 좌우되지만, 모듈 통합업체는 게이트 드라이버와 센서가 내장된 지능형 전력 모듈로 다변화를 추진하고 있습니다. 중국의 주요 디스크리트 부품 공급업체들이 유럽 경쟁사보다 평균 20-30% 낮은 평균 판매 가격으로 스터드형 및 캡슐형 디바이스를 제공함에 따라, 저/중정격 출력 제품의 가격 경쟁이 심화되고 있습니다. 동시에 위조품의 위험과 인증 지연으로 인해 추적 가능성과 수직적 통합 제조의 중요성이 커지고 있습니다.

세계 사이리스터 시장 동향 및 인사이트

아시아 해상풍력 발전을 통합하는 HVDC 링크 확대

중국, 한국, 호주에서는 대규모 해상풍력 회랑이 계속해서 새로운 ±800kV 송전선로의 기반이 되고 있으며, 각 회랑은 용량 1기가와트당 200-300개의 프레스팩형 장치를 필요로 합니다. 중국 하미 충칭과 닝샤-후난 송전선로에만 16GW의 컨버터 용량이 추가되며, 여기에는 라인 정류단용 사이리스터 밸브가 지정되어 있습니다. 2024년 승인된 한국의 '서해안 에너지 고속도로'는 2028년까지 1,600개의 고출력 장치 수요를 확보하고 있습니다. 호주의 마리너스 링크는 사이리스터에 대해 개별적으로 고전압 위치를 확보한 혼합 밸브 방식을 채택하고 있다(hitachienergy.com). 따라서 프로젝트 수주 잔고는 2030년대 초까지 지속될 것으로 예상되며, 전압원 변환기(VSC)의 선택이 증가하는 가운데서도 사이리스터 시장은 유지될 것으로 보입니다.

EU 전력 사업자의 그리드 코드에 따른 동적 무효전력 보상 의무화 의무화

업데이트된 ENTSO-E 지침에 따라 배전 사업자는 피크 및 비피크 시간대에 역률을 ±0.95 이내로 유지해야 합니다. 독일 연방 네트워크청은 10MW 이상의 발전소에 대해 2026년 1월까지 동적 지원 시스템 도입을 의무화하고 있으며, 이로 인해 사이리스터 스위치드 커패시터 뱅크와 정적 무효전력 보상장치(SVC)에 대한 수주가 촉진되고 있습니다. 스페인에서는 이미 48개의 펄스 밸브 어셈블리가 장착된 1,800 MVAr의 정적 동기 보상 장치가 도입되었습니다. 이탈리아는 재생에너지 출력 억제를 완화하기 위해 2024년 900 MVAr의 유연한 교류 송전 시스템(FACTS) 장비를 발주했습니다. 2028년까지의 규정 준수 기간을 배경으로 유럽과 북미 전역의 사이리스터 시장을 뒷받침하는 단계적 개조 물결이 밀려오고 있습니다.

EV 인버터에서 SiC MOSFET을 통한 기존 제품 대체

주요 자동차 제조업체들은 인버터의 부피를 약 1/3로 줄이고 차량 주행거리를 약 6% 연장하는 SiC 디바이스로 전환하고 있으며, 400V 및 800V 시스템에서 기존 사이리스터 기반 보조기기를 대체하고 있습니다. 양산 규모 확대에 따라 SiC의 가격 프리미엄은 절연 게이트 바이폴라 트랜지스터(IGBT) 가격의 3배 이하로 축소되어 중급 모델 전환을 촉진하고 있습니다. 사이리스터 공급업체의 고주파 스위칭 능력이 부족하기 때문에 2025년에는 많은 브랜드에서 대당 탑재 금액이 6달러 이하로 떨어질 것으로 예측됩니다. 한때 성장의 주축이었던 자동차 부문의 매출은 현재 후퇴하고 있으며, 이는 모빌리티 부문의 사이리스터 시장의 상승 여력을 제한하고 있습니다.

부문 분석

2025년에는 사이리스터가 수요의 65.71%를 차지해, 전기 화학 처리, 모터 소프트 스타터, 자동차 발전기 레귤레이터의 저주파 위상 제어 정류기의 기초가 되었습니다. 이들 소자는 6,000-8,000V의 차단 용량과 정격 전류의 10배가 넘는 서지 내성을 갖추고 있으며, 대량 구매 시 15달러 이하로 판매되고 있어 가격에 민감한 산업용 틈새 시장에서 사이리스터 시장이 널리 보급되고 있습니다. 게이트 턴오프 사이리스터(GTO)는 모듈식 다단 컨버터 및 도시철도 업그레이드에서 보호 회로의 단순화를 위해 자가 정류 기능이 채택됨에 따라 2031년까지 연평균 복합 성장률(CAGR) 3.82%를 나타낼 것으로 예측됩니다. 이 부문의 성장은 중국의 고속철도 차량군에서 두드러지게 나타나고 있습니다. 새로운 컨버터가 진동과 온도 변동을 견딜 수 있지만, 고장 격리는 여전히 GTO에 의존하고 있습니다. 트라이액, 역전도형, 비대칭형은 주택용 디밍, 초퍼 구동 등 소규모 부문에 대응하고 있지만, 모두 핵심 SCR 수요 규모에는 미치지 못하는 상황입니다.

설계 채택 결정은 스위칭 속도와 암페어당 경제성 사이의 절충점을 반영합니다. 산업용 SCR의 사이리스터 시장 규모는 안정적이지만, 전력 밀도 및 라이드 스루가 더 빠른 턴오프가 필요한 부문에서는 GTO의 침투가 진행되고 있습니다. 양방향 트라이액 매출은 보합세를 보이고 있습니다. 이는 스마트홈 허브가 기존 조광기를 솔리드 스테이트 릴레이로 대체하고 있기 때문입니다. 다이오드와 사이리스터를 하나의 다이에 집적하여 인덕턴스를 감소시키는 역전도형은 초퍼 용도에서 점점 더 많은 관심을 받고 있습니다. 반면 비대칭형은 역방향 응력이 거의 발생하지 않는 HVDC(고압직류송전선로)에 대응하고 있습니다. 이 다섯 가지 디바이스 제품군을 모두 아우르는 공급업체는 교차 판매의 이점을 누리고 있으며, 이는 매출의 적절한 집중화에 기여하고 있습니다.

2025년에는 500MW 이하 용도가 45.83%의 점유율을 차지했으며, 중전압 드라이브, 지역 고정형 무효전력 보상장치(SVC), 배전 레벨 컨버터가 그 뒤를 이었습니다. 정격의 표준화로 설계가 효율화되어 설치 공간의 제약이 최종 전류 밀도보다 우선시되는 기존 설비의 업그레이드에 선호되고 있습니다. 1,000MW 이상의 설비는 수십억 달러 규모의 HVDC 회선이 해상풍력 발전소와 국경을 넘는 송전망을 연결하기 때문에 CAGR 3.97%를 나타낼 것으로 예측됩니다. 한국의 8GW 서해안 기간선로에는 약 1,600단의 고출력 장치가 적층되고, 각 단마다 여러 개의 프레스팩이 직렬로 연결될 예정이다(home.kepco.co.kr). 사우디의 750MW 알루미늄 정류기 단지와 같은 500-1,000MW 규모의 중규모 프로젝트는 자본 효율의 균형이 잘 잡혀 있고 고조파도 관리 가능한 수준입니다.

고출력 주문의 경우, 장치당 3-4kW의 방열을 견딜 수 있는 캡슐 패키징이 선호되며, 직접 수냉이 필요합니다. IEC 60747-9에 따른 인증은 18개월이 소요되기 때문에 사내에 검사 베이를 보유한 기존 제조업체는 진입장벽의 혜택을 받고 있습니다. 반면, 미쓰비시전기가 제공하는 차세대 8,500V 프레스팩 IGBT 모듈은 설치 면적이 작지만 40-50%의 비용 프리미엄이 있어 공간 제약이 있는 변전소에만 적용되고 있습니다. 따라서 기가 와트급 전력망이 증가함에 따라 메가 와트급 부문에서 사이리스터 시장 점유율은 꾸준히 확대되고 있습니다. 다만, 와이드밴드 갭 디바이스가 중형 부문에서 점차 점유율을 빼앗아가고 있는 점은 예외입니다.

지역별 분석

2025년에는 중국의 12GW HVDC 용량 증설과 인도의 6,400km에 달하는 철도 노선 전철화 등에 힘입어 아시아태평양이 45.48%의 점유율로 사이리스터 시장을 주도했습니다. 일본은 여전히 고전압 게이트 턴오프 스택을 필요로 하는 모듈형 다단변환기 하이브리드를 사용하여 섬 간 연결을 강화하고 있으며, 한국의 8GW 핵심 프로젝트가 수년간의 수주 잔고를 뒷받침하고 있습니다. 호주의 마리너스 링크(Marinus Link)는 VSC 기술을 도입하여 메가 와트당 장치 수를 줄이면서 건설은 2030년대 초까지 연장될 것으로 예측됩니다. 또한, 이 지역에는 세계 최대 규모의 개별 반도체 제조 클러스터가 존재하며, 중국 팹은 2025년에 드라이브, 가전제품, 트랙션용으로 4억 2,000만 개를 출하할 예정입니다.

중동은 2026-2031년 동안 CAGR 4.08%로 가장 높은 성장률을 보일 것으로 예측됩니다. 이는 사우디아라비아의 NEOM 메가 프로젝트가 4GW 분량의 전해조용 정류기를 발주하고 있으며, 1GW당 800-1,000개의 고전류 캡슐이 필요하기 때문이다(neom.com). 수다이르, 알 다흐라 등의 태양광 발전소에는 사이리스터 스위치드 커패시터 뱅크와 고정형 무효전력 보상장치(SVC)가 통합되어 있으며, 이를 합치면 900MVAr 이상의 무효전력 보상 용량을 가지고 있습니다. 바레인과 카타르의 알루미늄 제련소 개보수에는 수천 개의 고전류 장치가 소비되고 있으며, 2028년까지 최소 3개의 걸프 지역 전해조 프로젝트가 계획되어 있습니다. 따라서 이 지역 수요는 탄화수소 수입에 연동된 에너지 다변화 예산과 밀접한 관련이 있습니다.

북미와 유럽에서는 완만하게 확대되고 있습니다. 독일에서는 2026년부터 동적 무효전력 지원이 의무화됨에 따라 설비 개보수가 진행되고 있으며, 스페인에서는 1,800 MVAr의 STATCOM 도입으로 송전망에 즉각적인 효과를 입증하고 있습니다. 그러나 미국 전력회사의 게이트 턴오프 스택 인증 주기가 18개월을 초과할 수 있어 수익 인식이 지연될 수 있습니다. 남미에서는 북동부 풍력발전을 통합하는 브라질의 600 MVAr FACTS 계약이 중심이 되고 있습니다. 한편, 아프리카의 프로젝트 파이프라인은 남아공의 직렬 커패시터 회랑이 주도하고 있지만, 재정적 제약으로 인해 가동은 2027년 이후로 미뤄질 것으로 예측됩니다. 전반적으로, 세계 동향은 지역별 정책 및 프로젝트 자금 조달률이 사이리스터 시장 동향을 좌우하고 있음을 강조하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Thyristor market size was valued at USD 1.77 billion in 2025 and is estimated to grow from USD 1.95 billion in 2026 to reach USD 2.31 billion by 2031, at a CAGR of 3.45% during the forecast period (2026-2031).

Demand is steady because utilities still favor line-commutated valves for multi-gigawatt high-voltage direct current (HVDC) corridors, even as silicon-carbide metal-oxide-semiconductor field-effect transistors (SiC MOSFETs) win share in automotive and high-frequency industrial drives. Procurement cycles are shaped by large grid projects that lock in orders years ahead, while module integrators diversify toward intelligent power modules that embed gate drivers and sensors. Price competition is intensifying in low-and mid-power ratings as Chinese discrete suppliers offer stud and capsule devices at 20-30% lower average selling prices than European peers. At the same time, counterfeit risk and certification delays are raising the importance of traceability and vertically integrated manufacturing.

Global Thyristor Market Trends and Insights

Expansion of HVDC Links Integrating Offshore Wind in Asia

Mega-scale offshore wind corridors continue to anchor new +-800 kV lines across China, South Korea, and Australia, each requiring between 200-300 press-pack devices per gigawatt of capacity. China's Hami-Chongqing and Ningxia-Hunan lines alone add 16 GW of converter capacity that specifies thyristor valves for line-commutated stages. Korea's West Coast Energy Expressway, approved in 2024, locks in 1,600 high-power devices through 2028 . Australia's Marinus Link adopts a mixed valve approach that still reserves discrete high-voltage positions for thyristors [hitachienergy.com]. Project backlogs therefore extend into the early 2030s, sustaining the Thyristor market even as voltage-source converter (VSC) choices rise.

Grid-Code-Mandated Dynamic Reactive-Power Compensation in EU Utilities

Updated ENTSO-E guidance now obliges distribution operators to maintain power factor within +-0.95 during peak and off-peak windows. Germany's Federal Network Agency sets a January 2026 deadline for plants above 10 MW to install dynamic support, stimulating orders for thyristor-switched capacitor banks and static var compensators. Spain has already deployed 1,800 MVAr of static synchronous compensators equipped with 48-pulse valve assemblies. Italy awarded 900 MVAr of flexible alternating current transmission systems (FACTS) gear in 2024 to reduce renewable curtailment. Compliance windows to 2028 underpin a rolling retrofit wave that supports the Thyristor market across Europe and North America.

SiC MOSFET Cannibalization in EV Inverters

Leading automakers have migrated to SiC devices that shrink inverter volume by nearly one-third and raise vehicle range by about 6%, displacing legacy thyristor-based auxiliaries in 400-V and 800-V systems. Mass-production scale has reduced the SiC premium to less than triple insulated-gate bipolar transistor (IGBT) pricing, encouraging mid-tier models to switch. Thyristor vendors lack comparable high-frequency switching capability, so content per vehicle fell below USD 6 in 2025 for many brands. Automotive revenue, formerly a growth pillar, is now retreating, limiting the Thyristor market's upside in mobility segments.

Other drivers and restraints analyzed in the detailed report include:

- Modernization of Aluminum-Smelter Rectifiers in Gulf Cooperation Council Countries

- Fast-Charging Infrastructure for Two-Wheeler EVs in China and India Using SCR Stacks

- Counterfeit SCR Modules Causing OEM Recalls in Southeast Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicon-controlled rectifiers secured 65.71% of demand in 2025, anchoring low-frequency phase-controlled rectifiers across electro-chemical processing, motor soft-starters, and automotive alternator regulators. These devices combine 6,000-8,000 V blocking strength with surge tolerance above 10X rated current, while selling for under USD 15 in volume, which keeps the Thyristor market pervasive in price-sensitive industrial niches. Gate turn-off thyristors are forecast to log a 3.82% CAGR to 2031 as modular multilevel converters and urban rail upgrades adopt their self-commutating capability for simplified protection. The segment's growth is evident in China's high-speed train fleet, where new converters withstand vibration and temperature swings yet still rely on GTOs for fault isolation. Triacs, reverse-conducting, and asymmetric variants each address smaller pockets such as residential dimming or chopper drives, but none rival the scale of core SCR demand.

Design-in decisions reflect a trade-off between switching speed and per-ampere economics. The Thyristor market size for SCRs in industrial service remains stable, whereas GTO penetration rises where power density and ride-through dictate faster turn-off. Bidirectional triac sales stay flat because smart-home hubs replace legacy dimmers with solid-state relays. Reverse-conducting types gain in traction choppers, collapsing diode and thyristor into one die to cut inductance, while asymmetric parts meet HVDC poles that rarely see reverse stress. Suppliers that span all five device families capture cross-sell benefits, contributing to moderate revenue concentration.

Applications under 500 MW held 45.83% share in 2025, covering medium-voltage drives, regional static var compensators, and distribution-level converters. Standardized ratings streamline engineering, favorite for brownfield upgrades where footprint constraints override ultimate current density. Above 1,000 MW installations are forecast to grow at a 3.97% CAGR because multibillion-dollar HVDC corridors link offshore wind farms and cross-border grids. South Korea's 8 GW West Coast backbone will use about 1,600 stacked levels of high-power devices, each level series-connecting multiple press packs [home.kepco.co.kr]. Mid-tier 500-1,000 MW projects such as Saudi Arabia's 750 MW aluminum rectifier complex demonstrate balanced capital efficiency and manageable harmonics.

High-power orders favor capsule packages that tolerate 3-4 kW heat dissipation per device, necessitating direct liquid cooling. Certification under IEC 60747-9 can take 18 months, so incumbents with in-house test bays enjoy an access moat. Meanwhile, next-generation 8,500 V press-pack IGBT modules from Mitsubishi Electric offer smaller footprints, but their 40-50% cost premium limits adoption to space-constrained substations. The Thyristor market share in mega-watt segments therefore expands steadily as gigawatt-scale links multiply, even though wide-bandgap devices nibble at the mid-range.

The Thyristor Market Report is Segmented by Device Type (Silicon-Controlled Rectifier (SCR), and More), Power Rating (Below 500 MW, 500-1000 MW, and Above 1000 MW), Mounting and Package (Stud-Type, Capsule/Disc, and Module), Triggering Method (Electrical, Light, Pulse Transformer, and More), End-Use Industry (Industrial Drives and Motor Control, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the Thyristor market with 45.48% share in 2025, lifted by China's addition of 12 GW HVDC capacity and India's electrification of 6,400 route-kilometers of railway track. Japan is reinforcing inter-island links with modular multilevel converter hybrids that still need high-voltage gate turn-off stacks, and South Korea's 8 GW backbone project sustains a multiyear order book. Australia's Marinus Link introduces VSC technology, trimming devices per megawatt yet extending construction through the early 2030s. The region also houses the world's largest discrete manufacturing clusters, with Chinese fabs shipping 420 million units in 2025 for drives, appliances, and traction.

The Middle East is projected to post the fastest 4.08% CAGR during 2026-2031 as Saudi Arabia's NEOM mega-project orders rectifiers for 4 GW of electrolyzers, each gigawatt requiring 800-1,000 high-current capsules [neom.com]. Solar plants such as Sudair and Al Dhafra integrate thyristor-switched capacitor banks and static var compensators that together exceed 900 MVAr of reactive support. Aluminum smelter upgrades in Bahrain and Qatar consume thousands of high-current devices, and at least three Gulf potline projects are queued through 2028. Regional demand therefore ties closely to energy-diversification budgets linked to hydrocarbon revenue.

North America and Europe exhibit moderate expansion. Germany's mandate for dynamic reactive support effective 2026 is triggering retrofits, and Spain's 1,800 MVAr STATCOM rollout showcases immediate grid benefits. Certification cycles for gate turn-off stacks in U.S. utilities, however, may exceed 18 months, delaying revenue recognition. South America centers on Brazil's 600 MVAr FACTS contracts that integrate Northeastern wind, while Africa's pipeline is led by South Africa's series capacitor corridor, yet fiscal constraints push commissioning beyond 2027. Collectively, the global footprint underscores how region-specific policies and project financing rates govern the Thyristor market trajectory.

- Infineon Technologies AG

- Mitsubishi Electric Corp.

- ABB Ltd.

- STMicroelectronics N.V.

- Vishay Intertechnology Inc.

- Littelfuse Inc.

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Dynex Semiconductor Ltd.

- IXYS Corp. (Littelfuse)

- WeEn Semiconductors Co. Ltd.

- Shindengen Electric Mfg. Co. Ltd.

- Dongguan Yangjie Electronic Co.

- Jiangsu JieJie Microelectronics

- Sensata Technologies Inc.

- CRRC Zhuzhou Institute (CRRC CSI)

- Diodes Inc.

- Central Semiconductor Corp.

- GeneSiC Semiconductor (Navitas)

- Powerex Inc.

- Semikron Danfoss A/S

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-code-mandated Dynamic Reactive-Power Compensation in EU Utilities

- 4.2.2 Expansion of HVDC Links Integrating Offshore Wind in Asia

- 4.2.3 Fast-charging Infrastructure for 2-wheeler EVs in China and India using SCR Stacks

- 4.2.4 Modernization of Aluminum-smelter Rectifiers in Gulf Cooperation Council Countries

- 4.2.5 Surge in Solid-state Circuit Breakers for Rail Locomotives in India and Germany

- 4.2.6 Adoption of Radiation-hard Optically Triggered Thyristors in Avionics

- 4.3 Market Restraints

- 4.3.1 SiC MOSFET Cannibalization in EV Inverters

- 4.3.2 Counterfeit SCR Modules Causing OEM Recalls in Southeast Asia

- 4.3.3 Lengthy Certification Cycles for GTOs in United States Utilities

- 4.3.4 Volatile Polysilicon Pricing Inflating Discrete Thyristor Cost

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Device Type

- 5.1.1 Silicon-Controlled Rectifier (SCR)

- 5.1.2 Gate Turn-Off Thyristor (GTO)

- 5.1.3 Bidirectional Triac

- 5.1.4 Reverse Conducting Thyristor

- 5.1.5 Asymmetric Thyristor (ASCR)

- 5.2 By Power Rating

- 5.2.1 Less than 500 MW

- 5.2.2 500 - 1 000 MW

- 5.2.3 Above 1 000 MW

- 5.3 By Mounting and Package

- 5.3.1 Stud-Type

- 5.3.2 Capsule / Disc

- 5.3.3 SMD and Clip-mount

- 5.3.4 Module (Intelligent Power Module, Hybrid)

- 5.4 By Triggering Method

- 5.4.1 Electrical Gate Triggered

- 5.4.2 Light Triggered (LTT)

- 5.4.3 Pulse Transformer Triggered

- 5.5 By End-use Industry

- 5.5.1 Industrial Drives and Motor Control

- 5.5.2 HVDC and FACTS (SVC, STATCOM)

- 5.5.3 Renewable Power Conversion (Solar, Wind)

- 5.5.4 Transportation (Rail Traction, Marine)

- 5.5.5 Automotive (On-board Chargers, EV Powertrain)

- 5.5.6 Consumer Electronics and Appliances

- 5.5.7 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 ABB Ltd.

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Vishay Intertechnology Inc.

- 6.4.6 Littelfuse Inc.

- 6.4.7 ON Semiconductor Corp.

- 6.4.8 Renesas Electronics Corp.

- 6.4.9 Dynex Semiconductor Ltd.

- 6.4.10 IXYS Corp. (Littelfuse)

- 6.4.11 WeEn Semiconductors Co. Ltd.

- 6.4.12 Shindengen Electric Mfg. Co. Ltd.

- 6.4.13 Dongguan Yangjie Electronic Co.

- 6.4.14 Jiangsu JieJie Microelectronics

- 6.4.15 Sensata Technologies Inc.

- 6.4.16 CRRC Zhuzhou Institute (CRRC CSI)

- 6.4.17 Diodes Inc.

- 6.4.18 Central Semiconductor Corp.

- 6.4.19 GeneSiC Semiconductor (Navitas)

- 6.4.20 Powerex Inc.

- 6.4.21 Semikron Danfoss A/S

- 6.4.22 Fuji Electric Co., Ltd.

- 6.4.23 Toshiba Electronic Devices & Storage Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment