|

시장보고서

상품코드

2044249

프랑스의 접착제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)France Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

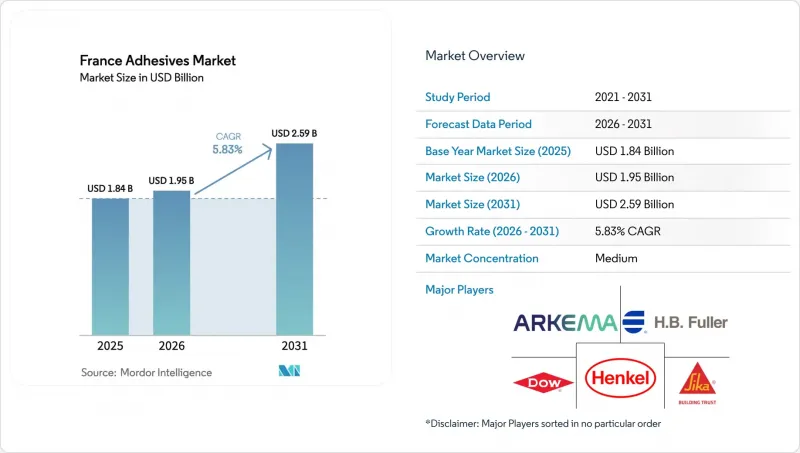

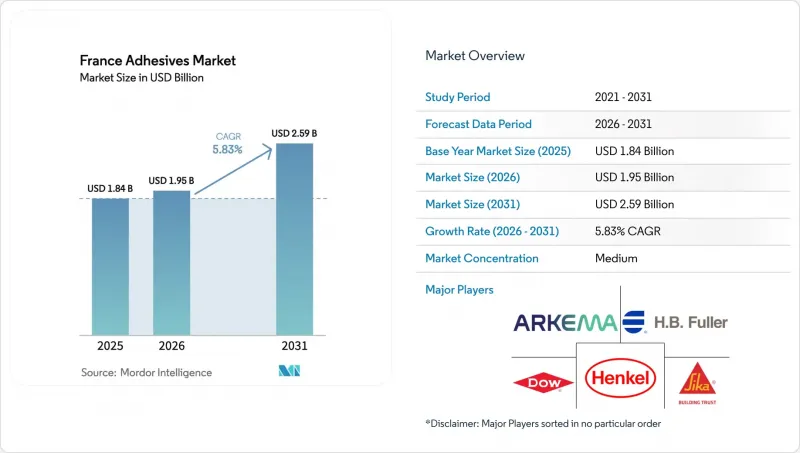

프랑스의 접착제 시장 규모는 2025년에 18억 4,000만 달러, 2026년에 19억 5,000만 달러되어, 2031년까지 25억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.83%로 성장할 전망입니다.

프랑스의 접착제 시장은 개보수 중심의 건설 수요 회복에 힘입어 60년 만에 최저치를 기록한 국내 자동차 생산의 타격을 완화하는 동시에 REACH 및 RE2020 규제 요건을 준수하는 수성 및 바이오 화학제품으로의 대체가 가속화되고 있습니다. 중국 내 322억 유로 규모의 에너지 개조 프로젝트에서 단열 테이프, 타일용 접착제, 구조용 유리 실란트에 대한 수요가 가장 견조하지만, 원자재 가격 상승과 이산화티타늄 가격이 2020년 이전보다 70% 더 높은 수준이기 때문에 수익률은 여전히 어려운 상황입니다. 동시에 전기자동차(EV) 조립 라인에서는 경량화와 배터리 주행거리 연장을 위해 고성능 에폭시 및 폴리우레탄 접착제에 대한 수요가 증가하고 있으며, 평균적인 EV의 경우 배터리 팩과 모터의 접합부에는 이미 약 8파운드의 접착제 및 실란트가 사용되고 있습니다. 사용되고 있습니다. 세계 전략 기업들의 볼트온 방식의 인수합병이 진행되면서 경쟁은 더욱 치열해지고 있습니다. Arkema는 2024년 12월 Dow의 포장용 라미네이트 사업을 인수했고, 헨켈은 2026년 1월 ATP 인수에 합의했습니다. 이를 통해 저 VOC 제품 포트폴리오를 확보하고, 리노베이션 프로젝트에 보다 깊이 있게 진입하고자 합니다.

프랑스 접착제 시장 동향 및 인사이트

개보수 및 에너지 절약형 건설 수요

'MaPrimeRenov'&'를 중심으로 한 에너지 절약 개보수 인센티브로 2023년에는 50만 5,126건의 프로젝트에 19억 5,000만 유로가 지급되어 2020년부터 2024년 중반까지 누적 322억 유로 규모의 공사가 창출되었습니다. 이로 인해 저 VOC 실란트, 밀폐 테이프, 바이오 패널용 접착제에 대한 수요가 지속적으로 증가하고 있습니다. RE2020에 따른 매립 탄소 상한선은 2022년 640kg CO2e/m2에서 2031년까지 415kg CO2e/m2로 강화되고 있으며, 이에 따라 배합 제조업체는 UF 수지 및 페놀 수지를 바이오 대체품으로 전환해야 합니다. 160mm 미네랄 울을 사용한 연속 단열 시스템, 조립식 CLT 벽 및 방습 막은 모두 우수한 동결-융해 안정성과 낮은 배출 특성을 가진 접착제에 의존합니다. Certificats d'&Economies d'Energie(에너지 절약 인증서)를 통한 자금 지원은 2024년 41억 5,000만 유로에 달하고, 개보수 공사에 더욱 박차를 가하고 있습니다. 공장에서 생산된 부재는 이미 현장에서의 폐기물을 약 30% 절감하고 있으며, 조립라인의 가동을 유지하는 속경화형 패널 접착제에 대한 수요를 높이고 있습니다.

자동차 경량화 및 EV 조립에 대한 요구

전기자동차(EV) 프로그램에서는 하중을 분산시키고, 이종 금속과 복합재료를 접착하고, 180-250°C의 도장 소성 사이클을 견딜 수 있는 구조용 에폭시 및 폴리우레탄 접착제가 필수적입니다. 스텔란티스는 2030년까지 배터리 무게를 절반으로 줄이기 위해 토리노의 배터리 기술 센터에 4,000만 달러 이상을 투자했습니다. 이 목표는 부서지기 쉬운 금속 간 화합물 발생을 방지하는 접착제로 리벳과 용접을 대체하는 것과 직결되어 있습니다. 접착제와 리벳을 결합한 하이브리드 접합은 배터리 하우징에서 박리 저항과 기밀성을 동시에 만족시키는 새로운 표준이 되고 있습니다. 2024년 프랑스의 자동차 생산량은 지난 60년 동안 최저 수준으로 떨어졌지만, 장기적인 EV로의 전환으로 생산량은 회복될 것으로 예측됩니다. 2024년 4.5% 감소한 자동차 트림 및 내장재 접착제의 단기적인 침체는 예측 기간 동안 프랑스 접착제 시장을 주도할 준비가 되어 있는 고부가가치 배터리용도의 구조적인 상승 추세를 가리고 있습니다.

이소시아네이트 및 용매에 대한 REACH 규제 강화

2023년 8월 24일부터 유리 디이소시아네이트 함량이 0.1%를 초과하는 폴리우레탄계 접착제를 산업용으로 사용하는 경우, 인증된 작업자에 대한 교육, 문서화 및 정기적인 업데이트가 의무화됩니다. 소규모 컨버터는 생산 라인을 개조하거나 '저배출' 등급으로 배합을 변경하기 위해 불균형적인 컴플라이언스 비용을 부담하고 있습니다. 배합 변경에는 1년이 걸리는 경우가 많아 제품 출시가 늦어지고, 연구개발 예산이 묶이게 됩니다. 이 규정은 구조용, 바닥재용 및 연포장용 부문에서 MDI, TDI, HDI, IPDI를 대상으로 합니다. ECHA는 연간 3,000건의 천식 환자 감소를 예상하고 있지만, 규제 면제 블렌드가 보급될 때까지 단기적인 혼란으로 인해 프랑스 접착제 시장의 물량 성장은 억제될 것으로 보입니다.

부문 분석

수성 플랫폼은 VOC 규제 준수와 타일용 접착제 및 종이 라미네이트의 시멘트계 기판과의 호환성으로 인해 2025년에도 프랑스 접착제 시장에서 가장 큰 44.68%의 점유율을 유지할 것으로 예측됩니다. 핫멜트 시스템은 포장 라인이 클램핑 시간과 에너지 소비를 줄이는 속경화성 및 감압성 접착제 등급에 대한 투자를 늘리면서 CAGR 6.74%로 성장하여 프랑스 접착제 시장에서 점유율을 확대할 것으로 예측됩니다. 초저단량체 폴리우레탄계 핫멜트는 경화 지연 없이 0.1%의 이소시아네이트 임계치를 충족하기 때문에 유연성 식품 포장 분야에서 수요가 증가하고 있습니다. 범용 제품 분야에서는 수성 아크릴계 접착제가 E0 배출 기준이 적용되는 제본, 라벨 부착, 내장용 목재 패널 등의 용도를 커버하고 있습니다. 반응성 에폭시 및 폴리우레탄은 구조용 틈새 시장, EV 배터리 팩, 풍력 터빈 블레이드, 항공기 내장재 등에 사용되며, 20-35MPa의 중첩 전단 강도는 프리미엄 가격을 정당화합니다.

핫멜트 공급업체는 장비 OEM 제조업체와의 수직적 통합을 강화하고 있으며, 이를 통해 컨버터가 분당 400미터 이상의 라인 속도로 작동할 수 있도록 하고 있습니다. 이는 주문형 생산 셀을 업그레이드하는 EC용 골판지 공장에 매우 중요합니다. 수성 수지 배합 제조업체들은 점도의 급격한 상승 없이 고형분율을 65%까지 높이는 고형분 분산 기술에 투자하고 있으며, 이를 통해 도포량의 경제성을 향상시키고 있습니다. UV 경화형은 틈새 시장이지만, 전자기기 및 의료기기 분야에서 두 자릿수 성장을 기록하고 있으며, 1초 이내 경화로 열 응력을 피할 수 있다는 점이 높이 평가받고 있습니다. 컨버터 업체들이 신발 및 가구 생산 라인에서 톨루엔계 캐리어를 단계적으로 폐지함에 따라 솔벤트계 접착제의 사용량은 지속적으로 감소하는 추세입니다. 이러한 기술적 변화와 함께 경기 순환에 따른 변동은 있지만, 프랑스 접착제 시장의 중기적 회복을 뒷받침하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The France Adhesives Market size is projected to be USD 1.84 billion in 2025, USD 1.95 billion in 2026, and reach USD 2.59 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031. The France adhesives market is riding a renovation-led construction rebound, accelerating substitution toward water-borne and bio-based chemistries that comply with REACH and RE2020 mandates while buffering the hit from a 60-year low in domestic vehicle production. Volume growth is strongest in thermal-insulation tapes, tile adhesives, and structural glazing sealants used in the nation's EUR 32.2 billion energy-retrofit pipeline, yet raw-material inflation and titanium-dioxide costs remain 70% higher than pre-2020, keeping margins tight. At the same time, electric-vehicle (EV) assembly lines are pulling demand toward high-performance epoxy and polyurethane bonds that cut weight and extend battery range, with an average EV already using nearly 8 lb of adhesives and sealants in its battery pack and motor interfaces. Competitive intensity is rising as global strategics execute bolt-on deals. Arkema bought Dow's packaging-lamination line in December 2024, and Henkel signed to acquire ATP in January 2026, to lock in low-VOC portfolios and deeper access to renovation projects.

France Adhesives Market Trends and Insights

Renovation and Energy-Efficiency Construction Demand

Energy-retrofit incentives, led by MaPrimeRenov', disbursed EUR 1.95 billion to 505,126 projects in 2023 and generated EUR 32.2 billion of cumulative works between 2020 and mid-2024, driving sustained pull for low-VOC sealants, airtightness tapes, and bio-based panel adhesives. Embodied-carbon caps under RE2020 are tightening from 640 kg CO2e/m2 in 2022 to 415 kg CO2e/m2 by 2031, pushing formulators to swap UF and phenolic resins for bio-sourced alternatives. Continuous-insulation systems using 160 mm mineral wool, prefabricated CLT walls, and vapor-barrier membranes all rely on adhesives with superior freeze-thaw stability and low emissions. Funding from Certificats d'Economies d'Energie hit EUR 4.15 billion in 2024, further accelerating retrofit activity. Factory-built elements already cut on-site waste by roughly 30%, increasing demand for fast-curing panel bonds that keep assembly lines moving.

Automotive Lightweighting and EV Assembly Needs

Electric-vehicle programs depend on structural epoxy and polyurethane adhesives that distribute loads, bond dissimilar metals to composites, and survive 180-250°C paint-bake cycles. Stellantis invested over USD 40 million in a Turin battery technology center aiming to halve battery weight by 2030, a goal linked directly to replacing rivets and welds with adhesives that avoid brittle intermetallics. Hybrid joints, adhesive plus rivet, are becoming the new norm in battery housings, providing peel resistance plus sealing. Although France's vehicle output slumped to a six-decade low in 2024, the long-run shift to EVs is expected to restore volume. Short-run softness in automotive trim and interior adhesives, down 4.5% in 2024, masks a structural upswing in high-value battery applications primed to lift the France Adhesives market over the forecast horizon.

REACH Tightening on Isocyanates and Solvents

Since August 24, 2023, industrial use of polyurethane adhesives with more than 0.1% free diisocyanate requires certified worker training, documentation, and periodic renewals. Small converters shoulder disproportionate compliance costs as they retrofit lines or reformulate into "micro-emission" grades. Reformulations often span a full year, delaying product launches and tying up research and development budgets. The rule covers MDI, TDI, HDI, and IPDI across structural, flooring, and flexible-packaging segments. Although ECHA forecasts 3,000 fewer asthma cases annually, near-term disruption clips volume growth in the France Adhesives market until exempt blends gain scale.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Water-Borne/Low-VOC Systems

- EU Green-Taxonomy Incentives for Bio-Based Formulas

- Escalating Compliance Cost for SME Converters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne platforms retained the largest 44.68% France adhesives market share in 2025 due to their compliance with VOC legislation and compatibility with cementitious substrates in tile adhesives and paper lamination. Hot-melt systems are forecast to expand at a 6.74% CAGR, lifting their slice of the France Adhesives market size as packaging lines invest in fast-setting, pressure-sensitive grades that reduce clamp time and energy use. Demand for ultra-low-monomer polyurethane hot melts is rising in flexible food packaging because they meet 0.1% isocyanate thresholds without curing delays. On the commodity end, water-borne acrylics cover bookbinding, labeling, and interior wood panels where E0 emissions rules apply. Reactive epoxies and polyurethanes occupy structural niches, EV battery packs, wind turbine blades, and aircraft interiors, where lap-shear strengths of 20-35 MPa justify premium pricing.

Hot-melt suppliers are deepening vertical ties with equipment OEMs so converters can run at line speeds above 400 m/min, critical for e-commerce corrugated plants upgrading box-on-demand cells. Water-borne formulators invest in high-solid dispersion tech that boosts solids to 65% without viscosity spikes, improving coat-weight economics. UV-cured volumes, though niche, post double-digit growth in electronics and medical devices where sub-second cure avoids thermal stress. Solvent-borne usage continues to shrink as converters phase out toluene carriers in shoe and furniture lines. Combined, technology shifts underpin medium-term upswing in the France adhesives market despite cyclical bumps.

The France Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- Bolton Adhesives

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

- ADERIS Specialities

- ITW Performance Polymers

- Wacker Chemie AG

- BASF SE

- Dymax Corporation

- Parker Hannifin Corp

- KLEIBERIT SE & CO. KG

- RAMSA France

- Pidilite Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation and energy-efficiency construction demand

- 4.2.2 Automotive lightweighting and EV assembly needs

- 4.2.3 Rising demand for water-borne/low-VOC systems

- 4.2.4 EU green-taxonomy incentives for bio-based formulas

- 4.2.5 Paris-2024 retrofits and heritage-building restorations

- 4.3 Market Restraints

- 4.3.1 REACH tightening on isocyanates and solvents

- 4.3.2 Escalating compliance cost for SME converters

- 4.3.3 Laser-welding substitution in selected auto parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Bolton Adhesives

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Sika AG

- 6.4.11 ADERIS Specialities

- 6.4.12 ITW Performance Polymers

- 6.4.13 Wacker Chemie AG

- 6.4.14 BASF SE

- 6.4.15 Dymax Corporation

- 6.4.16 Parker Hannifin Corp

- 6.4.17 KLEIBERIT SE & CO. KG

- 6.4.18 RAMSA France

- 6.4.19 Pidilite Industries Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment