|

시장보고서

상품코드

2044254

독일의 접착제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

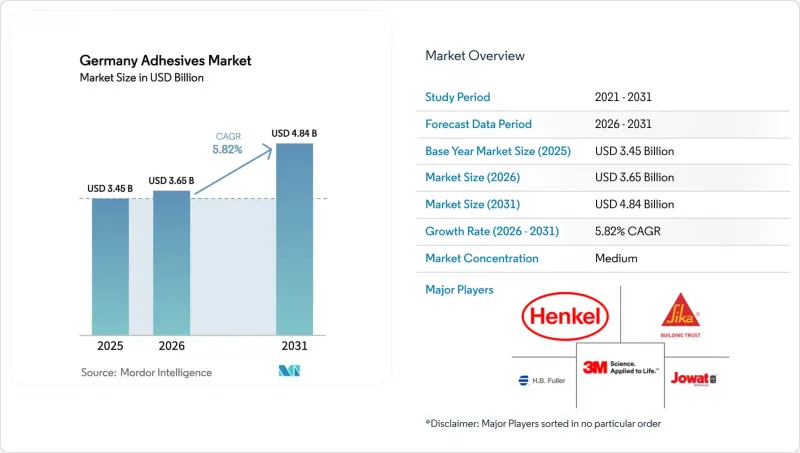

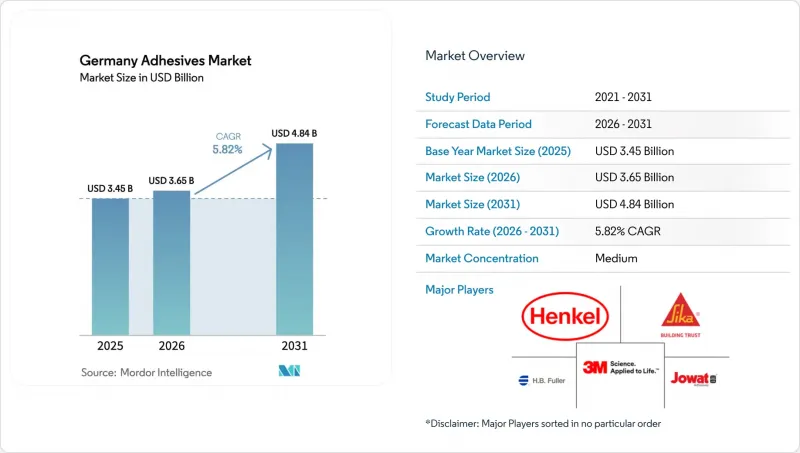

독일의 접착제 시장 규모는 2025년 34억 5,000만 달러에서 2026년에는 36억 5,000만 달러로 확대되어 2031년까지 48억 4,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.82%를 나타낼 것으로 예측됩니다. 이러한 성장은 리노베이션 중심의 건설 수요, 전기자동차 생산량 증가, 컨버터에 저 VOC 및 박리성 화학물질로의 전환을 의무화하는 포장 규제 개혁에 기인합니다. 국내 배합업체들은 에너지 가격이 미국의 2-3배 수준에 머물러 있고, 누적 규제비용이 부가가치의 13%에 육박하는 등 국내 시장 수익률을 압박하고 있어 수출에 힘을 쏟고 있습니다. 수성 기술은 2026년 중반 EU에서 도입될 VOC 규제 상한선을 배경으로 우위를 유지하고 있지만, 자동화 및 바이오화 노력이 가속화됨에 따라 핫멜트도 탄력을 받고 있습니다. 한편, 세계 기업들은 대형 인수를 통해 특수 분야에서의 입지를 굳히고 있으며, 중소기업(SME)은 맞춤형과 서비스 강화를 통해 지역별 틈새 시장을 지키고 있는 상황입니다.

독일 접착제 시장 동향과 인사이트

건설 부문의 리노베이션 붐

1990년 이전에 지어진 건물이 2030년까지 연방정부의 배출량 55% 감축 목표를 달성하기 위해 다층 단열, 창문 기밀화, 외벽 클래딩이 필요하기 때문에 에너지 절약형 개보수가 수요의 대부분을 차지하고 있습니다. 2024년 건설용 접착제 출하량은 15.4% 증가했지만, 목재 및 종이의 최종 시장은 축소되었습니다. 이는 개보수 프로젝트에서 평방미터당 접착제 사용량이 증가한 것을 반영합니다. VINNAPAS VAE 파우더 등의 배합으로 동결융해 내구성을 손상시키지 않으면서 클링커 함량이 적은 CEM II 타일 시스템을 가능하게 합니다. 숙련공 부족으로 인해 시공이 지연되고, 특히 정밀한 파사드 접착의 경우 비용이 상승하여 프로젝트 실행에 대한 리스크가 여전히 남아 있습니다.

유연성과 재활용성이 뛰어난 포장으로의 전환

개정된 포장법(VerpackDG)에 따라 2029년까지 플라스틱 포장재의 90% 재활용이 의무화되어, 생산자책임재활용제도(EPR)에 따른 벌칙을 피하기 위해 단일 소재 필름과 박리 가능한 접착제의 채택이 촉진되고 있습니다. 폴리에틸렌 및 폴리프로필렌 구조물에는 용제 배출을 없애고 기계적 재활용이 가능하기 때문에 수성 및 핫멜트 시스템이 선호됩니다. 2025년 4월에 출시된 헨켈의 워시오프 라벨은 병에서 병까지의 루프에서 PET 플레이크의 품질을 유지하며, 고객 검증 기간이 6개월에 불과해 시장 보급을 가속화하고 있습니다.

용제에 대한 엄격한 VOC 및 REACH 규제

EU는 2026년 인테리어 제품의 VOC 허용 함량을 30g/L로 낮추고, 작업장 내 포름알데히드 노출 한계치를 0.3ppm으로 설정했습니다. 이로 인해 중소기업들은 배합 변경 및 설비 교체에 200만-500만 유로를 지출해야 하는 실정입니다. 전환 기간 동안 이중 재고는 운전 자금을 압박하는 반면, 항공우주 분야와 고온 환경에서의 자동차 접착 분야에서 수성 화학제품은 여전히 성능 측면에서 문제가 남아있습니다.

부문 분석

2025년 독일 접착제 시장에서 수성 시스템은 41.15%의 점유율을 차지했습니다. 이는 실내 배출량을 30g/L로 제한하는 EU의 VOC 규제를 배경으로 목공, 포장, 건설 분야의 사용자들이 저용제 옵션으로 전환한 것이 주요 원인으로 분석됩니다. 독일 접착제 시장에서 수성 시스템의 우위는 성숙한 생산 인프라와 VOC 함량 1g/L 이하, 바이오 원료 함유량 최대 50% 등 VAE 공중합체의 성능 향상을 반영하고 있습니다. 그러나 포장 라인에서 속효성 점착성이 요구됨에 따라 핫멜트는 2031년까지 연평균 복합 성장률(CAGR) 6.67%로 가장 높은 성장률을 보이고 있으며, BioRUHM의 바이오 반응성 등급은 골판지를 넘어 자동차의 목재 및 금속 구조물까지 적용 범위를 넓혀가고 있습니다.

용제계 제품의 생산량은 계속 줄어들고 있지만, 수계 시스템이 수분 흡수, 느린 경화 또는 고온 안정성 등의 이유로 수계 시스템을 채택할 수 없는 분야, 특히 항공우주 항공기 내장재에서 여전히 중요한 역할을 하고 있습니다. 반응성 화학물질(에폭시, 폴리우레탄, 시아노아크릴레이트)은 항공우주용 복합재료, 의료기기, 전자기기의 기반이 되며, 높은 중첩 전단강도와 정밀한 경화 프로파일을 통해 높은 수익률을 보장합니다. UV 경화형 및 하이브리드 반응성 핫멜트는 즉각적인 핸들링과 최종 가교가 융합되어 카테고리의 경계를 재정의하고 독일 접착제 시장의 경쟁력을 강화할 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Germany Adhesives Market size is projected to grow from USD 3.45 billion in 2025 to USD 3.65 billion in 2026, and reach USD 4.84 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031. Growth stems from renovation-led construction demand, rising electric-vehicle output, and packaging reforms that oblige converters to switch to low-VOC and debondable chemistries. Domestic formulators sharpen export focus because energy prices remain two to three times U.S. levels and cumulative regulation costs approach 13% of value-added, eroding home-market margins. Water-borne technology maintains a lead on the back of EU mid-2026 VOC caps, while hot melts gain traction as automation and bio-based initiatives accelerate. Meanwhile, global players consolidate specialty niches through large acquisitions, leaving small and medium-sized enterprises (SMEs) to defend regional pockets through customization and service intensity.

Germany Adhesives Market Trends and Insights

Construction-Sector Renovation Boom

Energy-efficiency retrofits dominate demand as pre-1990 structures require multilayer insulation, window sealing, and facade cladding to meet the federal 55% emissions-reduction target by 2030. Construction adhesives volume rose 15.4% in 2024 while wood and paper end-markets shrank, reflecting higher adhesive intensity per square meter in renovation projects. Formulations such as VINNAPAS VAE powders enable lower-clinker CEM II tile systems without sacrificing freeze-thaw durability. Project execution risk remains as skilled-labor shortages delay installations and lift costs, particularly for precision facade bonding.

Shift Toward Flexible and Recyclable Packaging

The amended Packaging Act (VerpackDG) forces 90% recyclability of plastic packs by 2029, incentivizing mono-material films and debondable adhesives to avoid extended producer responsibility penalties. Water-borne and hot-melt systems are preferred for polyethylene and polypropylene structures because they remove solvent emissions and allow mechanical recycling. Henkel's wash-off labels, launched in April 2025, preserve PET flake quality during bottle-to-bottle loops and require only six months of customer validation, accelerating market uptake.

Stringent VOC and REACH Regulations on Solvents

The EU slashed allowable VOC content to 30 g/L for interior products in 2026 and imposed workplace formaldehyde exposure limits of 0.3 ppm, forcing SMEs to spend EUR 2-5 million on reformulation and equipment upgrades. Dual inventories during the transition squeeze working capital, while water-borne chemistries still face performance gaps in aerospace and high-temperature automotive bonding.

Other drivers and restraints analyzed in the detailed report include:

- Thermal-Conductive Adhesives for EV Battery Cells

- Bio-Based Adhesives Backed by German Bioeconomy Strategy

- Specialty-Polymer Supply-Chain Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems captured 41.15% of Germany adhesives market share in 2025 on the strength of EU VOC limits that cap interior emissions at 30 g/L, steering woodworking, packaging, and construction users toward low-solvent options. Their dominance in Germany adhesives market size reflects mature production infrastructure and improved VAE copolymer performance, including less than or equal to 1 g/L VOC content and up to 50% bio input. Yet hot melts post the fastest 6.67% CAGR to 2031 as packaging lines demand instant tack, and BioRUHM's bio-reactive grades broaden application reach beyond cartons into automotive wood-metal structures.

Solvent-borne volumes continue to shrink but retain critical roles where water uptake, slow cure, or high-temperature stability preclude aqueous systems, particularly in aerospace interiors. Reactive chemistries - epoxies, polyurethanes, cyanoacrylates - anchor aerospace composites, medical devices, and electronics, commanding premium margins because of high lap-shear strength and precise cure profiles. UV-cure and hybrid reactive hot melts blend instant handling with final cross-linking, a convergence likely to redefine category boundaries and sharpen Germany adhesives market competitiveness.

The Germany Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and Other End-User Industries). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- ITW Performance Polymers

- Jowat SE

- Klebchemie M.G. Becker GmbH & Co. KG

- Lohmann GmbH & Co. KG

- Permabond

- Rampf Holding GmbH & Co. KG

- Sika AG

- Wacker Chemie AG

- Wevo-Chemie GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction-sector renovation boom

- 4.2.2 Shift toward flexible and recyclable packaging

- 4.2.3 Healthcare and medical-device bonding growth

- 4.2.4 Bio-based adhesives backed by German Bioeconomy Strategy

- 4.2.5 Thermal-conductive adhesives for EV battery cells

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and REACH regulations on solvents

- 4.3.2 Specialty-polymer supply-chain disruptions

- 4.3.3 Skilled-labor gap in precision adhesive application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hexion Inc.

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 Klebchemie M.G. Becker GmbH & Co. KG

- 6.4.13 Lohmann GmbH & Co. KG

- 6.4.14 Permabond

- 6.4.15 Rampf Holding GmbH & Co. KG

- 6.4.16 Sika AG

- 6.4.17 Wacker Chemie AG

- 6.4.18 Wevo-Chemie GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment