|

시장보고서

상품코드

2044279

자수기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Embroidery Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

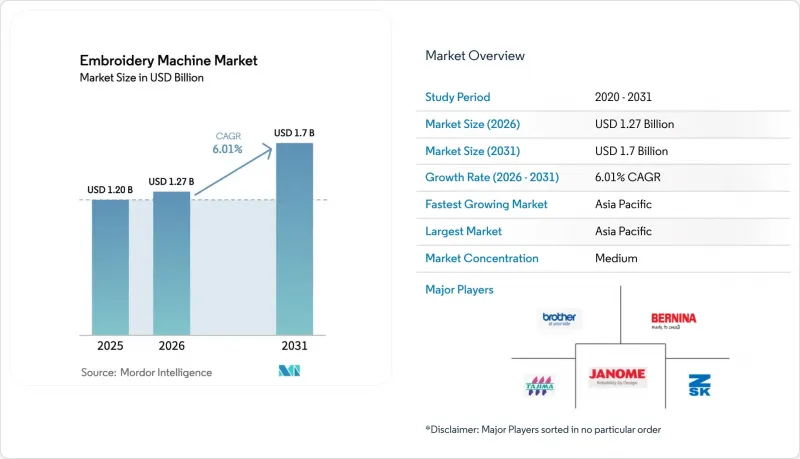

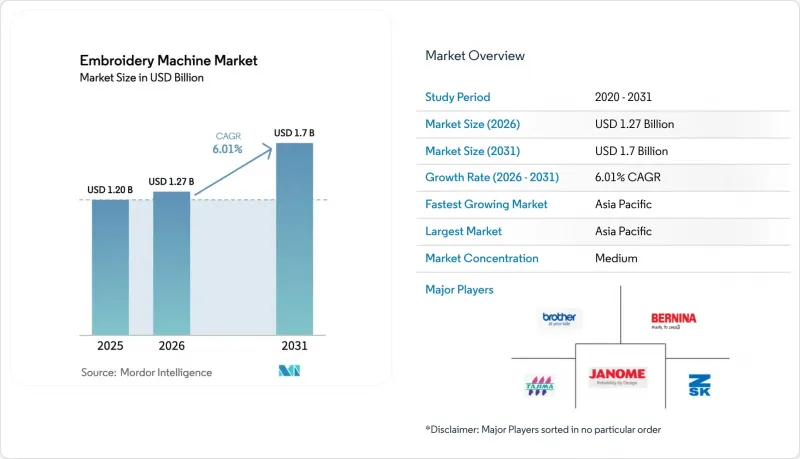

자수기 시장 규모는 2025년 12억 달러에서 2026년에는 12억 7,000만 달러로 확대되어 2030년까지 17억 달러에 이를 것으로 예상되고 있어 2026년부터 2030년까지 CAGR 6.01%로 성장할 전망입니다.

생성형 AI를 통한 자동 디지털화로 디자인 리드타임이 단축되고, EU의 탄소 관세 규정으로 인해 데코레이터들이 스크린 인쇄에서 실을 이용한 로고로 전환하고, IIoT를 활용한 가동률 보장으로 자동화 투자 회수 기간이 단축됨에 따라 고처리량 멀티헤드 시스템과 이동성이 높은 싱글헤드 유닛에 대한 수요가 증가할 것으로 예측됩니다. 고처리량 멀티헤드 시스템과 이동성이 높은 싱글헤드 유닛 모두에 대한 수요가 예상됩니다. 북미의 팬 상품 사업자는 새로운 NIL(Name, Image, and Likeness: 이름, 초상, 초상화) 비즈니스 기회를 수익화하기 위해 10바늘 재봉틀을 선택했고, 아시아태평양의 위탁 생산 공장에서는 사람의 감시 없이 야간에도 재봉틀을 가동하는 무인화 공장을 도입하고 있습니다. 일본과 한국에서는 IE4/IE5 서보 모터를 대상으로 한 정부의 환경대응기기 보조금으로 운영비용이 절감되고 있으며, OEM 업체들은 중소기업의 컨트롤러 노후화에 대한 우려를 해소하기 위해 지속적으로 업데이트되는 펌웨어를 세트로 제공하는 경우가 늘고 있습니다. 이러한 요인들이 결합되어 자수기 시장은 의류 시장의 경기 변동에 영향을 덜 받는 균형 잡힌 수요 구조를 형성하고 있습니다.

세계 자수기 시장 동향과 인사이트

생성형 AI를 통한 자동 디지털화로 DTC 브랜드 디자인 시간 단축

생성형 AI 모델은 고객의 아트워크를 몇 분 만에 최적화된 스티치 파일로 변환할 수 있어 소규모 의류 제조업체의 병목 현상이었던 2-4시간의 수작업 워크플로우를 대체할 수 있게 되었습니다. 초기 현장 데이터에 따르면, 디자인 매칭 정확도는 87%, 수정 작업은 최대 30% 감소하여 DTC(Direct-to-Consumer) 판매자의 차별화 요소인 '주문에서 배송까지 48시간'이라는 약속을 뒷받침하고 있습니다. 빠른 디자인 반복을 통해 브랜드는 추가 비용 없이 개인화를 통합할 수 있으며, 평균 주문 금액을 약 5분의 1로 늘릴 수 있습니다. 소프트웨어가 구독 모델로 전환됨에 따라 OEM은 지속적인 수익을 얻고 알고리즘을 지속적으로 개선하여 가격으로 인한 고객 이탈을 방지하는 '클라우드의 해자'를 구축하고 있습니다. 단기적인 구매 고려자들에게 AI를 통한 디지털화는 스티치 수와 필드 크기를 뛰어넘어 구매 기준의 상위 3위를 차지했습니다.

인도 전자상거래: 실시간 개인화 기능으로 단품 배송이 급증하는 인도 전자상거래

인도 마켓플레이스에서는 구매자가 사진을 업로드하고 결제 전 모형을 생성할 수 있는 실시간 미리보기 엔진을 도입했습니다. 이로 인해 로트 단위의 경제성이 무너지고, 1점 단위의 유연성이 필수적이 되었습니다. 자수 제품을 12%의 세율로 분류하는 GST(물품용역세) 혜택으로 스크린 인쇄 제품에 비해 수익률이 확대되어 영세 사업자가 9개월 이내에 손익분기점에 도달할 수 있게 되었습니다. 2025년 내내 5,000달러 미만의 단품 수입이 급증하여 자수기 시장에서 가장 빠르게 확대되었습니다. 힌디어, 타밀어, 벵골어로의 소프트웨어 현지화를 통해 도입 장벽을 더욱 낮췄으며, 2급 도시의 당일 배송 네트워크를 통해 24시간 이내에 원사 및 안정제를 공급하고 있습니다. 초기 도입자들은 하루 20-25건의 주문 제작 주문을 보고하고 있으며, 이는 이 부문의 현금 흐름의 합리성을 증명하고 있습니다.

하이브리드 DTF 프린터, APAC 지역의 판촉용 자수 시장을 잠식하다!

직접 투 필름(DTF) 소모품 비용이 감소함에 따라 APAC의 판촉물 공급업체들은 생산량의 약 1/3을 하이브리드 프린터로 전환하고 있습니다. 하이브리드 프린터는 로고 1개당 0.65달러로 풀컬러 그래픽을 전사할 수 있는 반면, 자수 실의 경우 1.80달러가 소요됩니다. 특히 모자, 토트백, 회의용 기념품 등 촉감이 중요하지 않은 분야, 특히 손맛을 중요시하지 않는 분야에서는 소규모의 엔트리 레벨 자수점은 점유율을 지키기 힘들어지고 있습니다. 이에 반해 기계 제조업체들은 한 번의 패스로 자수와 인쇄를 동시에 할 수 있는 콤보 헤드를 도입하고 있지만, 가격이 비싸서 보급은 이제 막 시작 단계입니다. 중기적으로는 더 이상의 점유율 하락을 막기 위해 자수는 고부가가치 제품이나 테크니컬 아이템에 대한 프리미엄 마감으로 재포지셔닝할 필요가 있습니다.

부문 분석

2025년 매출에서 차지하는 비중은 미미하지만, 단일 헤드 기계는 전체 제품 카테고리 중 가장 높은 성장률을 나타낼 것으로 예상되며, CAGR은 8.25%를 나타낼 것으로 예측됩니다. 마이크로 배치 생산의 경제성에서 5분 미만의 셋업 시간은 단발 주문에서 멀티헤드 머신에 불리한 유휴 시간을 제거하여 단발 주문에 유리하게 작용합니다. 하루에 20개의 작업을 처리하는 싱글 헤드 머신은 3개의 장시간 생산에 묶여 있는 6헤드 머신보다 더 높은 ROA(총자산수익률)를 창출하는 경우가 많습니다. 브라더의 PR1055X에 탑재된 카메라 가이드식 정렬 기능은 재료 손실을 최대 15%까지 줄일 수 있습니다. 500대 주문 생산에서 멀티헤드 플랫폼은 여전히 필수적이기 때문에 자수기 시장은 생산량의 양 극단에서 효율성의 균형을 유지하고 있습니다.

셔닐과 스팽글 재봉틀은 여전히 틈새 시장이지만, 촉감으로 차별화를 추구하는 대학 재킷과 고급 섬유 생산업체를 끌어들이고 있습니다. 레이저 아플리케 하이브리드 기계는 혼합 미디어 기술로 인해 30%의 가격 프리미엄이 정당화되는 맞춤형 장식 분야를 차지하고 있습니다. 따라서 제품의 다양성은 OEM 제조업체가 패션의 주기성에 대한 리스크 헤지를 가능하게 하고, 개별 부문 수요 변동에도 불구하고 자수기 산업의 안정화에 기여하고 있습니다.

2025년 매출 중 전자동 설비가 64.65%를 차지하고 있으며, 컴퓨터 비전 센서와 AI 경로 계획 기능으로 다운타임이 감소함에 따라 그 비중은 더욱 확대될 것으로 예측됩니다. 중국의 무인 공장에서는 심야 교대 근무 시 분당 최대 1,000 스티치까지 무인 가동이 이루어지고 있으며, 처리 능력의 향상을 입증하고 있습니다. 2,500달러의 개조 키트를 사용하면 반자동 라인을 부분 자동화로 전환할 수 있으며, 비용에 민감한 구매자에게는 일시적인 해결책이 될 수 있습니다. 수동 기계는 인간의 불완전함이 최종 사용자에게 장인의 고급스러움을 보여주는 오뜨 꾸뛰르 아틀리에에서 계속 사용되고 있습니다.

방글라데시와 같이 인건비가 저렴한 시장에서는 반자동 기계가 합리적이지만, 노동 임금이 시간당 평균 10 달러 이상인 지역에서는 컴퓨터 제어 라인이 주류를 이루고 있습니다. 자동화를 통한 비용 절감 효과는 매년 누적되기 때문에 컴퓨터 제어기 출하량은 연간 7.75%의 성장률을 보일 것으로 예측되며, 이는 자수기 시장 전체 규모 확대를 상회할 것으로 전망됩니다.

지역별 분석

아시아태평양은 2025년 매출의 62.55%를 차지해, 중국의 18만대 도입과 인도의 싱글 헤드 머신 붐에 힘입어 CAGR 7.45%를 나타낼 것으로 예측됩니다. 광동성, 절강성, 장쑤성 클러스터에서는 공급업체가 같은 지역에 밀집해 있는 것을 활용해 납기를 72시간으로 단축하고 있습니다. 2024년 이후 IIoT 보급률이 급증하고 OEE가 13% 포인트 향상됨에 따라 구매자는 센서 지원 기기로의 표준화를 결정했습니다. 인도는 상황이 다릅니다. 실시간 개인화 기능을 통해 소량 주문을 즉시 배송으로 전환할 수 있기 때문에 국내 판매의 55% 이상을 단일 헤드 머신이 차지하고 있습니다. 일본과 한국에서는 IE4 모터에 대한 정부 보조금으로 인해 신규 도입보다 기존 기기의 교체가 가속화되고 있습니다. 한편, 호주는 여전히 틈새 시장으로 스포츠 용품 커스터마이징에 중점을 두고 있습니다.

북미에서는 NIL(National Identity League)이 주도하는 고등학교 굿즈가 성장을 견인하고 있습니다. 텍사스와 캘리포니아 주에서만 2025년 미국 수요의 약 40%를 차지했습니다. 캐나다에서는 주로 난연성 로고가 지정된 자원 부문용 유니폼이 판매되고 있습니다. 멕시코의 마킬라도라(수출가공지구)는 USMCA(미국-멕시코-캐나다 협정)의 관세 특혜 혜택을 받고 있으며, 수익률은 낮지만 자수 제품을 미국 소매점 진열대에 더 가깝게 가져가는 데 성공했습니다.

유럽은 여전히 양극화되어 있습니다. 서유럽에서는 CBAM(탄소국경조정조치) 준수를 배경으로 갱신 수요가 추구되고 있으며, 기업용 유니폼 공급업체에게 다두식 재봉틀의 업그레이드는 매력적인 선택이 되고 있습니다. 동유럽에서는 EU에 대한 관세 면제 혜택을 활용해 저임금 노동력을 바탕으로 순 생산능력을 확대되고 있습니다. 남부 지역은 의류 소비 침체로 어려움을 겪고 있으며, 기계의 수명주기가 최대 10년까지 연장되고 있습니다. 북유럽의 바이어들은 안전복용 반사 원사를 필요로 하고 있으며, 이는 작지만 안정적인 틈새 시장입니다. 중동의 성장은 신규 호텔용 고급 린넨에 집중되어 있는 반면, 아프리카 시장 침투율은 남아공과 나이지리아를 제외하고는 여전히 낮은 수준에 머물러 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Embroidery Machine Market size is expected to increase from USD 1.20 billion in 2025 to USD 1.27 billion in 2026 and reach USD 1.7 billion by 2030, growing at a CAGR of 6.01% over 2026-2030.

Generative-AI auto-digitizing compresses design lead-times, EU carbon-tariff rules redirect decorators from screen-printing to thread-based logos, and IIoT-enabled uptime guarantees shorten automation payback periods, so both high-throughput multi-head systems and agile single-head units find addressable demand. North American fan-merch operators choose 10-needle machines to monetize new Name, Image, and Likeness (NIL) opportunities, while Asia-Pacific contract factories deploy lights-out floors that keep stitchers running overnight without human supervision. Government green-equipment rebates covering IE4/IE5 servo motors lower operating costs in Japan and South Korea, and OEMs increasingly bundle evergreen firmware to ease small-business fears of controller obsolescence. Collectively, these forces provide a balanced demand mix that insulates the embroidery machine market from cyclical apparel swings.

Global Embroidery Machine Market Trends and Insights

Generative-AI Auto-Digitizing Cuts Design Time for Custom DTC Brands

Generative models now translate customer artwork into optimized stitch files in minutes, replacing the 2-4-hour manual workflow that once bottlenecked small apparel houses. Early field data show 87% design-match accuracy and up to 30% lower rework, which supports the 48-hour order-to-ship promises that differentiate direct-to-consumer sellers. Rapid design iteration also lets brands bundle personalization without charging a premium, lifting average order value by roughly one-fifth. As software moves to subscription models, OEMs collect recurring revenue and continuously improve algorithms, adding a cloud moat that discourages price-based churn. Near-term buyers cite AI digitizing as a top three purchase criterion, overtaking needle count and field size.

Indian E-Commerce Real-Time Personalization Spikes Single-Head Shipments

Indian marketplaces introduced real-time preview engines that let shoppers upload photos and generate mock-ups before checkout, collapsing batching economics and making single-head flexibility indispensable. GST incentives that classify embroidery at a 12% tax rate widen the margin compared with screen-printed goods, allowing micro-entrepreneurs to break even in under nine months. Unit imports priced below USD 5,000 surged throughout 2025, representing the fastest expansion in the embroidery machine market. Software localization in Hindi, Tamil, and Bengali further lowers adoption barriers, while same-day courier networks in Tier 2 cities supply threads and stabilizers within 24 hours. Early adopters report daily volumes of 20 to 25 bespoke orders, proving the cash-flow logic for the segment.

Hybrid DTF Printers Cannibalize Promo-Product Embroidery in APAC

As Direct-to-Film consumable costs drop, APAC promo suppliers shift roughly one-third of volume to hybrid printers that transfer full-color graphics at USD 0.65 per logo versus USD 1.80 for thread. Entry-level embroidery shops lacking scale struggle to defend share where tactile quality is less valued, particularly on caps, totes, and conference giveaways. Machine makers respond by introducing combo heads that embroider and print in one pass, but adoption is nascent due to higher ticket prices. Over the medium horizon, embroidery must reposition as a premium finish for high-value or technical items to avoid further share erosion.

Other drivers and restraints analyzed in the detailed report include:

- EU CBAM Carbon Tariffs Shift Decorators from Screen-Print to Thread Logos

- IIoT Predictive Maintenance Lowers Downtime in Chinese Contract Factories

- EU Apparel Spending Slowdown Delays Capex Refresh Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Despite accounting for only a small fraction of 2025's revenue, single-head machines are projected to achieve the highest growth rate among all product classes, with an anticipated CAGR of 8.25%. Micro-batch economics favor their sub-5-minute setup times, eliminating the idle windows that penalize multi-head gear on one-off orders. A single-head unit processing 20 daily jobs often yields higher ROA than a 6-head station locked into three long runs. Brother's PR1055X camera-guided alignment feature trims material waste by up to 15%. Multi-head platforms remain indispensable for 500-unit contract runs, so the embroidery machine market balances efficiency at both volume extremes.

Chenille and sequin machines remain niche, enticing varsity-jacket and luxury-textile producers seeking tactile differentiation. Laser applique hybrids occupy bespoke decor where mixed-media techniques can justify 30% price premiums. Product diversity therefore enables OEMs to hedge against fashion cyclicality, helping stabilize the embroidery machine industry despite demand swings in any single segment.

Fully automatic equipment owned 64.65% of the 2025 turnover and should widen its share as computer-vision sensors and AI path planners shave downtime. Lights-out Chinese floors run unattended graveyard shifts at up to 1,000 stitches per minute, proving the throughput upside. Retrofit kits costing USD 2,500 convert semi-automatic lines to partial autonomy, a stopgap for cost-sensitive buyers. Manual machines continue in haute-couture ateliers where human imperfection signals artisanal luxury to end consumers.

Semi-automatic gear makes sense in wage-advantaged markets such as Bangladesh, while computerized lines dominate regions where labor averages USD 10/hour or more. Because automation savings compound each year, computerized shipments are projected to grow 7.75% annually, outstripping the broader embroidery machine market size expansion.

The Embroidery Machine Market Report is Segmented by Product (Single-Head Embroidery Machines, and More), by Technology (Manual Embroidery Machines and More), by Application (Apparel & Garments and More), by End-User (Home/Personal Use (Residential / Hobbyist) and More), by Distribution Channel (Offline and More), and by Geography (Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 62.55% of 2025 turnover and should grow at a 7.45% CAGR, led by China's 180,000-unit installed base and India's single-head boom. Guangdong, Zhejiang, and Jiangsu clusters exploit co-located suppliers that shrink turnaround to 72 hours. IIoT penetration rose sharply post-2024, with OEE gains of 13 percentage points convincing buyers to standardize on sensor-ready machines. India differs: real-time personalization converts small orders into immediate dispatch, so single-head share tops 55% of domestic sales. Government rebates on IE4 motors in Japan and South Korea accelerate replacement rather than incremental units, while Australia remains niche, focused on sports customization.

North America relies on NIL-driven high-school merch to sustain growth. Texas and California alone captured nearly 40% of 2025 U.S. demand; Canada sells mainly into resource-sector uniforms that specify flame-resistant logos. Mexico's maquiladoras enjoy USMCA tariff relief that pulls embroidery closer to U.S. retail shelves, albeit at lower margins.

Europe remains bifurcated. Western Europe pursues replacement anchored to CBAM compliance, making multi-head upgrades attractive for corporate-uniform suppliers. Eastern Europe expands net capacity, leveraging lower labor aboard EU duty-free access. Southern regions struggle with soft apparel spend, lengthening machine life cycles to as much as 10 years. Nordic buyers need reflective thread for safety wear, a small but steady niche. Middle East growth centers on luxury linens for new hotels, whereas Africa's penetration stays low outside South Africa and Nigeria.

- Brother Industries Ltd.

- Bernina International AG

- Janome Sewing Machine Co. Ltd.

- Tajima Industries Ltd.

- ZSK Stickmaschinen GmbH

- Ricoma International Corp.

- Melco International

- PFAFF Industriesysteme und Maschinen GmbH

- Singer Sewing Company

- SWF (SunStar Co. Ltd.)

- Barudan Co. Ltd.

- HappyJapan Inc.

- JUKI Corporation

- Zhejiang Lejia Embroidery Machine Co.

- Shanghai Feiyue Group Co.

- Aresse International Corp.

- BAI Embroidery Machine (Shenzhen)

- Mitsubishi Electric Machine Tool Div.

- Suntech Machinery (China)

- Mobase Sunstar (China)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Generative-AI auto-digitising cuts design time for custom DTC brands (NA, EU)

- 4.2.2 EU CBAM carbon tariffs shift decorators from screen-print to thread logos

- 4.2.3 Indian e-commerce real-time personalisation spikes single-head shipments

- 4.2.4 IIoT predictive-maintenance lowers downtime in Chinese contract factories

- 4.2.5 Government green-equipment rebates for high-efficiency servo motors (JP, KR)

- 4.2.6 US NIL expansion to high-school sports boosts fan-merch 10-needle demand

- 4.3 Market Restraints

- 4.3.1 EU apparel spending slowdown delays cap-ex refresh cycles

- 4.3.2 Hybrid DTF printers cannibalise promo-product embroidery in APAC

- 4.3.3 Skilled-operator shortage persists across NA & EU despite upskilling grants

- 4.3.4 Rapid controller-software obsolescence raises perceived investment risk for SMEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (Eco-design & Machinery Directive amendments, EU 2028)

- 4.6 Technological Outlook (AI stitch-optimisation, smart hoops, hybrid print-plus-embroidery heads)

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Product

- 5.1.1 Single-Head Embroidery Machines

- 5.1.2 Multi-Head Embroidery Machines

- 5.1.3 Chenille Embroidery Machines

- 5.1.4 Others (Sequin, Laser, Cap/Flat, etc.)

- 5.2 By Technology

- 5.2.1 Manual Embroidery Machines

- 5.2.2 Semi-Automatic Machines

- 5.2.3 Fully Automatic/Computerized Machines

- 5.3 By Application

- 5.3.1 Apparel & Garments

- 5.3.2 Home Textiles

- 5.3.3 Technical Textiles (Auto, Medical, Aero)

- 5.3.4 Others (Fashion Accessories, Corporate Branding & Uniforms, Promotional Products, etc,)

- 5.4 By End-User

- 5.4.1 Home/Personal Use (Residential / Hobbyist)

- 5.4.2 Commercial/Small Business Use (less than 10 machines)

- 5.4.3 Industrial Use (>=10 machines)

- 5.4.4 Others (vocational training, Fashion/ design schools)

- 5.5 By Distribution Channel

- 5.5.1 Offline (Direct, Dealers, Specialty, Big-Box)

- 5.5.2 Online (OEM Direct, E-commerce)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Peru

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Qatar

- 5.6.5.4 Kuwait

- 5.6.5.5 Turkey

- 5.6.5.6 Egypt

- 5.6.5.7 South Africa

- 5.6.5.8 Nigeria

- 5.6.5.9 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Brother Industries Ltd.

- 6.4.2 Bernina International AG

- 6.4.3 Janome Sewing Machine Co. Ltd.

- 6.4.4 Tajima Industries Ltd.

- 6.4.5 ZSK Stickmaschinen GmbH

- 6.4.6 Ricoma International Corp.

- 6.4.7 Melco International

- 6.4.8 PFAFF Industriesysteme und Maschinen GmbH

- 6.4.9 Singer Sewing Company

- 6.4.10 SWF (SunStar Co. Ltd.)

- 6.4.11 Barudan Co. Ltd.

- 6.4.12 HappyJapan Inc.

- 6.4.13 JUKI Corporation

- 6.4.14 Zhejiang Lejia Embroidery Machine Co.

- 6.4.15 Shanghai Feiyue Group Co.

- 6.4.16 Aresse International Corp.

- 6.4.17 BAI Embroidery Machine (Shenzhen)

- 6.4.18 Mitsubishi Electric Machine Tool Div.

- 6.4.19 Suntech Machinery (China)

- 6.4.20 Mobase Sunstar (China)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment