|

시장보고서

상품코드

2044284

영국의 MLCC 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)United Kingdom MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

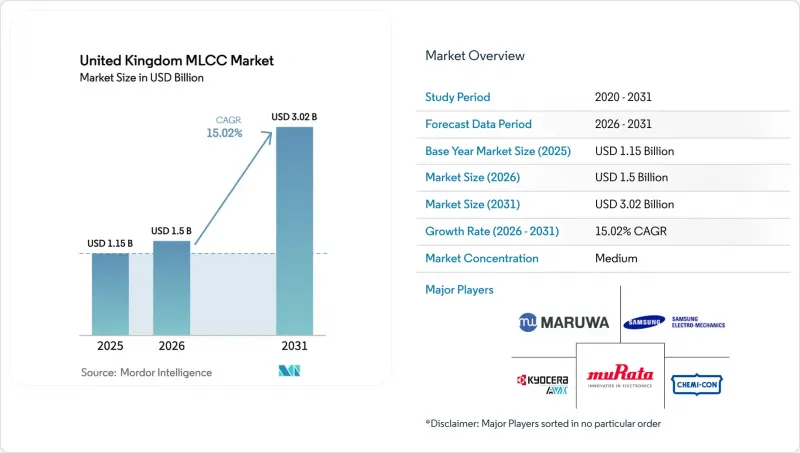

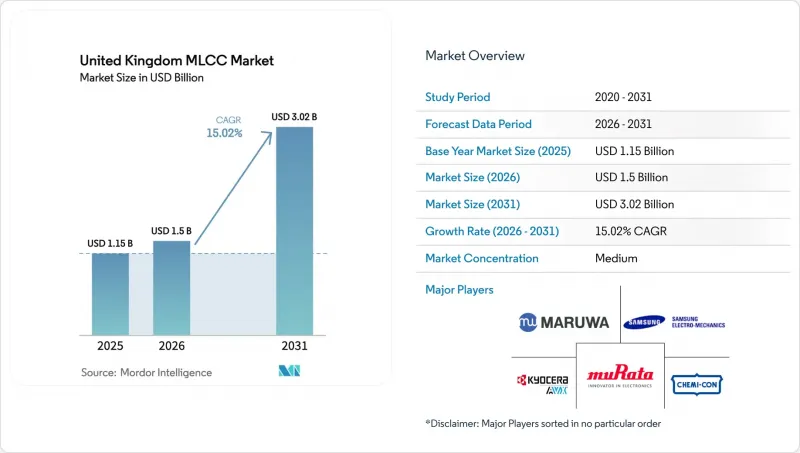

영국의 MLCC 시장 규모는 2025년에 11억 5,000만 달러로 평가되었고 2026년 15억 달러에서 2031년까지 30억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 15.02%를 나타낼 전망입니다.

무공해 자동차에 대한 강력한 정책적 지원, 프보고서 지역 내 유리한 감가상각 규정, AUKUS의 방산 전자장비 현지 조달이 맞물려 국내 수요를 활성화하고 있습니다. 그러나 세계 공급 능력의 압박으로 인해 평균 판매 가격은 계속 상승하고 있으며, 구매자는 이중 소싱 및 완충 재고 전략으로 전환하고 있습니다. 이에 대해 현지 유통업체들은 할당 리스크를 억제하기 위해 자동차 및 의료 거점과 가까운 곳에 보세 재고를 확대하는 방식으로 대응하고 있습니다. 동시에 800V 자동차 플랫폼, 소형화된 의료용 임플란트, 고주파 5G 무선으로의 전환으로 제품 구성은 고전압, 초고안정성, 초소형 커패시터로 전환되고 있습니다.

영국 MLCC 시장 동향과 인사이트

2030년 영국 내연기관(ICE) 금지에 대비한 전기차 생산량 급증

영국 자동차 제조업체들은 2030년 내연기관차(ICE) 금지 조치에 대응하기 위해 전기차(EV) 생산을 확대하고 있으며, 대당 커패시터 탑재량은 약 3배로 증가하고 있습니다. 서머셋의 타타(Tata)와 선덜랜드의 AESC의 기가팩토리 투자는 현지 배터리 및 파워일렉트로닉스 생태계를 뒷받침하는 기반이 되고 있으며, 영국 MLCC 시장 인증 작업을 주도하고 있습니다. 25억 파운드 규모의 'DRIVE35' 프로그램에는 파워 일렉트로닉스 공급망에 대한 설비 투자로 26억 달러가 할당되어 있어, 정책의 견인력이 지속될 것임을 시사하고 있습니다. 전기차 한 대당 약 1만 개의 커패시터가 탑재되어 있으며, 800V 아키텍처로의 설계 전환으로 인해 내전압 요구사항이 더욱 높아졌습니다. 현지 유통업체들은 현재 아시아로부터공급 부족으로 인한 영향을 피하기 위해 웨스트미들랜즈 지역의 OEM 기지 근처에 보세 재고를 확보해두고 있습니다. 이러한 움직임은 영국 MLCC 시장의 성장 전망에 더욱 힘을 실어주고 있습니다.

5G의 빠른 확산으로 스몰셀 수요 증가

통신사업자들은 수천 개의 스몰셀 기지국을 사용하여 5G 네트워크의 밀도를 높이고 있으며, 각 기지국에는 고주파 바이패스 기능을 위해 수십 개의 0201 및 0402 커패시터가 탑재되어 있습니다. Ofcom의 'Connected Nations' 데이터는 런던, 맨체스터, 버밍엄의 도시 지역 커버리지가 빠르게 확대되고 있음을 보여줍니다. Murata Manufacturing의 커패시터 매출은 2025년 상반기 전년 동기 대비 9% 증가했는데, 이는 통신 부문으로부터의 수주에 기인한 것입니다. 전력 밀도가 증가함에 따라 설계자들은 바이어스 하에서도 정전 용량이 안정된 X7R 및 X5R 유전체를 선호하고 있으며, 고급 재료 노하우를 가진 공급업체를 선호하고 있습니다. 따라서 이러한 통신망 확충은 영국 MLCC 시장에 더욱 큰 호재로 작용하고 있습니다.

MLCC 수급 불균형 지속, 리드 타임 장기화

인공지능(AI) 서버 수요로 인해 Murata Manufacturing의 세계 가동률이 95%에 육박하고 있으며, 버퍼 재고가 고갈되고 있습니다. 할당 위험으로 인해 영국 바이어들은 계약 기간이 길어지거나 현물 시장에서 할증된 가격을 지불해야 하는 상황에 처했습니다. 추적성이 요구되는 자동차 및 국방 관련 프로그램이 가장 큰 영향을 받고 있습니다. 일부 Tier 1 공급업체는 현재 폴리머 하이브리드 커패시터와 필름 커패시터를 듀얼 소스로 채택하고 있지만, 재인증 비용이 높아서 대체 움직임이 억제되고 있습니다.

부문 분석

2025년 영국 MLCC 시장 점유율의 45.72%는 클래스2 구성이 차지해, 그 중심은 고용량 X7R과 X5R 등급입니다. 그 우월성은 민수용 및 산업용 기판에서 디커플링 및 에너지 저장 용도에 적합한 체적 효율에서 비롯됩니다. 그러나 자동차용 인버터, 레이더 모듈, 임베디드 디바이스에서 노화가 거의 없고 공차가 엄격한 제품이 선호됨에 따라 클래스 1 C0G 및 NP0 부품은 2031년까지 연평균 복합 성장률(CAGR) 15.42%로 확대될 것으로 예측됩니다. 따라서 정밀 타이밍 및 센싱 회로용 영국 MLCC 시장은 클래스 1 기술로 전환하고 있습니다.

공급업체들은 TDK의 3225 형태 10nF, 1,250V C0G 등 고전압 클래스 1 제품 라인업을 확대되고 있습니다. 자동차 엔지니어는 배터리 관리의 정확성을 보장하기 위해 바이어스 하에서 안정적인 정전 용량을 중요시하는 반면, 의료기기 제조업체는 수십년동안 온도 불변성을 필요로 합니다. 이러한 특성으로 인해 클래스 1 부품은 마이크로패럿당 비용이 높은 경우에도 설계 채택을 획득할 수 있으며, 영국 MLCC 시장에서 예측 우위를 강화하고 있습니다.

2025년 기준, 402 사이즈가 영국 MLCC 시장 점유율의 37.29%를 차지하고 있으며, 이는 픽앤플레이스 수율과 정전 용량 여유의 균형을 반영합니다. 그러나 5G 무선기와 혈당 패치에서 기판 면적의 제약으로 인해 201 형태는 CAGR 15.83%로 성장하고 있습니다. TDK의 1608 케이스 커패시터와 같이 100V에서 10배의 커패시턴스 향상을 실현하는 등 기술적 진보를 통해 설계자는 더 작은 실장 면적에서 동일한 커패시턴스를 확보할 수 있게 되었습니다.

로직이 칩렛 패키징으로 전환됨에 따라 수동 부품의 배치 면적은 더욱 줄어들고, 더 작은 형태에 대한 수요가 증가하고 있습니다. 영국 MLCC 시장에서 201 및 01005 사이즈 수요는 의료용 웨어러블 기기 및 통신용 스몰셀 부문에서 가장 빠르게 증가할 것으로 예측됩니다. 한편, 자동차 파워 일렉트로닉스 기판에서는 리플 전류에 대응하기 위해 여전히 1210 사이즈 이상의 부품이 사용되고 있습니다. 이러한 양극화된 수요로 인해 공급업체는 다양한 케이스 사이즈의 제품 라인업을 갖추는 것이 필수적입니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The United Kingdom MLCC market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.50 billion in 2026 to reach USD 3.02 billion by 2031, at a CAGR of 15.02% during the forecast period (2026-2031).

Solid policy support for zero-emission vehicles, favorable capital-allowance rules inside Freeport zones, and defense-electronics localisation under AUKUS together energize local demand. Tight global capacity, however, continues to lift average selling prices, nudging buyers toward dual-sourcing and buffer-stock strategies. Local distributors are responding by expanding bonded inventory close to automotive and medical hubs to limit allocation risk. At the same time, the pivot to 800-volt vehicle platforms, miniaturised medical implants, and high-frequency 5G radios is tilting the product mix toward high-voltage, ultra-stable, and ultra-small capacitors.

United Kingdom MLCC Market Trends and Insights

Surge in EV Manufacturing Ahead of the 2030 UK ICE Ban

United Kingdom vehicle makers are scaling up electric-vehicle output to meet the 2030 ban on internal-combustion engines, lifting per-car capacitor content roughly threefold. Gigafactory investments by Tata in Somerset and AESC in Sunderland anchor local battery and power-electronics ecosystems, pulling qualification work into the United Kingdom MLCC market. The GBP 2.5 billion DRIVE35 program earmarks USD 2.6 billion for capital expenditure on power-electronics supply chains, signaling continued policy pull. Each electric vehicle contains about 10,000 capacitors, and design migration to 800-volt architectures further raises voltage-rating requirements. Local distributors now maintain bonded stock near West Midlands OEM sites to avoid Asian allocation shocks. These moves jointly amplify the growth outlook of the United Kingdom MLCC market.

Accelerated 5G Roll-Out Boosting Small-Cell Demand

Telecom operators are densifying 5G networks with thousands of small-cell base stations, each loaded with dozens of 0201 and 0402 capacitors for high-frequency bypass functions. Ofcom's Connected Nations data confirms rapid urban coverage expansion in London, Manchester, and Birmingham. Murata's capacitor revenue rose 9% year on year in the first half of fiscal 2025, driven partly by telecommunications orders. As power density climbs, designers prefer X7R and X5R dielectrics with stable capacitance under bias, and they favor suppliers with advanced material know-how. This telecom build-out therefore feeds an incremental tailwind into the United Kingdom MLCC market.

Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

Artificial-intelligence server demand has pushed Murata's global utilisation towards 95%, draining buffer inventory. Allocation risk forces UK buyers to accept longer contract horizons or pay premiums on the spot market. Automotive and defense programs that need traceable lots face the greatest exposure. Some tier-1s now dual-source with polymer hybrids or film capacitors, but re-qualification costs remain high, tempering substitution.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Compact Medical Wearables and Implantables

- Government Tax Incentives for On-Shore Passive-Component Production

- Nickel and Copper Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 2 compositions held 45.72% of the United Kingdom MLCC market share in 2025, anchored by high-capacitance X7R and X5R grades. Their dominance comes from volumetric efficiency that suits decoupling and energy-storage tasks across consumer and industrial boards. However, Class 1 C0G and NP0 parts are projected to expand at a 15.42% CAGR through 2031 as automotive inverters, radar modules, and implantables prioritize near-zero aging and tight tolerance. The United Kingdom MLCC market for precision timing and sensing circuits is therefore tilting toward Class 1 technology.

Suppliers are widening high-voltage Class 1 offerings, such as TDK's 10 nF, 1,250 V C0G in 3225 format. Automotive engineers value stable capacitance under bias for battery-management accuracy, while medical device makers need temperature-invariant behavior over decades. These attributes let Class 1 parts capture design wins even where their cost per microfarad is higher, reinforcing their forecast outperformance in the United Kingdom MLCC market.

The 402 size accounted for 37.29% of the United Kingdom MLCC market share in 2025, reflecting its balance of pick-and-place yield and capacitance headroom. Yet board-area scarcity in 5G radios and glucose patches is driving a 15.83% CAGR for the 201 format. Designers can now achieve the same capacitance in fewer footprints due to breakthroughs such as TDK's 1608 case capacitors with tenfold capacitance gains at 100 V.

As more logic shifts to chiplet packages, the passive placement area shrinks further, raising demand for smaller formats. The United Kingdom MLCC market size allocated to 201 and even 01005 footprints will likely rise fastest in medical wearables and telecom small cells. In contrast, power-electronics boards in vehicles still rely on 1210 or larger parts for ripple-current handling. This dual-track demand keeps a broad case-size portfolio essential for suppliers.

The United Kingdom MLCC Market Report is Segmented by Dielectric Type (Class 1 and Class 2), Case Size (201, 402, 603, 1005, 1210, and Other Case Sizes), Voltage (Low Voltage, Mid Voltage, and High Voltage), MLCC Mounting Type (Metal Cap, Radial Lead, and Surface Mount), End-User Application (Aerospace and Defence, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kyocera AVX Components Corporation

- MARUWA Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Samwha Capacitor Co., Ltd.

- TAIYO YUDEN Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Worth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Industry Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- KEMET Corporation

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Exxelia Group

- Knowles Precision Devices

- NIC Components Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Manufacturing Ahead of 2030 UK ICE-Ban

- 4.2.2 Accelerated 5G Infrastructure Roll-Out Boosting Small-Cell Demand

- 4.2.3 Rising Demand for Compact Medical Wearables and Implantables

- 4.2.4 Government Tax Incentives for On-Shore Passive Component Production

- 4.2.5 Battery Management-System Design Shifts to Higher Capacitance

- 4.2.6 Defence Electronics Localisation under AUKUS and UK MoD Initiatives

- 4.3 Market Restraints

- 4.3.1 Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

- 4.3.2 Nickel and Copper Price Volatility Squeezing Margins

- 4.3.3 Regulatory Hurdles for New Fab Construction (Planning and ESG)

- 4.3.4 Growing Substitution by Embedded Capacitors in HDI PCBs

- 4.4 Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 0201

- 5.2.2 0402

- 5.2.3 0603

- 5.2.4 1005

- 5.2.5 1210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage

- 5.3.1 Low Voltage (Less Than or Equal to 100 V)

- 5.3.2 Mid Voltage (100-500 V)

- 5.3.3 High Voltage (Greater Than500 V)

- 5.4 By MLCC Mounting Type

- 5.4.1 Metal Cap

- 5.4.2 Radial Lead

- 5.4.3 Surface Mount

- 5.5 By End-User Application

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunication

- 5.5.8 Other End-User Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kyocera AVX Components Corporation

- 6.4.2 MARUWA Co., Ltd.

- 6.4.3 Murata Manufacturing Co., Ltd.

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics Co., Ltd.

- 6.4.6 Samwha Capacitor Co., Ltd.

- 6.4.7 TAIYO YUDEN Co., Ltd.

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology, Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Worth Elektronik GmbH and Co. KG

- 6.4.12 Yageo Corporation

- 6.4.13 Panasonic Industry Co., Ltd.

- 6.4.14 Holy Stone Enterprise Co., Ltd.

- 6.4.15 KEMET Corporation

- 6.4.16 Darfon Electronics Corp.

- 6.4.17 Shenzhen Sunlord Electronics Co., Ltd.

- 6.4.18 Exxelia Group

- 6.4.19 Knowles Precision Devices

- 6.4.20 NIC Components Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment