|

시장보고서

상품코드

2044292

아시아태평양의 엔지니어링 연구개발 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Engineering Research And Development Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

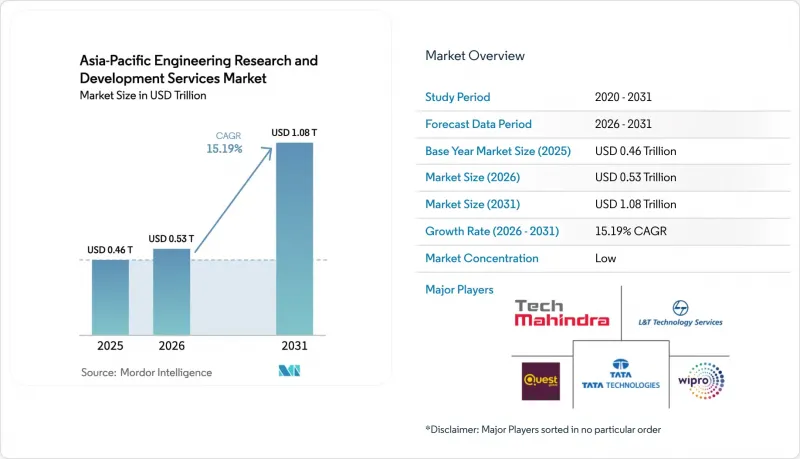

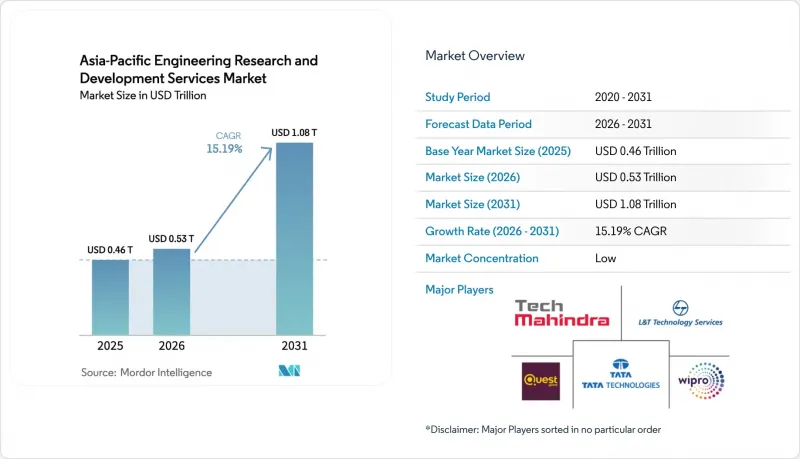

아시아태평양의 엔지니어링 연구개발 서비스 시장 규모는 2025년 4,629억 6,000만 달러에서 2026년에는 5,332억 8,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 15.19%로 성장을 지속하여, 2031년에는 1조 815억 1,000만 달러에 이를 것으로 예측됩니다.

유럽 및 미국 동종업계 대비 50-70%의 비용 우위, 추론 엔지니어링을 국내로 유치하는 국가 주도의 AI 정책, 그리고 정부 지원의 5G 및 6G 테스트베드가 결합되어 핵심 제품 개발 주기를 이 지역으로 끌어들이고 있습니다. 인도는 여전히 가장 큰 수익 거점이지만, 중국과 일본은 자국 내 혁신과 Beyond-5G 프로그램을 통해 벤더 기반을 다변화하고 있습니다. 엔지니어링 서비스 제공업체와 세계 역량 센터는 AI 인재를 확보하기 위한 경쟁이 치열해지면서 이직률과 부동산 비용을 줄일 수 있는 제2의 도시 마이크로 허브로의 이동을 유도하고 있습니다. 2025년 이후 강화된 수출 관리 감독으로 인해 내부 엔지니어링 모델과 하이브리드형 배송 아키텍처로의 구조적 전환이 촉진되고 있습니다.

아시아태평양의 엔지니어링 R&D 서비스 시장 동향 및 인사이트

디지털 퍼스트 제품 수명주기로의 전환

디지털 트윈, 모델 기반 시스템 엔지니어링, 시뮬레이션 기반 검증을 통해 물리적 프로토타입의 반복 횟수를 크게 줄이고, 클라우드 네이티브 제품 수명주기 관리 스택을 갖춘 아태지역 센터로 워크로드를 이전하고 있습니다. 일본의 '2025 통합 혁신 전략'은 HPC를 활용한 설계에 2,000억 달러 이상을 할당하고 있습니다. 생성형 AI 툴을 도입한 기업들은 시장 출시 기간을 25% 단축할 수 있었습니다고 보고하고 있지만, 기술 부족에 직면해 있습니다. 인도에서는 스스로를 AI 전문가라고 생각하는 사람 중 5명 중 1명만이 프로덕션 환경에서 모델을 배포하고 있습니다. 따라서 디지털 엔지니어링 위협에 대한 안전한 대응을 입증해야 하는 지역 벤더들에게 ISO 15288 및 IEC 62443 인증은 더 이상 선택이 아닌 필수 조건이 되고 있습니다.

아시아태평양의 아웃소싱에 적합한 비용 격차

베트남의 엔지니어 인건비는 미국의 약 30%, 서유럽의 약 50% 수준이며, 오프쇼어로 이전된 프로젝트에서 40% 이상의 매출총이익률을 유지하고 있습니다. 싱가포르와 베트남을 결합한 딜리버리 체제로 싱가포르에서 고객 맞춤형 아키텍처 설계를 진행하고, 호치민시에서 대량의 구현 작업을 진행함으로써 베트남의 효율적인 STEM 분야 취업 허가 제도를 활용하고 있습니다. 그러나 인도 주요 도시의 부동산 가격 및 임금 상승으로 인해 코임바토르, 비샤카파트남 등 제2의 거점으로의 이동이 진행되고 있습니다. 이들 지역에서는 운영비가 20-30% 저렴하고, 지방정부가 '플러그 앤 플레이' 형태의 캠퍼스에 공동 투자하고 있습니다.

엔지니어 인력의 지속적인 유출

반도체 및 임베디드 설계 직군의 연간 25-30%의 이직률은 생산성을 떨어뜨리고, 고액의 채용 보너스를 지불하게 만듭니다. 2024년 EY 조사에 따르면, 조직에 대한 소속감을 느끼는 엔지니어는 43%에 불과해 인력 유지의 위험성을 시사하고 있습니다. 인도 주요 도시의 15%가 넘는 임금 상승은 동유럽과의 비용 격차를 좁히고 있습니다. 서비스 제공업체들은 현재 운영 예산의 더 많은 부분을 재교육 아카데미와 웰니스 정책에 할당하고 있으며, 이는 단기적인 수익률을 압박하는 요인으로 작용하고 있으며, 아시아태평양의 엔지니어링 R&D 서비스 시장에서 서비스 제공 속도를 유지하는 데 필수적인 요소입니다.

부문 분석

2025년 아시아태평양 엔지니어링 R&D 서비스 시장에서 아웃소싱 서비스는 68.21%의 점유율을 차지했습니다. 그러나 수출 규제가 강화되는 가운데, 캡티브 센터는 15.53%의 성장률을 보일 것으로 예측됩니다. 사노피와 같은 다국적 기업은 2026년까지 하이데라바드의 직원 수를 4,500명으로 늘리고, 3개 대륙에 분산되어 있던 임상 및 규제 관련 워크플로우를 중앙집중화했습니다. 이번 전환으로 임상시험 신청 주기가 5분의 1 가까이 단축될 것으로 예측됩니다. 또한, 캡티브 센터는 인도의 GENESIS 인센티브와 시너지를 발휘하는 한편, 기밀성이 높은 코드를 기업 방화벽 내에 보관할 수 있어 제3자와의 라이선싱 마찰을 줄일 수 있습니다.

단기적으로는 변동비용의 유연성으로 인해 ICE에서 EV로의 파워트레인 재설계와 같은 플랫폼 전환에 있어 아웃소싱의 유용성이 유지되고 있습니다. 이 경우, 공급자는 12주 이내에 다분야의 팀을 구성하고, 이 팀을 통해 12주 이내에 프로젝트를 수행합니다. 그러나 중국이나 인도네시아의 데이터 현지화 요구 사항으로 인해, 보호된 알고리즘은 사내 팀이 담당하고 검증 업무는 외부에 위탁하는 하이브리드 모델이 점차 확산되고 있습니다. 조호르와 페낭의 면세 산업단지는 법인세를 5%, 지식근로자 개인소득세를 15%로 낮춰 자체 소유 시설의 매력을 높이고 있습니다.

2025년 기준, 엔지니어링 서비스 제공업체는 아시아태평양 엔지니어링 R&D 서비스 시장 규모의 54.12%를 차지했으며, 세계 역량 센터(GCC)는 15.59%의 연평균 복합 성장률(CAGR)로 빠르게 성장하고 있습니다. 인도에는 1,700개 이상의 세계 역량 센터(GCC)가 있으며, 2024년 기준 646억 달러의 수익을 창출할 것으로 예측됩니다. 기업들이 ISO 13485 및 AS9100을 준수하기 위해 노력하는 가운데, 이 수치는 2030년까지 1,050억 달러를 넘어설 것으로 예측됩니다. 또한, GCC 내 지적재산권 관리 체계는 새로운 수출 관리 규제에 대한 대응을 용이하게 합니다.

이러한 변화에도 불구하고, 규모의 우위를 바탕으로 대형 ESP(엔지니어링 서비스 제공업체)는 여전히 대형 프로젝트에서 중심적인 역할을 하고 있습니다. L&:T;:Technology Services는 2025년 1억 달러 규모의 반도체 프로그램을 수주하며 공급자의 기동성을 입증했습니다. 2026년 힐하우스 캐피탈이 퀘스트월드에 45억 달러를 투자한 사례에서 알 수 있듯이, 사모펀드의 관심은 여전히 높습니다. 그럼에도 불구하고 GCC와 ESP 모두 과거 비용 절감을 위해 활용되던 지방도시에서 임금 프리미엄을 높이는 치열한 인재 쟁탈전에 직면해 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Asia-Pacific engineering research and development services market size is expected to grow from USD 462.96 billion in 2025 to USD 533.28 billion in 2026 and is forecast to reach USD 1,081.51 billion by 2031 at 15.19% CAGR over 2026-2031.

Cost advantages of 50-70% versus Western peers, sovereign-AI mandates that keep inference engineering onshore, and government-funded 5G-6G test beds combine to pull core product-development cycles into the region. India remains the single largest revenue hub, while China and Japan diversify the vendor base with indigenous-innovation and Beyond-5G programs. Engineering service providers and global capability centers intensify competition for AI-ready talent, nudging both groups toward tier-2 city micro-hubs that lower attrition and real-estate costs. Heightened export-control scrutiny since 2025 is reinforcing a structural pivot toward in-house engineering models and hybrid delivery architectures.

Asia-Pacific Engineering Research And Development Services Market Trends and Insights

Shift to Digital-First Product Life-Cycles

Digital twins, model-based systems engineering, and simulation-driven validation have slashed the number of physical-prototype loops and redirected workload to Asia-Pacific centers equipped with cloud-native product lifecycle management stacks. Japan's 2025 Integrated Innovation Strategy earmarks more than USD 200 billion for HPC-enabled design. Firms adopting generative AI tooling report 25% shorter time-to-market but face skill shortages; only 1 in 5 self-identified AI professionals in India deploys models in production . ISO 15288 and IEC 62443 certifications are, therefore, becoming table stakes for regional vendors that must demonstrate the secure handling of digital engineering threads.

Outsourcing-Friendly Cost Differentials in Asia-Pacific

Engineering wages in Vietnam equal roughly 30% of U.S. rates and 50% of Western European levels, preserving gross margins above 40% for projects shifted offshore. Singapore-Vietnam delivery splits combine client-facing architecture in Singapore with volume execution in Ho Chi Minh City, leveraging Vietnam's streamlined STEM work-permit regime. However, rising real estate and salary inflation in tier-1 Indian cities is fueling a drift toward second-tier hubs such as Coimbatore and Visakhapatnam, where operating expenses are 20-30% lower and local governments co-invest in plug-and-play campuses.

Persistent Engineering-Talent Attrition

Annual churn of 25-30% in semiconductor and embedded design roles erodes productivity and forces premium hiring bonuses. A 2024 EY survey showed that only 43% of engineers felt organizational belonging, signaling retention risk. Compensation inflation above 15% in tier-1 Indian cities narrows the cost gap versus Eastern Europe. Providers now allocate a growing share of operating budgets to reskilling academies and wellness initiatives, which depress short-term margins yet remain essential for sustaining delivery velocity in the Asia-Pacific engineering research and development services market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Electric Vehicle and Autonomous Platform Programs

- Government-Funded 5G-6G Test-Beds

- IP-Protection and Export-Control Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Outsourced services controlled 68.21% of Asia-Pacific engineering research and development services market share in 2025. Captive centers, however, are projected to clock a 15.53% growth pace as export rules tighten. Multinationals like Sanofi expanded Hyderabad headcount to 4,500 in 2026, centralizing clinical and regulatory workflows once spread across three continents. That shift cuts investigational new drug filing cycles by nearly one-fifth. Captives also dovetail with India's GENESIS incentives, while allowing sensitive code to remain behind corporate firewalls, limiting third-party licensing friction.

Near-term, variable-cost flexibility keeps outsourcing relevant for platform migrations such as ICE-to-EV powertrain redesigns where providers spin up multidisciplinary squads inside 12 weeks. Yet data-localization in China and Indonesia is nudging hybrid models that reserve protected algorithms for in-house teams and farm out validation. Tax-holiday parks in Johor and Penang amplify the appeal of owned facilities by dropping corporate levies to 5% and personal taxes to 15% for knowledge staff.

Engineering service providers held 54.12% of Asia-Pacific engineering research and development services market size in 2025, but global capability centers are accelerating faster at a 15.59% CAGR. India hosts more than 1,700 GCCs generating USD 64.6 billion in fiscal 2024, and that figure could surpass USD 105 billion by 2030 as firms chase ISO 13485 and AS9100 compliance. GCC internal control of intellectual property also eases navigation of new export-control layers.

Despite the swing, scale advantages keep large ESPs center-stage for mega deals. L&T Technology Services landed a USD 100 million semiconductor program in 2025, evidencing provider agility. Private-equity interest remains strong, as a USD 4.5 billion Hillhouse stake in Quest Global showed in 2026. Still, both GCCs and ESPs confront a ferocious talent war that inflates wage premiums in second-tier cities once tapped for cost savings.

The Asia-Pacific Engineering Research and Development Services Market is Segmented by Sourcing Model (In-house/Captive Engineering, and More), Service Provider Type (Global Capability Centres, and More), Industry Vertical (Automotive, and More), Service Line (Mechanical and Electrical Engineering, and More), Delivery Model (Onshore, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- L&T Technology Services Limited

- Tata Technologies Limited

- QuEST Global Services Pte. Ltd.

- Wipro Limited

- Tech Mahindra Limited

- Infosys Limited

- Cyient Limited

- HCL Technologies Limited

- KPIT Technologies Limited

- GlobalLogic Inc.

- Persistent Systems Limited

- Tata Elxsi Limited

- Harman International Industries, Incorporated

- Capgemini SE (Capgemini Engineering)

- Accenture plc

- DXC Technology Company

- Alten S.A.

- SII Group SA

- AKKA Technologies SE

- NTT DATA Corporation

- Pactera Technology International Ltd.

- Industrial Technology Research Institute (ITRI)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Digital-First Product Life-Cycles

- 4.2.2 Outsourcing-Friendly Cost Differentials in Asia-Pacific

- 4.2.3 Accelerated Electric Vehicle and Autonomous Platform Programs

- 4.2.4 Government-Funded 5G/6G Test-Beds

- 4.2.5 Tier-2 City Micro-Hubs and Tax-Holiday Parks

- 4.2.6 Generative-AI-Assisted Design-for-Manufacture

- 4.3 Market Restraints

- 4.3.1 Persistent Engineering-Talent Attrition

- 4.3.2 IP-Protection and Export-Control Compliance Costs

- 4.3.3 Rising Project-Based Billing Price Pressure

- 4.3.4 Data-Localization Laws Limiting Code-Transfer

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape and Policy Developments

- 4.6 Technological Outlook, Digital Engineering and Industry 4.0

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Key Base-Indicator Analysis

- 4.9.1 Current Available Talent Pool of Engineers

- 4.9.2 Talent Upskill Initiatives (Govt and Industry)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sourcing Model

- 5.1.1 In-house/Captive Engineering

- 5.1.2 Outsourced Engineering Services

- 5.2 By Service Provider Type

- 5.2.1 Global Capability Centres (GCCs)

- 5.2.2 Engineering Service Providers (ESPs)

- 5.3 By Industry Vertical

- 5.3.1 Automotive

- 5.3.2 Industrial

- 5.3.3 Aerospace and Defence

- 5.3.4 Consumer Electronics

- 5.3.5 Semiconductor

- 5.3.6 BFSI

- 5.3.7 Retail

- 5.3.8 Healthcare

- 5.3.9 IT and Telecom

- 5.3.10 Rest of Industry Verticals

- 5.4 By Service Line

- 5.4.1 Mechanical and Electrical Engineering

- 5.4.2 Embedded Engineering

- 5.4.3 Software Engineering

- 5.5 By Delivery Model

- 5.5.1 Onshore

- 5.5.2 Offshore

- 5.5.3 Near-shore

- 5.5.4 Hybrid

- 5.6 By Country

- 5.6.1 China

- 5.6.2 India

- 5.6.3 Japan

- 5.6.4 South Korea

- 5.6.5 Australia

- 5.6.6 Singapore

- 5.6.7 Malaysia

- 5.6.8 Indonesia

- 5.6.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 L&T Technology Services Limited

- 6.4.2 Tata Technologies Limited

- 6.4.3 QuEST Global Services Pte. Ltd.

- 6.4.4 Wipro Limited

- 6.4.5 Tech Mahindra Limited

- 6.4.6 Infosys Limited

- 6.4.7 Cyient Limited

- 6.4.8 HCL Technologies Limited

- 6.4.9 KPIT Technologies Limited

- 6.4.10 GlobalLogic Inc.

- 6.4.11 Persistent Systems Limited

- 6.4.12 Tata Elxsi Limited

- 6.4.13 Harman International Industries, Incorporated

- 6.4.14 Capgemini SE (Capgemini Engineering)

- 6.4.15 Accenture plc

- 6.4.16 DXC Technology Company

- 6.4.17 Alten S.A.

- 6.4.18 SII Group SA

- 6.4.19 AKKA Technologies SE

- 6.4.20 NTT DATA Corporation

- 6.4.21 Pactera Technology International Ltd.

- 6.4.22 Industrial Technology Research Institute (ITRI)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment