|

시장보고서

상품코드

2061515

사료 프리믹스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Feed Premix - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

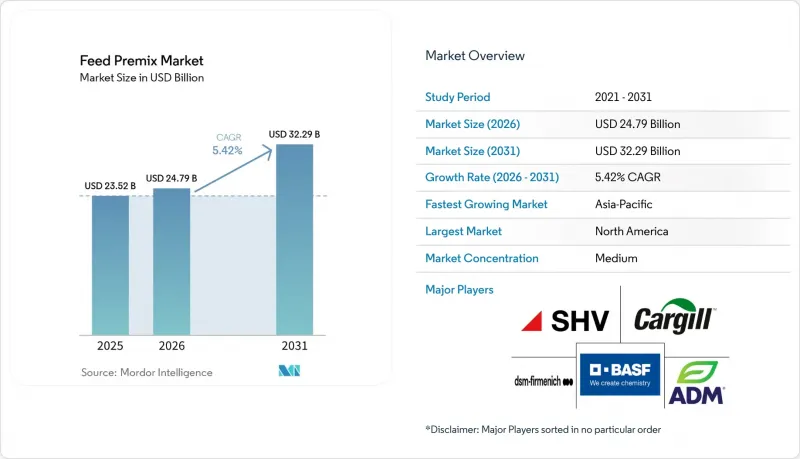

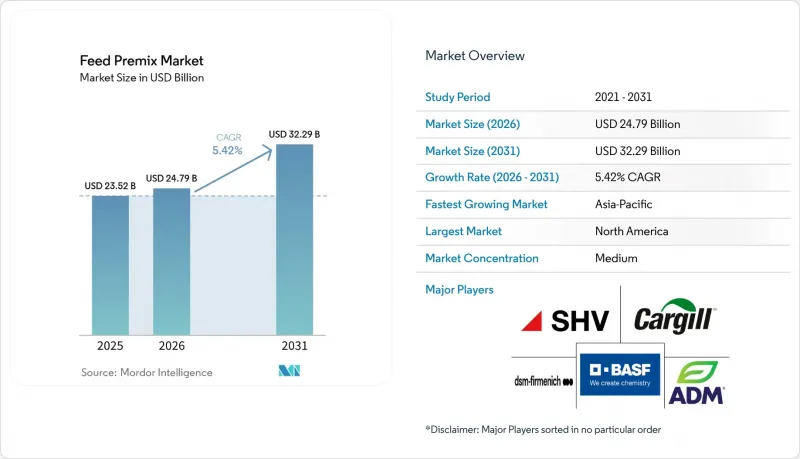

Mordor Intelligence에 의하면, 사료 프리믹스 시장 규모는 2025년 235억 2,000만 달러로 평가되었습니다. 2026년 247억 9,000만 달러에서 2031년까지 322억 9,000만 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.42%를 나타낼 것으로 예측됩니다.

본 보고서는 성분 유형(비타민, 미네랄, 아미노산 등), 형태(분말 및 액체), 동물 종(가금류, 반추동물, 돼지, 수산 양식, 반려동물, 기타 동물) 및 지역(북미, 유럽, 아시아태평양, 남미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 사료 프리믹스 시장 동향 및 인사이트

가금류 및 산란용 사료 소비량 증가

Alltech Agri-Food Outlook에 따르면, 2025년 육계용 사료 생산량은 2024년 대비 3.7% 증가하여 4억 40만 톤에 달했습니다. 이로 인해 가금류는 사료 프리믹스 시장에서 프리믹스 수요의 최대 소비 기반으로서의 입지를 공고히 했습니다. 이러한 수요 증가는 단순히 사육 두수 증가 때문만이 아니라, 대규모 가금류 생산 시스템에서 생산자들이 더 높은 밀도의 사육 환경, 더 짧은 생산 주기, 그리고 더 엄격한 사료 전환율 목표로 전환하고 있기 때문입니다. 이러한 경영 모델에서는 완성 사료 1톤당 반드시 배합되는 비타민과 미량 미네랄에 대한 수요가 증가하고 있습니다. 『Alltech Agri-Food Outlook 2026』에 따르면, 붉은살고기 가격 상승에도 불구하고 아시아와 아프리카에서 계란 소비가 견조한 추세를 보인 데 힘입어, 2024년부터 2025년에 걸쳐 산란용 사료도 3.2% 증가한 1억 8,010만 톤을 기록했습니다. 따라서 가금 사료는 계절에 따른 구매가 아닌 빈번한 생산 주기를 통해 갱신되는 광범위하고 지속적인 수요 기반을 사료 프리믹스 시장에 제공합니다. 또한, 전 세계 배합사료 생산량에서 육계 및 산란계용 사료가 차지하는 비중이 크기 때문에 품질의 일관성을 해치지 않으면서 인증 프리믹스 공급업체와의 관계를 끊는 것은 생산자에게 있어 어려운 일입니다. 따라서 개별 지역에서 질병이 발생해 혼란이 빚어지더라도, 가금 사료는 사료 프리믹스 시장에 있어 안정화 요인이 됩니다.

아시아 및 아프리카의 상업용 배합사료 보급률

Alltech Agri-Food Outlook에 따르면, 아프리카에서는 2024년부터 2025년에 걸쳐 상업용 사료 생산량이 11.5% 증가하여, 본 보고서 초안에 보고된 지역별 성장률 중 가장 높은 증가율을 기록했습니다. 나이지리아, 이집트, 케냐, 에티오피아 등 시장에서 가금류, 젖소, 반추동물 각 부문의 생산량이 증가했습니다. 더 큰 의의는 이러한 변화가 비공식적인 곡물 혼합에서 산업적인 배합 사료 유통 경로로 전환되고 있음을 반영하고 있다는 점에 있습니다. 사료 생산이 정식 제분 시스템으로 전환되면, 인증 프리믹스는 단순한 선택적 첨가물이 아니라 표준 투입 자재가 됩니다. 이러한 변화로 인해, 가축 사육 두수만으로는 추정할 수 있는 것보다 더 빠른 속도로 프리믹스 수요가 증가하는 경향이 있습니다. 동남아시아에서는 카길사가 2024년에 베트남에 설립한 ‘Giang Dien’ 프리믹스 공장이 연간 생산 능력 4만 톤, 자동화율 95% 이상을 자랑하며, 추적 가능성과 수출 품질 기준을 충족하는 현지 생산 체제가 구축되고 있음을 보여주고 있습니다. 또한, 인도네시아의 동물용 사료 원료 할랄 인증 요건 역시 사료 제조업체들이 문서화되고 검증된 프리믹스를 조달하도록 유도하는 요인이 되고 있습니다. 그 결과, 사료 프리믹스 시장에서 개발도상 지역의 상업용 사료 체계화는 여전히 가장 뚜렷한 구조적 성장 요인 중 하나입니다.

농가의 이익률에 가해지는 압박과 비용 변동

원가 압박은 사료 프리믹스 시장에 있어 여전히 뚜렷한 제약 요인으로 작용하고 있습니다. 왜냐하면 곡물이나 첨가제의 가격이 급등하면 사료 구매자들은 종종 배합 품질을 조정하기 때문입니다. 2026년 초 옥수수 조달 비용이 급등했고, 같은 기간 대두박 가격도 상승함에 따라 가금류 및 돼지 사육 농가의 이익률이 압박을 받았습니다. 이러한 압박이 거세지면, 일부 구매자들은 고품질의 프리믹스 배합을 유지하기보다는 사양이 낮은 블렌드나 저렴한 미네랄 원료로 전환하게 됩니다. 이와 유사한 비용 압박은 2025년부터 2026년에 걸쳐 멕시코만 연안 지역에서 발생한 공급 차질 당시 비타민, 아미노산, 미네랄, 유기산에도 영향을 미쳤으며, 비타민 E나 메티오닌 등의 원료에서 현저한 가격 상승이 나타났습니다. 이러한 압력은 최소한의 영양 요건보다 구매의 유연성이 더 높은 특수 기능성 제품에 대해 더 크게 작용하는 경향이 있습니다. 따라서 구매자들은 공급 계획을 보호하기 위해 선물 계약, 옵션 및 이중 조달 전략에 대한 의존도를 높이고 있습니다. 그럼에도 불구하고, 생산자가 프리미엄 배합의 깊이보다는 원가 관리를 우선시할 경우, 이익률에 가해지는 압박이 사료 프리믹스 시장의 가치 성장을 둔화시킬 가능성이 있습니다.

부문별 분석

2025년에는 비타민 프리믹스가 이 부문을 주도하며 32.1%의 점유율을 차지했습니다. 이는 모든 종에서 면역, 번식, 도체 품질에 있어 핵심적인 역할을 하고 있다는 점이 배경이 되고 있습니다. 사료 프리믹스 업계에서 이 부문은 가장 광범위한 수요 기반을 유지하고 있습니다. 왜냐하면, 비용 압박이 가해지는 시기라 하더라도 시판 사료에서 비타민이 제외되는 경우는 거의 없기 때문입니다. 가금류, 돼지, 반추동물, 수산 양식, 반려동물사료 등 폭넓은 용도로 사용됨으로써, 전 세계적으로 안정적이고 장기적인 수요를 지속적으로 뒷받침하고 있습니다.

미네랄 프리믹스는 사료 프리믹스 시장에서 생체 이용률과 배설에 대한 엄격한 관리가 점점 더 중요해짐에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.6%라는 가장 빠른 속도로 성장할 것으로 전망됩니다. 아미노산 블렌드 역시 조단백질 함량을 낮추는 전략의 혜택을 보고 있는 반면, 효소 프리믹스는 보다 다양한 대체 원료를 사용하는 배합 사료의 재설계를 통해 수요가 확대되고 있습니다. 프로바이오틱스와 프리바이오틱스 혼합물은 항생제 사용이 제한된 생산 시스템에서 그 중요성이 커지고 있으며, 항산화제, 산미료 및 특수 기능성 혼합물은 단독 첨가제가 아닌 다기능 패키지의 일부로 판매되는 사례가 늘고 있습니다. 정밀 영양 프로그램과 지속가능성에 중점을 둔 가축 생산 시스템은 전 세계적으로 첨단 미네랄 및 기능성 프리믹스 솔루션의 도입을 더욱 가속화하고 있습니다.

지역별 분석

2025년 북미는 사료 프리믹스 시장의 34.3%를 차지했습니다. 이는 높은 생산 능력을 갖춘 사료 공장, 엄격한 감독 체계, 그리고 소, 가금류, 돼지공급망에서 ‘체중 증가 비용의 최적화’에 대한 지속적인 노력에 힘입은 결과입니다. 이 지역의 생산자들은 첨단 NIR 분석 기술과 클라우드 연동형 배합 소프트웨어를 활용하여 프리믹스의 배합량을 실시간으로 조정함으로써, 영양소의 낭비를 줄이는 동시에 표시 기준을 준수하고 있습니다. 미국 식품의약국(FDA)이 2024년 10월에 발표한 동물사료 원료 승인 및 사료 표시 규정 준수 요건 업데이트 등, 규제가 명확해짐에 따라 사료 업계 전반에 걸쳐 추적 가능성과 배합 표준화가 강화되었으며, 프리믹스 제조업체는 규제 측면에서의 확실성이 높아짐에 따라 지역별 생산 능력과 기술 지원 체계를 확대할 수 있게 되었습니다.

아시아태평양은 가축 사육 두수의 급격한 증가와 자가 배합 사료에 비해 시판 사료의 경쟁력이 높아지는 추세에 힘입어, 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 7.9%라는 가장 빠른 성장 궤도를 보이고 있습니다. 중국의 프리믹스 제조업체들은 농업농촌(MARA)가 2024년에 승인한 첨가물을 활용하여, 생산성 향상을 추구하는 통합형 양식업자들에게 어필할 수 있는 신규 배합 사료 시장 출시를 가속화하고 있습니다. 인도의 낙농업 현대화, 인도네시아의 새우 양식 확대, 그리고 태국의 육계 수출이 대상 시장 규모를 더욱 확대시키고 있습니다. 한때는 유럽과 미국 시장이 중심이었던 디지털 사료 플랫폼이, 현장 기술자가 그 자리에서 영양 밀도를 조정할 수 있는 클라우드 기반 모바일 도구를 통해 동남아시아에서 급속히 보급되고 있습니다.

유럽은 사료 프리믹스 시장에서 성숙한 지역이긴 하지만, 항생제 규제 및 첨가물 사용 중단으로 인해 제품 설계가 재검토되고 있어 배합 변경이 빈번하게 이루어지는 지역입니다. 남미에서는 가금류 및 쇠고기 시장의 성장 여지가 계속해서 예상되지만, 농가 이익률의 변동에 따라 사료 배합 수준이 일시적으로 낮아질 가능성이 있습니다. 2025년에 아프리카는 사료 생산 성장률이 가장 높았습니다. 이는 가금류 및 젖소 생산 시스템에서 배합 사료가 농장에서 직접 배합하는 방식을 점차 대체하고 있기 때문에 중요한 의미를 지닙니다. 중동 수요는 여전히 식량 안보를 배경으로 한 축산 투자에 집중되어 있으며, 이로 인해 유럽과 아시아공급업체 양측으로부터의 프리믹스 수입 증가가 뒷받침되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the feed premix market size is projected to grow from USD 23.52 billion in 2025 and USD 24.79 billion in 2026 to USD 32.29 billion by 2031, registering a CAGR of 5.42% between 2026 and 2031.

This report is Segmented by Ingredient Type (Vitamins, Minerals, Amino Acids, and More), by Form (Powder and Liquid), by Animal Type (Poultry, Ruminants, Swine, Aquaculture, Pets, and Other Animals), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Premix Market Trends and Insights

Rising Poultry and Egg Feed Intensity

Broiler feed production rose 3.7% to 400.4 million metric tons in 2025 compared to 2024, which reinforced poultry as the largest consumption base for premix demand in the feed premix market, according to Alltech Agri-Food Outlook. Demand is not coming only from flock growth, because producers are also moving toward denser housing, faster cycles, and tighter feed conversion targets in large poultry systems. That operating model raises the need for dependable vitamin and trace mineral inclusion per ton of finished feed. Layer feed also increased by 3.2% to 180.1 million metric tons between 2024 and 2025, supported by steady egg consumption in Asia and Africa amid higher red meat prices, according to the Alltech Agri-Food Outlook 2026. Poultry, therefore, provides the feed premix market with a broad, recurring demand base that is renewed through frequent production cycles rather than seasonal buying. The large share of broiler and layer feed in global compound feed output also limits producers' ability to move away from certified premix suppliers without compromising quality consistency. This makes poultry a stabilizing force for the feed premix market even when disease events disrupt individual regions.

Commercial Compound Feed Penetration in Asia and Africa

Africa recorded 11.5% growth in commercial feed production between 2024 and 2025, the fastest regional growth rate reported in the draft, with gains across poultry, dairy, and ruminant systems in markets such as Nigeria, Egypt, Kenya, and Ethiopia, according to Alltech Agri-Food Outlook. The larger significance is that this shift reflects a move away from informal grain blending toward industrial compound feed channels. Once feed output moves into formal mill systems, certified premix becomes a standard input rather than an optional add-on. That change tends to raise premix demand faster than animal numbers alone would suggest. In Southeast Asia, Cargill Incorporated's Giang Dien premix plant in Vietnam, established in 2024, features an annual capacity of 40,000 metric tons and over 95% automation, showing how local production is being built around traceability and export-grade quality requirements. Indonesia's halal certification requirements for animal nutrition inputs are also pushing mills toward documented and verified premix procurement. As a result, commercial feed formalization remains one of the clearest structural growth supports for the feed premix market in developing regions.

Farmer Margin Pressure and Cost Volatility

Cost pressure remains a clear restraint for the feed premix market because feed buyers often adjust formulation quality when grain and additive costs rise quickly. Corn procurement costs increased sharply in early 2026, while soybean meal prices also moved higher over the same period, squeezing margins for poultry and swine producers. When these pressures intensify, some buyers shift toward lower-specification blends or cheaper mineral sources rather than maintaining premium premix formulas unchanged. Similar cost stress affected vitamins, amino acids, minerals, and organic acids during the 2025-2026 Gulf supply disruption, with vitamin E and methionine among the inputs facing notable price increases. This pressure tends to weigh more heavily on specialty functional products because those purchases are more flexible than minimum nutritional requirements. Buyers are therefore relying increasingly on forward contracting, options, and dual sourcing strategies to protect supply plans. Even so, margin pressure can still slow value growth in the feed premix market when producers prioritize cost control over premium formulation depth.

Other drivers and restraints analyzed in the detailed report include:

- Antibiotic-Reduction Nutrition Programs

- Precision Nutrition and Digital Formulation Adoption

- Regulatory Fragmentation for Feed Premixes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vitamin premixes led this segment with a 32.1% share in 2025, supported by their central role in immunity, reproduction, and carcass quality across species. Within the feed premix industry, this category remained the broadest demand base because commercial diets rarely remove vitamins even during periods of cost pressure. Their widespread inclusion across poultry, swine, ruminant, aquaculture, and pet nutrition applications continues to support stable, long-term global demand.

Mineral premixes are projected to grow at the fastest pace, at a 7.6% CAGR from 2026 to 2031, as tighter control of bioavailability and excretion becomes more important in the feed premix market. Amino acid blends also benefit from lower crude protein strategies, while enzyme premixes gain from reformulated diets that use more variable alternative ingredients. Probiotic and prebiotic blends are gaining momentum in antibiotic-restricted production systems, and antioxidant, acidifier, and specialty functional blends are increasingly sold as part of multi-functional packages rather than stand-alone additives. Precision nutrition programs and sustainability-focused livestock production systems are further accelerating the adoption of advanced mineral and functional premix solutions globally.

Geography Analysis

North America held a 34.3% share of the feed premix market in 2025, underpinned by high-throughput feed mills, rigorous oversight, and an enduring focus on cost-of-gain optimization within cattle, poultry, and swine supply chains. The region's producers use sophisticated NIR analytics and cloud-linked formulation software to adjust premix inclusion in real time, reducing nutrient waste and ensuring label compliance. Ongoing regulatory clarity, such as the Food and Drug Administration's (FDA's) October 2024 update to animal feed ingredient approval and feed labeling compliance requirements, has strengthened traceability and formulation standardization across the feed industry, enabling premix manufacturers to expand regional production capacity and technical support operations with greater regulatory certainty.

The Asia-Pacific region exhibits the fastest trajectory, with an 7.9% CAGR from 2026 to 2031, driven by rapid livestock population growth and a growing dominance of commercial feeds over farm-mixed rations. China's premix manufacturers capitalize on the Ministry of Agriculture and Rural Affairs' (MARA) 2024 additive approvals, accelerating time-to-market for novel blends that appeal to integrators seeking performance lifts. India's dairy modernization, Indonesia's shrimp expansion, and Thailand's broiler exports further enlarge addressable volumes. Digital feed platforms, once the domain of Western markets, are proliferating in Southeast Asia through cloud-based mobile tools that enable field technicians to adjust nutrient density on-site.

Europe remains a mature but reformulation-heavy region for the feed premix market because antibiotic restrictions and additive withdrawals are reshaping product design. South America continues to offer poultry and beef growth potential, although farmer margin volatility can lead to temporary downgrades in formulation depth. Africa posted the fastest feed production growth rate in 2025, and that is important because compound feed is replacing on-farm mixing in poultry and dairy systems. Middle East demand remains centered on food security-driven livestock investment, which supports incremental premix imports from both European and Asian suppliers.

- Cargill, Incorporated.

- Archer Daniels Midland Company

- DSM-Firmenich AG

- BASF SE

- Nutreco N.V. (SHV Holdings N.V.)

- Evonik Industries AG

- Alltech Inc.

- Land O'Lakes Inc.

- Adisseo (China National Bluestar Group)

- International Flavors & Fragrances Inc.

- Koninklijke De Heus B.V.

- Novus International, Inc.

- Kemin Industries, Inc.

- Phibro Animal Health Corporation

- Zinpro Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising poultry and egg feed intensity

- 4.2.2 Commercial compound feed penetration in Asia and Africa

- 4.2.3 Antibiotic-reduction nutrition programs

- 4.2.4 Precision nutrition and digital formulation adoption

- 4.2.5 Increasing feed fortification in dairy production systems

- 4.2.6 Alternative ingredients requiring micronutrient formulation adjustment

- 4.3 Market Restraints

- 4.3.1 Farmer margin pressure and cost volatility

- 4.3.2 Regulatory fragmentation for feed premixes

- 4.3.3 Trace-mineral supply chain disruptions

- 4.3.4 Consumer pushback on over-fortified animal products

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Ingredient Type

- 5.1.1 Vitamins

- 5.1.2 Minerals

- 5.1.3 Amino Acids

- 5.1.4 Antioxidants

- 5.1.5 Enzymes

- 5.1.6 Probiotics and Prebiotics

- 5.1.7 Acidifiers

- 5.1.8 Other Specialty Functional Premixes

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Liquid

- 5.3 By Animal Type

- 5.3.1 Poultry

- 5.3.2 Ruminants

- 5.3.3 Swine

- 5.3.4 Aquaculture

- 5.3.5 Pets

- 5.3.6 Other Animals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Netherlands

- 5.4.3.7 Poland

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Thailand

- 5.4.4.6 Vietnam

- 5.4.4.7 Indonesia

- 5.4.4.8 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated.

- 6.4.2 Archer Daniels Midland Company

- 6.4.3 DSM-Firmenich AG

- 6.4.4 BASF SE

- 6.4.5 Nutreco N.V. (SHV Holdings N.V.)

- 6.4.6 Evonik Industries AG

- 6.4.7 Alltech Inc.

- 6.4.8 Land O'Lakes Inc.

- 6.4.9 Adisseo (China National Bluestar Group)

- 6.4.10 International Flavors & Fragrances Inc.

- 6.4.11 Koninklijke De Heus B.V.

- 6.4.12 Novus International, Inc.

- 6.4.13 Kemin Industries, Inc.

- 6.4.14 Phibro Animal Health Corporation

- 6.4.15 Zinpro Corporation