|

시장보고서

상품코드

2061518

의료 업계 첨단 인증 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Advanced Authentication In Healthcare Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

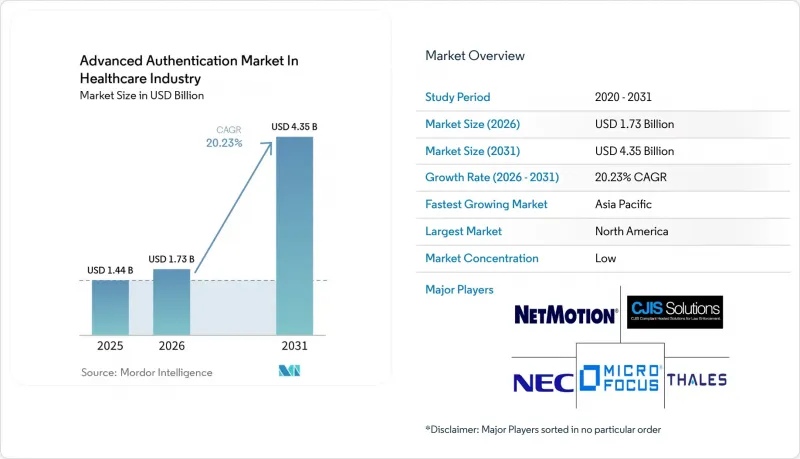

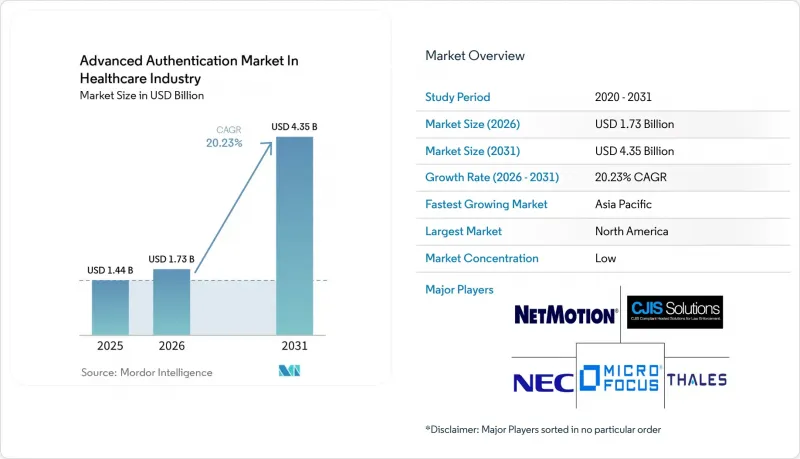

의료 업계 첨단 인증 시장 규모는 2025년에 14억 4,000만 달러로 평가되었고, 2026년 17억 3,000만 달러로 추정되고, 2031년까지 43억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 20.23%를 나타낼 전망입니다.

본 보고서는 인증 방식별(생체 인증, 스마트 카드 등), 인증 요소별(단일 요소, 다중 요소), 구성 요소별(솔루션, 서비스), 도입 형태별(온프레미스, 클라우드), 최종 사용자별(병원 및 진료소, 건강보험 사업자 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

의료 업계 첨단 인증 시장 동향

의료 분야 랜섬웨어 공격 증가로 보안 예산이 늘어나고 있습니다.

2024년에 발생한 444건의 의료 사이버 사고 중 238건이 랜섬웨어에 의한 것이었으며, 이는 침해된 기록의 69%를 차지하여 인증 정보 탈취 위협의 심각성을 여실히 보여주고 있습니다. Change Healthcare의 시스템 장애로 인한 24억 달러의 손실은 의료 사이버 보안 분야에서 취약한 인증 체계가 초래할 수 있는 경제적 손실의 규모를 여실히 보여주었습니다. 평균 보안 예산은 IT 지출의 5%에서 12%로 증가했으며, 현재 이사회 지침에서 비밀번호 폐지가 측정 가능한 환자 안전 목표로 자리 잡고 있습니다. FinCEN은 2022-2024년 발생한 389건의 의료 관련 사고와 관련된 랜섬웨어 몸값 지급액이 3억 540만 달러에 달하는 것으로 집계했으며, 이로 인해 비밀번호 없는 전략의 비즈니스적 타당성이 더욱 강화되었습니다. 피싱 방지 기능을 도입한 의료 기관에서는 특권 계정 침해 건수가 현저히 감소했으며, 강력한 신원 확인과 랜섬웨어에 대한 내성 간의 연관성이 입증되었습니다.

환자 데이터 보호에 관한 규제 요건

2023년 3월부터 시행되고 있는 FDA 섹션 524B에 따르면, 의료기기 제조업체는 인증 기능을 탑재하고 모든 시판 전 신청 시 소프트웨어 부품 목록을 공개해야 합니다. 2025년 7월에 발간된 NIST SP 800-63A-4에서는 생체 인증 기준이 업데이트되어, 1만 회당 1회 미만의 오일치율로 제시 공격을 감지할 수 있게 되었습니다. HIPAA 집행이 강화되면서, 2024년에는 접근 제어 미비 사항과 관련해 1억 4,200만 달러의 벌금이 부과되었습니다. 유럽의 GDPR(EU 개인정보보호규정) 역시 유사한 제재 조치를 규정하고 있으며, 전 세계 매출액의 최대 4%에 달하는 벌금이 부과될 수 있어 다국적 기업들은 대륙을 넘나들며 ID 정책을 통일해야 하는 압박을 받고 있습니다. 현재 사이버 보험 갱신 시 다단계 인증 도입이 의무화되어 있으며, 규제와 시장의 힘이 동일한 인증 기준으로 수렴되고 있습니다.

기존 병원 IT 시스템의 높은 도입 비용

많은 병원에서는 지원이 종료된 운영 체제에서 실행되는 150개 이상의 애플리케이션을 운영하고 있습니다. 각 레거시 플랫폼에 대한 맞춤형 통합으로 인해 프로젝트 비용이 수백만 달러 규모로 불어나, 이익률이 2-3%에 불과한 의료 기관들에게는 큰 과제가 되고 있습니다. ID 게이트웨이는 구식 LDAP나 독자적인 로그인 방식을 최신 SAML이나 OAuth로 변환하지만, 시스템에 복잡성을 더하게 됩니다. 설비투자위원회는 눈에 보이지 않는 보안 대책보다 진단 장비를 우선시하는 경우가 많으며, 그 결과 보안 침해나 사법적 합의가 이루어질 때까지 업그레이드가 미뤄지는 경향이 있습니다.

부문별 분석

2025년, 의료 업계 첨단 인증 시장 매출액 중 생체 인증이 47.85%를 차지하여, 이 부문은 첨단 인증 시장 점유율의 거의 절반을 차지했습니다. 이 방식이 뛰어난 점은 수술팀이 장갑을 낀 채로 손가락 지문이나 손바닥 정맥 스캔을 통해 1초도 채 걸리지 않아 기록에 접근할 수 있기 때문입니다. 생체 인증 시장 규모는 생체 인증 유효성 판정 기준이 성숙해짐에 따라 2031년까지 연평균 성장률(CAGR) 19.60%로 확대될 것으로 전망됩니다. 각 벤더사는 모바일 카트에 다중 파장 센서를 탑재하여, 한 번의 조작으로 기기와 세션을 모두 보호하고 있습니다. 도입의 성패는 정확도를 저하시키지 않으면서 스캐너를 소독하는 위생 프로토콜에 달려 있습니다.

의료 업계의 고도화된 인증 시장에서 모바일 스마트 인증은 가장 빠른 성장세를 보이고 있으며, 2031년까지 연평균 성장률(CAGR) 22.05%로 확대될 것으로 전망됩니다. 이는 물리적 출입 통제와 논리적 로그인이 하나의 스마트폰 지갑에 통합된 데서 비롯된 것입니다. 병원은 이러한 디지털 배지를 즉시 무효화할 수 있으므로, 직원이 퇴사할 때 발생할 수 있는 위험을 줄일 수 있습니다. 스마트카드는 국방보건국(DHA)의 의무화 조치에 따라 여전히 사용되고 있지만, 리더기 유지 비용이 높기 때문에 수요는 점차 정체되고 있습니다. 하드웨어 토큰은 휴대전화 사용이 금지된 무균 구역의 보안을 보장하지만, FIDO 2의 기기 내 키가 표준화됨에 따라 시장 점유율은 감소하고 있습니다. 일회용 비밀번호는 SIM 스와핑 공격 사례가 보고됨에 따라 점차 지지를 잃어가고 있습니다.

의료 업계의 고도화된 인증 시장에서 다중 인증 솔루션은 2025년에 63.10%의 시장 점유율을 차지할 것으로 예상되며, 사이버 보험사들이 이를 도입하지 않은 경우 보상을 거부하게 됨에 따라 연평균 성장률(CAGR) 21.10%로 성장하고 있습니다. 위험 기반 인증 엔진은 현재 비정상적인 동작이 감지된 경우에만 인증 요소의 수를 늘리도록 설계되어 있어, 보안과 의료진의 편의성을 모두 충족시키고 있습니다. 2024년 하반기에 보고된 푸시 알림 피로 공격으로 인해, 리플레이 공격을 차단하는 FIDO2 하드웨어 키로의 전환이 가속화되었습니다. 다중 인증 도입과 관련된 의료 업계의 고급 인증 시장 규모는 2031년까지 28억 6,000만 달러에 달할 것으로 전망됩니다.

단일 요소 인증은 여전히 엔드포인트의 36.90%를 보호하고 있으며, 그 중 상당수는 편의성이 위험성을 상쇄하는 환자 포털입니다. 거버넌스 위원회는 데이터 분류 수준에 따라 애플리케이션을 구분하여, 전자 처방전 시스템에는 생체 인증과 토큰을 결합한 인증 게이트를 도입하는 한편, 카페테리아 시스템에서는 사용자 이름과 비밀번호 조합을 유지하고 있습니다. 이 계층형 모델은 NIST의 지침을 따르고 있으며, 도입을 저해할 수 있는 일률적인 마찰을 피하고 있습니다.

지역별 분석

북미는 막대한 정보 유출 비용, 적극적인 규제 당국, 그리고 풍부한 IT 예산을 바탕으로 2025년 의료 업계 첨단 인증 시장 매출의 39.95%를 차지하며 시장을 주도했습니다. OCR(미국 시민권 및 인권국)은 2024년에 1억 4,200만 달러의 벌금을 부과했으며, 그 중 68%는 인증 미비 때문이었습니다. Change Healthcare의 시스템 장애는 생태계 전체에 파급되는 영향을 보여주었으며, 이로 인해 ID 관리가 이사회 안건으로 상정되게 되었습니다. 캐나다에서는 주별 전자 건강 카드를 통해 비슷한 과정을 밟고 있지만, 멕시코는 도입 초기 단계에 있으며, 민간 의료기관이 전자 차트를 도입함에 따라 ID 관리 기능을 추가하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 22.60%를 기록할 전망이며, 지역별로는 가장 빠른 성장세를 보이고 있습니다. 일본은 EHR 키오스크에 얼굴 인식 기능을 탑재하는 정부의 디지털화 계획에 따라 병원의 신원 관리 시스템을 현대화하고 있습니다. 인도는 Aadhaar의 생체 인증을 Ayushman Bharat Digital Mission과 연계하여, 지문 및 홍채 스캔을 통해 보호되는 대규모 신규 사용자 기반을 구축하고 있습니다. 중국에서는 국가 의료 클라우드를 활용하는 스마트 병원 구축에 있어 다중 인증 관리가 의무화되어 있습니다. 호주와 한국은 성숙한 광대역 환경과 스마트폰 보급률을 바탕으로 원격의료 분야의 모바일 인증을 추진하고 있습니다. 이러한 성장세와 더불어, 데이터 보호법은 국가마다 크게 다르기 때문에 공급업체는 의료 업계의 각 고도화된 인증 시장에 맞추어 클라우드 호스팅 및 키 위탁 모델을 조정해야 합니다.

유럽은 이 두 극의 중간에 위치하고 있습니다. 전 세계 매출의 최대 4%에 달하는 GDPR(EU 개인정보보호규정) 벌금이 조기 준수를 촉진하고 있으며, 독일의 전자 건강 카드 프로그램에는 기본적으로 X.509 인증서가 내장되어 있습니다. 영국의 NHS는 통합 의료 시스템 전반에 ID를 도입하고 있으나, 그 복잡성으로 인해 도입 일정이 지연되고 있습니다. 프랑스, 이탈리아, 스페인은 국가 디지털 헬스 기금을 통해 투자를 진행하고 있지만, 조달 주기는 여전히 길어지고 있습니다. 동유럽에서는 첨단 인증 시장의 도입 속도가 더딘 데다 구식 인프라가 클라우드 전환을 가로막고 있지만, EU 전역의 표준 규격이 통합을 향해 꾸준한 압력을 가하고 있습니다. 남미, 중동 및 아프리카에서는 보급률이 낮지만, 신규 병원 건설의 혜택을 받아 클라우드 네이티브 ID 관리로 단숨에 전환할 수 있는 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the advanced authentication market size in healthcare industry was valued at USD 1.44 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 4.35 billion by 2031, at a CAGR of 20.23% during the forecast period (2026-2031).

This report is Segmented by Authentication Method (Biometric, Smart Card, and More), Authentication Factor (Single Factor, Multi-Factor), Component (Solutions, Services), Deployment Mode (On-Premises, Cloud), End User (Hospitals and Clinics, Health Insurance Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Advanced Authentication Market In Healthcare Industry

Rising Healthcare Ransomware Attacks Driving Security Budgets

Ransomware caused 238 of 444 healthcare cyber events in 2024 and accounted for 69% of compromised records, underscoring the lethality of credential theft pipelines. The USD 2.4 billion fallout from the Change Healthcare outage revealed the monetary weight of weak authentication in the healthcare cybersecurity space. Average security budgets rose from 5% to 12% of IT spending, and board directives now frame password retirement as a measurable patient safety objective. FinCEN tracked USD 305.4 million in ransomware payouts tied to 389 healthcare incidents between 2022 and 2024, which hardened the business case for password-less strategies. Providers that rolled out phishing-resistant factors recorded measurable drops in privileged-account compromise, validating the link between strong identity proofing and ransomware resilience.

Regulatory Mandates for Patient Data Protection

FDA Section 524B, operational since March 2023, requires device manufacturers to embed authentication and publish software bills of materials in every pre-market submission. NIST SP 800-63A-4, issued in July 2025, upgrades biometric standards to include presentation-attack detection at false-match rates below 1 in 10,000. HIPAA enforcement accelerated, with USD 142 million in 2024 penalties tied to access-control lapses. The European GDPR mirrors these fines, with penalties of up to 4% of global revenue, prompting multinationals to unify their identity policies across continents. Cyber-insurance renewals now mandate multi-factor deployment, making regulatory and market forces converge on the same authentication baseline.

High Implementation Costs for Legacy Hospital IT Systems

Many hospitals juggle more than 150 applications that run on unsupported operating systems. Custom integration for each legacy platform pushes project bills into the multi-million-dollar range, a challenge for providers running on 2-3% margins. Identity gateways translate old LDAP or proprietary log-ons into modern SAML or OAuth, but add complexity. Capital committees often choose diagnostic equipment over invisible security, leading to deferred upgrades until after a breach or consent decree.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Connected Medical Devices Expanding Attack Surface

- Shift to Remote Telehealth Requiring Secure Identity Verification

- Interoperability Challenges Among Disparate Healthcare Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biometrics accounted for 47.85% of advanced authentication market in healthcare industry revenue in 2025, giving this segment nearly half of the advanced authentication market share. The modality excels because surgical teams can unlock records with gloved fingerprints or palm-vein scans in under one second. The advanced authentication market size for biometrics is projected to rise at 19.60% CAGR through 2031 as liveness detection standards mature. Vendors embed multispectral sensors into mobile carts, securing both device and session in one gesture. Implementation success hinges on hygiene protocols that disinfect scanners without degrading accuracy.

Mobile smart credentials record the fastest growth, in advanced authentication market in healthcare industry, at a 22.05% CAGR to 2031, driven by the convergence of physical door access and logical log-on inside one smartphone wallet. Hospitals can revoke these digital badges instantly, trimming risk when staff depart. Smart cards persist under Defense Health Agency mandates but face plateauing demand because reader fleets are expensive to maintain. Hardware tokens secure sterile zones where phones are barred; however, market share is eroding as FIDO2 on-device keys become the standard. One-time passwords are falling out of favor after documented SIM-swap exploits.

Multi-factor solutions, in advanced authentication market in healthcare industry, held 63.10% share in 2025 and expand at 21.10% CAGR as cyber-insurance carriers refuse coverage without them. Risk-based engines now elevate factor count only when anomalous behavior is detected, blending security with clinician usability. Push-fatigue attacks documented in late 2024 accelerated migration to FIDO2 hardware keys that block replay. The advanced authentication market in healthcare industry size tied to multi-factor deployments is forecast at USD 2.86 billion by 2031.

Single-factor still protects 36.90% of endpoints, largely patient portals where convenience outweighs risk. Governance committees segment applications by data-classification level, deploying biometric-plus-token gates on e-prescribing while keeping username-password pairs on cafeteria systems. This tiered model aligns with NIST guidance and avoids blanket friction that could undercut adoption.

Geography Analysis

North America dominated with 39.95% of 2025 revenue of advanced authentication market in healthcare industry, helped by high breach costs, aggressive regulators, and strong IT budgets. OCR issued USD 142 million in penalties during 2024, and 68% cited authentication gaps. The Change Healthcare outage demonstrated ecosystem-wide ripple effects, which moved identity to the board agenda. Canada follows similar paths through provincial e-healthcards, while Mexico is earlier in its journey but is adding identity controls as private providers adopt electronic records.

The Asia-Pacific region posts the fastest regional growth at a 22.60% CAGR through 2031. Japan modernizes hospital identity under government digitization schemes that embed face recognition in EHR kiosks. India links Aadhaar biometrics to the Ayushman Bharat Digital Mission, creating a massive new user base secured by fingerprints and iris scans. China mandates multi-factor authentication controls within smart hospital rollouts that utilize national health clouds. Australia and South Korea ride mature broadband and smartphone penetration to push mobile authentication in remote care. Despite momentum, data-protection laws vary widely, so vendors must tailor cloud hosting and key escrow models by advanced authentication market in healthcare industry.

Europe sits between these poles. GDPR fines up to 4% of global turnover motivate early compliance, and Germany's e-healthcard program embeds X.509 certificates by default. The United Kingdom's NHS is rolling identity across integrated care systems, yet complexity slows timelines. France, Italy, and Spain invest through national digital-health funds, but procurement cycles remain lengthy. Advanced authentication market adoption is slower in Eastern Europe, and older infrastructure restrains cloud shifts, yet pan-EU standards exert steady pressure for convergence. South America, the Middle East, and Africa trail in penetration but benefit from new hospital builds that can leapfrog straight to cloud-native identity.

- NetMotion Software, Inc (Absolute Software Corporation)

- CJIS Solutions LLC

- Micro Focus International PLC (OpenText UK Holding Limited)

- Auth0 Inc (an Okta Company)

- WideBand Corporation

- Fujitsu Limited

- Thales Group (Gemalto NV)

- NEC Corporation

- Broadcom Inc (CA Technologies)

- Dell Technologies Inc

- IDEMIA France SAS (Safran Identity and Security)

- HID Global Corporation

- Lumidigm Inc (HID Global)

- PistolStar Inc (SailPoint Company)

- Okta Inc

- Ping Identity Holding Corp

- OneSpan Inc

- Imprivata Inc

- Microsoft Corporation

- RSA Security LLC

- Duo Security Inc (Cisco Systems)

- M2SYS Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Connected Medical Devices Expanding Attack Surface

- 4.2.2 Regulatory Mandates for Patient Data Protection

- 4.2.3 Shift to Remote Telehealth Requiring Secure Identity Verification

- 4.2.4 Rising Healthcare Ransomware Attacks Driving Security Budgets

- 4.2.5 Integration of Biometric Authentication in EHR Systems

- 4.2.6 Rapid Adoption of Zero Trust Architecture in Hospital IT Networks

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs for Legacy Hospital IT Systems

- 4.3.2 Interoperability Challenges Among Disparate Healthcare Applications

- 4.3.3 User Resistance from Clinical Staff Due to Workflow Friction

- 4.3.4 Limited Broadband Connectivity in Rural Healthcare Facilities

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Authentication Method

- 5.1.1 Biometric

- 5.1.2 Smart Card

- 5.1.3 Mobile Smart Credentials

- 5.1.4 Hardware Token

- 5.1.5 Other Authentication Methods

- 5.2 By Authentication Factor

- 5.2.1 Single Factor

- 5.2.2 Multi-Factor

- 5.3 By Component

- 5.3.1 Solutions

- 5.3.2 Services

- 5.4 By Deployment Mode

- 5.4.1 On-Premises

- 5.4.2 Cloud

- 5.5 By End User

- 5.5.1 Hospitals and Clinics

- 5.5.2 Health Insurance Providers

- 5.5.3 Pharma and Biotech Companies

- 5.5.4 Medical Device Manufacturers

- 5.5.5 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 NetMotion Software, Inc

(Absolute Software Corporation)

- 6.4.2 CJIS Solutions LLC

- 6.4.3 Micro Focus International PLC

(OpenText UK Holding Limited)

- 6.4.4 Auth0 Inc (an Okta Company)

- 6.4.5 WideBand Corporation

- 6.4.6 Fujitsu Limited

- 6.4.7 Thales Group (Gemalto NV)

- 6.4.8 NEC Corporation

- 6.4.9 Broadcom Inc (CA Technologies)

- 6.4.10 Dell Technologies Inc

- 6.4.11 IDEMIA France SAS (Safran Identity and Security)

- 6.4.12 HID Global Corporation

- 6.4.13 Lumidigm Inc (HID Global)

- 6.4.14 PistolStar Inc (SailPoint Company)

- 6.4.15 Okta Inc

- 6.4.16 Ping Identity Holding Corp

- 6.4.17 OneSpan Inc

- 6.4.18 Imprivata Inc

- 6.4.19 Microsoft Corporation

- 6.4.20 RSA Security LLC

- 6.4.21 Duo Security Inc (Cisco Systems)

- 6.4.22 M2SYS Technology

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment