|

시장보고서

상품코드

2061532

아시아태평양의 스마트 키 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Smart Key - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

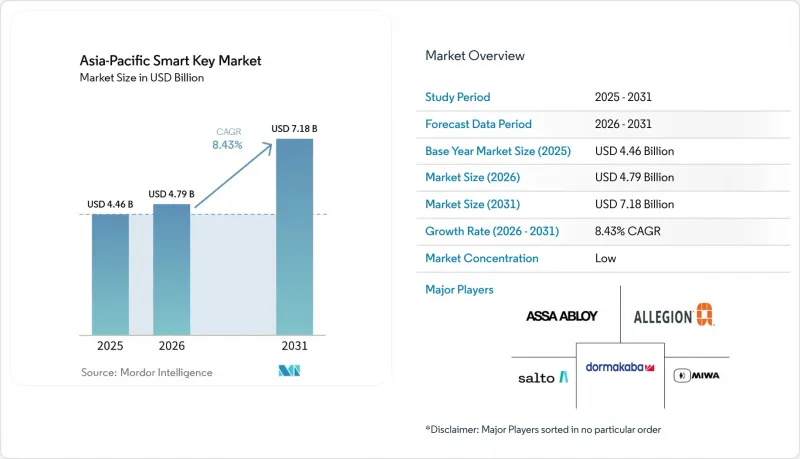

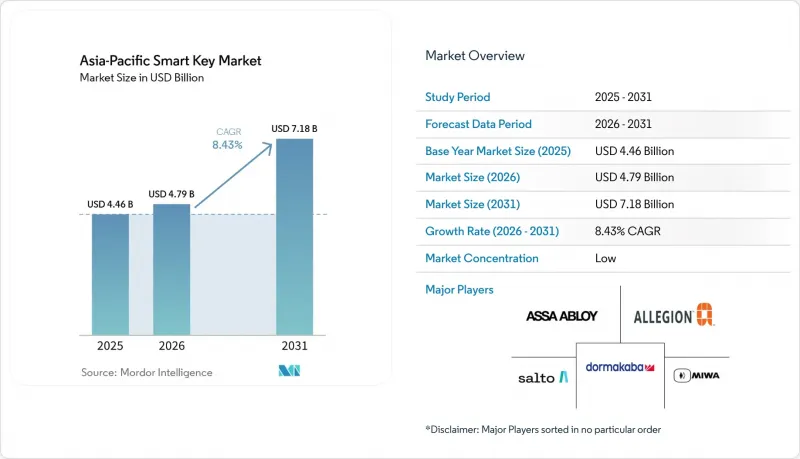

아시아태평양의 스마트 키 시장 규모는 2025년 44억 6,000만 달러로 평가되었고, 2026년에는 47억 9,000만 달러로 추정되고, 2026-2031년 CAGR 8.43%로 성장을 지속할 전망이며, 2031년까지 71억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(스마트 카 키, 스마트 도어 키 및 잠금 연동형 인증 정보, 모바일 기반 및 가상 키 등), 기술별(RFID, 블루투스 및 BLE, NFC, Wi-Fi 등), 인증 방법별(스마트폰 기반 접근 등), 최종 사용자 산업별(자동차, 주택, 호스피탈리티 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 스마트 키 시장 동향 및 인사이트

아시아태평양 도시 가구의 스마트 홈 보급 확대

인구가 밀집된 도시 지역에서 스마트 홈의 보급이 확대됨에 따라, 해당 지역 전체의 주거용 출입 통제 시스템 잠재 시장이 커지고 있습니다. 가장 큰 수요는 개발사, 집주인 및 임대 관리 업체가 출입 관리 시스템을 독립형 기기로 판매하는 것이 아니라, 보다 광범위한 디지털 홈 서비스에 통합할 수 있는 분야에서 발생하고 있습니다. 이로 인해 고급 아파트나 전문적으로 관리되는 부동산의 갱신 주기가 빨라지는 한편, 신축 부동산의 경우 건설 중에 직접 설치할 수 있게 됩니다. 또한, 단순히 하드웨어 가격만으로 경쟁하는 것이 아니라, 잠금, 인증 정보, 사용자 권한, 거주자 지원을 단일 서비스 계층으로 통합할 수 있는 브랜드의 가치도 높아집니다. 아시아태평양의 스마트 키 시장에서 주거용 수요는 개발업체나 부동산 관리 회사와 같은 기관 투자자들에 의해 점점 더 주도되고 있으며, 도입 기간이 단축됨과 동시에 가격 결정권이 플랫폼 주도형 공급업체로 이동하고 있습니다. 이러한 변화는 입주 기간 전반에 걸쳐 지속적인 인증 정보 관리, 원격 프로비저닝, 방문자 접근, 라이프사이클 서비스를 지원할 수 있는 공급업체에게도 유리하게 작용하고 있습니다.

호스피탈리티 업계의 비접촉식 게스트 출입 및 모바일 키로의 전환

이 지역의 숙박업자들은 프런트 데스크에 대한 의존도를 낮추고 투숙객의 체크인 시 불편함을 해소할 수 있어, 비접촉식 체크인 방식으로 전환하고 있습니다. 미쓰이 부동산은 2026년 3월, Vingcard사의 클라우드 기반 출입 관리 시스템 'Vostio'와 MIFARE 2GO 인증 정보를 활용하여, 자회사인 '미쓰이 가든 호텔' 및 'sequence' 호텔 브랜드 전 지점에 Apple Wallet을 지원하는 'Room Key'를 도입했습니다. 이러한 전개는 호텔이 더 이상 락 하나만으로 평가를 내리지 않고 있음을 보여줍니다. 왜냐하면 현재의 실제 의사 결정 과정에는 인증 정보의 전달, 클라우드를 통한 오케스트레이션, 그리고 시설 시스템 간의 상호 운용성이 포함되기 때문입니다. 월렛 기반 접속이 중요시되는 또 다른 이유는 전용 앱 다운로드나 계정 설정에 따른 사용자의 진입 장벽을 낮추고, 게스트의 참여율을 저해하는 요인을 해소할 수 있다는 점에 있습니다. 아시아태평양의 스마트 키 시장에서 호텔에서의 도입은 모바일 인증의 유효성을 입증하는 명확한 사례가 되고 있으며, 서비스 아파트나 기업 시설 등 다른 환경에서도 스마트폰을 통한 출입이 보편화되는 데 일조하고 있습니다. 따라서, 도어 하드웨어, 인증 정보 발급, 호텔 워크플로 소프트웨어를 연동할 수 있는 공급업체는 호스피탈리티 업계의 차세대 수요를 선점하는 데 있어 더 유리한 입장에 있다고 할 수 있습니다.

높은 초기 개조 및 통합 비용

높은 개조 및 통합 비용은 특히 커넥티드 액세스를 위한 명확한 예산이 확보되지 않은 오래된 건물이나 소규모 부동산 포트폴리오의 경우, 여전히 광범위한 도입을 제한하고 있습니다. 문제는 대개 잠금 장치 자체에만 국한되지 않습니다. 도입 시에는 문, 전원, 네트워크, 인증 정보 발급 워크플로우 및 현지 서비스 체계의 업그레이드도 필요할 수 있기 때문입니다. 이는 건물 유형이 다양하여, 도입을 시작하기 전에 시공업체가 현장 차원에서 더 많은 개조 작업을 수행해야 할 가능성이 있는 2급 및 3급 도시에서 더욱 큰 문제가 되고 있습니다. 지속적인 소프트웨어 비용도 중요한 요소입니다. 포트폴리오 운영자는 초기 도입 비용뿐만 아니라, 여러 거점에 걸쳐 있는 다수의 문을 관리하기 위한 월 이용료도 고려해야 하기 때문입니다. 그 결과, 도입은 우선 신축 건물, 고급 호텔, 기업 캠퍼스, 그리고 소프트웨어 및 서비스의 전체 스택을 수용할 수 있는 개발사 주도의 프로젝트에 집중되는 경향이 있습니다. 아시아태평양의 스마트 키 시장에서는 사용자의 관심과 기술적 준비도가 모두 높아지고 있음에도 불구하고, 이러한 비용 구조로 인해 실질적인 개선 대상이 되는 범위가 좁아지고 있습니다.

부문별 분석

2025년, 스마트 자동차 키는 아시아태평양 스마트 키 시장 점유율의 48.33%를 차지했으며, 자동차 분야가 다른 분야를 압도적인 차이로 제치고 최대 제품 부문이 되었습니다. 이 리드는 원격 출입 시스템, 이모빌라이저 연동 시스템, 그리고 점점 더 널리 보급되고 있는 스마트폰 기반 디지털 액세스 도구에 대한 OEM의 장기적인 투자를 반영하고 있습니다. 2025년 말까지 CCC 인증은 16개 자동차 제조업체의 제품을 포괄하고 있었으며, APAC(아시아태평양) 지역 브랜드들이 그 기반에서 확고한 입지를 차지하고 있었습니다. 이러한 규모 덕분에 자동차 부문은 가장 광범위한 도입 실적을 쌓았으며, 공급업체의 판매량, 표준화 참여, 그리고 생태계 내에서의 가시성 측면에서 핵심적인 위치를 유지했습니다. 동시에, 자동차 분야의 성장은 여전히 차량 출시 주기, 공급업체 검증 기간 및 생산 일정에 좌우되기 때문에 그 성숙도는 다른 인증 범주를 어느 정도 속도로 추월할 수 있는지에 자연스러운 제약을 가하고 있습니다.

모바일 기반 및 가상 키 시장은 2031년까지 연평균 성장률(CAGR) 9.03%를 나타낼 것으로 예측되며, 이 광범위한 카테고리 내에서 소프트웨어 및 지갑 중심의 더욱 강력한 성장 경로를 시사하고 있습니다. Allegion은 2026년, Aliro 1.0이 Apple, Google, Samsung의 전체 지갑 환경에서 모바일 인증 정보와 리더기 간의 통신을 위한 표준화된 모델을 구축할 것이라고 발표했습니다. 스마트 도어 키나 잠금 장치 연동형 인증 수단은 주택 및 상업용 빌딩이 자동차 분야를 제외한 다른 분야에서 가장 광범위한 도입 기반을 제공하고 있기 때문에 여전히 중요합니다. 반면, 스마트 키, 카드, 웨어러블 기기는 공유 액세스나 일시적인 액세스가 일반적인 기관의 업무 흐름에 적합합니다. 아시아태평양의 스마트 키 시장에서 이러한 구성 비율은 하드웨어 출하량이 여전히 광범위한 범위를 차지하고 있음을 시사하지만, 상업적 초점은 소프트웨어 제어, 인증 수단의 이동성, 그리고 지속적인 서비스 가치로 점차 이동하고 있습니다. 따라서 아시아태평양의 스마트 키 업계는 새로운 잠금 방식의 등장보다는 기기 상위 계층에 있는 인증 레이어를 누가 통제하느냐에 따라 그 양상이 변화하고 있습니다.

2025년 기준, RFID는 아시아태평양 스마트 키 시장의 34.87%를 차지했으며, 이는 호텔 및 리조트 업계의 잠금 장치, 사무실 출입 카드, 대중교통과 연계된 인증 환경에서 RFID가 오랫동안 확립해 온 역할을 반영한 것입니다. 그 지위가 여전히 확고한 이유는 운영자가 워크플로를 이해하고 있고, 직원들이 인증 정보를 발급하는 방법을 알고 있으며, 많은 시설에서 이미 리더기가 도입되어 있어 이를 단기간에 교체하려면 막대한 비용이 들기 때문입니다. 실용적인 관점에서 볼 때, 이로 인해 RFID는 기능의 참신함보다 신뢰성이 중시되는 중규모 호텔, 기업 시설, 공공시설, 복합 용도 빌딩에서 확고한 역할을 수행하고 있습니다. 이미 구축된 인프라는 카드 기반 접근이 일상화되고 업데이트 주기가 긴 성숙한 환경에서 특히 중요합니다. 즉, 현재 기술 전환의 대부분은 기존의 RFID 지원 인프라에서 급격하게 전환되는 것이 아니라, 하이브리드 구성을 통해 이루어지고 있다는 뜻입니다.

블루투스 저에너지(BLE)는 2031년까지 연평균 성장률(CAGR) 9.43%를 나타낼 것으로 예측되며, 근접형 및 지갑 기반 접근 경험 분야에서 선호되는 기술로 자리매김하고 있습니다. 카 커넥티비티 컨소시엄(CCC)은 디지털 키의 인증 대상을 BLE 및 UWB로 확대했습니다. 이를 통해 더욱 원활한 핸즈프리 사용 및 기기 간 연동 사례가 지원됩니다. 탭 기반 접속 방식은 여전히 친숙하고 신뢰도가 높기 때문에 NFC는 여전히 강력한 보조 역할을 수행하고 있습니다. 반면, Wi-Fi는 주요 인증 채널이라기보다는 원격 관리, 프로비저닝, 펌웨어 업데이트 분야에서 그 중요성을 유지하고 있습니다. 아시아태평양의 스마트 키 시장에서 기술 경쟁은 단순한 연결성 강조에서 벗어나, 상호 운용성, 리더기 호환성, 인증 정보 이관, 그리고 전반적인 사용자 경험의 질에 초점을 맞춘 보다 실용적인 검증 단계로 전환되고 있습니다. 따라서 아시아태평양의 스마트 키 업계는 멀티 프로토콜 아키텍처로 전환되고 있으며, 성공을 거둘 벤더는 단일 무선 표준을 추진하는 기업이 아니라 사업자의 복잡성을 단순화하는 기업이 될 가능성이 높다고 볼 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the asia-Pacific smart key market size is expected to grow from USD 4.46 billion in 2025 to USD 4.79 billion in 2026 and is forecast to reach USD 7.18 billion by 2031 at 8.43% CAGR over 2026-2031.

This report is Segmented by Product Type (Smart Car Keys, Smart Door Keys and Lock-Linked Credentials, Mobile-Based and Virtual Keys, and More), Technology (RFID, Bluetooth and BLE, NFC, Wi-Fi, and More), Authentication Method (Smartphone-Based Access, and More), End-User Industry (Automotive, Residential, Hospitality, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Smart Key Market Trends and Insights

Rising Smart Home Penetration In Urban Asia-Pacific Households

Rising smart home adoption in dense urban areas is expanding the addressable market for residential access systems across the region. The strongest demand is emerging where developers, landlords, and managed rental operators can bundle access into the broader digital home offer rather than sell it as a standalone device purchase. This speeds up replacement cycles in premium apartments and professionally managed properties, while new construction enables more direct installation during construction. It also raises the value of brands that can tie locks, credentials, user permissions, and resident support into a single service layer, rather than competing solely on hardware price. In the Asia-Pacific smart key market, residential demand is increasingly shaped by institutional buyers such as developers and property managers, shortening rollout timelines and shifting pricing power toward platform-led vendors. That change also favors suppliers that can support recurring credential management, remote provisioning, visitor access, and lifecycle service over the full occupancy period.

Hospitality Shift Toward Contactless Guest Access And Mobile Keys

Hospitality operators across the region are moving toward contactless access because it reduces reliance on the front desk and removes friction at guest arrival. Mitsui Fudosan introduced Room Key in Apple Wallet across its Mitsui Garden Hotels and sequence hotel brands in March 2026 using Vingcard's Vostio cloud-based access management system and MIFARE 2GO credentials. This kind of rollout shows that hotels are no longer evaluating locks in isolation, because the real decision now includes credential delivery, cloud orchestration, and property system compatibility. Wallet-based entry also matters because it lowers the user barrier that comes with proprietary app downloads and account setup, which can slow guest participation. In the Asia-Pacific smart key market, hotel adoption has become a visible proof point for mobile credentials and is helping normalize phone-based access across other settings such as serviced apartments and enterprise spaces. Vendors that can link door hardware, credential issuance, and hotel workflow software are therefore better placed to capture the next phase of hospitality spending.

High Upfront Retrofit And Integration Costs

High retrofit and integration costs continue to limit broader deployment, especially in older buildings and smaller property portfolios that lack a clear budget for connected access. The challenge is usually broader than the lock itself, because deployment may also require upgrades to doors, power, networking, credential-issuance workflows, and local service capabilities. This is a larger problem in tier-2 and tier-3 cities, where building stock is more varied, and installers may need to make more site-level modifications before a rollout can begin. Recurring software fees also matter, because portfolio operators have to evaluate not only the first installation cost but also the monthly expense of managing many doors across several sites. As a result, adoption tends to concentrate first in new construction, premium hospitality, enterprise campuses, and developer-led projects that can absorb the full software and service stack. In the Asia-Pacific smart key market, this cost profile narrows the practical retrofit base, even as user interest and technology readiness both improve.

Other drivers and restraints analyzed in the detailed report include:

- Continued OEM Adoption of Connected Vehicle Digital Keys

- Enterprise Retrofit Demand For Cloud-Based Access Control

- Cybersecurity And Credential Spoofing Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart Car Keys held 48.33% of the Asia-Pacific smart key market share in 2025, which made automotive the largest product segment by a clear margin. That lead reflects the long history of OEM investment in remote entry, immobilizer-linked systems, and increasingly phone-based digital access tools. By the end of 2025, CCC certification covered products from 16 automakers, and APAC brands were firmly represented in that base. This scale gave the automotive segment the deepest installed footprint and kept it central to supplier volume, standards participation, and ecosystem visibility. At the same time, automotive growth remains tied to vehicle launch cycles, supplier validation windows, and production schedules, so its maturity imposes natural limits on how quickly it can outpace other credential categories.

Mobile-Based and Virtual Keys are forecast to grow at a 9.03% CAGR through 2031, pointing to a stronger software- and wallet-led growth path within the broader category. Allegion stated in 2026 that Aliro 1.0 creates a standardized model for mobile credentials and reader communication across Apple, Google, and Samsung wallet environments. Smart Door Keys and lock-linked credentials remain important because residential and commercial buildings provide the widest non-automotive installed base, while Smart Key Fobs, Cards, and Wearables still fit institutional workflows where shared or temporary access is common. In the Asia-Pacific smart key market, this mix suggests that hardware volume will remain broad, but the commercial center of gravity is moving toward software control, credential portability, and recurring service value. The Asia-Pacific smart key industry is therefore being reshaped less by the presence of a new lock format and more by who controls the credential layer that sits above the device.

RFID accounted for 34.87% of the Asia-Pacific smart key market in 2025, reflecting its long-established role in hospitality locks, office access cards, and transit-linked credential environments. Its position remains strong because operators understand the workflow, staff know how to issue credentials, and many sites already have readers that are expensive to replace quickly. In practical terms, this gives RFID a durable role across mid-market hotels, corporate facilities, institutional sites, and mixed-use buildings where reliability matters more than feature novelty. The installed base is especially relevant in mature environments where card-centric access has become routine, and replacement cycles are long. That means a large part of the current technology transition is happening through hybrid stacks rather than through abrupt migration away from existing RFID-supported infrastructure.

Bluetooth Low Energy is forecast to grow at 9.43% CAGR through 2031 and is becoming the preferred layer for proximity-based and wallet-driven access experiences. The Car Connectivity Consortium expanded Digital Key certification to include BLE and UWB, which supports more seamless hands-free and cross-device use cases. NFC still plays a strong supporting role because tap-based access remains familiar and dependable, while Wi-Fi continues to matter for remote management, provisioning, and firmware updates rather than as the main credential channel. In the Asia-Pacific smart key market, technology competition is shifting from basic connectivity claims to a more practical test that centers on interoperability, reader compatibility, credential handoff, and the overall quality of the user journey. The Asia-Pacific smart key industry is therefore moving toward multi-protocol architectures in which the most successful vendors are likely to be those that simplify complexity for operators rather than those that promote a single wireless standard.

List of Companies Covered in this Report:

- ASSA ABLOY AB

- Allegion plc

- dormakaba Holding AG

- SALTO Systems, S.L.

- MIWA Lock Co., Ltd.

- ZKTeco Co., Ltd.

- igloohome Pte Ltd.

- U-tec Group Inc.

- OpenKey, Inc.

- Blockchain Lock Inc.

- KEYU Intelligence Co., Ltd.

- Nuki Home Solutions GmbH

- LOQED B.V.

- Latch, Inc.

- Kisi, Inc.

- Shenzhen Kaadas Intelligent Technology Co., Ltd.

- Guangdong Be-Tech Security Systems Co., Ltd.

- SimonsVoss Technologies GmbH

- Gantner Electronic GmbH

- Onity, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Smart Home Penetration in Urban Asia-Pacific Households

- 4.2.2 Hospitality Shift Toward Contactless Guest Access and Mobile Keys

- 4.2.3 Enterprise Retrofit Demand for Cloud-Based Access Control

- 4.2.4 Continued OEM Adoption of Connected Vehicle Digital Keys

- 4.2.5 Expansion of Co-Living, Short-Stay Rentals, and Unmanned Space Formats

- 4.2.6 Insurance and Compliance Push for Audit-Ready Access Logs

- 4.3 Market Restraints

- 4.3.1 High Upfront Retrofit and Integration Costs

- 4.3.2 Cybersecurity and Credential Spoofing Risks

- 4.3.3 Fragmented Interoperability Across Property, Wallet, and Vehicle Ecosystems

- 4.3.4 Installer and After-Sales Capability Gaps Outside Tier-1 Cities

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Smart Car Keys

- 5.1.2 Smart Door Keys and Lock-Linked Credentials

- 5.1.3 Mobile-Based and Virtual Keys

- 5.1.4 Smart Key Fobs, Cards, and Wearables

- 5.2 By Technology

- 5.2.1 RFID

- 5.2.2 Bluetooth and BLE

- 5.2.3 NFC

- 5.2.4 Wi-Fi

- 5.2.5 Biometric Authentication

- 5.3 By Authentication Method

- 5.3.1 Smartphone-Based Access

- 5.3.2 Key Fob-Based Access

- 5.3.3 Card Key-Based Access

- 5.3.4 Keypad and PIN-Based Access

- 5.3.5 Biometric-Based Access

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Residential

- 5.4.3 Hospitality

- 5.4.4 Enterprise and Commercial Buildings

- 5.4.5 Industrial and Public Infrastructure

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASSA ABLOY AB

- 6.4.2 Allegion plc

- 6.4.3 dormakaba Holding AG

- 6.4.4 SALTO Systems, S.L.

- 6.4.5 MIWA Lock Co., Ltd.

- 6.4.6 ZKTeco Co., Ltd.

- 6.4.7 igloohome Pte Ltd.

- 6.4.8 U-tec Group Inc.

- 6.4.9 OpenKey, Inc.

- 6.4.10 Blockchain Lock Inc.

- 6.4.11 KEYU Intelligence Co., Ltd.

- 6.4.12 Nuki Home Solutions GmbH

- 6.4.13 LOQED B.V.

- 6.4.14 Latch, Inc.

- 6.4.15 Kisi, Inc.

- 6.4.16 Shenzhen Kaadas Intelligent Technology Co., Ltd.

- 6.4.17 Guangdong Be-Tech Security Systems Co., Ltd.

- 6.4.18 SimonsVoss Technologies GmbH

- 6.4.19 Gantner Electronic GmbH

- 6.4.20 Onity, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment