|

시장보고서

상품코드

2061549

호흡 모니터링 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Respiratory Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

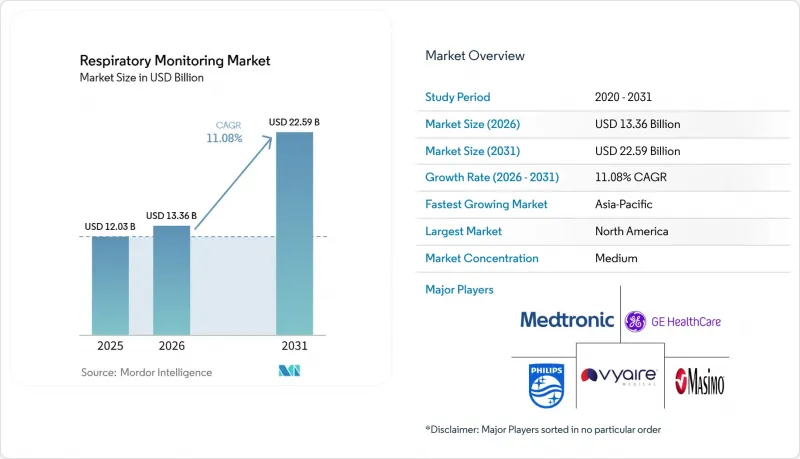

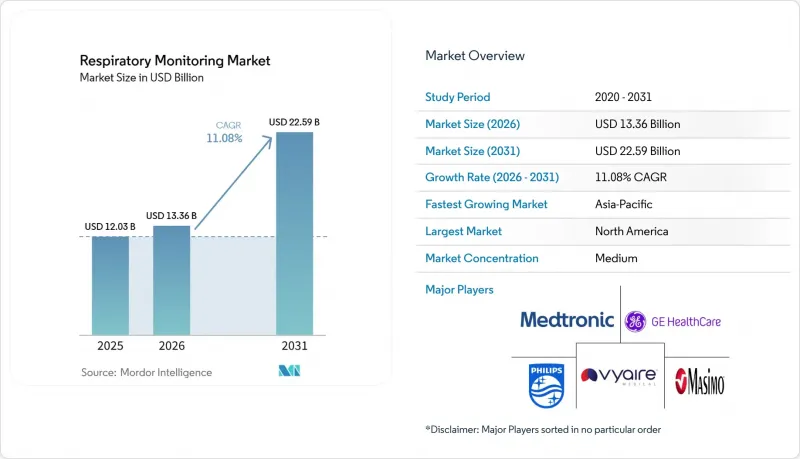

Mordor Intelligence에 의하면, 호흡 모니터링 시장 규모는 2025년 120억 3,000만 달러로 평가되었습니다. 2026년 133억 6,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 11.08%를 나타내, 2031년까지 225억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 기기 유형(스파이로미터, 피크 유량계, 맥박 산소 포화도 측정기 등), 기술(웨어러블 호흡 센서 및 비웨어러블/탁상형·휴대용 기기), 최종 사용자(병원 및 진료소, 재택 간호 환경 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 호흡 모니터링 시장 동향 및 인사이트

AI를 활용한 원격 호흡 모니터링 도입이 급증하고 있습니다.

호흡 모니터링 시장은 AI 분석 기술이 조사 기관에서 호흡음, 유량, 산소 포화도를 실시간으로 처리하는 상용 플랫폼으로 전환됨에 따라 변화를 겪고 있습니다. 『Annals of Family Medicine』지에 실린 연구에 따르면, AI가 탑재된 가정용 청진기는 소아 천식의 급성 악화를 93.2%의 정확도로 식별할 수 있는 것으로 나타났습니다. 종단적 데이터셋을 통해 학습된 알고리즘은 현재 만성폐쇄성폐질환(COPD) 악화 직전에 나타나는 미묘한 패턴 변화를 감지하여 조기 치료 조정을 촉진하고, 응급실 이용을 줄이고 있습니다. 병원에서는 이러한 예측 대시보드를 전자의무기록에 통합하여, 임상 중증도 점수에 따라 의료진에게 자동 알림을 보낼 수 있도록 하고 있습니다. 마찬가지로, 각 벤더사들도 엣지 측에서 데이터를 익명화하는 페더레이티드 러닝 기술을 적용하여, 인사이트의 질을 저하시키지 않으면서도 개인정보 보호 규제를 준수하고 있습니다. 능동적인 자가 보고가 어려운 소아 및 고령 환자층에게 있어, 수동적인 AI 청취 시스템은 기존의 폐기능 검사를 대체할 수 있는 부담이 적은 대안이 됩니다.

호흡기 질환 증가

세계적으로 만성폐쇄성폐질환(COPD)와 천식의 유병률이 증가하고 있으며, 2025년에는 만성 호흡기 질환이 장애 조정 생명년(DALY)의 상위 5대 원인으로 꼽혔습니다. 보험사는 재입원 감소 실적과 보상 보너스를 연계함으로써, 의료 제공업체가 지속적인 모니터링 체계를 도입하도록 장려하고 있습니다. 이에 반해, 호흡기 모니터링 시장에서는 산소 포화도, 기류, 음향 분석을 결합한 다중 매개변수 장치가 등장하여, 증상에 기반한 단계적 대응 모델보다 더 조기에 염증 반응을 포착할 수 있게 되었습니다. 호기 응축액 속의 아질산염을 검출하는 캘리포니아 공과대학의 ‘EBCare’ 마스크는 바이오마커 감지 기술이 연구 단계에서 임상 현장으로 넘어가고 있음을 보여주는 좋은 사례입니다. 호흡기내과 의사들은 현재 웨어러블 데이터를 위험도 계층화 알고리즘에 반영하고, 흡입용 코르티코스테로이드 투여량을 동적으로 조정함으로써 급성기 의료 이용 건수가 현저히 감소했음을 입증하고 있습니다. 질병 부담이 큰 국가의 정부는 COPD 환자를 위한 원격 모니터링 키트에 대한 지원을 제공하는 공공 조달 제도를 도입하여, 조기 개입을 보장하고 3차 의료의 부담을 줄이고 있습니다.

엄격한 규제 승인

리콜 이후의 혼란으로 인해 FDA의 심사가 더욱 엄격해졌으며, 호흡 모니터링 기기는 안전 감시의 최전선에 자리 잡게 되었습니다. 클래스 II 의료기기의 경우, 개정된 510(k) 지침에 따라 확장된 벤치 테스트 및 시판 후 조사 프로토콜의 제출이 의무화되어 있습니다. 2024년 Philips 레스피로닉스(Philips Respironics)에 대한 합의 판결은 규정 준수 위반이 초래하는 재정적·평판상의 위험을 여실히 드러내고 있습니다. 그 결과, 중소 혁신 기업들은 검증 주기가 장기화되면서 자본 여력이 압박받고, 수익 창출이 지연되는 상황에 직면해 있습니다. 위험을 줄이기 위해 벤처 투자자들은 프로토타입 단계부터 ‘품질 설계(QbD)’를 문서화한 스타트업에 자금을 지원하고 있습니다. 일부 제조업체들은 심사를 가속화하기 위해 ‘획기적인 의료기기’ 지정을 목표로 하고 있지만, 증거 제출에 따른 부담은 여전히 크습니다. 유럽에서도 의료기기 규정(MDR) 준수에 따라 문서화 기준이 마찬가지로 강화되었으며, 번역 비용과 인증 기관에 지불하는 비용이 추가되면서 이익률이 압박받고 있습니다.

부문별 분석

맥박 산소 포화도 측정기는 2025년 호흡 모니터링 시장 점유율의 36.62%를 차지했으며, 외과, 중환자실, 외래 진료 등 각 현장에서 없어서는 안될 존재인 만큼, 2031년까지 최대 수익원으로 자리매김할 것으로 전망됩니다. 이러한 범용성, 비침습적 설계, 그리고 확립된 보험 급여 체계가 지속적인 수요를 뒷받침하고 있습니다. 이 부문의 혁신은 SpO2뿐만 아니라 관류 지수와 호흡수를 측정하는 다중 스펙트럼 센서에 초점을 맞추고 있으며, 업무 흐름을 방해하지 않으면서 임상적 가치를 높이고 있습니다. 또한, 각 벤더사는 데이터를 병원의 전자건강기록(EMR)으로 자동 전송하는 블루투스 지원 손가락 착용형 모델을 출시하여, 병동 내 지속적인 모니터링을 개선하고 있습니다.

카프노그래프는 시장 점유율은 작지만, 수술실 이외의 다양한 용도로의 확대에 힘입어 8.54%라는 가장 높은 예측 연평균 성장률(CAGR)을 보이고 있습니다. 응급실에서는 현재 소생 시 신속한 기도 평가를 위해 소형 메인스트림 센서가 도입되어 있으며, 처치용 진정실에서는 맥박 산소 포화도 측정보다 더 조기에 저환기를 감지하기 위해 카프노그래피가 활용되고 있습니다. 구급차에 탑재 가능한 크기의 휴대용 사이드스트림 장치는 병원 도착 전 환경 모니터링 범위를 확대하고 있으며, 이러한 기능은 고급 심폐소생술 프로토콜에서 점점 더 필수적인 요소가 되고 있습니다. 그 결과, 호흡 모니터링 시장에서는 맥박 산소 포화도 측정과 카프노그래피 모듈을 결합한 번들 판매 패키지가 등장하여, 외상 현장에서 종합적인 호흡 프로파일을 제공합니다.

지역별 분석

2025년, 북미는 전 세계 매출의 41.62%를 차지했습니다. 이는 안정적인 보험 급여, 확립된 원격의료 인프라, 그리고 성인의 6.3%에 육박하는 COPD 유병률을 반영한 것입니다. 미국의 호흡 모니터링 시장은 FDA의 ‘브레이크스루 디바이스 프로그램’의 혜택을 받고 있습니다. 이 프로그램은 패혈증 선별 검사를 받은 중환자실 환자를 위한 예측 카프노그래피 알고리즘 등, AI를 활용한 솔루션의 도입을 가속화하고 있습니다. 2025년 Philips와 매사추세츠 종합병원·브리검 병원의 제휴와 같은 산학 협력을 통해, 대규모 실세계 데이터가 정교한 임상 판단 규칙으로 활용되면서 기기의 유용성이 향상되었습니다. 캐나다에서는 재택 산소 요법의 비용 부담을 줄이는 것을 장려하고 있으며, 각 주의 분석 허브에 데이터를 제공하는 전국적인 산소 포화도 추적 네트워크의 시범 운영을 진행하고 있습니다.

유럽에서는 국민보건서비스(NHS)의 조달 체계 내에서 비용 절감 효과가 입증된 의료기기가 우선적으로 선정되고 있으며, 공급업체에 대해 체계적인 의료경제학적 자료의 제출이 권장되고 있습니다. 독일의 DIGA 제도는 디지털 헬스 용도의 처방 허가를 가능하게 하고 있으며, 2024년부터 4개의 호흡기 관련 앱이 추가됨에 따라 스마트폰을 이용한 폐기능 검사에 대한 의사의 신뢰도가 높아지고 있습니다. 또한, 유럽의 호흡기 모니터링 시장은 의료기기 규정(MDR)의 시판 후 조사 요건에 따라 형성되고 있으며, 제조업체들은 의무화된 모니터링 보고 요건을 준수하는 장기 보증 업그레이드 사항을 사전에 패키지에 포함시켜야 하는 상황에 직면해 있습니다.

아시아태평양은 가장 빠른 성장세를 보이고 있으며, 도시화, 대기질 악화, 흡연율 상승이 맞물려 호흡기 질환 환자 수가 증가함에 따라 연평균 성장률(CAGR)은 14.01%로 성장을 지속하고, 있습니다. 중국과 인도는 2024년에 총 300만 대 이상의 휴대용 맥박 산소 포화도 측정기를 수입했으나, 의료 기술의 자급자족을 촉진하기 위한 정부의 인센티브 덕분에 국내 생산 능력이 급속히 확대되고 있습니다. 현지 스타트업은 비용 효율이 뛰어난 인쇄 전자를 활용해 50달러 미만의 센서를 개발함으로써, 지방 도시에서도 널리 사용할 수 있도록 하고 있습니다. 일본에서는 급속한 고령화를 배경으로, 스마트 스피커에 내장된 AI 기반 기침 모니터링 시스템의 도입이 확대되고 있어, 눈에 띄지 않는 방식으로 고령자 돌봄 상황을 모니터링할 수 있게 되었습니다. 호주의 외딴 지역에 위치한 원주민 커뮤니티에서는 위성 통신 기능을 갖춘 웨어러블 기기를 활용하여 폐 기능 측정 데이터를 대도시의 호흡기과 팀에 전송함으로써 지리적 격차를 해소하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the respiratory monitoring market size is expected to grow from USD 12.03 billion in 2025 to USD 13.36 billion in 2026 and is forecast to reach USD 22.59 billion by 2031 at 11.08% CAGR over 2026-2031.

This report is Segmented by Device Type (Spirometers, Peak Flow Meters, Pulse Oximeters, and More), Technology (Wearable Respiratory Sensors and Non-wearable/Table-top & Hand-Held Devices), End-User (Hospitals & Clinics, Home-Care Settings, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Respiratory Monitoring Market Trends and Insights

Surge in AI-Powered Remote Respiratory Telemonitoring Adoption

The respiratory monitoring market is transforming as AI analytics migrate from research labs into commercial platforms that process breath sounds, flow rates, and oxygen saturation in real time. An Annals of Family Medicine study showed AI-enabled home stethoscopes identifying pediatric asthma flare-ups with 93.2% accuracy. Algorithms trained on longitudinal data sets now detect subtle pattern deviations that precede COPD exacerbation, prompting earlier therapy adjustments and reducing emergency department utilization. Hospitals are integrating these predictive dashboards into electronic health records so that care teams receive automated alerts flagged by clinical severity scores. Vendors are likewise embedding federated-learning techniques that anonymize data at the edge, addressing privacy mandates without sacrificing insight quality. For pediatric and geriatric cohorts who struggle with active self-reporting, passive AI listening systems offer a less burdensome alternative to conventional spirometry.

Rise in the Number of Respiratory Diseases

Global COPD and asthma prevalence are climbing, with chronic respiratory disorders ranking among the top five causes of disability-adjusted life years in 2025. Payers are linking reimbursement bonuses to documented reductions in hospital readmissions, pushing providers to adopt continuous monitoring pathways. The respiratory monitoring market is answering with multi-parameter devices that combine oximetry, airflow, and acoustic analytics to catch inflammatory events sooner than symptom-based escalation models. Caltech's EBCare mask, which detects nitrite in exhaled breath condensate, exemplifies how biomarker sensing is moving from bench to bedside. Pulmonologists now embed wearable data into risk-stratification algorithms that dynamically adjust inhaled corticosteroid dosage, demonstrating measurable declines in acute care visits. Governments in high-burden countries are launching public procurement schemes to subsidize remote monitoring kits for COPD patients, ensuring earlier intervention and easing tertiary-care loads.

Stringent Regulatory Approval

Post-recall turbulence has intensified FDA scrutiny, elevating respiratory monitoring devices to the forefront of safety oversight. Class II devices must now submit expanded bench testing and post-market surveillance protocols under updated 510(k) guidance. The 2024 consent decree against Philips Respironics underscores the financial and reputational stakes of non-compliance. Consequently, small innovators face protracted validation cycles that strain capital reserves and delay revenue realization. To mitigate risk, venture investors are channeling funds toward start-ups that embed quality-by-design documentation from the prototype phase onward. Some manufacturers are pursuing Breakthrough Device designation to accelerate review, though the evidence burden remains significant. In Europe, alignment with the Medical Device Regulation has likewise raised documentary thresholds, adding translation and notified-body costs that pinch margins.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Smartphone-Based Spirometry Apps Driving Early COPD Detection

- High Prevalence of Tobacco Smoking

- High Price of the Monitoring Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pulse oximeters contributed 36.62% to the respiratory monitoring market share in 2025 and are projected to maintain the largest revenue pool through 2031 due to their essential status across surgical, critical-care, and ambulatory settings. Their universal applicability, non-invasive design, and established reimbursement paths underpin durable demand. The segment's innovation pipeline centers on multispectral sensors that capture perfusion index and respiratory rate, alongside SpO2, adding clinical value without disrupting workflow. Vendors are also rolling out Bluetooth-enabled fingertip models that auto-transmit data to hospital EMRs, improving continuous ward surveillance.

Capnographs, although representing a smaller share, exhibit the highest forecast CAGR at 8.54%, driven by broader application beyond operating rooms. Emergency departments now deploy compact mainstream sensors for rapid airway assessment during resuscitation, while procedural sedation suites rely on capnography to flag hypoventilation earlier than pulse oximetry. Portable sidestream units sized for ambulances are extending monitoring into pre-hospital environments, a capability increasingly mandated in advanced life-support protocols. The respiratory monitoring market is consequently witnessing bundled sales packages that combine oximetry and capnography modules, offering a holistic respiratory profile in trauma settings.

Geography Analysis

North America accounted for 41.62% of global revenue in 2025, reflecting robust payer reimbursement, entrenched telemedicine infrastructure, and a COPD prevalence nearing 6.3% of adults. The respiratory monitoring market in the United States benefits from the FDA Breakthrough Device Program, which accelerates AI-driven solutions such as predictive capnography algorithms for sepsis-screened ICU patients. Academic-industry collaborations, like the 2025 Philips-Mass General Brigham partnership, channel large real-world data pools into refined clinical-decision rules that elevate device utility. Canada, incentivizing home oxygen therapy cost offsets, is piloting nationwide oximetry tracking networks that feed provincial analytics hubs.

In Europe, National Health Service procurement frameworks favor devices with proven cost-avoidance outcomes, encouraging vendors to supply structured health-economic dossiers. Germany's DIGA pathway, allowing prescription of digital health applications, has added four respiratory apps since 2024, boosting physician confidence in smartphone spirometry. The European respiratory monitoring market is also shaped by the Medical Device Regulation's post-market surveillance demands, prompting manufacturers to pre-package long-term warranty upgrades that align with mandatory vigilance reporting.

Asia Pacific exhibits the fastest expansion, logging a 14.01% CAGR as urbanization, air-quality deterioration, and smoking prevalence converge to swell respiratory caseloads. China and India collectively imported over 3 million handheld oximeters in 2024, yet domestic production capacity is scaling rapidly with government incentives for med-tech self-reliance. Local start-ups leverage cost-efficient printed electronics to create sub-USD 50 sensors, democratizing access across tier-2 cities. In Japan, a rapidly aging population is driving the adoption of AI-augmented cough monitors integrated into smart speakers, offering unobtrusive elder-care oversight. Australia's remote Indigenous communities benefit from satellite-enabled wearables that transmit lung function metrics to metropolitan pulmonology teams, bridging the tyranny of distance.

- Koninklijke Philips

- Medtronic plc (Covidien)

- GE Healthcare

- Masimo

- Dragerwerk

- Vyaire Medical

- Nihon Kohden

- Smiths Group

- Resmed

- Hamilton Medical

- Getinge

- Fisher & Paykel Healthcare

- Nonin Medical

- Honeywell International (Healthcare Sensors)

- Hill-Rom (Baxter)

- AirSep Corporation (CAIRE Inc.)

- VitalConnect Inc.

- Microlife Corp.

- Mindray Bio-Medical Electronics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI-Powered Remote Respiratory Telemonitoring Adoption

- 4.2.2 Rise in the Number of Respiratory Diseases

- 4.2.3 Rise of Smartphone-Based Spirometry Apps Driving Early COPD Detection and Development of Advanced Technologies

- 4.2.4 High Prevalence of Tobacco Smoking

- 4.2.5 Government-Funded Neonatal Respiratory Screening Programs across Nordic Nations

- 4.2.6 Stringent Workplace Safety Mandates Accelerating Continuous Respiratory Monitoring in Industrial Settings

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Approval

- 4.3.2 High Price of the Monitoring Devices

- 4.3.3 Supply-Chain Bottlenecks for Micro-Optical Sensors Driving Device Backlogs

- 4.3.4 High Calibration-Frequency Requirement Limiting Wearable Gas Analyzer Acceptance in Pediatric Care

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Spirometers

- 5.1.2 Peak Flow Meters

- 5.1.3 Sleep Test Devices (Polysomnographs)

- 5.1.4 Gas Analyzers

- 5.1.5 Pulse Oximeters

- 5.1.6 Capnographs

- 5.1.7 Other Monitoring Devices

- 5.2 By Technology

- 5.2.1 Wearable Respiratory Sensors

- 5.2.2 Non-wearable/Table-top & Hand-held Devices

- 5.3 By End-user

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home-care Settings

- 5.3.3 Ambulatory Surgical & Specialty Centers

- 5.3.4 Emergency Medical Services & Field Use

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Koninklijke Philips N.V.

- 6.3.2 Medtronic plc (Covidien)

- 6.3.3 GE Healthcare

- 6.3.4 Masimo Corporation

- 6.3.5 Dragerwerk AG & Co. KGaA

- 6.3.6 Vyaire Medical, Inc.

- 6.3.7 Nihon Kohden Corporation

- 6.3.8 Smiths Medical (ICU Medical)

- 6.3.9 ResMed Inc.

- 6.3.10 Hamilton Medical AG

- 6.3.11 Getinge AB

- 6.3.12 Fisher & Paykel Healthcare

- 6.3.13 Nonin Medical Inc.

- 6.3.14 Honeywell International (Healthcare Sensors)

- 6.3.15 Hill-Rom (Baxter)

- 6.3.16 AirSep Corporation (CAIRE Inc.)

- 6.3.17 VitalConnect Inc.

- 6.3.18 Microlife Corp.

- 6.3.19 Mindray Bio-Medical Electronics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment