|

시장보고서

상품코드

2061583

샘플 조제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Sample Preparation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

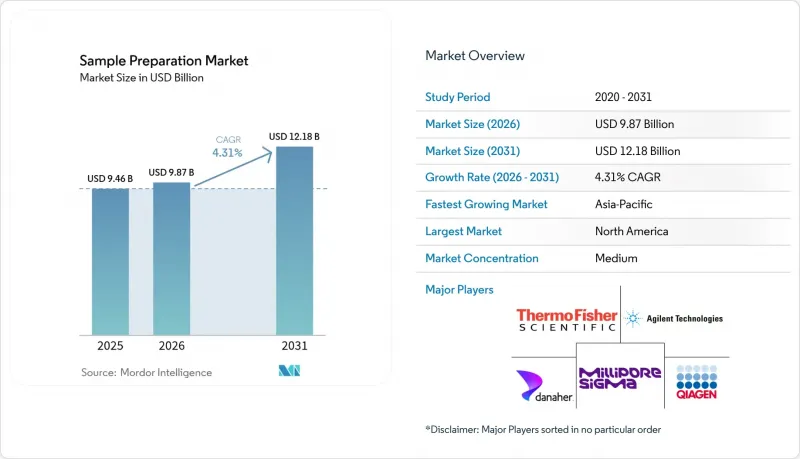

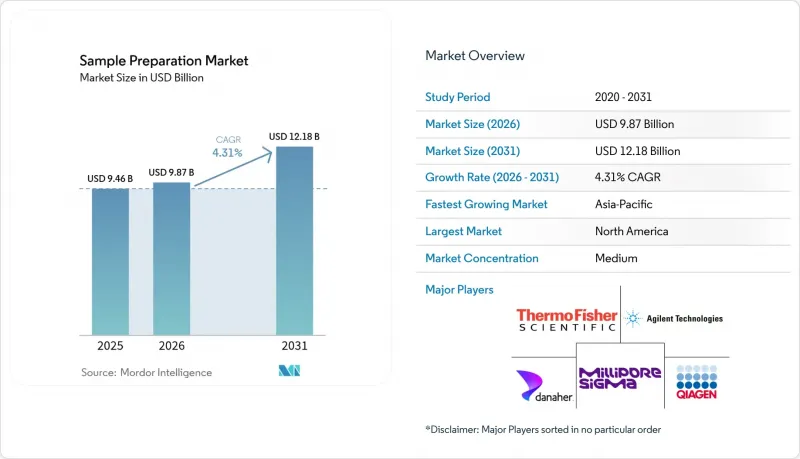

Mordor Intelligence에 의하면, 세계의 샘플 조제 시장 규모는 2025년 94억 6,000만 달러로 평가되었습니다. 2026년에는 98억 7,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 4.31%를 나타내, 2031년에는 121억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품(샘플 조제 장비, 소모품 등), 기술(수동, 반자동 등), 용도(유전체학, 단백질체학, 후성유전체학 등), 최종 사용자(제약 회사, 생명공학 기업 등) 및 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 샘플 조제 시장 동향 및 분석

오믹스 연구 및 정밀 의학에 대한 전 세계적 투자 급증

멀티오믹스 데이터를 전자의무기록에 통합하는 것은 데이터 조화 측면에서 상당한 진전을 가져왔으며, 첨단 샘플 조제 기술에 대한 수요를 촉진하고 있습니다. 통합 유전체학 및 단백체학 대시보드를 도입한 병원들은 분석 결과의 편차 원인 중 하나로 시료 불일치를 중요한 요인으로 지목하고 있습니다. 이러한 과제를 해결하기 위해, 다양한 검체 유형에 걸쳐 추출 효율을 표준화하고 신뢰할 수 있는 결과를 보장하며, 실용적인 바이오마커를 식별할 수 있도록 하는 검증된 키트 기반 워크플로우를 도입하는 추세가 점점 더 확산되고 있습니다. 이러한 변화가 샘플 조제 시장을 주도하고 있으며, 각 공급업체들은 차세대 시퀀싱 및 고분해능 질량 분석 플랫폼 모두와의 호환성을 확보하기 위해 자사 화학 시약의 인증 획득에 주력하고 있습니다. 추적성에 대한 공통된 요구 사항에 힘입어, 임상 실험실과 연구소의 경계가 점점 더 모호해짐에 따라 시장 역학도 변화하고 있습니다. 이에 대응하여 규제 당국은 사전 분석 변수에 관한 지침을 개정하고 있으며, 규정 준수 관련 과제가 증가함에 따라 신규 시장 진출기업의 진입 장벽이 높아지고 있습니다.

자동화된 고처리량 검체 전처리에 대한 수요가 증가함에 따라 검사실의 생산성이 향상됩니다.

검사 건수 증가와 인력 부족에 대응하기 위해, 검사실에서는 96웰 또는 384웰 플레이트를 1시간 이내에 처리할 수 있는 자동 액체 처리 시스템에 대한 투자를 확대되고 있습니다. 자동화는 전략적 자산임이 입증되었으며, 단백질체학 워크플로우에서 시료 간 편차를 1.8배 감소시켜 품질과 생산성을 모두 향상시키고 있습니다. 이러한 추세가 샘플 조제 시장의 성장을 주도하고 있으며, 하드웨어 OEM 제조업체와 시약 전문 기업이 전략적 제휴를 맺고, 최종 사용자의 검증 부담을 줄여주는 턴키 솔루션을 제공합니다. 이 기술을 조기에 도입한 기업에 따르면, 기술 인력을 반복적인 피펫팅 작업에서 데이터 분석 업무로 재배치함으로써 직원들의 사기가 향상될 뿐만 아니라, 보고서 작성 소요 시간도 단축된다고 합니다. 이는 수탁 연구 시장에서 매우 중요한 경쟁 우위가 됩니다. 그 결과, 조달위원회는 보다 종합적인 평가 체계를 도입하여, 처리량 지표뿐만 아니라 기회 비용 절감도 고려하여 투자 수익률(ROI)을 평가했습니다. 이러한 관점의 진화로 인해 반자동화 플랫폼에서 완전 자동화 플랫폼으로의 전환이 가속화되고 있으며, 이는 시장의 확산을 더욱 촉진하고 있습니다.

전자동 샘플 조제 플랫폼의 높은 설비 투자 비용 및 운영 비용

종합 워크스테이션의 높은 비용(대개 10만 달러를 초과함)은 소규모 연구소나 가격에 민감한 지역에게 큰 장벽이 되어 시장 보급에 영향을 미치고 있습니다. 또한, 서비스 계약, 교정, 전용 소모품을 포함한 연간 운영비는 워크스테이션 정가의 15%에서 20%를 차지하고 있어, 연구소는 신중한 예산 편성 전략을 수립할 수밖에 없습니다. 이러한 비용 구조로 인해 샘플 조제 시장은 양극화되고 있습니다. 처리량이 많은 진단센터는 고가의 장비 투자를 정당화할 수 있는 반면, 지역 병원은 비용 효율성을 극대화하기 위해 모듈식 시스템이나 시약 렌탈 모델을 선호하는 경향이 있습니다. 이에 대응하여 각 벤더사는 옵션 모듈을 지원하도록 설계된 코어 덱을 갖춘 확장성 있는 시스템을 전략적으로 출시하고 있습니다. 이러한 시스템을 통해 검사실은 수요 증가에 따라 자성 비드 유닛이나 진공 여과 유닛을 추가할 수 있어, 변화하는 운영 요구 사항에 대응할 수 있습니다. 이러한 모듈성은 자산의 수명을 연장할 뿐만 아니라, 기술적 노후화의 위험을 줄이고, 중고 장비 시장에서의 재판매 가치를 높여 시장 경쟁력을 강화합니다.

부문별 분석

2025년, 시약 및 소모품은 샘플 조제 시장을 독점하며 53.78%의 점유율을 확보해 공급업체에게 가장 큰 수익원이 되었습니다. 이러한 확고한 입지는 일관된 재구매 주기에 기인합니다. 각 검사에는 추출 컬럼, 비드 또는 버퍼 키트가 필요하기 때문에 자본 설비의 사이클에 영향을 받지 않는 안정적인 현금 흐름이 확보됩니다. 소모품 분야에서 샘플 조제 키트는 2026년부터 2031년까지 연평균 성장률(CAGR) 9.02%를 기록하며, 일반 시약의 성장률을 상회할 것으로 전망됩니다. 이러한 변화는 연구소에서 운영자 간 편차를 줄여주는 검증된 기법을 사용하는 키트를 선호하는 경향에서 비롯된 것입니다. 이러한 추세는 특히 액체 생검 워크플로우에서 두드러지며, 무세포 DNA 추출용으로 설계된 키트는 극소량의 혈장에서도 뛰어난 회수율을 보여주고 있습니다. 또한, 연구소가 특정 장비에 연계된 독자적인 화학 기술을 도입하면 소모품에 대한 가격 결정력이 강화됩니다. 이러한 추세에 따라 공급업체들은 자사 플랫폼과 물리적 또는 전자적으로 호환되는 카트리지 및 컬럼을 개발하도록 유도받고 있으며, 이는 고객 충성도 향상으로 이어지고 있습니다.

2025년 기준으로 반자동 기술은 샘플 조제 시장에서 46.85%의 점유율을 차지했으며, 업무 체계를 대폭 개편하지 않으면서도 적정한 처리 능력 향상을 원하는 검사실에서 선호되고 있습니다. 이러한 시스템은 대개 탁상형 자성 비드 프로세서와 수동 피펫팅 스테이션을 통합하여 비용과 성능의 균형을 맞추고 있습니다. 그러나 인건비 상승과 엄격한 재현성 기준을 배경으로, 완전 자동화 플랫폼 시장은 2031년까지 연평균 성장률(CAGR) 10.22%를 나타낼 것으로 전망됩니다. 완전 자동화 솔루션을 도입한 연구소에서는 추적성 향상 및 교차 오염 감소와 같은 추가적인 이점이 자주 강조되고 있으며, 이러한 이점들은 모두 비용이 많이 드는 재분석을 줄이는 데 기여합니다. 또한, 소프트웨어 업데이트를 통해 새로운 프로토콜이 원격으로 도입됨에 따라 자동화 하드웨어의 수명이 연장되고 있어, 총 소유 비용(TCO)을 평가하는 예산 위원회에게 더욱 매력적인 선택지가 되고 있습니다.

지역별 분석

북미는 강력한 연방 연구 보조금, 차세대 실험실 자동화의 신속한 도입, 그리고 바이오의약품 기업 본사의 집중에 힘입어 35.10%의 시장 점유율로 샘플 조제 시장을 선도하고 있습니다. FDA 및 CLIA 기준에 기반한 해당 지역의 규제 체계는 분석 전 품질 관리를 의무화하고 있으며, 이는 표준화된 키트와 추적 가능한 워크플로우에 대한 수요를 이끌고 있습니다. QIAGEN과 Bio-Manguinhos/Fiocruz간의 제휴와 같은 파트너십은 기존 공급업체들이 북미의 솔루션을 신흥 공중보건 시장에 적용하려는 노력을 잘 보여주고 있으며, 이를 통해 세계 입지를 강화하고 다양한 자원에 맞춘 제품 개발을 촉진하고 있습니다. 그 결과, 차별화를 꾀하는 학술 의료 센터들은 단일 세포 멀티오믹스 플랫폼에 대한 투자를 확대되고 있습니다. 이로 인해 장비 도입 대수가 정체되는 상황에서도 소모품 처리 능력은 향상되고 있습니다. 지역 시장에서는 인증 주기에 맞추어 문서화 작업을 효율화하는 통합형이자 규정 준수를 중시하는 솔루션이 주류를 이루고 있습니다.

아시아태평양은 제약 생산의 급증과 국내 생명공학 생태계를 강화하기 위한 정부의 강력한 인센티브에 힘입어 가장 빠른 성장세를 보이고 있습니다. 중국의 5개년 계획에서는 하이엔드 장비에 막대한 자금이 배정되어 있으며, 이에 따라 현지 연구소들은 중간 단계를 건너뛰고 완전 자동화된 워크플로를 도입하고 있습니다. 일본과 한국에서는 고령화가 진행됨에 따라, 특히 종양학 및 유전성 질환 분야의 분자진단 검사 수요가 증가하고 있습니다. 현지 언어를 지원하는 소프트웨어와 소용량 시약 팩의 부상은 핵심 화학 공정을 유지하면서도 지역별 맞춤화를 통해 시장 점유율을 확보할 수 있는 가능성을 여실히 보여주고 있습니다. 특히, 최근의 지정학적 혼란은 공급망의 회복탄력성이 얼마나 중요한지 부각시키고 있으며, 다국적 기업들은 수주를 확보하기 위해 이 지역에 생산 거점을 설립하도록 장려받고 있습니다.

유럽의 샘플 조제 업계는 ‘호라이즌 유럽’과 같은 이니셔티브 덕분에 활기를 띠고 있으며, 정밀한 시료 처리가 필요한 오믹스 프로젝트에 자금이 투입되고 있습니다. EU의 실험실 지속가능성 관련 규제는 친환경 소모품으로의 전환을 촉진하고 있으며, 공급업체들은 환경에 미치는 영향을 최소화하면서 동시에 수율을 극대화할 수 있는 키트를 개발해야 하는 상황에 놓여 있습니다. 산학 협력의 부상은 특수 추출 화학 기술의 개발을 가속화하고 있으며, 업계 주요 기업들과의 라이선싱 계약을 통해 성장하는 스타트업들을 탄생시키고 있습니다. 동시에, GDPR(EU 개인정보보호규정)에 따른 엄격한 데이터 보호 요건으로 인해 보안과 감사 대응 기능을 모두 갖춘 기기용 소프트웨어에 대한 수요가 증가하고 있으며, 기존의 성능 기준에 더해 조달 결정 기준도 변화하고 있습니다. 이러한 동향들이 맞물리면서, 유럽은 전 세계 규제 및 지속가능성 흐름을 주도하는 중심적인 역할을 더욱 공고히 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the global sample preparation market size is expected to grow from USD 9.46 billion in 2025 to USD 9.87 billion in 2026 and is forecast to reach USD 12.18 billion by 2031 at 4.31% CAGR over 2026-2031.

This report is Segmented by Product (Sample-Preparation Instruments, Consumables, and More), Technology (Manual, Semi-Automated, and More), Application (Genomics, Proteomics, Epigenomics, and More), End-User (Pharmaceutical Companies, Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Sample Preparation Market Trends and Insights

Surging Global Investment in Omics Research and Precision-Medicine

The integration of multi-omics data into electronic medical recordsis driving significant advancements in data harmonization, fueling the demand for sophisticated sample preparation technologies. Hospitals that deploy unified genomics and proteomics dashboards have identified sample inconsistencies as a critical factor contributing to analytical variances. To address this challenge, they are increasingly adopting validated, kit-based workflows that standardize extraction efficiencies across various specimen types, ensuring reliable results and enabling the identification of actionable biomarkers. This shift is propelling the sample preparation market, with vendors striving to certify their chemistries for compatibility with both next-generation sequencing and high-resolution mass spectrometry platforms. The growing overlap between clinical and research laboratories, driven by shared requirements for traceability, is reshaping market dynamics. In response, regulatory bodies are updating guidelines on pre-analytical variables, creating additional compliance challenges and raising the entry barriers for new market players.

Growing Demand for Automated, High-Throughput Sample-Prep to Boost Laboratory Productivity

In response to rising test volumes and staffing shortages, laboratories are increasingly investing in automated liquid-handling stations capable of processing 96- or 384-well plates in under an hour. Automation is proving to be a strategic asset, delivering a 1.8-fold reduction in sample-to-sample variation for proteomics workflows, thereby enhancing both quality and productivity. This trend is driving growth in the sample preparation market, with hardware OEMs and reagent specialists forming strategic partnerships to offer turnkey solutions that reduce the validation burden for end users. Early adopters report that reallocating technicians from repetitive pipetting tasks to data interpretation not only improves workforce morale but also shortens report-generation timelines, a critical competitive advantage in the contract-research market. Consequently, procurement committees are adopting a broader valuation framework, assessing return on investment not only through throughput metrics but also by factoring in opportunity cost savings. This evolving perspective is accelerating the shift from semi-automated to fully automated platforms, further driving market adoption.

High Capital and Operating Costs of Fully Automated Sample-Prep Platforms

High costs of comprehensive workstations, often exceeding USD 100,000, create a significant barrier for small laboratories and price-sensitive regions, impacting market adoption. Additionally, annual operating expenditures, including service contracts, calibrations, and proprietary consumables, account for 15% to 20% of the workstation's list price, driving laboratories to adopt cautious budgeting strategies. This cost dynamic has segmented the sample preparation market: high-throughput reference centers justify investments in premium machines, while community hospitals prefer modular systems or reagent-rental models to optimize cost efficiency. In response, vendors are strategically launching scalable systems with core decks designed to accommodate optional modules. These systems allow laboratories to add magnetic-bead or vacuum-filtration units as demand grows, aligning with evolving operational needs. This modularity not only extends asset lifecycles but also reduces the risk of technological obsolescence, enhancing resale values in the secondary-equipment market and strengthening market competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Clinical Adoption of Genomic Sequencing and Liquid-Biopsy Diagnostics

- Expansion of Biopharma R&D and Manufacturing Volumes Requiring Robust Sample Preparation

- Shortage of Skilled Personnel to Operate and Maintain Sophisticated Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, consumables dominated the sample preparation market, securing a 53.78% share and emerging as the top revenue source for vendors. This stronghold is attributed to consistent repurchase cycles; each test relies on extraction columns, beads, or buffer kits, ensuring stable cash flows that remain unaffected by capital-equipment cycles. Within the consumables realm, sample-prep kits are projected to grow at a 9.02% CAGR from 2026 to 2031, surpassing the growth of general reagents. This shift is driven by laboratories' preference for method-validated kits, which reduce inter-operator variability. The trend is especially evident in liquid-biopsy workflows, where kits designed for cell-free DNA extraction achieve superior recovery from minimal plasma volumes. Furthermore, once a laboratory commits to a proprietary chemistry linked to specific instrumentation, it gains enhanced pricing power over consumables. This trend motivates vendors to create cartridges and columns that are either physically or electronically compatible with their platforms, bolstering customer loyalty.

In 2025, semi-automated technologies held a 46.85% share of the sample preparation market, appealing to labs that seek moderate throughput improvements without overhauling their operations. These systems often integrate bench-top magnetic-bead processors with manual pipetting stations, striking a balance between cost and performance. However, fully automated platforms are projected to grow at a 10.22% CAGR through 2031, fueled by escalating labor costs and stringent reproducibility standards. Labs that have embraced fully automated solutions frequently highlight added advantages, including enhanced traceability and reduced cross-contamination, both of which diminish expensive re-runs. Furthermore, as software updates roll out new protocols remotely, the longevity of automation hardware increases, making it more appealing for budget committees assessing the total cost of ownership.

Geography Analysis

North America leads the sample preparation market with 35.10% market share, buoyed by strong federal research grants, swift adoption of next-gen lab automation, and a concentration of biopharma headquarters. The region's regulatory framework, guided by FDA and CLIA standards, enforces pre-analytical quality controls, driving demand for standardized kits and traceable workflows. Partnerships, like QIAGEN's with Bio-Manguinhos/Fiocruz, highlight established vendors' efforts to adapt North American solutions for emerging public health markets, enhancing global presence and tailoring products to diverse resources. Consequently, academic medical centers, seeking distinction, are channeling investments into single-cell multi-omics platforms. This boosts consumables throughput, even as instrument installations plateau. The regional market leans towards integrated, compliance-focused solutions, streamlining documentation for accreditation cycles.

Asia Pacific is witnessing the fastest growth, driven by a surge in pharmaceutical manufacturing and robust government incentives bolstering domestic biotech ecosystems. China's Five-Year Plans allocate significant funds towards high-end instrumentation, pushing local labs to bypass intermediate technologies in favor of fully automated workflows. In Japan and South Korea, an ageing population is driving up the demand for molecular-diagnostic testing, particularly in oncology and inherited disorders. The rise of local-language software and smaller reagent pack sizes underscores the potential of regional customization in capturing market share, all while keeping core chemistries intact. Notably, recent geopolitical disruptions have underscored the importance of supply-chain resiliency, prompting multinationals to set up manufacturing hubs in the region to secure tenders.

Europe's Sample Preparation industry thrives on initiatives like Horizon Europe, channeling funds into omics projects that demand meticulous sample handling. EU mandates on lab sustainability spark a shift towards eco-friendly consumables, urging vendors to innovate kits that minimize environmental harm while maximizing yield. The rise of academic-industrial partnerships accelerates the development of specialized extraction chemistries, birthing start-ups that flourish through licensing agreements with industry giants. Concurrently, the stringent data-protection mandates of GDPR heighten the demand for secure, audit-compliant instrument software, reshaping procurement decisions alongside traditional performance benchmarks. Collectively, these dynamics reinforce Europe's pivotal role as a trendsetter in global regulatory and sustainability movements.

- Thermo Fisher Scientific

- Agilent Technologies

- Merck KGaA (MilliporeSigma)

- Danaher Corporation (Beckman Coulter & Cytiva)

- QIAGEN

- PerkinElmer

- Illumina

- Bio-Rad Laboratories

- Tecan Group

- Biotage

- Norgen Biotek

- Eppendorf

- Hamilton Company

- Promega

- LGC Biosearch Technologies

- Takara Bio

- Beckton Dickinson

- Fluidigm

- Analytik Jena GmbH

- Brooks Life Sciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Global Investment in Omics Research and Precision-Medicine

- 4.2.2 Growing Demand for Automated, High-Throughput Sample-Prep to Boost Laboratory Productivity

- 4.2.3 Increasing Clinical Adoption of Genomic Sequencing and Liquid-Biopsy Diagnostics

- 4.2.4 Expansion Of Biopharma R&D And Manufacturing Volumes Requiring Robust Sample Preparation

- 4.2.5 Supportive Government Funding and Public-Private Partnerships for Life-Science Tool Innovation

- 4.2.6 Advancements In Automation, Microfluidics and Reagent Chemistries Enhancing Workflow Efficiency

- 4.3 Market Restraints

- 4.3.1 High Capital and Operating Costs of Fully Automated Sample-Prep Platforms

- 4.3.2 Shortage Of Skilled Personnel to Operate and Maintain Sophisticated Systems

- 4.3.3 Stringent Regulatory Requirements for Clinical-Grade Reagents Extending Time-To-Market

- 4.3.4 Supply-Chain Vulnerabilities for Specialty Enzymes, Magnetic Beads and Plastics

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Sample-Preparation Instruments

- 5.1.1.1 Extraction Systems

- 5.1.1.2 Automated Workstations

- 5.1.1.3 Evaporation Systems

- 5.1.1.4 Liquid-Handling Platforms

- 5.1.1.5 Other Instruments

- 5.1.2 Consumables

- 5.1.3 Sample-Preparation Kits

- 5.1.3.1 Purification Kits

- 5.1.3.2 Isolation Kits

- 5.1.3.3 Extraction Kits

- 5.1.4 Accessories & Software

- 5.1.1 Sample-Preparation Instruments

- 5.2 By Technology

- 5.2.1 Manual

- 5.2.2 Semi-Automated

- 5.2.3 Fully Automated

- 5.3 By Application

- 5.3.1 Genomics

- 5.3.2 Proteomics

- 5.3.3 Epigenomics

- 5.3.4 Other Application

- 5.4 By End-User

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biotechnology Companies

- 5.4.3 Molecular Diagnostics Labs

- 5.4.4 Academic & Research Institutes

- 5.4.5 CROs & CDMOs

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 Merck KGaA (MilliporeSigma)

- 6.3.4 Danaher Corporation (Beckman Coulter & Cytiva)

- 6.3.5 QIAGEN N.V.

- 6.3.6 PerkinElmer Inc.

- 6.3.7 Illumina Inc.

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 Tecan Group Ltd.

- 6.3.10 Biotage AB

- 6.3.11 Norgen Biotek Corp.

- 6.3.12 Eppendorf AG

- 6.3.13 Hamilton Company

- 6.3.14 Promega Corporation

- 6.3.15 LGC Biosearch Technologies

- 6.3.16 Takara Bio Inc.

- 6.3.17 Becton, Dickinson and Company

- 6.3.18 Fluidigm Corporation

- 6.3.19 Analytik Jena GmbH

- 6.3.20 Brooks Life Sciences

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment