|

시장보고서

상품코드

2061584

집단건강관리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Population Health Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

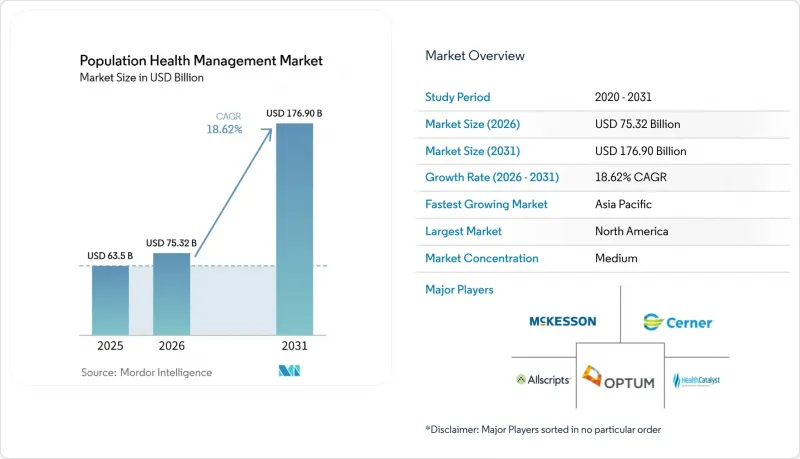

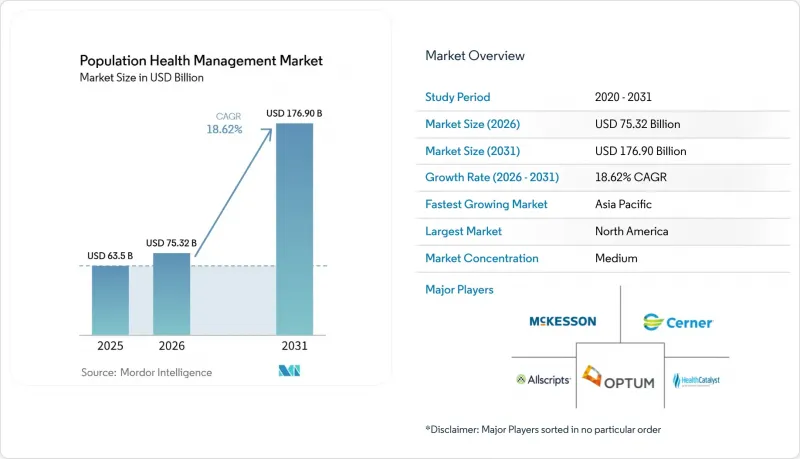

Mordor Intelligence에 의하면, 집단건강관리 시장 규모는 2025년 635억 달러로 평가되었습니다. 2026년에는 753억 2,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 18.62%를 나타내, 2031년에는 1,769억 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어, 서비스, 하드웨어), 솔루션 유형(인구 건강 분석, 환자 참여 솔루션 등), 제공 형태(On-Premise, 클라우드 기반/웹 기반, 하이브리드), 최종 사용자(의료 제공업체, 보험사), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다.

세계의 집단건강관리 시장 동향 및 인사이트

케어 연속체 전반에 걸친 통합된 종단적 환자 기록의 필요성

종합적인 환자 파일을 작성하는 의료기관에서는 코딩 누락 해소율이 7% 더 높고, 연간 건강검진 건수가 17% 더 많은 것으로 보고되어, 통합된 데이터가 품질 지표를 직접적으로 향상시킨다는 사실이 입증되었습니다. 실용적인 교훈으로, 일관성 있는 기록은 임상의에게 도움을 줄 뿐만 아니라, 위험 기반 계약에서 수익 확보에도 기여합니다. 종단적 데이터 세트는 전략적 자산이므로, 조직은 상호 운용성을 단순한 IT 업무가 아닌 이사회 차원의 우선 과제로 다루고 있습니다.

장기적인 관리가 필요한 만성 질환의 부담 증가

현재 미국에서 의료비의 90%는 만성 질환 치료에 지출되고 있습니다. 집단건강관리 플랫폼은 임상 워크플로우에 지속적인 모니터링을 결합하여 이러한 과제를 해결하고 있으며, Senscio Systems사의 Ibis Health와 같은 프로그램은 입원율을 29% 감소시켰습니다. 알고리즘을 활용한 알림은 환자의 예방적 관리 습관을 형성하고, 지속적인 소통을 일상적인 습관으로 정착시킬 수 있습니다.

다직종 도입 팀의 필요성

Health Catalyst는 효과적인 도입을 위해서는 임상, 분석, 관리 각 분야의 전문 지식이 융합되어야 한다고 지적하고 있습니다. 데이터 사이언스자 및 케어 조정 전문가의 부족으로 인해 시스템 가동에 차질이 발생하고 있어, 조직은 관리형 서비스 모델로 전환하고 있습니다. 인력 공급이 따라잡을 때까지는 서비스 부문의 성장률이 소프트웨어 부문을 상회할 것으로 예측됩니다.

부문별 분석

이 소프트웨어는 2025년 집단건강관리(Population Health Management) 시장에서 43.55%의 점유율을 차지하며, 가치 기반 프로그램의 핵심이 되는 분석 대시보드, 리스크 모델, 품질 보고 도구를 제공했습니다. 이러한 플랫폼들은 의료 서비스의 사각지대를 해소하고 규제 당국에 대한 신고 절차를 지원하며, 많은 의료 제공업체의 디지털 전략의 기반이 되고 있습니다. 소프트웨어 라이선스에는 단계적 업그레이드가 포함되어 있기 때문에 의료 서비스 제공업체들은 신속한 규정 준수 업데이트를 위해 종종 벤더 종속성을 감수하기도 합니다.

그러나 서비스 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 19.94%를 나타낼 것으로 예측되며, 조직들이 도입, 변경 관리 및 지속적인 최적화를 위해 외부 전문가에 의존하게 됨에 따라 하드웨어 부문의 기여도를 넘어설 것으로 전망됩니다. 이러한 추세는 많은 의료 시스템이 자체 역량을 구축하기보다 복잡한 업무를 외부에 위탁하는 것을 선호한다는 것을 보여주며, 간접적으로 컨설팅 파트너의 잠재적 수익을 확대시키고 있습니다. 현재 하드웨어는 집단건강관리(Population Health Management) 시장 규모에서 가장 작은 비중을 차지하고 있지만, 혈당 측정기나 맥박 산소 포화도 측정기 등의 원격 모니터링 기기가 그 구도를 변화시키고 있습니다. 이러한 점에서 볼 때, 웨어러블 기기에 대한 소비자의 수용도가 높아짐에 따라 임상용 기기의 도입 기반이 점진적으로 확대되고, 공급업체가 구축한 데이터 파이프라인이 강화될 것으로 예측됩니다. 분석 엔진으로 유입되는 생리학적 데이터 스트림이 늘어남에 따라, 의료진은 조기에 개입할 수 있게 되어 급성기 의료 비용을 절감할 수 있습니다. 이러한 피드백 루프는 보안 네트워크 장비 및 엣지 스토리지에 대한 새로운 수요를 창출하며, 원격 모니터링 시장이 성숙기에 접어들면 하드웨어 매출이 급증할 가능성을 시사합니다.

2025년 기준으로 인구 건강 분석은 31.05%의 시장 점유율을 차지했으며, 이는 급성 및 만성 질환과 사회적 위험 요인을 분석하는 밀리맨(Milliman)의 MARA와 같은 플랫폼에 힘입은 결과입니다. 공유된 분석 프레임워크는 단일한 ‘진실의 버전’을 기반으로 인센티브를 조율하여, 지불자와 의료 제공업체 간의 협력을 강화하고 있습니다.

환자 참여 솔루션 시장은 연평균 성장률(CAGR) 21.48%를 나타낼 것으로 예측되며, 이는 적극적으로 참여하는 가입자가 참여하지 않는 가입자에 비해 4배 더 많은 건강 관련 활동을 완료한다는 인식이 확산되고 있음을 반영합니다. 이러한 추세의 확산은 가입자용 앱이 머지않아 선택적 참여 유도 기능에서 위험 계약의 핵심 구성 요소로 전환될 것임을 시사합니다. 케어 조정 및 위험 계층화 도구는 다양한 환경에 걸친 다직종 팀을 연결하는 데 있어, 여전히 집단건강관리 업계에서 필수적입니다. EHR(전자건강기록)과의 연동이 강화되면, 임상의의 화면 조작 시간이 단축되어 업무 만족도가 점차 향상될 것입니다. 임상 워크플로 관리 시스템은 규모는 작지만, 진료 현장에 인구통계학적 인사이트를 접목하여 치료 순응도를 높입니다. 현장 직원들이 소비자용 앱처럼 매끄러운 인터페이스를 원함에 따라, 도입은 더욱 확대될 것으로 예측됩니다.

지역별 분석

북미는 2025년에 집단건강관리 시장의 48.35%를 차지했습니다. 이는 성숙한 EHR의 보급률, 가치 기반 인센티브, 활발한 M&A에 힘입어 2024년 시장 규모는 690억 달러에 달했습니다. 업계 통합을 통해 분산된 데이터 소스가 통합되면서, 지역별 분석 데이터의 예측 정확도가 향상되고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 18.96%를 나타낼 것으로 전망됩니다. 급속한 도시화, 스마트폰의 보급, 그리고 고령화가 맞물리면서 집단건강관리(PHM) 업계의 솔루션에 유리한 환경이 조성되고 있습니다. 디지털 헬스 서비스를 처음 이용하는 사용자를 유치할 때, 간소화된 사용자 인터페이스와 같은 문화적 적응은 가격과 마찬가지로 결정적인 요소가 될 수 있습니다.

유럽은 2050년까지 60세 이상 성인 인구가 3억 명을 넘어선 고령화 인구의 영향으로 여전히 강력한 성장세를 유지하고 있습니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정) 준수에 따라 공급업체는 제품 설계에 개인정보 보호 조치를 반영해야 하며, 이는 전 세계적인 모범 사례를 형성하고 있습니다. 강력한 개인정보 보호 규범은 궁극적으로 유럽공급업체들을 국경을 초월한 데이터 연계 분야에서 우선적인 파트너로 자리매김하게 할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the population health management market size is expected to grow from USD 63.5 billion in 2025 to USD 75.32 billion in 2026 and is forecast to reach USD 176.90 billion by 2031 at 18.62% CAGR over 2026-2031.

This report is Segmented by Component (Software, Services, and Hardware), Solution Type (Population Health Analytics, Patient Engagement Solutions, and More), Delivery Mode (On-Premise, Cloud-Based / Web-Based, and Hybrid), End User (Healthcare Providers, and Payers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America).

Global Population Health Management Market Trends and Insights

Need for Unified Longitudinal Patient Records Across Care Continuum

Healthcare organizations that create holistic patient files report 7% higher coding-gap closure and 17% more annual wellness visits, showing that integrated data directly boosts quality metrics. The practical takeaway is that a coherent record not only supports clinicians but also improves revenue capture under risk-based contracts. Because longitudinal data sets are strategic assets, organizations treat interoperability as a board-level priority rather than an IT task.

Escalating Chronic-Disease Burden Requiring Long-term Surveillance

Chronic conditions now consume 90% of healthcare spending in the United States. Population health platforms address this pressure by layering continuous monitoring on top of clinical workflows, cutting hospitalizations 29% in programs such as Senscio Systems' Ibis Health. Algorithm-driven alerts can normalize proactive care behaviors among patients, making continuous contact a routine expectation.

Need for Multidisciplinary Implementation Teams

Health Catalyst observes that effective deployments require combined clinical, analytics, and administrative expertise. Scarcity of data scientists and care-coordination specialists delays go-lives, nudging organizations toward managed-service models. The services segment is expected to outpace software until talent pipelines catch up.

Other drivers and restraints analyzed in the detailed report include:

- Public-Private Funding Surge in Digital Health Infrastructure

- Shift to Value-based Payment Models Accelerating PHM Adoption

- Reimbursement Gaps for Preventive/Population-based Care

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software commands a 43.55% Population Health Management market share in 2025, delivering analytics dashboards, risk models, and quality-reporting tools core to value-based programs. These platforms support care-gap closure and regulatory submissions, anchoring many provider digital strategies. Providers often accept vendor lock-in to obtain rapid compliance updates because software licenses bundle incremental upgrades.

The services segment, however, is forecast to grow at a 19.94% CAGR from 2026-2031, overtaking hardware's contribution as organizations lean on external experts for implementation, change management, and ongoing optimization. This trend reveals that many health systems prefer to outsource complexity rather than build in-house capabilities, indirectly expanding addressable revenue for consulting partners. Hardware currently forms the smallest slice of the Population Health Management market size, yet remote monitoring devices such as glucometers and pulse oximeters are starting to shift that balance. The inference is that consumer comfort with wearables will softly enlarge the install base of clinical-grade devices, reinforcing data pipelines built by software vendors. As more physiological data streams enter analytics engines, providers can intervene earlier, reducing acute-care costs. This feedback loop creates new demand for secure network gear and edge storage, indicating hardware revenues may spike once reimbursement codes for remote monitoring mature.

Population Health Analytics held 31.05% market share in 2025, underpinned by platforms like Milliman's MARA that parse acute, chronic, and social drivers of risk. Shared analytics frameworks align incentives on a single version of truth, deepening payer-provider collaborations.

Patient Engagement Solutions, forecast to post a 21.48% CAGR, reflect growing awareness that activated members complete four times more health actions than inactive peers. The rising tide suggests member-facing apps will soon migrate from optional engagement add-ons to central components of risk contracts. Care Coordination and Risk-Stratification tools remain vital in the Population Health Management industry, linking multidisciplinary teams across settings. Tighter EHR integration will lower clinician screen time and subtly improve job satisfaction. Clinical Workflow Management systems-though smaller-embed population insights at the point of care, driving adherence. Uptake is likely to strengthen as frontline staff demand frictionless interfaces that mirror consumer apps.

Geography Analysis

North America commands a 48.35% Population Health Management market share in 2025, supported by mature EHR penetration, value-based incentives, and active M&A worth USD 69 billion in 2024. Consolidation is integrating disparate data sources and improving the predictive accuracy of regional analytics pools.

Asia-Pacific is the fastest-growing region, poised for a 18.96% CAGR through 2031. Rapid urbanization, smartphone ubiquity, and an aging population converge to create fertile ground for Population Health Management industry solutions. Cultural adaptation, such as simplified user interfaces, may be as decisive as price when attracting first-time digital health users.

Europe maintains significant momentum, spurred by an older demographic set to top 300 million adults over 60 by 2050. GDPR compliance forces vendors to bake privacy safeguards into product design, shaping global best practices. Strong privacy norms may eventually position European suppliers as preferred partners for cross-border data collaborations.

- Allscripts

- Oracle Corporation (Oracle Health/Cerner)

- Optum

- Epic Systems

- Koninklijke Philips

- Health Catalyst

- IBM (Merative)

- Mckesson

- Conifer Health Solutions

- eClinicalWorks LLC

- Athenahealth

- Arcadia.io

- Cotiviti

- Medecision

- NextGen Healthcare

- Lumeris Inc.

- Innovaccer

- Persivia Inc.

- Lightbeam Health Solutions

- Enli Health Intelligence (symplr)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need for Unified Longitudinal Patient Records Across Care Continuum

- 4.2.2 Escalating Chronic-Disease Burden Requiring Long-term Surveillance

- 4.2.3 Public-Private Funding Surge in Digital Health Infrastructure

- 4.2.4 Shift to Value-based Payment Models Accelerating PHM Adoption

- 4.2.5 AI-powered Predictive Analytics Enabling Proactive Interventions

- 4.2.6 Regulatory Incentives (e.g., CMS QPP, EU HTA) Boosting Reporting Compliance

- 4.3 Market Restraints

- 4.3.1 Need for Multidisciplinary Implementation Teams

- 4.3.2 Reimbursement Gaps for Preventive/Population-based Care

- 4.3.3 Data-privacy & Interoperability Barriers Among Disparate Systems

- 4.3.4 Limited Digital Literacy in Low-resource Settings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Stand-alone Software

- 5.1.1.2 Integrated Software Suites

- 5.1.2 Services

- 5.1.2.1 Consulting & Training

- 5.1.2.2 Implementation & Integration

- 5.1.2.3 Support & Maintenance

- 5.1.3 Hardware

- 5.1.3.1 Servers & Storage

- 5.1.3.2 Networking Devices

- 5.1.3.3 Wearable & Remote-Monitoring Devices

- 5.1.1 Software

- 5.2 By Solution Type

- 5.2.1 Population Health Analytics

- 5.2.2 Patient Engagement Solutions

- 5.2.3 Care Coordination Tools

- 5.2.4 Risk-Stratification & Reporting Solutions

- 5.2.5 Clinical Workflow Management

- 5.3 By Delivery Mode

- 5.3.1 On-premise

- 5.3.2 Cloud-based / Web-based

- 5.3.3 Hybrid

- 5.4 By End-User

- 5.4.1 Healthcare Providers

- 5.4.2 Payers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Allscripts Healthcare Solutions Inc.

- 6.4.2 Oracle Corporation (Oracle Health/Cerner)

- 6.4.3 Optum Inc.

- 6.4.4 Epic Systems Corporation

- 6.4.5 Koninklijke Philips N.V.

- 6.4.6 Health Catalyst Inc.

- 6.4.7 IBM (Merative)

- 6.4.8 McKesson Corporation

- 6.4.9 Conifer Health Solutions

- 6.4.10 eClinicalWorks LLC

- 6.4.11 athenahealth Inc.

- 6.4.12 Arcadia.io

- 6.4.13 Cotiviti Inc.

- 6.4.14 Medecision Inc.

- 6.4.15 NextGen Healthcare Inc.

- 6.4.16 Lumeris Inc.

- 6.4.17 Innovaccer Inc.

- 6.4.18 Persivia Inc.

- 6.4.19 Lightbeam Health Solutions

- 6.4.20 Enli Health Intelligence (symplr)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment