|

시장보고서

상품코드

2061587

증기 터빈 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Steam Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

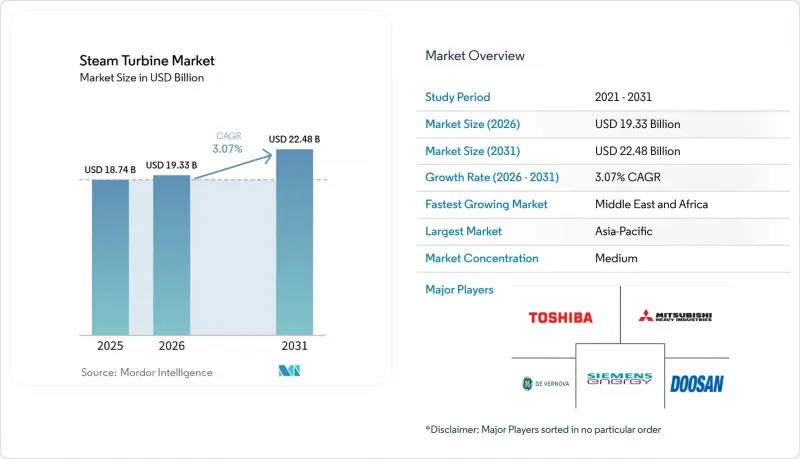

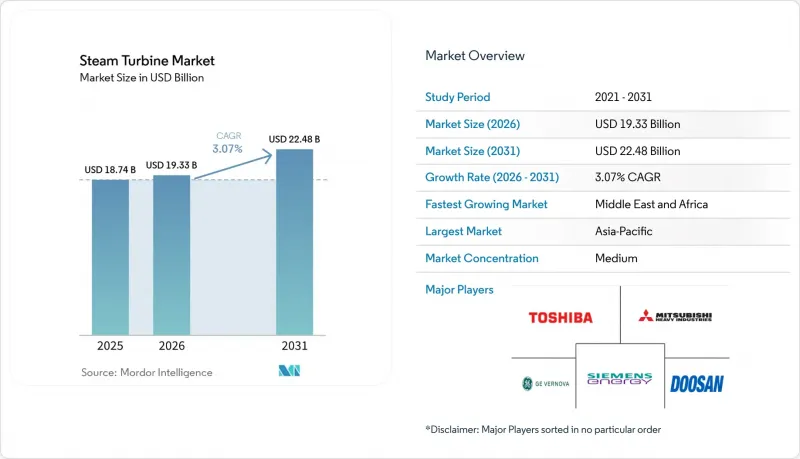

Mordor Intelligence에 의하면, 증기 터빈 시장 규모는 2025년 187억 4,000만 달러로 평가되었습니다. 2026년에는 193억 3,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 3.07%를 나타내, 2031년에는 224억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 출력(300MW 미만, 300-600MW, 600MW 이상), 발전소 연료(석탄, 천연가스, 원자력, 바이오매스/폐기물 발전), 최종 사용자 산업(발전, 석유 및 가스, 산업·기타), 그리고 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 증기 터빈 시장 동향과 분석

석탄 화력 발전의 단계적 폐지가 진행되는 전력망에서 유연한 기저 부하 용량에 대한 수요가 급증하고 있습니다.

급가동 및 저감속 기능을 갖춘 증기 터빈은 풍력 및 태양광 발전의 도입률이 이미 40%를 넘어선 전력망에서 관성력을 공급하는 동기 진상기로 유지되고 있습니다. 구형 아임계 석탄 화력 발전 설비를 폐지한 미국의 전력 회사는 현재, 30분 이내에 계통 연동이 가능한 수소 대응 복합 사이클 발전 설비를 활용해 계통 연동 능력을 재구축하고 있습니다. 이는 미국 중부 지역의 여러 ISO(독립계통운영기구)가 실시한 용량 경매에서 명시된 요건입니다. 2030년까지 갈탄 화력발전소 폐쇄를 연기하고 있는 독일의 사업자들은 크리프 손상이 발생하지 않으면서 하루 2회 사이클 운전이 가능한 단결정 블레이드 터빈을 발주하고 있습니다. 이러한 설비는 4시간을 초과하는 배터리 한계를 넘어서는 저녁 시간대 수요 급증 시 전압 안정화를 제공하며, 재생에너지에 부과되는 출력 제한 페널티를 상쇄합니다. 그 결과, 사이클 성능 향상과 합성 관성 패키지를 제공하는 증기 터빈 시장 진출기업들은 기존 설계에 비해 8%에서 12%의 설비 가격 프리미엄을 확보하고 있습니다.

첨단 증기 터빈을 활용한 노후 복합 화력 발전소의 리파워링

2000년부터 2010년 사이에 설치된 약 120GW 규모의 F급 가스 화력 발전소가 설계 수명에 다다르고 있어, 노후화된 증기 터빈을 H급 또는 J급 설비로 교체하는 리파워링 열풍이 일고 있습니다. 일반적인 500MW 출력 증설의 경우, 순효율이 2-3% 향상되고 자산 수명이 20년 연장됩니다. 이는 신규 건설(그린필드) 설비 투자액의 40-50%로 실현 가능하며, 가스 가격이 1MMBtu당 4달러일 경우 7년 이내에 투자 회수가 가능합니다. 유럽연합(EU)의 탄소 집약도 규제로 인해 전력 회사들은 신규 건설보다는 개보수를 선택하도록 권장받고 있으며, 이를 통해 기존 송전망 허가 및 수자원 이용권을 유지할 수 있습니다. 기존 기초에 설치 가능한 모듈식 터빈 배열을 공급하는 업체 덕분에 가동 중단 기간이 16주에서 10주로 단축되어, 상업용 발전소의 수익 손실 위험이 완화되었습니다. 부피 비율 기준 최대 30%의 수소 혼소 허용치는 현재 영국의 여러 용량 시장 입찰에서 필수 조건으로 적용되고 있으며, 이는 리파워링 수요를 더욱 촉진하고 있습니다.

유틸리티 규모의 태양광 발전 및 에너지 저장 시스템에서 LCOE의 급격한 하락

태양광 발전과 결합된 4시간 리튬이온 축전 시스템은 2025년에 세계 가중평균 발전 비용(LCOE)이 1MWh당 56달러에 달하여, 일조량이 많은 시장에서는 신규 복합 사이클 가스 발전보다 비용이 더 낮아졌습니다. 사막 지대나 열대 지역에서 설비 가동률이 30%를 넘어섬에 따라, 전력 회사들은 증기 발전 계약을 종료하고 재생에너지 포트폴리오로의 전환을 추진하고 있으며, 이로 인해 단기 잠재 수요가 연간 약 1GW 감소하고 있습니다. 각 OEM 업체들은 부가 서비스를 통한 수익과 신속한 블랙 스타트 능력을 강조하고 있지만, 2028년 이후에는 흐름 전지나 압축 공기 축전 등 장시간 축전 프로토타입이 이러한 우위를 위협하게 될 것입니다. 그 결과, 프로젝트 개발자들은 현재 가스 및 석탄에 대한 의존도를 높게 평가하고 있으며, 필요한 자기자본이익률을 200-250베이시스포인트 상향 조정하고 있습니다. 이로 인해 증기 터빈 시장의 성장 기회는 점점 줄어들고 있습니다.

부문별 분석

300-600MW급은 2025년 매출의 59.8%를 차지하며, 복합 사이클 및 초초임계 석탄 화력 발전 구성에서 그 우위를 여실히 보여주고 있습니다. 이러한 규모에서는 규모의 경제 효과가 일반적인 변압기 정격 및 지역 송전망 규격과 부합하여, 피크 시간대의 우선적인 전력 공급이 보장됩니다. 인도, 이집트, 사우디아라비아의 전력 회사들이 가스 및 원자력을 이용한 기저부하 발전 입찰을 최종 확정함에 따라, 이 등급의 증기 터빈 시장 규모는 2031년까지 135억 달러에 달할 것으로 전망됩니다. 효율 기록은 계속해서 갱신되고 있습니다. GE의 9HA.02는 2025년에 62.5%의 순 복합 사이클 효율을 달성한 반면, 지멘스 에너지의 SGT6-9000HL은 출력 저하 없이 50%의 수소 연소 능력을 입증했습니다.

300MW 미만의 발전 단위는 연평균 성장률(CAGR) 4.8%를 기록하며 시장 전체의 성장률을 상회할 것으로 전망됩니다. 이는 동남아시아와 라틴아메리카의 펄프, 섬유, 식품 산업 클러스터에서 현장 열병합 발전으로의 산업적 전환을 반영하고 있습니다. 150-250MW급 추출·응축형 플랜트가 인기를 끌고 있으며, 공정 증기를 활용함으로써 전력망에서 전력을 구매하는 경우와 비교해 석유화학제품의 이익률을 300베이시스포인트 이상 높일 수 있습니다. 마이크로 유틸리티 분야에서는 100MW 미만의 모듈식 발전소가, 최고 수준의 열효율보다는 신속한 도입을 중시하는 광산 캠프나 섬의 마이크로그리드에 대응하고 있습니다. 한편, 600MW를 초과하는 부문은 여전히 틈새 시장에 머물러 있으며, 인도의 신규 초임계 석탄 화력 발전소나 일부 AP1000 원자로 프로젝트로 한정되어 있습니다. 이 분야는 ESG 측면에서 역풍이 거세지고 있어, 금융기관의 투자 의욕도 제한적입니다.

지역별 분석

아시아태평양은 중국의 초초임계 화력 발전소 현대화 사업과 인도의 석탄·원자력 병용 정책이 조달을 주도함에 따라, 2025년 매출의 47.6%를 차지했습니다. 동남아시아에서는 산업 확장과 안정적인 연료 공급을 배경으로, 2025년부터 2028년에 걸쳐 15GW 규모의 열병합 발전 설비가 추가되었습니다. 그 결과, 해당 지역의 증기 터빈 시장에서는 대형 프레임 수주에 더해 중형 산업용 유닛의 수주량이 계속해서 증가하고 있습니다.

중동 및 아프리카의 증기 터빈 시장은 사우디아라비아의 30GW 규모 가스 화력 독립 발전 프로젝트, 아랍에미리트의 바라카 원자력 발전소 본격 가동, 그리고 이집트의 원자력·가스 복합 발전 등을 원동력으로 연평균 성장률(CAGR) 5.3%를 기록하며 성장할 전망입니다. 자플라 및 기타 비전통 가스전에서 공급되는 가스를 활용해 석유를 수출로 돌릴 수 있는 복합 화력 발전소의 건설이 촉진되고 있습니다. 동시에, 이집트와 사우디아라비아의 원자력 발전에 대한 의지가 향후 수년간 터빈 수요를 견고하게 뒷받침할 것으로 보이며, 해당 지역 시장 점유율은 2025년 12%에서 2031년까지 15%를 나타낼 것으로 예측됩니다.

북미와 유럽에서는 석탄 화력 발전의 단계적 폐지가 발전 설비 현대화 및 지역 난방 시설 개보수 효과를 상쇄함에 따라, 발전량이 정체되거나 소폭 증가하는 데 그칠 것입니다. 미국의 성장은 즉각 대응형 동기 발전 설비에 대한 용량 시장의 인센티브에 좌우되는 반면, 유럽 수요는 수소 활용이 가능한 가스전 및 바이오매스 열병합 발전(CHP)에 집중되어 있습니다. 남미는 여전히 틈새 시장이며, 브라질의 사탕수수 바가스 열병합 발전(CHP)과 아르헨티나의 바카 무에르타 가스 개발이 활동의 대부분을 차지하고 있습니다. 이러한 동향들이 맞물려, 증기 터빈 시장의 수익원 다각화가 전 세계적으로 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the steam turbine market size is expected to grow from USD 18.74 billion in 2025 to USD 19.33 billion in 2026 and is forecast to reach USD 22.48 billion by 2031 at 3.07% CAGR over 2026-2031.

This report is Segmented by Capacity (Below 300 MW, 300 To 600 MW, and Above 600 MW), Plant Fuel (Coal, Natural Gas, Nuclear, and Biomass/Waste-to-Energy), End-User Industry (Power Generation, Oil and Gas, and Industrial and Other), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Steam Turbine Market Trends and Insights

Surging Demand for Flexible Baseload Capacity in Coal-Retiring Grids

Steam turbines equipped with fast-start and low-turn-down features are being retained as synchronous condensers to supply inertia in grids where wind and solar penetration already exceeds 40%. U.S. utilities that decommissioned older subcritical coal units are now repowering interconnection rights with hydrogen-ready combined-cycle blocks that synchronize within 30 minutes, a requirement spelled out in several Midcontinent ISO capacity auctions. German operators delaying lignite closures until 2030 are ordering single-crystal bladed turbines that can cycle twice daily without creep damage. These installations provide voltage support during evening demand ramps longer than four-hour battery limits, offsetting curtailment penalties levied on renewables. Consequently, steam turbine market participants offering enhanced cycling capability and synthetic inertia packages are commanding 8% to 12% equipment price premiums over legacy designs.

Repowering of Ageing Combined-Cycle Plants with Advanced Class Steam Turbines

Roughly 120 GW of F-class gas plants installed between 2000 and 2010 are reaching design life, driving a repowering cycle that replaces aging steam trains with H- or J-class equipment. A typical 500 MW uprate boosts net efficiency by 2-3 percentage points and extends asset life 20 years at 40%-50% of greenfield capex, yielding paybacks under seven years at USD 4 per MMBtu gas prices. European Union carbon-intensity rules encourage utilities to retrofit rather than build new, preserving existing grid permits and water rights. Vendors supplying modular turbine trains that fit within existing foundations have shortened outage windows from 16 weeks to 10, reducing lost-revenue risk for merchant plants. Hydrogen co-firing tolerance up to 30% by volume is now a bid prerequisite in several U.K. capacity-market tenders, further stimulating repower demand.

Aggressive LCOE Decline of Utility-Scale Solar-Plus-Storage

Four-hour lithium-ion storage paired with PV reached a global weighted-average levelized cost of USD 56 per MWh in 2025, undercutting new combined-cycle gas in sunny markets. As capacity factors rise beyond 30% in deserts and tropics, utilities are canceling steam contracts in favor of renewable portfolios, trimming near-term addressable demand by almost 1 GW yearly. OEMs emphasize ancillary-service revenue and fast black-start capabilities, but long-duration storage prototypes such as flow batteries and compressed air threaten this advantage after 2028. Consequently, project developers now price gas and coal exposure higher, increasing required equity returns by 200-250 basis points, which compresses the steam turbine market opportunity window.

Other drivers and restraints analyzed in the detailed report include:

- Post-Inflation Industrial CAPEX Boom in South-East Asia

- Hydrogen-Ready Turbine Upgrades Unlocking Future Revenue Streams

- Water-Stress Regulations Curbing Once-Through Cooling Permits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 300 to 600 MW class contributed 59.8% of 2025 revenue, underscoring its dominance within combined-cycle and ultra-supercritical coal configurations. At this level, economies of scale match common transformer ratings and regional grid codes, ensuring dispatch priority during peak hours. The steam turbine market size for this class is forecast to rise to USD 13.5 billion by 2031 as utilities in India, Egypt, and Saudi Arabia finalize tenders for gas and nuclear baseload. Efficiency records continue to fall: GE's 9HA.02 notched 62.5% net combined-cycle efficiency in 2025, while Siemens Energy's SGT6-9000HL demonstrated 50% hydrogen capability without derate.

Below-300 MW units will outpace headline growth at 4.8% CAGR, mirroring an industrial pivot toward on-site cogeneration in Southeast Asia and LatAm pulp, textile, and food clusters. Extraction-condensing variants in the 150-250 MW band are gaining popularity, where process steam drives petrochemical margins upward of 300 basis points compared with grid purchases. At the micro-utility end, <100 MW modular trains address mining camps and island micro-grids that prize fast deployment over top-quartile heat rate. Conversely, the >600 MW bracket remains niche, restricted to new supercritical coal in India and select AP1000 reactor projects, facing stiffer ESG headwinds and limited lender appetite.

Geography Analysis

Asia-Pacific retained 47.6% of 2025 revenue as China's ultra-supercritical upgrades and India's coal-plus-nuclear trajectory dominated procurement. Southeast Asia added 15 GW of cogeneration through 2025-2028, reflecting industrial expansion and favorable fuel availability. As a result, the regional steam turbine market continues to generate large frame orders plus an accelerating volume of mid-sized industrial trains.

The Middle East and Africa steam turbine market is poised to grow at 5.3% CAGR, driven by Saudi Arabia's 30 GW gas-fired independent power projects, the United Arab Emirates' full Barakah ramp-up, and Egypt's nuclear and gas blend. Gas availability from Jafurah and other unconventional fields encourages combined-cycle builds that free oil for export. Concurrently, nuclear ambitions across Egypt and Saudi Arabia lock in multi-year turbine demand, elevating the regional contribution from 12% share in 2025 to an expected 15% by 2031.

North America and Europe experience flat-to-modest expansion as coal exits counterbalance repowering and district-heating retrofits. U.S. growth hinges on capacity-market incentives for fast-start synchronous capacity, while European demand centers on hydrogen-ready gas blocks and biomass CHP. South America remains niche, with Brazil's sugar-bagasse CHP and Argentina's Vaca Muerta gas development representing most activity. Together, these dynamics maintain global diversification of revenue streams within the steam turbine market.

- Siemens Energy AG

- GE Vernova Inc.

- Mitsubishi Heavy Industries Ltd.

- Toshiba Energy Systems & Solutions

- Dongfang Turbine Co. Ltd.

- Doosan Enerbility Co., Ltd.

- Bharat Heavy Electricals Ltd.

- Harbin Electric Corp.

- Ansaldo Energia SpA

- Fuji Electric Co., Ltd.

- Kawasaki Heavy Industries Ltd.

- MAN Energy Solutions SE

- Elliott Group

- Triveni Turbines Ltd.

- WEG SA

- Hitachi-Zosen Corp. (Energy Solutions)

- Shanghai Electric Group Co. Ltd.

- Baker Hughes Co.

- Nanjing Turbine & Electric Machinery Group

- Siemens-Gamesa (Steam generator for hybrid plants)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for flexible baseload capacity in coal-retiring grids

- 4.2.2 Repowering of ageing combined-cycle plants with advanced class steam turbines

- 4.2.3 Post-inflation industrial CAPEX boom in South-East Asia

- 4.2.4 Hydrogen-ready turbine upgrades unlocking future revenue streams

- 4.2.5 Government-led nuclear new-build programs in emerging markets

- 4.2.6 Decarbonized district-heating schemes using extraction-condensing units

- 4.3 Market Restraints

- 4.3.1 Aggressive LCOE decline of utility-scale solar-plus-storage

- 4.3.2 Water-stress regulations curbing once-through cooling permits

- 4.3.3 Slow EPC execution cycles inflating project IRRs

- 4.3.4 Financing flight from fossil-linked assets post-ESG mandates

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Materials, Digital Twins, Super-critical CO2)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity

- 5.1.1 Below 300 MW

- 5.1.2 300 to 600 MW

- 5.1.3 Above 600 MW

- 5.2 By Plant Fuel

- 5.2.1 Coal

- 5.2.2 Natural Gas

- 5.2.3 Nuclear

- 5.2.4 Biomass/Waste-to-Energy

- 5.3 By End-user Industry

- 5.3.1 Power Generation

- 5.3.2 Oil and Gas (Up-/Mid-/Down-stream)

- 5.3.3 Industrial and Other

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Siemens Energy AG

- 6.4.2 GE Vernova Inc.

- 6.4.3 Mitsubishi Heavy Industries Ltd.

- 6.4.4 Toshiba Energy Systems & Solutions

- 6.4.5 Dongfang Turbine Co. Ltd.

- 6.4.6 Doosan Enerbility Co., Ltd.

- 6.4.7 Bharat Heavy Electricals Ltd.

- 6.4.8 Harbin Electric Corp.

- 6.4.9 Ansaldo Energia SpA

- 6.4.10 Fuji Electric Co., Ltd.

- 6.4.11 Kawasaki Heavy Industries Ltd.

- 6.4.12 MAN Energy Solutions SE

- 6.4.13 Elliott Group

- 6.4.14 Triveni Turbines Ltd.

- 6.4.15 WEG SA

- 6.4.16 Hitachi-Zosen Corp. (Energy Solutions)

- 6.4.17 Shanghai Electric Group Co. Ltd.

- 6.4.18 Baker Hughes Co.

- 6.4.19 Nanjing Turbine & Electric Machinery Group

- 6.4.20 Siemens-Gamesa (Steam generator for hybrid plants)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment