|

시장보고서

상품코드

2061588

유럽의 요실금용 기기 및 장루 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Incontinence Devices And Ostomy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

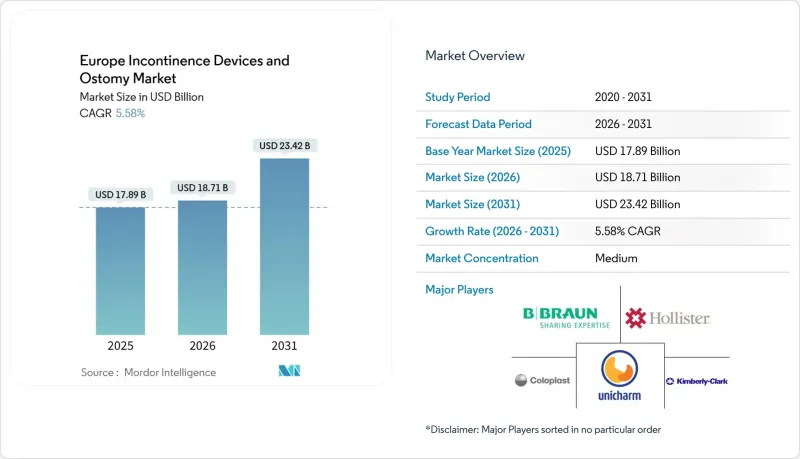

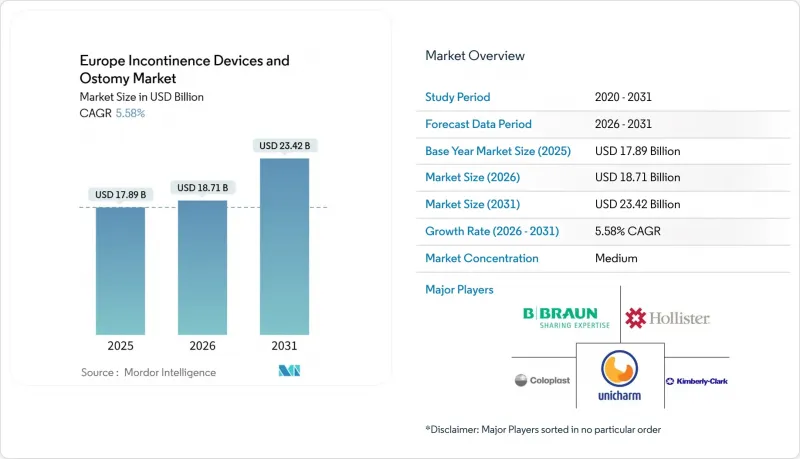

Mordor Intelligence에 의하면, 유럽의 요실금용 기기 및 장루 시장 규모는 2025년에 178억 9,000만 달러로 평가되었습니다. 2026년 187억 1,000만 달러에서 2031년까지 234억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.58%를 나타낼 전망입니다.

본 보고서는 제품 유형(요실금 관리 제품 및 장루 관리 제품), 용도(방광암 등), 최종 사용자(병원 등), 유통 채널(기관 입찰 조달 등), 기술/시스템(일회용 제품 등) 및 지역(독일 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 요실금용 기기 및 장루 시장 동향과 인사이트

고령화 및 비만 인구 증가

유럽은 세계에서 고령화가 가장 심하게 진행된 지역으로, 65세 이상 시민의 34%가 매주 절박성 요실금 또는 복압성 요실금 발작을 겪고 있는 것으로 보고되고 있습니다. 독일과 영국에서는 비만 유병률이 22%를 넘으며, 과도한 복압이 골반저 근육의 약화를 가속화하여 요실금을 유발하고 있습니다. 비뇨기과 의사들은 재발성 요로감염을 예방하기 위해 일회용 카테터와 패드를 처방하고 있으며, 이것이 외래 진료소에서의 대량 수요를 이끌고 있습니다. 이와 더불어, 노인 의학 지침에서는 대장 수술 후 회복기에 있는 고령자에게 장루 주머니의 용량을 늘릴 수 있으므로, 배변 관리용 파우치의 조기 도입을 권장하고 있습니다. 스페인에서는 평균 수명이 83세에 달함에 따라 만성 질환이나 장애를 안고 지내는 기간이 계속 늘어나고 있으며, 이는 유럽의 요실금용 기기 및 장루 시장에서의 고객 기반을 강화하고 있습니다.

신장·비뇨기 질환 유병률 증가

2형 당뇨병과 고혈압은 만성 신장 질환의 발병률을 높이고 있으며, 현재 북유럽 성인의 10%가 이 질환을 앓고 있습니다. 혈액투석 환자는 투석 세션 사이의 체액 균형을 조절하기 위해 간헐적 카테터 요법이나 대용량 요로 오스토미 주머니가 필요한 경우가 많습니다. 국가 건강보험 기금은 야간 소변을 안전하게 채취할 수 있는 밀폐형 배액백 비용을 환급하고 있으며, 이에 따라 해당 제품의 지속적인 판매가 확대되고 있습니다. 비뇨기과학회가 주관하는 계몽 프로그램은 1차 진료 의사들에게 뇌졸중 후 신경성 방광에 대한 선별 검사를 권장하고, 전문 요실금 치료 센터로의 의뢰를 촉진하고 있습니다. 의료기기 제조업체는 투석 클리닉과 제휴하여 주 단위 치료 패키지에 장루용 부속품을 포함시킴으로써 말기 신장 질환 환자들 사이에서 제품의 보급률을 높이고 있습니다.

장기 사용에 따른 합병증 및 장루 주변의 피부 문제

인공항문 성형술을 받은 환자의 약 35%가 수술 후 1년 이내에 피부염이나 점막·피부 박리를 경험하고 있으며, 이는 재입원 위험을 높이고 있습니다. 만성적인 누출은 원피스형 가방에 대한 신뢰를 떨어뜨리고, 신규 환자 유치를 주저하게 만드는 요인이 되고 있습니다. 환자 포럼에서는 부정적인 체험담이 퍼지면서, 소비자 직접 판매 채널에서의 도입 곡선이 장기화되고 있습니다. 의료 제공업체들은 추가 간호 시간과 하이드로콜로이드 드레싱 키트에 대한 투자를 감수해야 하며, 삶의 질(QOL)에 대한 우려 등으로 인해 보험사의 1회당 의료비가 상승하고 있어, 유럽의 요실금 의료기기 및 장루 시장에서의 급속한 성장이 억제되고 있습니다.

부문별 분석

2025년, 요실금 관리 제품은 유럽의 요실금용 기기 및 장루 시장의 66.56%를 차지했습니다. 이는 공립 병원의 성인용 기저귀, 패드, 간헐적 카테터에 관한 대규모 계약에 힘입은 결과입니다. 고령층에서 절박성 요실금 및 과다배출성 요실금의 유병률이 높다는 점이, EU의 인장 강도 및 생분해성 기준을 충족하는 흡수성 언더패드의 조달을 촉진하고 있습니다. 각 제조업체는 흡수력을 저해하지 않으면서 친환경 라벨 기준을 충족하기 위해 식물 유래 플라프 펄프와 SAP(고흡수성 폴리머)의 혼합물을 활용하고 있습니다. 고령 가구와 요양 시설이 누출 방지 기능이 있는 침구를 우선적으로 선택하는 가운데, 유럽의 요실금용 기기 및 장루 관리 시장 내 일회용 패드 시장 규모는 2031년까지 연평균 성장률(CAGR) 8.80%로 확대될 것으로 전망됩니다.

장루 관리 제품 시장 점유율은 작지만, 돌출형 기술과 냄새를 억제하는 활성탄 함유 필터 덕분에 평균 판매 가격(ASP)은 높은 수준을 유지하고 있습니다. 2피스식 배액 시스템은 배리어 링을 통해 착용 기간을 최대 7일까지 연장할 수 있어, 배설량이 많은 회장 장루 환자들 사이에서 호평을 받고 있습니다. 세라마이드가 함유된 피부 친화적인 하이드로콜로이드 웨이퍼는 장루 주변 피부염 발생률을 21% 감소시켜, 기존의 PVC 파우치에서 이 제품으로의 전환을 촉진하고 있습니다. 각 업체들은 소아용 파우치에 캐릭터 디자인을 적용한 제품에 투자하고 있으며, 소아기 히르슈스프룽병의 생존율이 향상됨에 따라 이 급성장 중인 마이크로 부문이 확대되고 있습니다.

2025년에는 대장암 수술이 지역 매출의 34.55%를 차지했으며, 이러한 수술과 관련된 유럽의 요실금용 기기 및 장루 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 7.20%를 나타낼 전망입니다. FIT 검사를 통한 선별 검사의 보급으로 조기 발견률은 향상되고 있지만, 수술률은 여전히 높은 수준을 유지하고 있으며, 장루 조성 건수도 변함없이 유지되고 있습니다. 조기 회복 프로토콜에서는 얇은 실리콘 베이스 플레이트가 필수로 규정되어 있어, 이에 따라 일체형 백의 보급이 가속화되고 있습니다.

도시 지역에서 이동 중 발생하는 사고가 끊이지 않는 가운데, 척수 손상 및 신경성 방광 분야는 꾸준한 성장을 기록하고 있습니다. 역류 방지 밸브가 장착된 요로 오스토미용 파우치는 마비 환자의 상행성 감염을 예방합니다. 경요도 전립선 절제술로 치료되는 양성 전립선 비대증의 경우, 수술 후에도 지속형 폴리 카테터가 계속 처방되고 있으나, 간헐적 자가 배뇨 프로그램은 감염 위험을 줄이고 입원 기간을 단축시킵니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the europe incontinence devices and ostomy market size was valued at USD 17.89 billion in 2025 and is estimated to grow from USD 18.71 billion in 2026 to reach USD 23.42 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

This report is Segmented by Product Type (Incontinence Care Products and Ostomy Care Products), Application (Bladder Cancer, and More), End-User (Hospitals and More), by Distribution Channel (Institutional Tender Procurement and More), by Technology / System (Disposable Products and More), and Geography (Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Incontinence Devices And Ostomy Market Trends and Insights

Rising Geriatric and Obese Population

Europe has the world's oldest regional median age, and 34% of citizens aged 65+ report urge or stress incontinence episodes every week. Obesity prevalence passes 22% in Germany and the United Kingdom, and excess abdominal pressure accelerates pelvic-floor weakening that triggers leakage. Urologists prescribe single-use catheters and pads to prevent recurrent urinary tract infections, driving bulk demand in outpatient clinics. Parallel gerontology guidelines recommend early adoption of bowel management pouches for seniors recovering from colorectal surgery, as they can increase ostomy bag volume. As life expectancy stretches to 83 years in Spain, years lived with chronic conditions and disability continue to rise, strengthening the customer base for the European incontinence devices and ostomy market.

Increasing Prevalence of Renal & Urological Disorders

Type 2 diabetes and hypertension increase chronic kidney disease incidence, which now affects 10% of adults in northern Europe. Hemodialysis patients often require intermittent catheterization and high-output urostomy pouches to manage fluid balance between sessions. National health funds reimburse closed-end drainage bags that allow secure night-time urine collection, expanding recurring unit sales. Awareness programs by urological associations encourage primary-care physicians to screen for neurogenic bladder after stroke and channel referrals to specialized continence centers. Device makers partner with dialysis clinics to bundle ostomy accessories with weekly treatment packs, thereby increasing product penetration among end-stage renal disease patients.

Complications & Peristomal Skin Issues with Long-Term Use

Nearly 35% of ostomates experience dermatitis or mucocutaneous separation in the first year post-surgery, raising readmission risk. Chronic leakage corrodes confidence in one-piece bags, fostering hesitation among new patients. Negative experiences circulate on patient forums, lengthening adoption curves in direct-to-consumer channels. Providers must invest in extra nursing hours and hydrocolloid dressing kits, inflating episode-of-care costs for insurers, such as quality-of-life concerns, tempering the rapid expansion of the European incontinence devices and ostomy market.

Other drivers and restraints analyzed in the detailed report include:

- Higher Incidence of Colorectal & Bladder Cancer

- Strong Reimbursement for Chronic Care in Western Europe

- Reimbursement Gaps in Eastern & Southern Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, incontinence care products captured 66.56% of the Europe incontinence devices and ostomy market, supported by large-volume contracts for adult diapers, pads, and intermittent catheters in public hospitals. The prevalence of urge and overflow incontinence among seniors drives procurement toward absorbent underpads that meet EU tensile-strength and biodegradability criteria. Manufacturers leverage plant-based fluff pulp and SAP blends to meet eco-label thresholds without compromising absorbency. The Europe incontinence devices and ostomy market size for disposable pads is now forecast to grow at an 8.80% CAGR through 2031 as aging households and nursing homes prioritize leak-proof nightwear.

Ostomy care products, while smaller in share, exhibit premium ASPs thanks to convexity technology and charcoal-infused filters that curb odor. Two-piece drainable systems are gaining favor among high-output ileostomy patients because barrier rings can prolong wear time up to 7 days. Skin-friendly hydrocolloid wafers with ceramide additives reduce peristomal dermatitis incidence by 21%, boosting switching momentum away from legacy PVC pouches. Vendors invest in pediatric pouches with cartoon imagery, a fast-growing micro-segment as survivorship improves in childhood Hirschsprung disease.

Colorectal cancer surgeries accounted for 34.55% of regional revenue in 2025, and the Europe incontinence devices and ostomy market size associated with these procedures is slated for a 7.20% CAGR during 2026-2031. Enhanced screening uptake via FIT tests boosts early detection, yet surgery rates remain high, sustaining stoma creation volumes. Fast-track recovery protocols mandate low-profile silicone baseplates, accelerating pull-through of one-piece bags.

Spinal cord injury and neurogenic bladder segments record steady growth as urban mobility accidents persist. Urostomy pouches with anti-reflux valves prevent ascending infections in paraplegic patients. Benign prostatic hyperplasia cases treated via trans-urethral resection continue to prescribe indwelling Foley catheters post-operatively, although intermittent self-catheterization programs lower infection risk and cut inpatient stay lengths.

List of Companies Covered in this Report:

- Abena A/S

- Alcare

- Atlantic Therapeutics Group

- Attindas Hygiene Partners

- Axonics Inc.

- B. Braun

- Becton Dickinson & Co. (BD)

- Boston Scientific

- Coloplast

- Convatec

- Essity AB (TENA)

- Hollister

- Johnson & Johnson Services, Inc. (Ethicon)

- Kimberly-Clark Worldwide

- Marlen Manufacturing

- Medtronic

- Ontex Group NV

- Hartmann Group

- Salts Healthcare

- Teleflex

- Unicharm

- Welland Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric and Obese Population

- 4.2.2 Increasing Prevalence of Renal & Urological Disorders

- 4.2.3 Higher Incidence of Colorectal & Bladder Cancer

- 4.2.4 Strong Reimbursement for Chronic Care in Western Europe

- 4.2.5 Shift Toward Tele-Urology & Remote Continence Monitoring

- 4.2.6 EU Circular Economy Pressure Spurring Eco-Friendly Disposables

- 4.3 Market Restraints

- 4.3.1 Complications & Peristomal Skin Issues with Long-Term Use

- 4.3.2 Reimbursement Gaps in Eastern & Southern Europe

- 4.3.3 High Lifetime Cost of Advanced Ostomy Supplies

- 4.3.4 MDR Post-Market Surveillance Raising Compliance Costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Incontinence Care Products

- 5.1.1.1 Absorbent Pads & Underpads

- 5.1.1.2 Intermittent Catheters

- 5.1.1.3 Incontince Bags

- 5.1.1.4 Pelvic-Floor Stimulation & Neuromodulation Devices

- 5.1.2 Ostomy Care Products

- 5.1.2.1 Ostomy Bags

- 5.1.2.1.1 One-piece Systems

- 5.1.2.1.2 Two-piece Systems

- 5.1.2.1.3 Drainable vs Closed-end

- 5.1.2.1.4 High-output & Pediatric Pouches

- 5.1.2.2 Skin Barriers & Seals

- 5.1.2.3 Irrigation & Accessories

- 5.1.2.4 Others

- 5.1.2.1 Ostomy Bags

- 5.1.1 Incontinence Care Products

- 5.2 By Application

- 5.2.1 Bladder Cancer

- 5.2.2 Colorectal Cancer

- 5.2.3 Crohns & Ulcerative Colitis

- 5.2.4 Benign Prostatic Hyperplasia / Post-Prostatectomy

- 5.2.5 Spinal Cord Injury & Neurogenic Bladder

- 5.2.6 Kidney Stone & Chronic Kidney Failure

- 5.2.7 Others

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home-Care Settings

- 5.3.4 Long-term Care & Nursing Homes

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 Institutional Tender Procurement

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies & Subscription Services

- 5.5 By Technology / System

- 5.5.1 Disposable Products

- 5.5.2 Reusable / Eco-friendly Products

- 5.5.3 Smart / Connected Continence & Ostomy Devices

- 5.6 By Region

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abena A/S

- 6.3.2 ALCARE Co. Ltd

- 6.3.3 Atlantic Therapeutics Group

- 6.3.4 Attindas Hygiene Partners

- 6.3.5 Axonics Inc.

- 6.3.6 B. Braun SE

- 6.3.7 Becton Dickinson & Co. (BD)

- 6.3.8 Boston Scientific Corporation

- 6.3.9 Coloplast A/S

- 6.3.10 ConvaTec Group Plc

- 6.3.11 Essity AB (TENA)

- 6.3.12 Hollister Incorporated

- 6.3.13 Johnson & Johnson Services, Inc. (Ethicon)

- 6.3.14 Kimberly-Clark Corporation

- 6.3.15 Marlen Manufacturing & Development

- 6.3.16 Medtronic plc

- 6.3.17 Ontex Group NV

- 6.3.18 Paul Hartmann AG

- 6.3.19 Salts Healthcare Ltd

- 6.3.20 Teleflex Incorporated

- 6.3.21 Unicharm Corporation

- 6.3.22 Welland Medical Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment