|

시장보고서

상품코드

2061593

비뇨기과 의료기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Urology Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

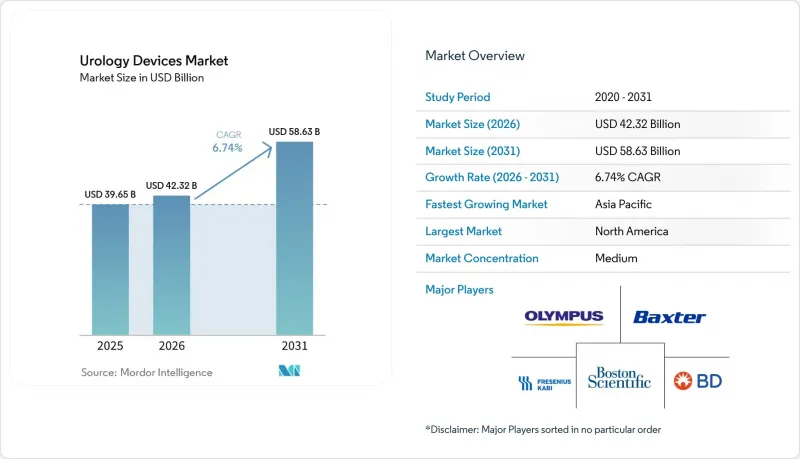

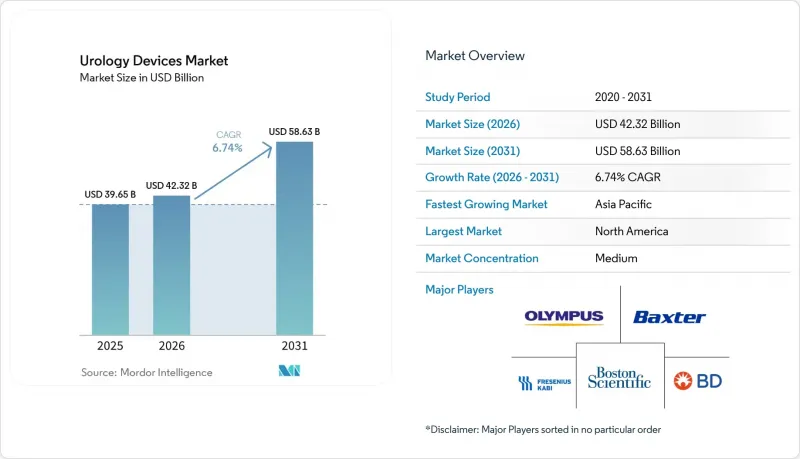

Mordor Intelligence에 의하면, 비뇨기과 의료기기 : 시장 규모는 2025년에 396억 5,000만 달러로 평가되었고, 2026년에 423억 2,000만 달러로 추정되고, 2031년까지 586억 3,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 6.74%로 성장할 것으로 전망됩니다.

본 보고서는 제품별(기기(투석 기기 등), 소모품 및 부속품별(생검 기기 등)), 기술별(저침습 수술용 기기, 로봇 보조 비뇨기과 수술 시스템 등), 질환별(신장 질환, 요로 결석 등), 최종 사용자별(병원 및 클리닉, 투석 센터 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 비뇨기과 의료기기: 시장 동향 및 분석

비뇨기 질환의 높은 유병률

미국에서는 약 4,000만 명의 남성이 신장 결석으로 고통받고 있으며, 이는 체외 충격파 쇄석기 및 일회용 요관경에 대한 지속적인 수요를 뒷받침하고 있습니다. 양성 전립선 비대증은 결국 남성 10명 중 8명에게 영향을 미치며, 최소 침습적 치료의 대상 환자층을 확대시키고 있습니다. 요실금은 약 3,000만 명의 성인에게 영향을 미치고 있으며, 이는 신경 조절 임플란트의 보급을 촉진하고 있습니다. 이러한 질환들은 반복적인 치료와 평생에 걸친 관리가 필요하기 때문에 경제 사이클 전반에 걸쳐 비뇨기과 의료기기 시장을 안정시키는 지속적인 수익원이 되고 있습니다.

고령화의 진행

평균 수명의 연장에 따라, 다인자성 비뇨기과적 문제를 안고 있는 고령자의 비율이 증가하고 있습니다. 의료 시스템 기획 담당자들은 비용 압박을 관리하는 한편, 고령 환자의 단기 입원 수요에 대응하기 위해 수술 건수를 입원 병동에서 외래 진료로 재배분하고 있습니다. 이에 대응하여 제조업체들은 신체 기능이 약한 사용자에게 적합한 기기나 재택 모니터링을 지원하는 기기를 설계함으로써 대응하고 있으며, 이는 비뇨기과 의료기기 시장의 장기적인 성장을 뒷받침하고 있습니다.

세계적인 승인 및 시판 후 조사의 엄격한 요건

FDA가 조만간 시행할 품질 시스템 규정 개정은 ISO 13485를 준수하고 있지만, 제조업체에 문서화 및 감사 관행의 개선을 의무화함에 따라 규정 준수 비용이 증가하고 있습니다. 21 CFR Part 822에 따른 시판 후 조사에서는 장기간에 걸친 추적 조사가 요구되며, 이러한 부담은 중소 혁신 기업들에게 특히 큰 부담이 되고 있습니다. ANVISA와 EU의 유사한 규제 강화로 인해 제품 출시가 지연되면서, 비뇨기과 의료기기 시장의 신규 진출기업 수용 속도가 둔화되고 있습니다.

부문별 분석

2025년 비뇨기과 의료기기 시장에서는 기기가 66.92%를 차지했습니다. 이는 로봇 시스템, 투석 장치 및 툴륨 레이저가 막대한 초기 투자를 필요로 하기 때문입니다. 소모품 및 부속품 시장은 연평균 성장률(CAGR) 8.27%로 성장하고 있습니다. 이는 일회용 요관경이나 카테터가 예측 가능한 재주문 주기를 만들어내기 때문입니다. 내시경용 영상 타워, 분쇄기, 요역동학용 카트는 설비 투자 예산의 핵심을 이루고 있지만, 수익의 예측 가능성은 현재 모든 증례에 대응할 수 있는 일회용 제품으로 이동하고 있습니다. 의료기관이 통합된 영상 진단 및 내비게이션이 필요한 고도로 복잡한 수술을 시행할 경우, 기구의 하위 범주는 여전히 매우 중요합니다. 대용량 혈액투석 여과 시술이 승인된 프레제니우스 5008X와 같은 투석 콘솔은 단계적인 업그레이드가 장비 교체 수요를 유지하고 있음을 보여줍니다. 소모품의 경우, 생분해성 요관 스텐트와 항균 코팅이 재처리 부담을 늘리지 않으면서 각 브랜드의 차별화 요소로 작용하고 있습니다.

이러한 상황에서 비뇨기과 의료기기 시장의 소모품 시장 규모는 특히 1건당 비용의 투명성이 구매자의 선호도에 영향을 미치는 지역에서 더 큰 수익 점유율을 차지할 것으로 전망됩니다. 장비는 절대액 기준으로는 여전히 지배적인 위치를 유지할 것이지만, 대규모 설비 투자에 대한 승인 절차가 예산위원회로 인해 장기화되고 있어 그 성장률은 액세서리의 성장률보다 낮을 것으로 전망됩니다. 구형 홀뮴 YAG 레이저를 보유한 시설에서는 이를 경증 사례에 더 많이 활용하는 한편, 신규 자본을 트륨 플랫폼에 할당하는 경향이 강해지고 있어, 비뇨기과 의료기기 시장 내에서 바벨형 지출 패턴이 두드러지고 있습니다.

2025년 시점에서 비뇨기과 의료기기 시장의 45.71%를 저침습 수술용 기기가 차지했으나, 로봇 시스템은 연평균 성장률(CAGR) 10.31%라는 가장 급격한 성장세를 보이고 있습니다. 메드트로닉의 ‘Hugo’와 같은 신규 진입 제품은 인튜이티브 서지컬 이외의 대안을 고객에게 제공하며, 모듈식 구성 요소를 통해 도입 장벽을 낮추고 있습니다. AI 모듈은 광학 시스템에 컴퓨터 비전을 결합하여 영상 데이터를 실용적인 지침으로 변환함으로써, 학습 기간 단축에 기여하고 있습니다. 소형 초음파 발생기를 통해 시행되는 파쇄술은 비침습적 치료법의 선택지를 더욱 넓혀주고 있으며, 향후 10년 내에 기존의 충격파 시스템을 대체할 가능성이 있습니다.

앞으로 적층 가공 기술을 통해 방출 프로파일이 제어된 생분해성 요관 스텐트 등, 환자 개개인에게 최적화된 임플란트 제작이 가능해질 것입니다. 이미지 AI와 로봇 팔의 통합을 통해 경피적 신장 결석 제거술에서 신우로 진입하는 과정 등이 자동화되어, 효율성이 한층 더 향상될 것으로 예측됩니다. 이러한 기술들의 융합을 통해 비뇨기과 의료기기 시장 전반에 걸친 보급이 더욱 확대되고, 가격 결정력이 유지될 것입니다.

지역별 분석

북미는 견실한 보험 보상, 신속한 규제 승인 절차, 그리고 로봇 플랫폼의 확고한 도입 기반을 바탕으로 2025년에도 세계 시장 점유율 38.76%를 유지했습니다. FDA의 '브레이크스루 디바이스 프로그램'은 버스트파 체외 충격파 쇄석술 등의 기술에 대한 접근을 신속화하고 조기 수익 창출을 가능하게 함으로써, 이를 연구개발(R&D) 예산으로 환원하고 있습니다. 또한 미국에서는 일상적인 진단이 외래 진료 시설로 옮겨가면서, 제조업체 입장에서는 소형 내시경 타워를 도입할 수 있는 새로운 판로가 생겨나고 있습니다. 캐나다와 멕시코에서는 의료기기의 사양을 표준화하고 조달 주기를 단축하는 국경을 초월한 구매 협정을 통해 추가적인 성장이 기대되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 8.86%로 가장 빠르게 성장할 전망입니다. 중국, 일본, 한국의 고령화로 인해 시술 수요가 확대되는 한편, 공공 부문의 개혁을 통해 첨단 레이저 및 영상 진단 장비에 대한 자본 예산이 확보되고 있습니다. 올림푸스는 차세대 전립선 비대증(BPH) 치료 기기의 출시 지역으로 한국을 선정했는데, 이는 다국적 기업들이 해당 지역을 첨단 기술의 검증 무대로 보고 있음을 보여줍니다. 벤처 자금 조달이 위축되면서 기업 가치가 하락하고 있으며, 이는 자본력이 있는 기존 기업의 지역 진출 확대로 이어지는 통합을 촉진할 가능성이 있습니다.

유럽은 성숙한 시장이지만, 정책 주도형이며 환경 규제로 인해 원자재 선택지가 하룻밤 사이에 바뀔 가능성이 있습니다. 예상되는 PFAS(퍼플루오로알킬 물질) 사용 금지는 ePTFE(에틸렌-프로파일렌-테트라플루오로에틸렌) 기반 카테터 및 혈관 이식편 공급업체들에게 과제가 되고 있으며, 이에 따라 불소를 포함하지 않는 코팅 기술에 대한 연구가 가속화되고 있습니다. 독일, 프랑스, 이탈리아는 여전히 수요의 주축을 이루고 있지만, 이 지역 병원들은 대량으로 소비되는 소모품의 가격을 대폭 인하하고 있어, 공급업체들은 부가가치 서비스를 통해 수익률을 확보해야 하는 상황에 놓여 있습니다. 남미에서는 브라질을 필두로 성장의 조짐이 보입니다. 브라질에서는 ANVISA의 전자 라벨화 추진으로 인해 현지화 비용이 감소하고, 수출업체의 규정 준수 부담이 줄어들 가능성이 있습니다. 중동에서는 전문 병원에 대한 투자가 활발한 반면, 많은 아프리카 국가에서는 저비용 투석 및 카테터 치료 솔루션이 우선시되고 있어, 비뇨기과 의료기기 시장에는 다층적인 비즈니스 기회가 창출되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the urology devices market size is projected to be USD 39.65 billion in 2025, USD 42.32 billion in 2026, and reach USD 58.63 billion by 2031, growing at a CAGR of 6.74% from 2026 to 2031.

This report is Segmented by Product (Instruments [Dialysis Devices and More], Consumables & Accessories [Biopsy Devices and More]), Technology (Minimally-Invasive Surgery Devices, Robotic Urologic Surgery Systems and More), Diseases (Kidney Diseases, Urinary Stones, and More), End User (Hospitals & Clinics, Dialysis Centres and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Urology Devices Market Trends and Insights

High Incidence of Urologic Conditions

Kidney stones affect about 40 million men in the United States, underpinning sustained demand for lithotripsy devices and disposable ureteroscopes. Benign prostatic hyperplasia eventually impacts 8 of every 10 men, broadening the addressable base for minimally invasive treatments. Urinary incontinence afflicts roughly 30 million adults, fueling uptake of neuromodulation implants. Because these conditions require repeated or lifelong interventions, they provide recurring revenue streams that stabilize the urology devices market throughout economic cycles.

Rising Geriatric Population

Longer life expectancy is boosting the share of older adults who often present with multifactorial urological issues. Health-system planners are reallocating procedure volumes from inpatient wards to ambulatory settings in order to manage cost pressures while accommodating elderly patients' need for shorter stays . Manufacturers respond by designing devices that suit frail physiology and support at-home monitoring, reinforcing the long-run expansion of the urology devices market.

Stringent Global Approval and Post-Market Surveillance Requirements

The FDA's forthcoming Quality System Regulation amendments align with ISO 13485 but force manufacturers to retrofit documentation and audit practices, raising compliance costs. Post-market surveillance under 21 CFR Part 822 demands long-horizon follow-up studies, a burden that weighs heaviest on small innovators. Similar toughened regimes from ANVISA and the EU delay launches and reduce the pace at which the urology devices market can absorb new entrants.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Minimally Invasive and Robotic Surgery

- Preference for Single-Use Endoscopes and Catheters

- High Capital and Procedure Costs of Advanced Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments account for 66.92% of the urology devices market in 2025 because robotic systems, dialysis machines, and thulium lasers require sizable upfront purchases. Consumables and accessories are growing at an 8.27% CAGR as single-use ureteroscopes and catheters create predictable reorder cycles. Endoscopic visualization towers, lithotripters, and urodynamic carts anchor capital budgets, but revenue predictability now tilts toward disposables that match every case. The instruments subcategory remains pivotal when facilities pursue high-complexity surgeries that demand integrated imaging and navigation. Dialysis consoles like Fresenius 5008X, cleared to deliver high-volume hemodiafiltration, illustrate how incremental upgrades sustain replacement demand. On the consumables side, biodegradable ureteral stents and antimicrobial coatings are differentiating brands without adding reprocessing burdens.

In this context, the urology devices market size for consumables is on track to carve a larger revenue slice, especially in regions where cost-per-procedure transparency drives buyer preference. Instruments will keep dominating absolute value, but their growth rate will trail that of accessories because budget committees lengthen approval cycles for large capital outlays. Facilities that own older holmium YAG lasers increasingly redeploy them to lower-acuity cases while allocating fresh capital to thulium platforms, reinforcing a barbell spending pattern inside the urology devices market.

Minimally invasive surgery devices held 45.71% share of the urology devices market size in 2025, yet robotic systems are producing the steepest curve at a 10.31% CAGR. New entrants such as Medtronic's Hugo are broadening customer choice beyond Intuitive Surgical and, by offering modular components, lowering adoption thresholds. AI modules layer computer vision onto optics, translating video feeds into actionable prompts that help shorten learning curves. Burst wave lithotripsy, delivered via compact ultrasound emitters, is further expanding the non-invasive toolkit and may cannibalize traditional shock-wave systems over the next decade.

Looking ahead, additive manufacturing is enabling patient-specific implants such as biodegradable ureteral stents with controlled elution profiles. Integration between imaging AI and robotic arms is expected to automate sub-steps like calyx entry during percutaneous nephrolithotomy, refining efficiency benchmarks. The convergence of these modalities should deepen overall penetration and protect pricing power across the urology devices market.

Geography Analysis

North America preserved 38.76% global share in 2025 due to robust reimbursement, rapid regulatory pathways, and a well-entrenched installed base of robotic platforms. The FDA's Breakthrough Device Program expedites access for technologies such as burst wave lithotripsy, allowing early revenue capture that feeds back into R&D budgets. The United States is also reallocating routine diagnostics into ambulatory venues, giving manufacturers new channels to place compact endoscopy towers. Canada and Mexico generate incremental growth through cross-border purchasing agreements that standardize device specifications and shorten procurement cycles.

Asia-Pacific is the fastest climber with a 8.86% CAGR through 2031. Aging populations in China, Japan, and South Korea expand procedure demand while public-sector reforms unlock capital budgets for advanced lasers and imaging. Olympus chose South Korea to launch next-generation BPH devices, a sign that multinational firms view the region as a proving ground for premium technologies. Venture financing pullbacks have lowered valuations, which may spur consolidation that helps well-capitalized incumbents accumulate regional footprints.

Europe is a mature but policy-driven market in which environmental legislation can reshape material choices overnight. The anticipated PFAS prohibition challenges suppliers of ePTFE-based catheters and vascular grafts, prompting accelerated research into fluorine-free coatings. Germany, France, and Italy remain demand anchors, yet hospitals here are steeply discounting high-volume consumables, pushing vendors to extract margin from value-added services. South America holds pockets of growth led by Brazil, where ANVISA's e-labeling push may lower localization costs, easing compliance for exporters. The Middle East invests heavily in specialist hospitals while many African states prioritize low-cost dialysis and catheterization solutions, presenting tiered opportunities for the urology devices market.

- Baxter

- Boston Scientific

- Beckton Dickinson

- Cook Group

- Stryker

- Fresenius

- Intuitive Surgical

- Karl Storz

- Medtronic

- Olympus

- Coloplast

- Teleflex

- Cardinal Health

- Siemens Healthineers

- Dornier MedTech

- Richard Wolf

- Lumenis

- ConvaTec Group plc

- Terumo

- HuiZhou MIMED Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Incidence Of Urologic Conditions

- 4.2.2 Rising Geriatric Population

- 4.2.3 Technological Advancements In Minimally-Invasive & Robotic Surgery

- 4.2.4 Preference For Single-Use Endoscopes & Catheters

- 4.2.5 AI-Enabled Imaging & Navigation Improving Procedural Throughput

- 4.2.6 Home-Based Dialysis & Self-Catheterization Enabled By Tele-Urology

- 4.3 Market Restraints

- 4.3.1 Stringent Global Approval & Post-Market Surveillance Requirements

- 4.3.2 High Capital & Procedure Costs Of Advanced Systems

- 4.3.3 Sustainability Pressure On Single-Use Plastics & PFAS Coatings

- 4.3.4 Shortage Of Trained Urology Surgeons & Nurses In Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.1.1 Dialysis Devices

- 5.1.1.2 Endoscopes & Endovision Systems

- 5.1.1.3 Lasers & Lithotripsy Devices

- 5.1.1.4 Robotic Surgical Systems

- 5.1.1.5 Urodynamic Systems

- 5.1.1.6 Imaging & Navigation Devices

- 5.1.1.7 Bladder Management Devices

- 5.1.1.8 Other Instruments

- 5.1.2 Consumables & Accessories

- 5.1.2.1 Dialysis Consumables

- 5.1.2.2 Guidewires & Urinary Catheters

- 5.1.2.3 Stents (Ureteral & Urethral)

- 5.1.2.4 Biopsy Devices

- 5.1.2.5 Disposable Ureteroscopes

- 5.1.2.6 Continence Care Products

- 5.1.2.7 Other Consumables & Accessories

- 5.1.1 Instruments

- 5.2 By Technology

- 5.2.1 Minimally-Invasive Surgery Devices

- 5.2.2 Robotic Urologic Surgery Systems

- 5.2.3 AI-enabled Imaging & Navigation

- 5.2.4 3-D Printed & Patient-specific Implants

- 5.2.5 Other Emerging Technologies

- 5.3 By Disease

- 5.3.1 Kidney Diseases

- 5.3.2 Urological Cancer & BPH

- 5.3.3 Urinary Stones (Urolithiasis)

- 5.3.4 Pelvic Organ Prolapse

- 5.3.5 Urinary Incontinence

- 5.3.6 Other Diseases

- 5.4 By End-User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Dialysis Centres

- 5.4.3 Ambulatory Surgical Centres

- 5.4.4 Home-care Settings

- 5.4.5 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Baxter International Inc.

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Cook Medical Incorporated

- 6.3.5 Stryker Corporation

- 6.3.6 Fresenius Medical Care AG & Co. KGaA

- 6.3.7 Intuitive Surgical Inc.

- 6.3.8 KARL STORZ SE & Co. KG

- 6.3.9 Medtronic plc

- 6.3.10 Olympus Corporation

- 6.3.11 Coloplast A/S

- 6.3.12 Teleflex Incorporated

- 6.3.13 Cardinal Health Inc.

- 6.3.14 Siemens Healthineers AG

- 6.3.15 Dornier MedTech GmbH

- 6.3.16 Richard Wolf GmbH

- 6.3.17 Lumenis Ltd.

- 6.3.18 ConvaTec Group plc

- 6.3.19 Terumo Corporation

- 6.3.20 HuiZhou MIMED Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment